EPF Calculator: Best Ways to Plan Your PF Retirement Corpus 2026

Most salaried employees in India know that a portion of their salary goes to PF every month — but very few actually know how much that adds up to by retirement. That’s exactly what an EPF calculator tells you. “pair your EPF with a ₹100 per day SIP investment for faster wealth” The Employee Provident Fund is one of India’s most powerful retirement savings tools, and the numbers are better than most people expect. With an 8.25% interest rate for FY 2025-26, guaranteed by the government, EPF calculator consistently beats most fixed deposits and savings accounts — and the money compounds tax-free up to defined limits.

This guide explains how to use the EPF calculator, how PF contribution is calculated for both employees and employers, what the EPS pension component is, how interest is computed, when you can withdraw, what the tax rules are, and how to maximise your PF corpus before retirement. Use MoneyOra’s free EPF calculator to estimate your exact PF balance at retirement in seconds. Common EPF mistakes for freshers

What is EPF (Employee Provident Fund)?

The Employees’ Provident Fund is a mandatory retirement savings scheme governed by the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. It is managed by the Employees’ Provident Fund Organisation (EPFO), one of the world’s largest social security organisations by membership. “how EPF fits into your salary investment plan”

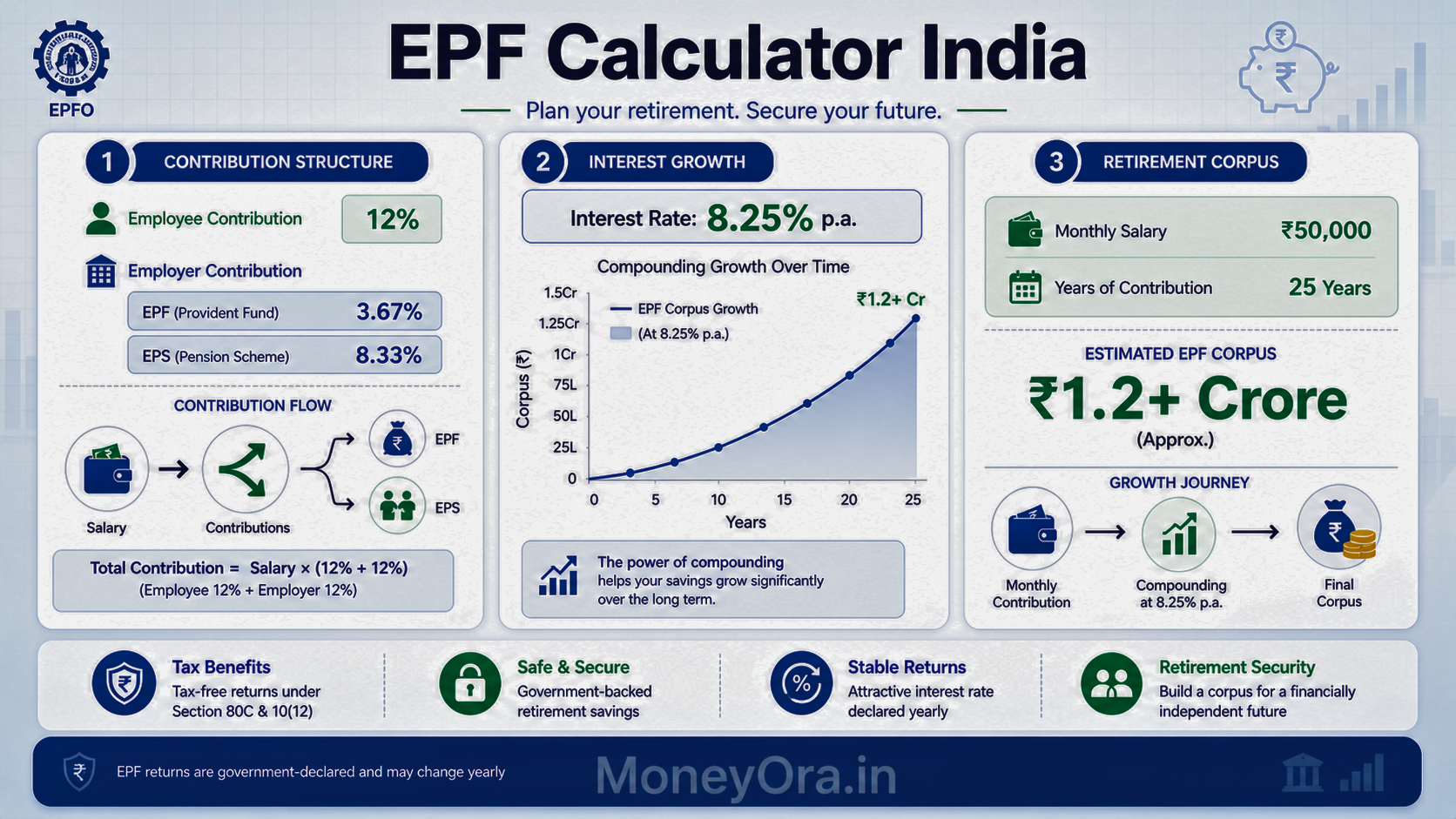

Here’s the basic structure. Every month, 12% of your basic salary plus Dearness Allowance (DA) is deducted and deposited into your EPF account. Your employer matches this with another 12%. That means 24% of your basic salary goes toward your retirement fund every single month — though the employer’s 12% is split between EPF and EPS (we’ll come to that shortly).

EPF is mandatory for:

- All organisations with 20 or more employees

- Employees earning a basic salary up to Rs 15,000/month (mandatory coverage)

- Employees earning above Rs 15,000 can be covered voluntarily by employer agreement

According to Wikipedia’s article on EPFO, the organisation manages a corpus of tens of lakhs of crore rupees and covers over 7 crore active members — making it one of the largest provident fund organisations in the world. Every employee in the formal sector builds their retirement corpus through this scheme, whether they actively think about it or not.

What makes EPF calculator stand out from other savings schemes is the combination of guaranteed returns (no market risk), tax-free compounding (up to defined limits), and the employer contribution — which is essentially free money added to your retirement account every month.

“EPF calculator combines steady contributions with compounding interest, making it one of the most powerful long-term retirement tools in India.”

How the EPF calculator works

The EPF calculator takes five inputs and gives you one very useful output: how much money you’ll have in your PF account when you retire.

What you enter in the EPF calculator

- Basic monthly salary + DA — the base on which EPF is calculated (not the total CTC)

- Your current age — to determine how many years of service remain until retirement at 58

- Your EPF contribution % — typically 12%, but can be higher if you’re contributing to VPF

- Annual salary increment % — accounts for salary growth over your career (typically 5-10%)

- EPF interest rate — 8.25% for FY 2025-26 (pre-filled in most calculators)

What the EPF calculator shows you

- Total employee contribution over career

- Total employer contribution to EPF (3.67% portion only — EPS is separate)

- Total interest earned on the accumulated balance

- Final EPF corpus at retirement age (58)

One important clarification: the EPF calculator shows the EPF corpus only — not the EPS pension amount. EPS gives you a monthly pension after retirement, not a lump sum. The EPF portion is what you can withdraw as a lump sum when you retire or become unemployed for 2+ months.

Use MoneyOra’s EPF calculator online right now — it’s free, takes under a minute, and shows a year-by-year projection of your PF balance growth.

EPF calculation formula with worked example

Let’s walk through the full EPF calculation step by step. This is exactly what the PF calculator does automatically.

EPF contribution formula

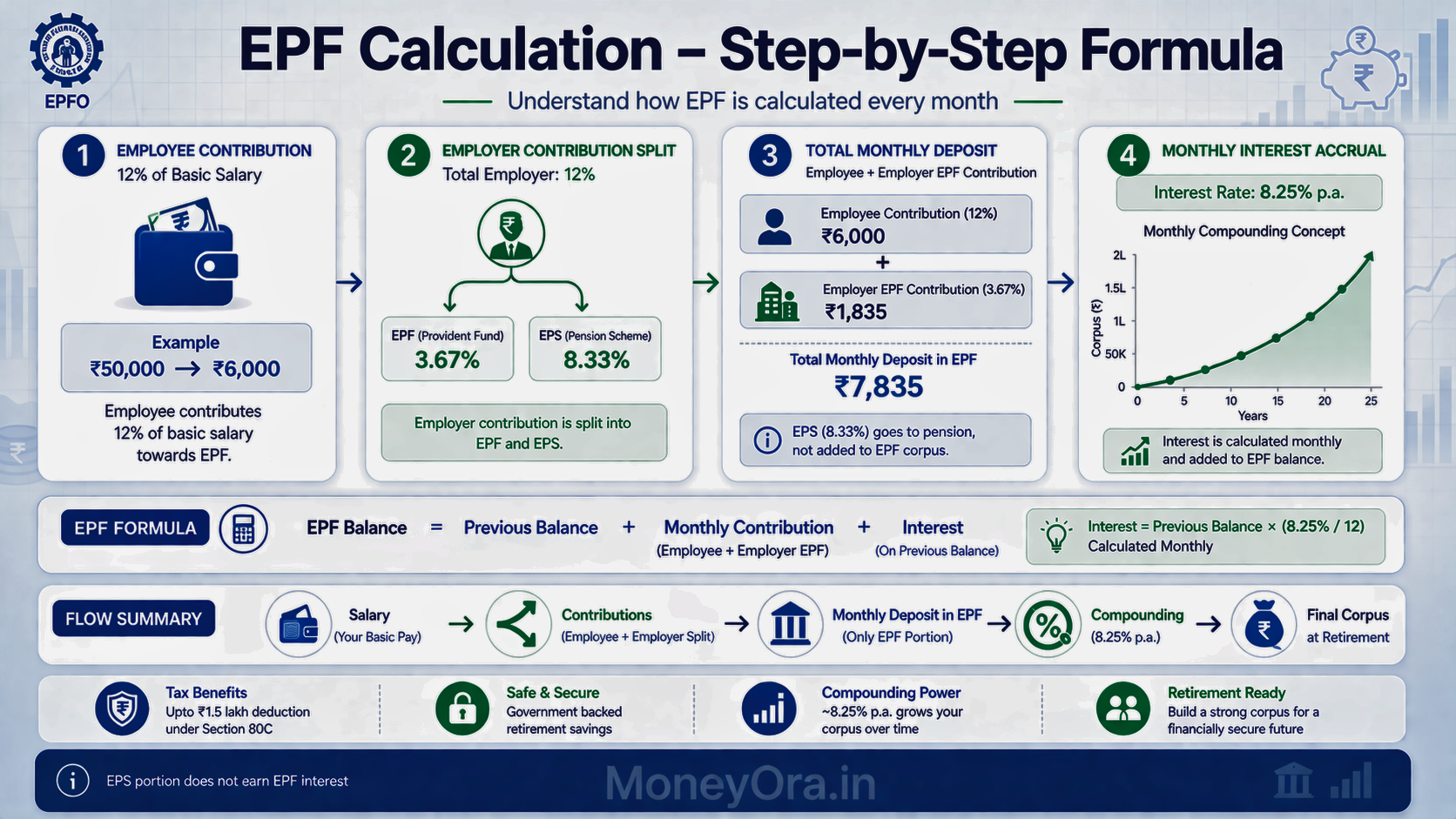

Employee EPF contribution = 12% × (Basic Salary + DA)

Employer EPF contribution = 3.67% × (Basic Salary + DA)

Employer EPS contribution = 8.33% × (Basic Salary + DA) — capped at Rs 1,250/month

Total monthly EPF deposit = Employee (12%) + Employer EPF (3.67%)

Monthly interest = Running EPF balance × (8.25% ÷ 12)

Worked example — Basic salary Rs 30,000/month

Step 1: Monthly contributions

- Employee contribution: 12% × Rs 30,000 = Rs 3,600

- Employer EPF contribution: 3.67% × Rs 30,000 = Rs 1,101

- Employer EPS contribution: 8.33% × Rs 15,000 (wage ceiling) = Rs 1,250 (not part of EPF corpus)

- Total monthly EPF deposit: Rs 3,600 + Rs 1,101 = Rs 4,701

Step 2: First-year interest (simplified)

- Month 1: Deposit Rs 4,701. No interest (joining month)

- Month 2: Balance Rs 9,402 × 0.6875% (monthly rate) = Rs 64.64 interest

- This continues each month — rising balance earns more interest every month

- All monthly interest accrues but is credited to account at year-end (March 31)

Step 3: 30-year projection (10% annual salary increment, 8.25% interest)

| Year | Monthly Basic Salary | Monthly EPF Deposit | EPF Balance (approx.) |

|---|---|---|---|

| Year 1 | Rs 30,000 | Rs 4,701 | Rs 58,000 |

| Year 5 | Rs 43,923 | Rs 6,883 | Rs 5.2 lakh |

| Year 10 | Rs 70,781 | Rs 11,092 | Rs 17.8 lakh |

| Year 20 | Rs 1,83,724 | Rs 28,783 | Rs 95 lakh |

| Year 30 | Rs 4,76,988 | Rs 74,761 | Rs 3.2 crore+ |

That Rs 3.2 crore figure for a person who started at Rs 30,000 basic salary with 10% annual increments shows the power of EPF compounding over 30 years. The interest-on-interest effect is enormous by year 20 onwards.

Run your own exact numbers using MoneyOra’s PF calculator. You can also use the CAGR calculator to check what compounded annual growth rate 8.25% produces over your specific career tenure — the result is usually more impressive than people expect.

“Understanding the EPF contribution split and compounding formula helps you estimate your real retirement corpus more accurately.”

EPF interest rate 2025-26 — 8.25% explained

The EPF interest rate for FY 2025-26 is 8.25% per annum — unchanged from FY 2024-25. This rate was confirmed by EPFO’s Central Board of Trustees in consultation with the Ministry of Finance.

How EPF interest is calculated

Interest is calculated monthly but credited annually. This is a common source of confusion.

Every month, EPFO calculates interest on the closing balance at 0.6875% (8.25% ÷ 12). This monthly interest accrues but does not appear in your passbook immediately. At the end of the financial year (March 31), all accumulated monthly interest is credited to your account in one go. In practice, the credit usually shows up in the EPFO passbook between July and September.

This monthly calculation actually benefits you. Interest is computed on the month-end balance — so as your balance grows each month from new contributions, the interest base expands. It’s effectively monthly compounding with annual crediting.

EPF interest rate history

| Financial Year | EPF Interest Rate |

|---|---|

| FY 2025-26 | 8.25% |

| FY 2024-25 | 8.25% |

| FY 2023-24 | 8.25% |

| FY 2022-23 | 8.15% |

| FY 2021-22 | 8.10% |

| FY 2020-21 | 8.50% |

| FY 2019-20 | 8.50% |

| FY 2018-19 | 8.65% |

Even in years when bank FD rates dropped to 5–6%, EPF held at 8.10–8.50%. That consistency is one of EPF’s most underappreciated features. For a comparison, check MoneyOra’s FD calculator — most bank FDs for equivalent durations offer significantly lower net returns especially after tax.

The official EPF interest rate announcements are published on the EPFO’s official website at epfindia.gov.in. Check there after each financial year’s announcement for the latest confirmed rate before updating your EPF calculator inputs.

EPF vs EPS — what goes where in your account

This is the most misunderstood part of PF. Many employees assume their employer’s full 12% goes into EPF. It doesn’t. Here’s exactly how the employer’s 12% is split.

Employer’s 12% contribution breakdown

- 3.67% → goes into your EPF account (the lump-sum withdrawable amount)

- 8.33% → goes into EPS (Employee Pension Scheme), capped at Rs 1,250/month

- 0.50% → goes to EDLI (Employees’ Deposit Linked Insurance — life insurance)

- 0.50% → goes to EPFO administration charges

The EPS component funds your monthly pension after retirement — but it is not part of the lump-sum EPF corpus that the EPF calculator projects. It’s a separate benefit entirely.

What this means in rupees

For a basic salary of Rs 30,000/month:

- Employee contribution to EPF: Rs 3,600

- Employer contribution to EPF: Rs 1,101 (3.67%)

- Employer contribution to EPS: Rs 1,250 (8.33% of Rs 15,000 ceiling — not Rs 30,000)

- Monthly EPF deposit (what earns 8.25% interest): Rs 3,600 + Rs 1,101 = Rs 4,701

The EPF wage ceiling for EPS is Rs 15,000. Even if your basic salary is Rs 1 lakh, the maximum EPS contribution is 8.33% of Rs 15,000 = Rs 1,250. Anything above Rs 15,000 in your employer’s contribution gets routed to EPF instead. This benefits higher-salary employees — a larger proportion of their employer’s 12% goes to EPF (lump sum) rather than EPS (pension).

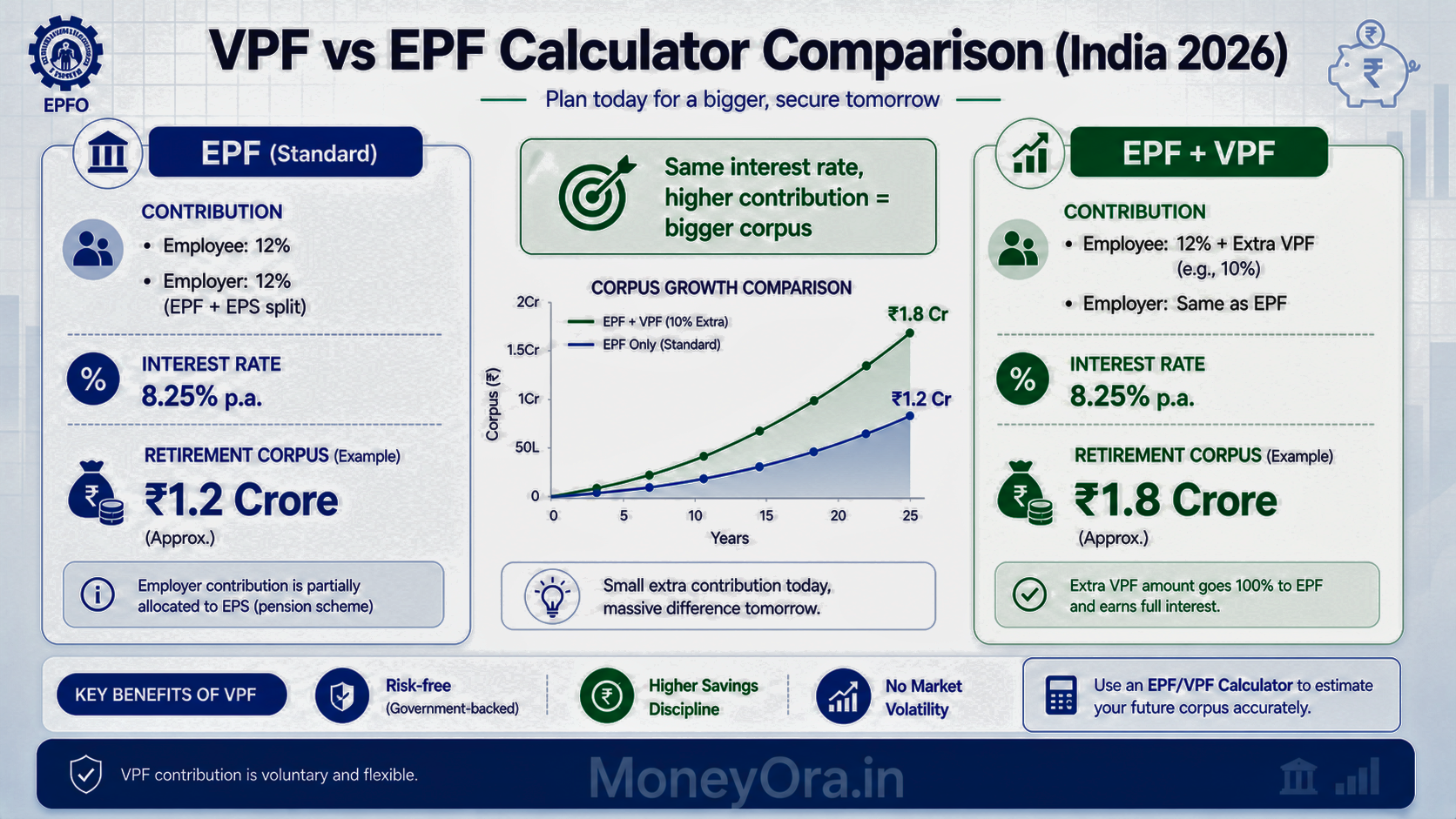

VPF calculator — contributing more than 12%

The Voluntary Provident Fund (VPF) allows you to contribute more than the mandatory 12% to your PF account. VPF earns the exact same 8.25% interest as EPF and is treated identically for tax purposes.

Why VPF makes sense

At 8.25% guaranteed return with tax-free compounding (up to Rs 2.5 lakh annual contribution), VPF competes favourably against most debt instruments. There are very few investments that offer government-guaranteed 8.25% returns with zero market risk — and VPF is one of them.

VPF contribution example

Employee with Rs 50,000 basic salary:

- Mandatory EPF: 12% × Rs 50,000 = Rs 6,000/month = Rs 72,000/year

- VPF extra contribution: 10% × Rs 50,000 = Rs 5,000/month = Rs 60,000/year

- Total annual PF contribution: Rs 72,000 + Rs 60,000 = Rs 1,32,000/year — fully within the Rs 2.5 lakh tax-free limit

- All interest earned remains tax-free

VPF limit for tax-free interest

If your total employee PF contribution (EPF + VPF) exceeds Rs 2.5 lakh per year, interest on the excess becomes taxable as income from other sources. TDS applies at your slab rate. Most salaried employees stay well below this threshold — only those with very high salaries or large VPF top-ups cross it.

To see how VPF compares to other tax-saving instruments: the PPF calculator shows returns on Public Provident Fund (7.1% currently, also tax-free up to Rs 1.5L/year), and the NPS calculator shows National Pension System projections. Each has a different risk-return-tax profile — worth comparing before deciding where to put extra retirement savings.

“VPF allows you to increase your EPF contributions at the same interest rate, significantly boosting your retirement corpus without additional risk.”

EPF withdrawal rules — when and how much

EPF is designed as a long-term retirement instrument. But EPFO does allow withdrawals in specific situations — both partial and full.

Full EPF withdrawal

You can withdraw your full EPF balance (employee contribution + employer EPF contribution + interest) in two situations:

- At retirement — when you reach age 58

- After 2 consecutive months of unemployment — regardless of age

Partial EPF withdrawal — allowed purposes

| Purpose | Minimum service required | Maximum withdrawal amount |

|---|---|---|

| Medical emergency (self or family) | No minimum | 6 months basic salary or employee’s share + interest (lower of two) |

| Marriage (self, sibling, children) | 7 years | 50% of employee’s EPF share |

| Education (post-10th) | 7 years | 50% of employee’s EPF share |

| Home loan repayment | 5 years | 90% of total EPF balance |

| House purchase / construction | 5 years | 24 months basic salary + DA or total EPF (lower) |

| House renovation | 5 years (can apply twice) | 12 months basic salary or employee’s EPF share (lower) |

| Natural calamity / disaster | No minimum | Up to 3 months basic salary |

As of 2025, EPFO 3.0 is introducing PF-linked ATM cards that allow instant partial withdrawals (up to 50-75% of balance) for approved purposes without filing a claim form — making EPF more accessible during emergencies. This is still being rolled out but represents a significant upgrade to the withdrawal system.

If you’re considering using EPF for home loan repayment, pair this with MoneyOra’s home loan EMI calculator to see how a lump-sum EPF contribution toward principal affects your remaining loan term and total interest paid.

EPF tax rules — what’s exempt and what’s not

EPF is often called an EEE (Exempt-Exempt-Exempt) instrument, but that description has changed in recent years. Here’s the accurate tax picture.

Tax on EPF contribution (at investment stage)

Employee contributions to EPF qualify for deduction under Section 80C, up to Rs 1.5 lakh per year. This reduces your taxable income — so if you’re in the 30% slab, the Rs 1.5L 80C deduction saves Rs 45,000 in tax.

Tax on EPF interest (while accumulating)

This changed in Budget 2021. From FY 2021-22 onwards:

- Interest on EPF contributions up to Rs 2.5 lakh/year remains tax-free

- Interest on contributions above Rs 2.5 lakh/year is taxable at slab rate

- For employees without employer contribution (VPF only): tax-free limit is Rs 5 lakh/year

The Rs 2.5 lakh limit is only an issue for high earners. At Rs 30,000 basic salary, your annual EPF contribution is Rs 43,200 — well below the threshold. You’d need a basic salary above Rs 1.74 lakh/month before crossing the Rs 2.5 lakh annual limit.

Tax on EPF withdrawal

- If you’ve completed 5 continuous years of service: EPF withdrawal is fully tax-free

- If you withdraw before 5 years of service: TDS at 10% (PAN furnished) or 34.608% (no PAN) applies

- Employer’s contribution is added to income and taxed if withdrawn before 5 years

- At retirement (after 5 years): full withdrawal is tax-free — this is the EEE benefit that still stands

For most salaried employees who stay in the formal sector for 5+ years, EPF remains essentially EEE — contribution deducted from tax, accumulation tax-free, withdrawal tax-free. The only caveat is the Rs 2.5 lakh limit on tax-free interest for very high earners.

The Income Tax India portal has the latest rules on Section 80C deductions and EPF taxation — worth checking each budget year as rules can change.

How to check EPF balance — EPFO portal and UMANG

Your EPF balance is accessible through multiple channels. Here are all the ways to check it.

1. EPFO Member Portal (most detailed)

Go to epfindia.gov.in → Member e-Sewa → Passbook. Log in with your UAN and password. The passbook shows month-by-month contributions from employee and employer, plus annual interest credits. This is the most detailed view — useful for spotting missed contributions.

2. UMANG App

Download UMANG (Unified Mobile Application for New-age Governance) from the App Store or Play Store. Navigate to EPFO → Employee Centric Services → View Passbook. Same passbook data as the web portal, accessible on mobile.

3. Missed call (quickest)

Give a missed call to 9966044425 from your registered mobile number. EPFO sends an SMS with your current balance within seconds. This works only if your UAN is activated and mobile number is registered.

4. SMS

Send EPFOHO UAN ENG to 7738299899 from your registered mobile. You receive your EPF balance and last contribution details as an SMS.

5. Employer portal / Salary slip

Many employers now show EPF contributions on the monthly salary slip. The employee and employer contributions for each month are visible there. For full balance including interest, use the EPFO portal.

One thing to watch for: if your passbook shows a month where employer contribution is missing, contact your HR department immediately. Delayed or missed employer contributions cost you interest for that month and may indicate compliance issues at the company level.

What happens to EPF when you change jobs

Job changes are where most EPF planning errors happen. Here’s what you should and should not do.

Transfer EPF — don’t withdraw it

When you change jobs, transfer your EPF balance to your new employer’s account using Form 13 on the EPFO member portal. Your UAN stays the same across all jobs — only the PF account number changes. The UAN links all accounts under one umbrella.

Why transferring is important: every EPF account that’s left idle at an old employer stops receiving contributions. After 36 months of no contributions, the account becomes inoperative. Inoperative accounts still earn interest for 3 years post-inactivity, but then interest stops. Multiple idle PF accounts from multiple jobs are a common and costly mistake.

Never withdraw EPF on job change (unless absolutely necessary)

This is the single biggest EPF mistake Indian employees make. Withdrawing EPF at each job change breaks the compounding chain and triggers TDS. Here’s why it hurts so much:

Rs 5 lakh in EPF withdrawn at age 30, instead of being left to compound at 8.25% for 28 more years, would have grown to approximately Rs 43 lakh by retirement. That one premature withdrawal costs Rs 38 lakh in future retirement corpus.

The transfer process through the EPFO portal takes 10–15 days and is done entirely online — there’s no reason to withdraw just for the sake of convenience.

TDS rules on withdrawal before 5 years

If you’ve been employed for less than 5 continuous years (including service at previous employer if EPF was transferred) and withdraw:

- TDS at 10% if PAN is furnished

- TDS at 34.608% if PAN is not furnished

- Employer’s contribution becomes taxable income

- Previously claimed 80C deductions are reversed

The 5-year count includes all service periods where EPF was transferred — it’s continuous employment in the EPF system, not just one employer.

EPF vs PPF vs NPS — which is better for retirement?

This is one of the most searched retirement planning questions in India. The honest answer is: all three work together, not as alternatives. But let’s compare them directly.

| Feature | EPF | PPF | NPS |

|---|---|---|---|

| Current interest / return | 8.25% (FY 2025-26) | 7.1% (Q1 FY 2025-26) | 10-12% (market-linked, not guaranteed) |

| Return type | Guaranteed by govt | Guaranteed by govt | Market-linked (equity + debt mix) |

| Who can invest | Salaried employees (formal sector) | Anyone (including self-employed) | Anyone (Indian citizen, 18-70) |

| Annual investment limit | No upper limit (12% mandatory, VPF unlimited) | Rs 500 to Rs 1.5 lakh/year | No upper limit (tax benefit capped at Rs 2L) |

| Lock-in period | Until retirement / job exit conditions | 15 years (partial from year 7) | Until age 60 (partial exits allowed) |

| Withdrawal at maturity | 100% lump sum (tax-free after 5 years) | 100% lump sum (tax-free) | 60% lump sum + 40% mandatory annuity |

| Tax on interest | Tax-free up to Rs 2.5L/year contribution | Fully tax-free | Corpus growth: not taxed annually |

| 80C benefit | Yes (employee contribution) | Yes (up to Rs 1.5L) | 80CCD(1): Rs 1.5L + 80CCD(1B): Rs 50K extra |

| Employer contribution | Yes — 3.67% EPF + 8.33% EPS | No | Yes (10% of basic for central govt) |

| Partial withdrawal | Yes (specific purposes) | Yes (from year 7, limited) | Yes (after 3 years, specific purposes) |

Use MoneyOra’s PPF calculator and NPS calculator alongside the EPF calculator to model your total retirement corpus from all three sources. Most salaried employees end up with EPF as the mandatory foundation, PPF as a voluntary tax-free supplement, and NPS for additional equity exposure in retirement savings.

Pro tips to maximise your EPF corpus

- Use the EPF calculator with your actual basic salary (not CTC) and include a realistic salary increment rate. Most people underestimate their salary growth — even 8% annual increment makes a large difference over 25-30 years.

- Add VPF if you’re in the 30% tax bracket and have maxed out Section 80C with other instruments. VPF at 8.25% tax-free beats most debt mutual funds and corporate FDs on a post-tax basis at higher income levels.

- Never withdraw EPF for a car loan, personal loan, or non-emergency use. The opportunity cost is massive — money withdrawn at 35 costs you 23+ years of compounding at 8.25%.

- Check that your employer’s EPF contributions are deposited on time. EPFO mandates contributions by the 15th of the following month. Consistent delays by employers are a compliance violation you can report to EPFO.

- Transfer EPF immediately when changing jobs — don’t wait months. Idle accounts lose contributions (from the new employer) and can become complicated to consolidate later.

- Compare your EPF projection against expenses using MoneyOra’s tools. The SWP calculator can show you what monthly income your EPF lump sum generates if invested in a mutual fund post-retirement. The lumpsum calculator shows what EPF corpus grows to if reinvested.

- Use the EPF withdrawal provisions strategically — the home loan repayment provision (up to 90% after 5 years) is genuinely useful and avoids taking a separate personal loan at higher interest. Compare with MoneyOra’s personal loan EMI calculator to see the interest cost difference before deciding.

- Review your retirement plan annually. Run the EPF calculator each April with your updated salary, then check if the projected corpus is sufficient against expected retirement expenses. If not, adjust VPF contribution or SIP amount accordingly.

Common mistakes with EPF planning

These errors cost Indian employees lakhs of rupees in retirement corpus — and they’re all avoidable.

1. Withdrawing EPF on every job change

Already covered above — but worth repeating because it’s so common. Each withdrawal resets your compounding clock to zero and triggers TDS. Transfer, don’t withdraw.

2. Not tracking employer contributions

Many employers delay or occasionally miss EPF deposits. Every missing month costs you both the contribution amount and the interest on that amount. Check your EPFO passbook quarterly. If a month is missing, raise it with HR — and if HR doesn’t act, escalate to EPFO directly through their grievance portal.

3. Not activating UAN

Your UAN (Universal Account Number) is the master number that links all your EPF accounts. Without UAN activation, you can’t access your passbook, claim status, or transfer requests online. Activate your UAN at unifiedportal-mem.epfindia.gov.in the moment you join a new employer.

4. Not nominating a beneficiary

If you die without a nominee on your EPF account, your family has to go through a lengthy legal process to claim the balance. Submit Form 2 (nomination form) to your employer when you join. Update it when you marry or have children.

5. Not considering the EPS pension component

Many employees forget that 8.33% of the employer’s contribution goes to EPS, not EPF. This means their EPF corpus at retirement will be lower than expected if they calculated assuming the full 12% employer contribution goes to EPF. The EPF calculator on MoneyOra correctly handles this split — always use it rather than manual estimates.

6. Treating EPF as primary retirement corpus without planning additional investments

EPF is excellent, but for most salaried Indians, EPF alone is not enough for a comfortable retirement — especially if they start careers at Rs 20,000-30,000 basic salary. Plan additional retirement savings through SIP, PPF, or NPS. Use the SIP calculator to see how even Rs 5,000/month in a mutual fund SIP supplements EPF corpus over 20-30 years.

7. Not updating KYC on EPFO portal

Without KYC linking (Aadhaar + bank account + PAN) on the EPFO portal, online EPF claims and withdrawals face delays or rejections. Complete this once and update it if bank account details change.

How EPF fits into your complete retirement and financial plan

EPF is the foundation. For most salaried Indians, it’s the largest guaranteed savings pool they build over a career. But it works best as one piece of a larger plan.

For debt management alongside EPF savings: the EMI calculator, home loan EMI calculator, and car loan EMI calculator show monthly cash commitments clearly. High-interest consumer loans often cost more than EPF earns — clearing those first is usually the right call before adding VPF.

For wealth building beyond EPF: the SIP calculator and lumpsum calculator model equity mutual fund growth. The PPF calculator shows guaranteed returns from Public Provident Fund. The RD calculator models recurring deposit growth. Together, these give a multi-pillar retirement savings picture.

For investors who also trade stocks alongside long-term EPF savings: the stock return calculator, dividend calculator, PE ratio calculator, and stop loss calculator help manage the equity trading side. The brokerage calculator shows exact trading costs. And for options traders, the option price calculator and position size calculator complete the risk management toolkit.

For banking utility needs — verifying bank account details when linking your bank to EPFO for withdrawal — MoneyOra’s IFSC code finder and bank details finder are quick tools that save a branch visit.

Conclusion

EPF is probably the most underestimated financial instrument available to Indian salaried employees. It’s mandatory so people tend to treat it as background noise — money that disappears from the salary slip and reappears someday at retirement. But when you actually run the numbers through the EPF calculator, the corpus projection at retirement is often the largest single financial asset an average employee will accumulate in their lifetime.

The key things to apply from this guide: never withdraw EPF on a job change, transfer it instead. Add VPF if you’re in a high tax bracket and want guaranteed 8.25% tax-free returns. Check your EPFO passbook quarterly to confirm employer contributions are landing on time. And run the PF calculator with realistic salary growth projections — not just your current salary.

Use MoneyOra’s free EPF calculator to project your retirement corpus today. Change the salary growth rate, try adding VPF, and see what 30 years of compounding at 8.25% looks like on your specific numbers. Then pair it with the PPF calculator and SIP calculator to build a complete retirement plan across all three pillars.

Your retirement corpus starts with knowing your numbers — calculate yours free on MoneyOra.

Frequently Asked Questions About EPF Calculator

An EPF calculator estimates your PF balance.

It shows total retirement corpus.

You enter salary, age, and contribution.

It includes employee and employer share.

It also adds interest over time.

The EPF interest rate is 8.25% per year.

It is set by EPFO.

Monthly rate is 0.6875%.

Interest is credited yearly.

Credit date is March 31.

Employee contributes 12% of Basic + DA.

Employer contributes 12% total.

3.67% goes to EPF.

8.33% goes to EPS.

EPS is capped at ₹1,250/month.

Interest is calculated monthly.

It is credited annually.

Employer contributes 12% of Basic + DA.

Only 3.67% goes to EPF.

Remaining 8.33% goes to EPS.

EPS has ₹1,250 monthly cap.

EPS is separate from EPF corpus.

Yes, partial withdrawals are allowed.

Medical emergencies have no minimum service.

Marriage or education needs 7 years service.

Home-related withdrawals need 5 years.

Full withdrawal allowed after unemployment.

Also allowed at retirement age.

EPF interest is mostly tax-free.

Limit is ₹2.5 lakh yearly contribution.

Above this, interest becomes taxable.

Tax applies as per slab rate.

Most salaried employees stay below limit.

VPF is voluntary contribution.

It is above mandatory 12% EPF.

It earns same 8.25% interest.

Tax rules are same as EPF.

Higher contributions may become taxable.

EPF builds a lump sum corpus.

EPS provides monthly pension.

EPS is funded by employer contribution.

It is not part of EPF balance.

It is separate retirement benefit.

Use EPFO website for detailed info.

Use UMANG app for mobile access.

Missed call gives instant balance.

SMS also provides details.

Transfer EPF to new employer.

Use Form 13 online.

Your UAN remains same.

Avoid withdrawing PF.

Withdrawal breaks compounding.

It reduces long-term corpus.