SWP Calculator

Systematic Withdrawal Plan — calculate monthly income from your mutual fund corpus, how long it lasts & returns earned.

| Year | Opening Corpus | Returns | Withdrawal | Closing Corpus |

|---|

SWP Calculator: 5 Best Ways to Plan Monthly Income in 2026

Most people spend 30–35 years building a retirement corpus. But very few have a clear plan for drawing it down. That’s exactly where an SWP calculator helps. A Systematic Withdrawal Plan lets you invest a lumpsum in a mutual fund and receive a fixed amount every month — without selling the whole investment at once. Think of it as creating your own pension from your own money.

The SWP calculator takes three inputs — investment amount, monthly withdrawal, and expected return — and shows you exactly how long your corpus will last, how much interest it will earn while you’re withdrawing, and what balance remains at the end. Whether you’re planning retirement income, funding a child’s education, or simply building a monthly cash flow from your savings, this guide covers everything you need.

Use MoneyOra’s free SWP calculator to run your numbers right now — no login required.

What is a Systematic Withdrawal Plan (SWP)?

An SWP is the opposite of a SIP. With a SIP (Systematic Investment Plan), you invest a fixed amount every month into a mutual fund. With an SWP, you invest a lumpsum once and withdraw a fixed amount every month from it.

Here’s how it works in practice. Say you invest ₹50 lakh in a balanced mutual fund and set up an SWP of ₹30,000 per month. Each month, the fund house redeems just enough units from your holdings — at that day’s NAV — to pay you ₹30,000. The remaining units stay invested and continue to grow.

If the fund earns more than you withdraw, your corpus actually grows over time. If the fund earns less than your withdrawal rate, the corpus shrinks gradually. That balance is exactly what the SWP calculator helps you understand before you start.

Who uses SWP?

SWP is used by three broad groups of people in India:

- Retirees who want a monthly income without touching a fixed deposit or pension scheme

- Parents who want to set up monthly payments for a child’s college fees over 3–4 years

- Working professionals who have received a bonus or sale proceeds and want to create a supplementary monthly income

According to AMFI (Association of Mutual Funds in India), retail participation in mutual funds has grown significantly since 2020, and SWP registrations from retirees specifically have increased year-on-year. The product is well-suited for India’s growing base of self-employed and gig-economy workers who don’t have an employer pension.

How the SWP calculator works — formula explained

The SWP calculator uses a compound interest formula that accounts for monthly returns and monthly withdrawals simultaneously. Here’s the full calculation logic.

SWP formula

The remaining corpus after each month is calculated as:

Closing Balance = (Opening Balance × Monthly Return Rate) − Monthly Withdrawal

Where Monthly Return Rate = (1 + Annual Return ÷ 100) ^ (1/12) − 1

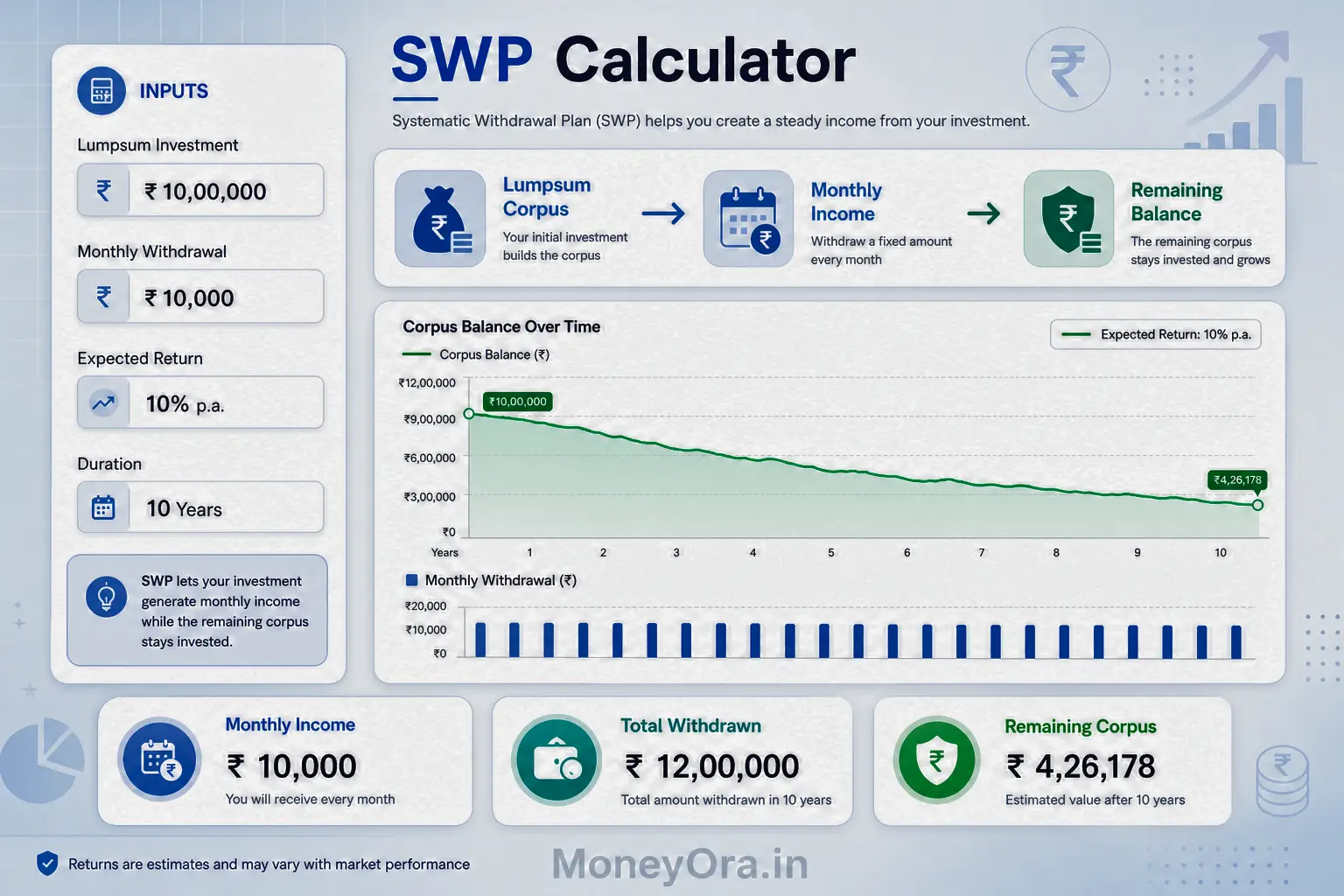

This repeats for every month of the tenure. The SWP calculator does all of this automatically — you just enter four numbers.

What you enter

- Total investment amount (lumpsum)

- Monthly withdrawal amount

- Expected annual return rate (%)

- Investment tenure (years or months)

What the SWP calculator shows you

- Total amount withdrawn over the full period

- Total returns earned during the SWP period

- Final remaining corpus at the end of the tenure

- Month-by-month withdrawal and balance schedule (in detailed calculators)

For example: ₹30 lakh invested at 10% annual return with ₹25,000 monthly withdrawal over 15 years gives a final corpus of approximately ₹45 lakh — you’ve withdrawn ₹45 lakh over 15 years AND still have ₹45 lakh left. That’s the real power of SWP when returns exceed withdrawal rate.

Run this scenario yourself with MoneyOra’s SWP calculator online. Adjust the numbers to match your situation and see the results instantly.

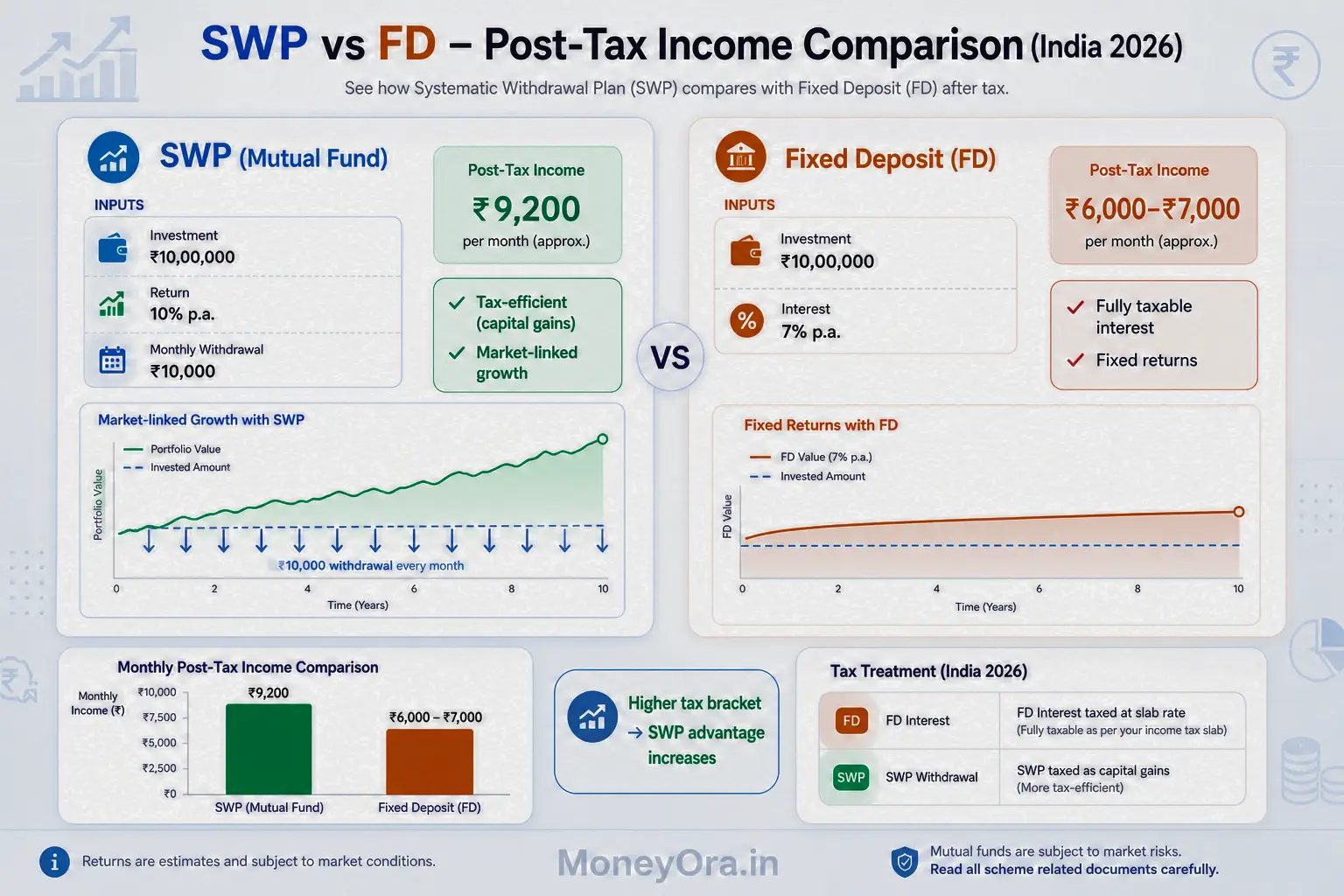

SWP vs FD: which gives better monthly income?

This is the most common question among Indian retirees. Fixed deposits feel safe. SWP feels uncertain. But when you look at the actual numbers — including tax — the picture is different.

| Factor | FD Monthly Income | SWP from Mutual Fund |

|---|---|---|

| Returns | 6–7% (fixed) | 8–12% (market-linked) |

| Tax on income | At slab rate (up to 30%) | Only capital gains portion taxed |

| Capital erosion | No (interest only) | Possible if return < withdrawal rate |

| Inflation protection | Limited | Higher for equity-oriented funds |

| Flexibility | Penalty for early exit | Can stop/pause anytime (exit load may apply) |

| Corpus growth potential | None | Yes, if fund return > withdrawal rate |

| Minimum investment | ₹1,000 | ₹5,000–₹25,000 |

The tax difference is significant. An FD returning 7% for someone in the 30% tax bracket gives a net return of about 4.9%. A balanced mutual fund SWP returning 10% with long-term capital gains tax of 12.5% on gains above ₹1.25 lakh gives a much higher post-tax return — even accounting for market risk.

Use MoneyOra’s FD calculator to calculate your exact fixed deposit returns and compare directly with the SWP calculator output.

SWP calculator with inflation — why it matters

A flat ₹30,000/month withdrawal sounds comfortable today. But in 10 years, at 6% inflation, that ₹30,000 buys only about ₹16,750 worth of goods and services. Your purchasing power is halved.

This is the problem that an SWP calculator with inflation solves. Instead of calculating with a fixed withdrawal, it lets you factor in a rising cost of living. The tool adjusts your expected spending upward each year and shows whether your corpus can sustain that increased withdrawal over time.

How SWP with inflation works

There are two approaches:

1. Inflation-adjusted withdrawal amount: You increase the monthly withdrawal amount each year by the expected inflation rate (typically 5–6%). So ₹30,000 in year 1 becomes ₹31,800 in year 2, ₹33,708 in year 3, and so on.

2. Inflation-adjusted return rate: You use the real return (nominal return minus inflation) as your expected rate in the SWP calculator. If your fund earns 10% and inflation is 6%, the real return is 4%. Calculate with 4% to see the inflation-adjusted corpus.

For long-term SWP planning (15+ years), always use the SWP calculator with inflation adjustment. A corpus that lasts 25 years on a flat calculation might last only 17 years once you account for rising withdrawals.

Thinking longer term? The CAGR calculator on MoneyOra can show you the compounded annual growth rate your existing investments have delivered — useful for setting realistic expected return inputs in the SWP calculator.

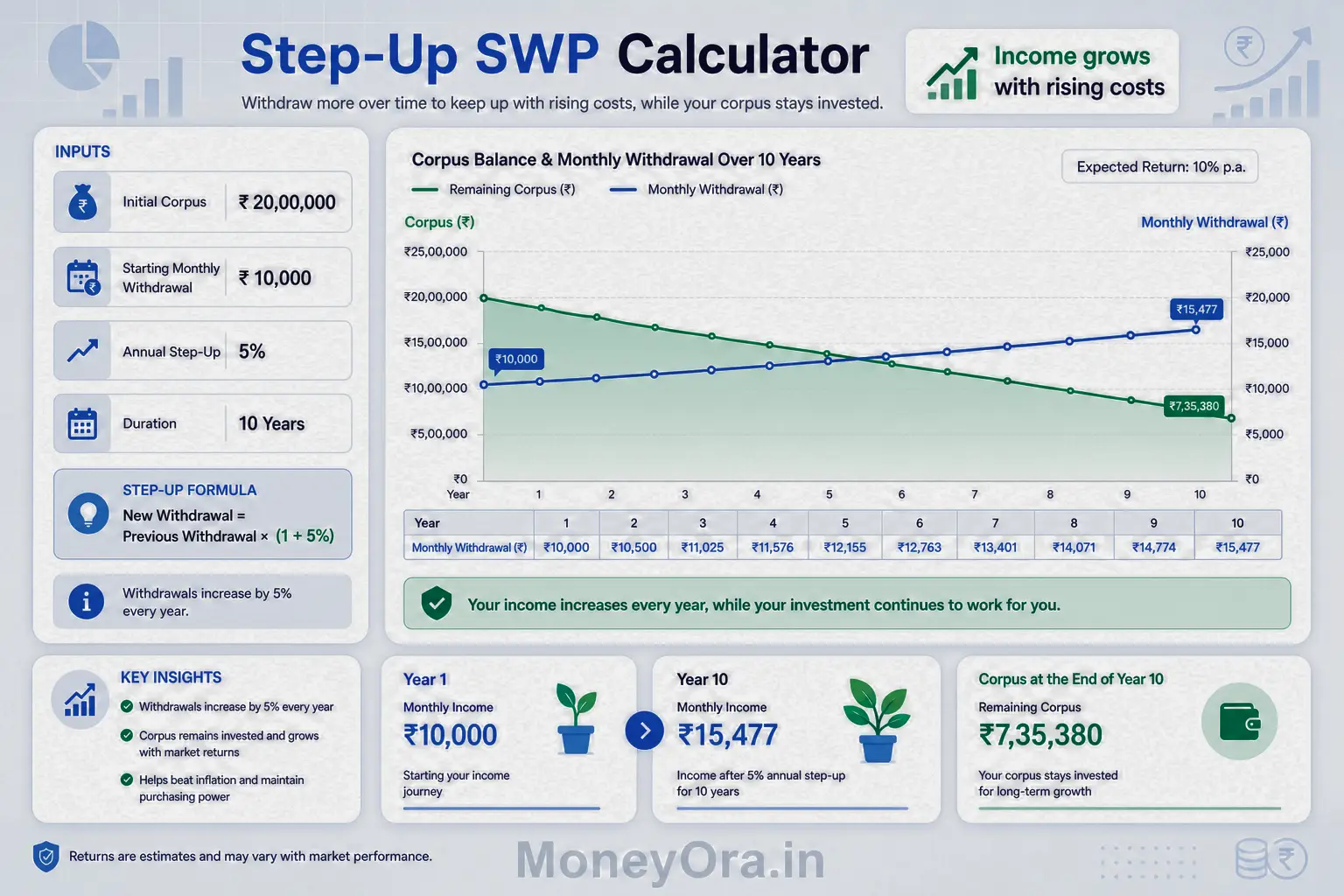

Step-up SWP calculator — increasing withdrawals each year

The step-up SWP is a more sophisticated version of the standard SWP. Instead of a fixed monthly withdrawal forever, you increase the withdrawal by a fixed percentage each year — usually 5–10%.

This works like a salary increment for your retirement income. It keeps pace with inflation without requiring you to sell all your units upfront.

Step-up SWP example

Starting withdrawal: ₹25,000/month. Annual step-up: 5%.

- Year 1: ₹25,000/month

- Year 2: ₹26,250/month

- Year 3: ₹27,562/month

- Year 5: ₹30,381/month

- Year 10: ₹38,783/month

Over 20 years with a 10% annual return on a ₹50 lakh corpus, the step-up SWP allows you to receive significantly more total income than a flat SWP — while still maintaining a meaningful corpus at the end.

Most AMCs don’t automate step-up SWP the way they automate step-up SIP. You typically need to place a fresh SWP mandate each year with the increased amount. But platforms like Zerodha Coin, Groww, and ICICI Direct are building support for step-up SWP automation.

To model a step-up SWP manually, use MoneyOra’s SWP calculator and run it year by year with the increased withdrawal amount each time.

SWP tax calculator — how withdrawals are taxed in India

Many investors assume that an SWP gives them ₹30,000 per month tax-free. That’s not accurate — but the tax treatment is still much better than FD interest. Here’s how it works.

Each SWP withdrawal has two parts

When you withdraw ₹30,000 in a month, the mutual fund redeems a certain number of units at the current NAV. The ₹30,000 received is made up of:

- Return of capital: The amount you originally invested (cost basis of units redeemed)

- Capital gains: The appreciation on those units since you bought them

Only the capital gains portion is taxable — not the full ₹30,000.

Tax rates by fund type (2025)

| Fund type | Holding period | Tax type | Tax rate |

|---|---|---|---|

| Equity / hybrid equity funds | Less than 1 year | STCG | 20% |

| Equity / hybrid equity funds | More than 1 year | LTCG (above ₹1.25 lakh) | 12.5% |

| Debt funds | Any period | Added to income | Slab rate (5–30%) |

| Balanced advantage / hybrid debt | More than 1 year | LTCG (if equity > 65%) | 12.5% |

The ₹1.25 lakh annual LTCG exemption is per financial year. For a retiree in the 5% or nil tax slab, the actual tax payable on SWP can be very low — sometimes zero for small monthly withdrawals from an equity fund held over 1 year.

The Income Tax India portal has the latest rates and exemption limits, which should be verified each financial year as budget changes can affect these figures.

For retirement planning that includes provident fund savings, pair the SWP calculator with MoneyOra’s EPF calculator and PPF calculator to see your full income picture in retirement.

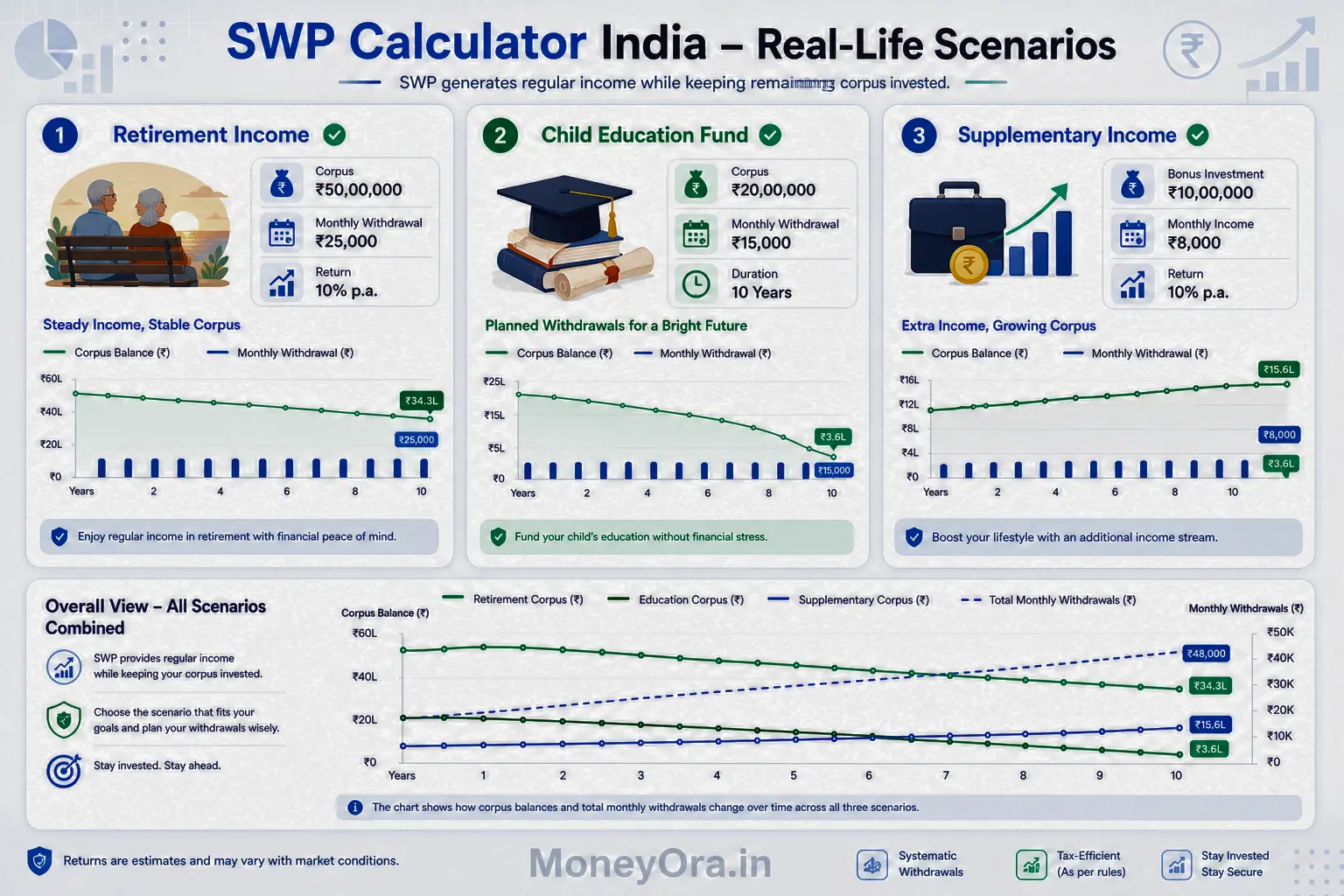

SWP calculator examples — real numbers for India

Let’s run three real scenarios through the SWP calculator so you can see how different inputs change the outcome.

Scenario 1: Retirement income — ₹50 lakh corpus

A 60-year-old investor has ₹50 lakh from EPF and PPF savings. They need ₹35,000/month for 25 years. Expected return: 9%.

- Monthly withdrawal: ₹35,000

- Corpus at end of 25 years: approximately ₹1.12 crore

- Total withdrawn: ₹1.05 crore

- Total returns earned: ₹1.67 crore

This works because the fund’s 9% return exceeds the effective withdrawal rate of about 8.4% annually.

Scenario 2: Child’s education — ₹10 lakh corpus

A parent has ₹10 lakh in a balanced fund. Their child needs ₹20,000/month for college fees for 4 years. Expected return: 8%.

- Monthly withdrawal: ₹20,000

- Corpus at end of 4 years: approximately ₹2.8 lakh

- Total withdrawn: ₹9.6 lakh

Here the corpus is nearly depleted because the withdrawal rate (24% per year) is far higher than the return rate. Fine for the purpose — planned exhaustion — but you should know this upfront.

Scenario 3: Supplementary income — ₹20 lakh bonus investment

A 45-year-old professional receives a ₹20 lakh bonus. They want ₹12,000/month for 10 years from it. Expected return: 10%.

- Monthly withdrawal: ₹12,000

- Corpus at end of 10 years: approximately ₹23.5 lakh

- Total withdrawn: ₹14.4 lakh

The corpus actually grew from ₹20 lakh to ₹23.5 lakh despite 10 years of withdrawals. The fund’s 10% return comfortably covered the ₹12,000 monthly withdrawal plus more.

Model all three scenarios yourself using MoneyOra’s free SWP calculator. Also use the lumpsum calculator to check what your current lumpsum investment could grow to before you start the SWP.

Best mutual funds for SWP in India

Not all mutual funds are equally suited for SWP. The biggest risk in SWP is capital erosion during a market downturn — when NAV falls, more units get redeemed for the same withdrawal amount, depleting the corpus faster.

For this reason, low-volatility funds work better for SWP than aggressive equity funds.

Fund categories suitable for SWP

Balanced advantage funds (also called dynamic asset allocation funds) adjust their equity-debt mix based on market valuations. They reduce equity exposure when markets are expensive and increase it when cheap. This lowers downside volatility, which protects SWP corpus during crashes.

Conservative hybrid funds keep 75–90% in debt and 10–25% in equity. They offer steady, FD-beating returns with lower risk — good for risk-averse retirees.

Equity savings funds hold equity, arbitrage, and debt. They combine equity tax treatment with lower volatility — a useful combination for SWP tax efficiency.

Short-duration debt funds or corporate bond funds work for very conservative investors who want almost no equity risk. Returns are lower (7–8%) but more predictable.

Funds to avoid for SWP

Small-cap funds, sectoral/thematic funds, and momentum funds have high volatility. During a 30–40% drawdown (which small-cap funds can experience), a fixed monthly SWP would rapidly consume units at depressed NAVs. This is the “sequence of returns risk” — getting bad returns early in your SWP is far more damaging than getting them later.

For evaluating any mutual fund’s valuation before starting SWP, MoneyOra’s PE ratio calculator and stock return calculator can give context on current market levels.

SWP on SBI, HDFC, ICICI, and Zerodha

All major mutual fund platforms in India support SWP. Here’s a quick overview of how it works on each platform.

SWP calculator SBI Mutual Fund

SBI Mutual Fund’s own SWP calculator at sbimf.com lets you simulate withdrawals from specific SBI MF schemes and compare with FD returns. You can start SWP online through SBI’s investor portal or CAMS. Minimum SWP withdrawal is typically ₹500/month.

SWP calculator HDFC Mutual Fund

HDFC Mutual Fund (now HDFC AMC) allows SWP registration through their portal, the MFOnline app, or through distributors. HDFC Balanced Advantage Fund is one of the most commonly used funds for SWP. Their calculator shows real-time NAV data.

SWP calculator ICICI Prudential

ICICI Direct’s SWP calculator lets you model withdrawals from any mutual fund available on their platform. ICICI Prudential Balanced Advantage Fund is a popular choice. SWP can be started from ₹1,000/month through ICICI Direct.

SWP calculator Zerodha

Zerodha Coin supports SWP for all direct-plan mutual funds on their platform. You can set SWP instructions directly from the Zerodha Coin app. Since Coin deals only in direct plans, you save on the distributor commission — which improves your net return and SWP sustainability.

SWP calculator Groww

Groww’s SWP calculator is among the most used in India. It provides a simple interface with instant calculation of total withdrawals, returns earned, and final corpus. Groww supports SWP on all open-ended funds available on their platform.

Regardless of which platform you use, always calculate using MoneyOra’s SWP calculator first to get an independent, unbiased projection before investing.

Common mistakes in SWP planning

These are the errors that most SWP investors make — and they’re all avoidable once you know what to look for.

1. Setting withdrawal rate too high

If your fund earns 8% and you withdraw 12% annually, your corpus will be fully exhausted within 10–12 years. A safe withdrawal rate for most balanced funds is 5–7% per year of the initial corpus. Above that, you’re drawing down principal faster than the fund can replenish it.

2. Choosing a volatile fund

A small-cap fund might average 15% over 10 years, but in year 2 it might fall 35%. If you’re withdrawing ₹50,000/month during that 35% drawdown, you’re selling units at the worst possible prices. The long-term average means nothing if you deplete the corpus in a bad early stretch.

3. Not accounting for inflation

A flat ₹30,000/month feels fine at 60. At 75, with 6% inflation running for 15 years, that same ₹30,000 buys less than ₹12,500 of today’s value. Always model at least a 5% annual step-up or use the SWP calculator with inflation to check long-term purchasing power.

4. Ignoring exit loads

Most equity funds charge a 1% exit load for redemptions within 1 year of each investment. If you start SWP immediately after investing, your first 12 months of withdrawals will incur exit load, reducing your actual monthly receipt. Check the exit load schedule before starting SWP.

5. Not reviewing the SWP annually

Markets move. Inflation changes. Your expenses change. An SWP set once and never reviewed can either deplete your corpus too fast or leave too much locked up. Review the SWP against your corpus value every 12 months and adjust the withdrawal if the fund has performed significantly above or below expectations.

6. Treating SWP as guaranteed income

SWP is not a pension. Returns are market-linked. In a severe bear market lasting 2–3 years, SWP from an equity fund can significantly deplete capital. Retirees often keep 2–3 years of expenses in a liquid fund or FD as a buffer so they can pause SWP during crashes rather than selling at low NAVs.

For risk-free, government-backed savings that complement an SWP strategy, the NPS calculator and PPF calculator show what guaranteed returns look like alongside market-linked SWP returns.

Pro tips for a sustainable SWP

These habits separate investors who successfully live off SWP for 25+ years from those who run out of corpus in 10.

- Start with a lower withdrawal and increase gradually. Begin at 5–6% annually and use a step-up SWP to raise withdrawals as the corpus grows. This protects capital in the early years when sequence-of-returns risk is highest.

- Hold 2–3 years of expenses in a liquid or ultra-short fund. Draw from this buffer during market downturns. Pause SWP when the equity fund falls more than 20%. Resume when it recovers. This alone can extend corpus life by 5–7 years in most scenarios.

- Use the SWP return calculator every year. Check: is my corpus higher or lower than the SWP calculator projected? If lower, consider reducing withdrawal by 10–15% temporarily.

- Favour direct plans for SWP. A 1% difference in annual return (direct vs regular plan) compounds significantly over 20 years. On a ₹50 lakh corpus, this can mean ₹20–30 lakh more over time — real money.

- Keep equity allocation at 50–70% for long-term SWP. Pure debt SWP often fails to outpace inflation over 20+ years. A balanced approach — part equity, part debt — gives both growth and stability.

- Use SWP alongside dividend income for diversification. MoneyOra’s dividend calculator can show how much dividend income you might receive from equity holdings — this can supplement or partially replace SWP income in good years.

- Check if your loans are manageable before starting SWP. If you have ongoing EMIs eating into your monthly budget, your required SWP withdrawal will be higher. Use the EMI calculator to see what happens to your monthly cash flow once existing loans are repaid.

SWP vs other income options — full comparison

Before you decide on SWP, it helps to see how it stacks up against every major income option available to Indian investors today.

| Income Option | Typical Return | Tax treatment | Capital preservation | Inflation protection | Flexibility | Best for |

|---|---|---|---|---|---|---|

| SWP (equity fund) | 9–12% | LTCG 12.5% | Market-linked | High | High | Long-term retirement |

| SWP (balanced fund) | 8–10% | LTCG 12.5% | Better than pure equity | Medium-high | High | Moderate risk retirees |

| Bank FD | 6–7% | Slab rate (up to 30%) | Full capital guaranteed | Low | Low (penalty on exit) | Conservative investors |

| Post Office MIS | 7.4% | Slab rate | Full | Low | None | Senior citizens |

| Senior Citizens FD | 7–7.5% | Slab rate | Full | Low | Limited | 60+ risk-averse investors |

| NPS Annuity | 6–6.5% | Pension taxable at slab | Yes | Very low | None (lifelong fixed) | Government employees |

| Dividend from stocks | 1–4% yield | Slab rate | Market-linked | Medium | High | Experienced equity investors |

| Rental income | 2–4% gross yield | Slab rate | Partial (property value) | Medium | Low | Property owners |

For most Indian investors between 55–70 years with a corpus of ₹20 lakh to ₹2 crore, a balanced advantage fund SWP offers the best combination of tax efficiency, returns, and flexibility.

The SIP-to-SWP journey: building and drawing down wealth

Most investors spend their working years building a corpus through SIP. Then at retirement, they switch to SWP for income. This is one of the most logical two-stage financial plans available to Indian retail investors.

Using MoneyOra’s SIP calculator, you can model exactly how much corpus your current monthly SIP investments will create by your target retirement age. Then feed that corpus number into the SWP calculator to see how much monthly income it generates.

For example: ₹10,000/month SIP for 25 years at 12% return gives approximately ₹1.89 crore. From that corpus, an SWP of ₹80,000/month at 9% return lasts over 40 years — well beyond any realistic retirement horizon.

You can also use the lumpsum calculator to check what a one-time investment today will grow to by retirement, and the RD calculator for recurring deposit-based corpus building alongside your mutual fund SIP.

For those managing home loans during wealth accumulation years, the home loan EMI calculator and personal loan EMI calculator help you see how much free cash flow you’ll have for SIP investment after loan repayment obligations are met.

Once you’re retired and drawing from SWP, keep emergency and short-term funds accessible. MoneyOra’s FD calculator helps you see how a 2-year emergency FD grows alongside your SWP corpus — the combination provides both security and income.

If you’re also setting up SWP across multiple banks and funds, the IFSC code finder and bank details finder on MoneyOra are quick tools to verify bank account details before linking them to your mutual fund SWP instructions.

Conclusion

An SWP is one of the smartest income tools available to Indian investors — but only when used with the right fund, the right withdrawal rate, and a clear plan. The SWP calculator removes all the guesswork. You put in four numbers and get a complete picture of how your corpus behaves over time.

The key things to remember: keep your withdrawal rate sustainable (5–7% of initial corpus per year), choose a low-volatility fund, account for inflation either through a step-up SWP or an inflation-adjusted calculation, and review your SWP every year.

Whether you’re 55 and planning retirement income, 40 and wanting supplementary monthly cash flow, or a parent setting up a college fee payment plan — the SWP calculator is the first calculation you should run.

Try MoneyOra’s free SWP calculator now. It’s free, instant, and designed for Indian investors. Then pair it with the SIP calculator to model the full SIP-to-SWP wealth journey from your working years to retirement.

Plan your monthly income today — before you need it, not after.

Frequently Asked Questions About SWP Calculator

An SWP calculator is a free online tool.

It shows how much you can withdraw monthly.

It works on a lumpsum mutual fund investment.

You enter amount, withdrawal, return rate, and tenure.

It shows final balance and total withdrawals instantly.

It applies compound interest monthly.

The remaining corpus earns returns each month.

Monthly withdrawal is deducted.

This repeats for the full tenure.

It shows final corpus and withdrawals.

SWP can be more tax-efficient than FD.

FD interest is taxed fully at slab rate.

SWP taxes only capital gains portion.

Equity LTCG is taxed at 12.5%.

Returns from mutual funds can be higher.

But they are not guaranteed.

At 10% return, you need ₹55–65 lakh.

This can sustain for 20 years.

At 8% return, requirement increases.

You may need ₹70–75 lakh.

Use calculator for exact planning.

Yes, SWP is taxable.

Only capital gains portion is taxed.

Not the full withdrawal.

Equity LTCG above ₹1.25 lakh is taxed at 12.5%.

Debt fund gains are taxed as per slab.

It includes yearly increase in withdrawal.

Usually 5–10% increase per year.

This helps adjust for inflation.

It shows impact on corpus over time.

Yes, SWP is available across major AMCs.

SBI, HDFC, ICICI, and others support SWP.

You can manage via apps or platforms.

Zerodha Coin and Groww also support it.

Minimum investment is ₹5,000–₹25,000.

This depends on fund house.

Minimum withdrawal is ₹500–₹1,000.

It varies by AMC.

SIP means investing regularly.

SWP means withdrawing regularly.

SIP builds wealth.

SWP generates income.

They are opposite strategies.

Balanced advantage funds are suitable.

Conservative hybrid funds are stable.

Equity savings funds reduce volatility.

Lower volatility protects corpus.

High volatility can deplete funds faster.