Fixed Deposit Returns

Calculator

See how your money grows — compare compound vs simple interest on any FD amount.

| Year | Opening Balance | Interest Earned | Closing Balance | Cumulative Interest |

|---|

FD Calculator – Free Fixed Deposit Calculator Online (2026)

Table of Contents

MoneyOra’s FD Calculator tells you exactly what your fixed deposit will be worth when it matures — the total amount, the interest earned, and a month-by-month or year-by-year breakdown. Type in your principal, rate, and tenure. That’s it. No login, no ads, no nonsense.

Fixed deposits are straightforward on paper — you put money in, you get more back. But the actual number depends on whether your bank compounds monthly or quarterly, whether you’re getting simple or compound interest, and how long you’re locking the money away. Getting that number wrong before you invest is a real problem. This calculator does the math correctly so you don’t have to guess. “gold vs FD — India’s RBI holds 880 tonnes, here’s the full gold reserve story”

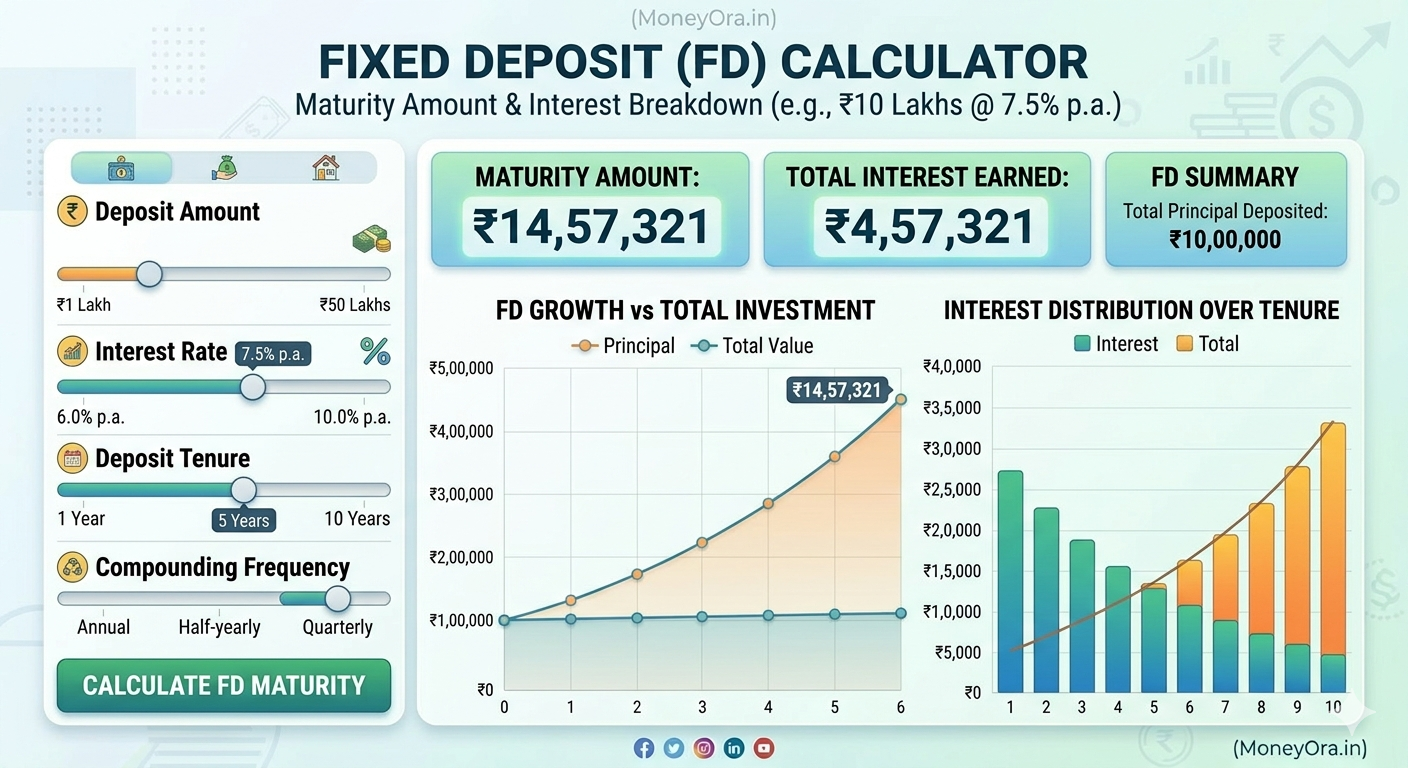

What Is an FD Calculator?

An FD Calculator takes three inputs — the amount you deposit, the annual interest rate, and the tenure — and shows you the maturity value. That’s the core of it.

A fixed deposit locks your money with a bank or NBFC for a set period, anywhere from 7 days to 10 years depending on the institution. “SIP vs FD during a market crash — which actually wins?” In return, you get a fixed interest rate that doesn’t move with the market. The catch is you can’t touch the money until maturity without paying a penalty.

Before you decide how much to put in and for how long, it’s worth knowing the exact number you’ll get out. That’s what the FD Calculator is for. MoneyOra’s version handles both simple interest and compound interest, and it shows you the full amortization schedule — not just the final maturity number.

How Does an FD Calculator Help?

The compound interest formula isn’t complicated, but applying it correctly — especially across different compounding frequencies — is easy to get wrong. Most people either use a rough estimate or trust whatever number the bank’s website shows them without checking.

Here’s where a fixed deposit calculator actually saves you trouble:

- You get the right number fast. Principal, rate, tenure — enter those three and you have the maturity amount in under a second. No spreadsheet needed.

- You can compare before committing. SBI is offering 6.8%. HDFC is at 7.1%. Bajaj Finance is at 8.05% but it’s an NBFC. Plug each rate into the FD Calculator and you see the actual rupee difference over your chosen tenure — not a percentage in the abstract.

- You plan around the real number. If you need ₹10 lakh in 4 years and you have ₹7 lakh now, you can work backwards: what rate gets you there? The calculator answers that without any algebra.

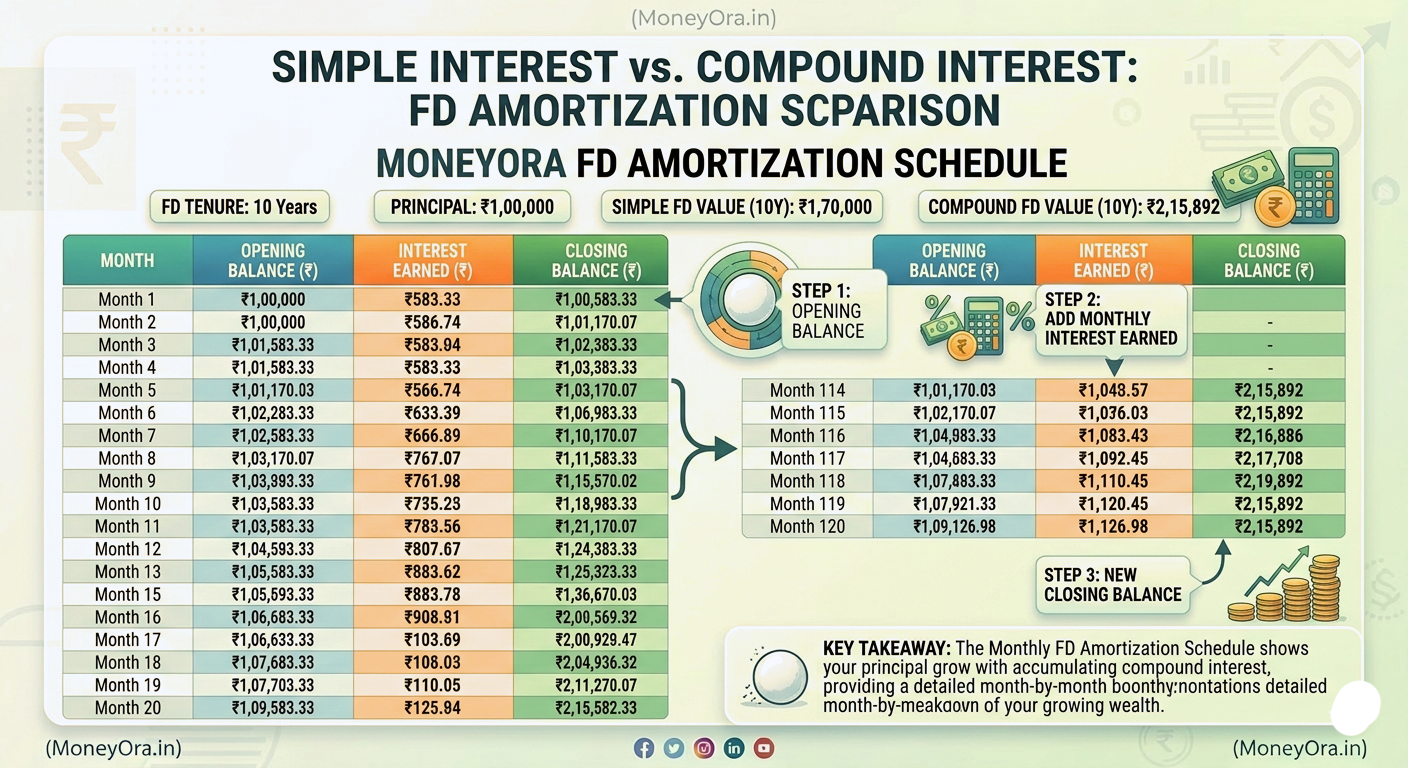

- The amortization schedule shows you when interest actually builds. A lot of the growth happens in the later years of a compound interest FD. Seeing that laid out year by year changes how you think about tenure.

The FD Maturity Formula

Banks use two methods to calculate FD interest. Which one applies to your deposit affects the final amount more than most people realise.

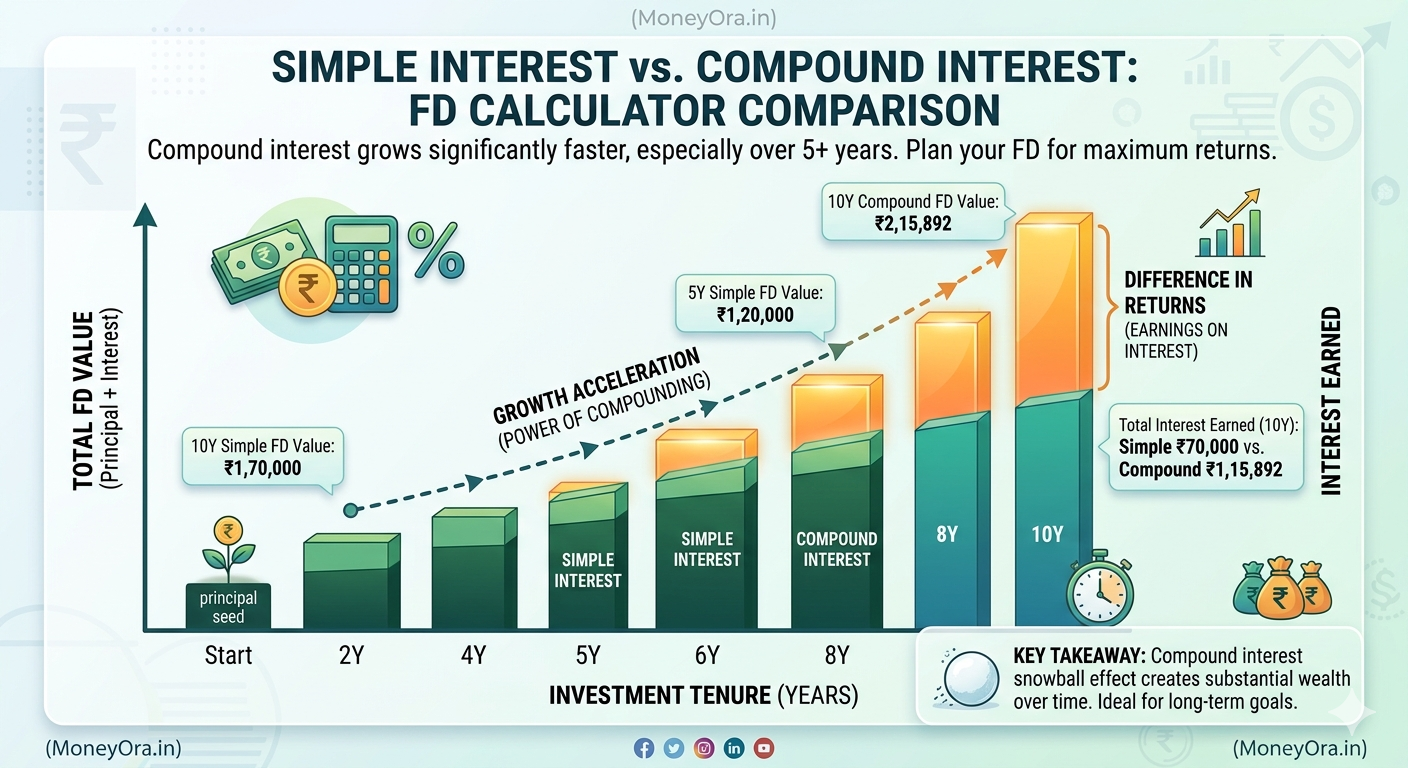

Simple Interest FD

The formula is: M = P + (P × r × t / 100)

- M = Maturity amount

- P = Principal

- r = Annual interest rate (%)

- t = Tenure in years

Example: ₹1,00,000 at 10% for 5 years.

M = ₹1,00,000 + (1,00,000 × 10 × 5 / 100)

M = ₹1,50,000

Simple interest calculates on the original principal only. The interest doesn’t compound — same amount added every year. Some NBFCs and older deposit schemes use this method.

Compound Interest FD

The formula is: M = P × (1 + r/n)n×t

- n = Compounding frequency per year (monthly = 12, quarterly = 4)

Same example: ₹1,00,000 at 10% for 5 years, compounded monthly.

M ≈ ₹1,64,531

That’s ₹14,531 more than simple interest over the same 5 years, same rate. The difference grows wider with longer tenures. At 10 years, it’s not even close.

Most banks in India use quarterly compounding for FDs. MoneyOra’s FD Calculator uses monthly compounding, which gives a slightly higher — and more favourable — estimate. Worth knowing when you compare.

Simple Interest vs Compound Interest — Side by Side

| Factor | Simple Interest FD | Compound Interest FD |

|---|---|---|

| Interest calculated on | Principal only | Principal + accumulated interest |

| Returns (₹1L, 10%, 5 yrs) | ₹1,50,000 | ₹1,64,531 |

| Better for | Short tenures (under 1 year) | Longer tenures (3 years+) |

| Who uses it | Some NBFCs, older schemes | Most scheduled banks |

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

How to Use This FD Calculator

Three fields. That’s all.

- Investment amount: Enter the principal — from ₹1,000 to ₹1 crore. Use the slider or type directly.

- Rate of interest: Enter the annual rate your bank or NBFC is offering. Check your FD offer letter or the bank’s website for the exact rate.

- Tenure in months: Enter how long you plan to keep the FD. The calculator accepts months (not years), so a 3-year FD is 36 months. A year-equivalent label appears automatically.

The FD Calculator updates instantly as you type or move the sliders. You’ll see:

- Maturity amount

- Total interest earned

- Effective yield as a percentage

- A bar chart showing year-by-year growth

- A full amortization schedule — switch between monthly and yearly view

Toggle between Compound and Simple Interest at the top to compare how much difference the interest method makes for your specific numbers.

What This Calculator Does That Others Don’t

Most FD calculators online show you a single number — the maturity amount — and stop there. That’s fine for a quick check but not much use if you’re planning around the investment.

MoneyOra’s FD Calculator is different in a few ways:

- Amortization schedule included. See how much interest accrues each month or year, what the closing balance is at each stage, and the running total. This is the kind of detail your bank’s own app usually buries or doesn’t show at all.

- Both interest types in one tool. Switch between simple and compound interest without opening a second tab.

- Tenure in months, not just years. If your FD is 18 months, you enter 18. No rounding, no approximation.

- Works on any device. The layout adjusts for mobile, tablet, and desktop without anything breaking or overlapping.

- No login, no ads. Open it, use it, close it.

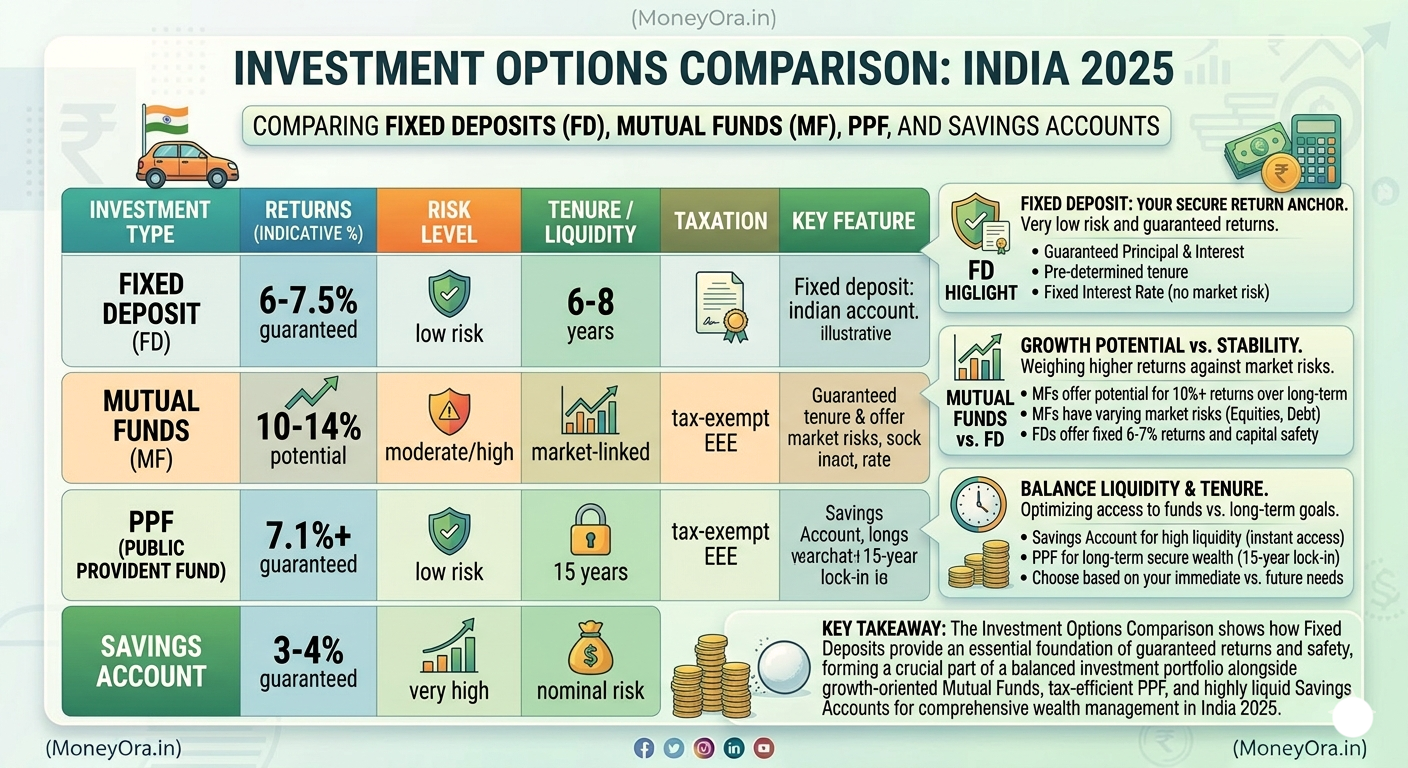

FD vs Other Investments — How It Compares

An FD isn’t the highest-return option available. It isn’t meant to be. What it offers is certainty — you know the exact number you’ll get back before you put the money in. That’s genuinely useful for a lot of financial goals.

| Investment | Typical Returns | Risk | Liquidity | Tax Benefit |

|---|---|---|---|---|

| Fixed Deposit | 6% – 9% p.a. | Very low | Medium (penalty on early withdrawal) | 5-yr FD under Section 80C |

| Savings Account | 2.5% – 4% p.a. | Very low | High | None |

| Debt Mutual Funds | 6% – 8% p.a. | Low to medium | High | None (LTCG after 3 yrs) |

| PPF | 7.1% p.a. (current) | Very low | Low (15-year lock-in) | Full EEE benefit |

| Equity / Stocks | 10% – 15% (historical average) | High | High | LTCG exemption up to ₹1L |

If you want guaranteed returns and don’t need the money for a defined period, an FD makes sense. If you can tolerate some volatility and have a longer horizon, equity gives you more. For mutual fund returns and risk disclosures, SEBI’s investor education portal is a good starting point. Most people end up using both — FDs for short-term goals, equity for long-term wealth building.

For current FD rates across major banks, the RBI’s deposit rate circulars publishes updated deposit rate data regularly.

Getting More Out of Your FD

A few things most people don’t think about until after they’ve locked in:

- Ladder your FDs. Instead of putting ₹5 lakh into a single 5-year FD, split it — ₹1 lakh each across 1, 2, 3, 4, and 5-year tenures. Every year one matures, you get access to cash and can reinvest at whatever the current rate is. If you prefer a monthly savings approach instead, check our RD Calculator for recurring deposits. It’s not complicated and it helps a lot with both liquidity and rate risk.

- Check NBFC rates, but check their credit rating too. Bajaj Finance and Shriram Finance regularly offer 0.5%–1% more than most banks. Use the FD Calculator to see what that actually adds up to over 3 years. Then check their credit rating — AA and above is the generally accepted minimum for safety.

- Senior citizens get a better deal. Banks add 0.25%–0.50% to the base rate for depositors over 60. On ₹10 lakh over 5 years that extra half percent comes to roughly ₹28,000–₹30,000 more at maturity. Worth checking with the calculator before assuming the standard rate applies.

- Tax-saving FDs lock you in for 5 years. The Section 80C deduction (up to ₹1.5 lakh) is the upside. The downside is zero liquidity for the full tenure — no premature withdrawal allowed. Don’t put emergency funds in here. More details on the Income Tax India’s official tax calculator.

- Set auto-renewal. When an FD matures and you don’t give the bank instructions, it often gets renewed at the current rate — which may be lower than when you originally invested. Auto-renewal keeps it active, but make sure you’re also watching those renewal rates.

Other free calculators on MoneyOra worth using alongside this one:

- EMI Calculator — for home, car, and personal loan EMIs

- SIP Calculator — for monthly mutual fund SIP projections

- PPF Calculator — for Public Provident Fund maturity and interest

- RD Calculator — for Recurring Deposit maturity amounts

FAQs

Yes. No account, no subscription, no charge.

MoneyOra's FD Calculator is free to use as many times as you need.

The calculator updates as you type — there's no submit button.

Enter your three inputs and the maturity amount, interest earned, and full amortization schedule appear immediately.

Simple interest is calculated on your original deposit every period — it doesn't grow.

Compound interest adds each period's interest back to the balance before calculating the next.

This means the amount grows faster over time.

For most bank FDs in India, compound interest applies.

The difference on a 5-year deposit at 10% is about ₹14,500 per lakh.

Use the FD Calculator toggle to see the exact gap for your numbers.

Yes. Enter whatever rate the NBFC is offering and the calculator works the same way.

Some NBFCs use simple interest for certain products.

Make sure you're using the right toggle in the FD Calculator.

The amortization schedule in the FD Calculator breaks down each period.

It shows opening balance, interest earned, closing balance, and cumulative interest.

You can switch between monthly and yearly views.

This helps you understand compounding in detail.

Up to 360 months — that’s 30 years.

Most bank FDs go up to 10 years.

The calculator supports longer periods for NBFC products and planning scenarios.

Yes, FD interest is added to your income and taxed as per your slab rate.

If your FD interest exceeds ₹40,000 (₹50,000 for senior citizens), TDS is deducted at 10%.

The FD Calculator shows gross returns.

Your final return depends on your tax bracket.

5-year tax-saving FDs qualify for Section 80C deduction up to ₹1.5 lakh.

However, interest earned is still taxable.

Bank calculators are limited to their own products.

They usually show only the maturity amount.

MoneyOra's FD Calculator is flexible and rate-agnostic.

It supports both simple and compound interest.

It also includes a full amortization schedule.

This makes it better for planning and comparison.

Before You Lock In

The FD itself isn't complicated.

What gets people is not knowing the exact maturity amount before they commit.

Another issue is locking in for too long at a rate that may drop later.

Use the FD Calculator.

Try different tenures and observe the amortization schedule.

Compare your bank's rate with NBFC options.

If you're also exploring loans or investments: