Car Loan EMI

Calculator

Monthly instalments for any currency — Home, Car, Personal & Education loans.

| Year | Principal | Interest | Total | Balance |

|---|

Car Loan EMI Calculator – Accurately Calculate 2026 Car Loan Monthly Instalments in India

Car Loan EMI Calculator

Use the car loan EMI calculator above — enter loan amount, interest rate, and tenure to get your monthly EMI, total interest payable, and a full amortization schedule instantly.

India crossed 4.2 million passenger vehicle sales in FY 2024-25. A significant chunk of those were financed — and for good reason. Car loans today are faster to get, more competitively priced, and available from more lenders than ever before. But taking a loan without knowing what the monthly repayment looks like is how people end up stretched thin for years.

A car loan EMI calculator tells you exactly what you are committing to before you sign anything. Not an approximation. Not a ballpark figure the dealer gives you. The actual number, calculated from the same formula every bank and NBFC uses.

Using a car loan EMI calculator takes under 60 seconds. This page explains how car loan EMI is calculated, what affects it, how to read an amortization schedule, and what to watch for when comparing offers. The car loan EMI calculator is at the top — use it first, then come back here if you want to understand what the numbers mean. Use these calculators to estimate repayment costs and understand how credit card interest charges affect your finances.

What Is a Car Loan EMI?

EMI stands for Equated Monthly Instalment. It is a fixed amount you pay every month for the entire duration of your car loan — the same rupee figure every month, from the first payment to the last.

That fixed amount has two components: principal and interest.

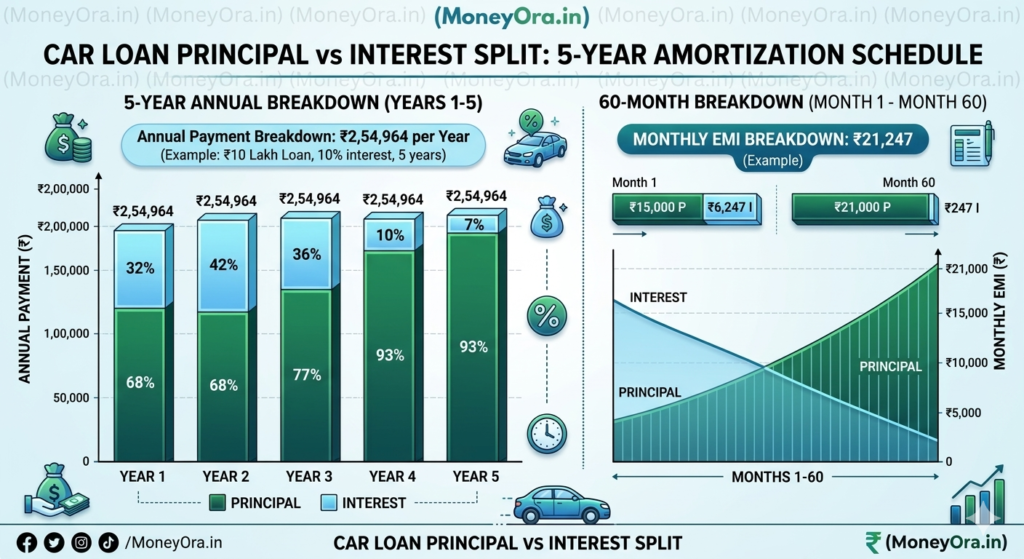

In the early months, most of your EMI goes toward interest. By the time you are near the end of the tenure, most of it reduces the outstanding principal. The total EMI stays the same throughout, but what it is made of shifts month by month. This is what an amortization schedule shows.

For example, if you borrow Rs 8 lakh at 9.5% for 5 years (60 months), your car loan EMI works out to approximately Rs 16,801. In month one, around Rs 10,469 of that reduces the principal and Rs 6,333 goes to interest. By month 60, nearly the entire payment is principal.

This matters because if you foreclose the loan early, you save significantly more interest in year one than in year four.

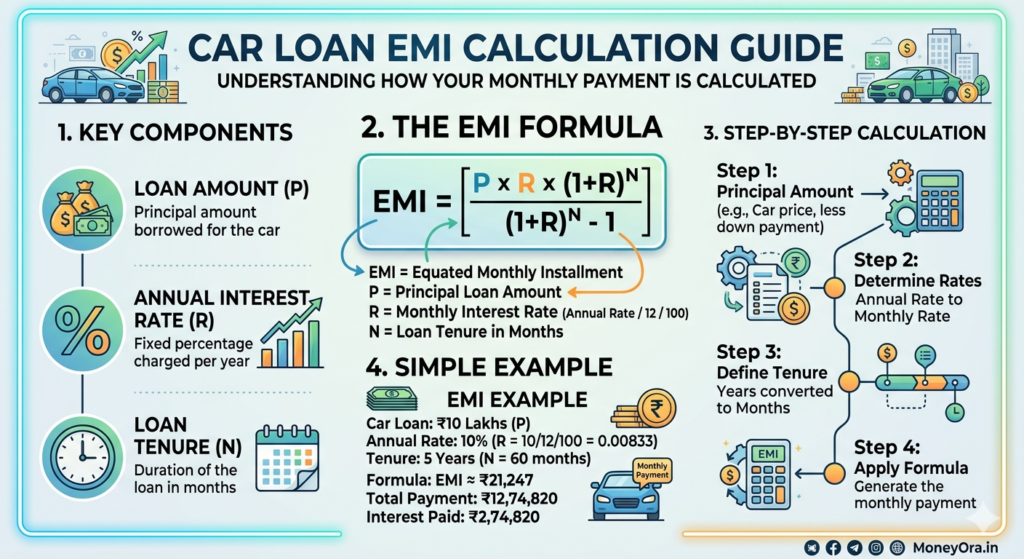

The Formula Behind the Car Loan EMI Calculation

Every bank, NBFC, and dealer finance desk uses the same standard EMI formula, as mandated by RBI guidelines on fair lending practices:

EMI = P × R × (1+R)^N ÷ [(1+R)^N – 1]

Where:

- P = Principal loan amount (the amount you are borrowing)

- R = Monthly interest rate (annual rate ÷ 12 ÷ 100)

- N = Loan tenure in months

Take a concrete example. You borrow Rs 10 lakh at 10% per annum for 7 years (84 months).

- R = 10 ÷ 12 ÷ 100 = 0.00833

- (1+R)^N = (1.00833)^84 = 2.009

- EMI = 10,00,000 × 0.00833 × 2.009 ÷ (2.009 – 1) = Rs 16,601

Total amount paid over 84 months = Rs 16,601 × 84 = Rs 13,94,484

Total interest paid = Rs 13,94,484 – Rs 10,00,000 = Rs 3,94,484

This is exactly what Moneyora’s car loan EMI calculator computes — instantly, without you needing to touch the formula.

How to Use Moneyora’s Car Loan EMI Calculator

Three inputs. No login, no registration. The car loan EMI calculator gives you results in under 5 seconds.

Step 1 — Enter the loan amount

This is the amount you plan to borrow, not the on-road price of the car. If the car costs Rs 12 lakh and you are making a Rs 3 lakh down payment, your loan amount is Rs 9 lakh.

Most lenders finance between 80% and 90% of the on-road price.

Step 2 — Enter the interest rate

Use the rate your bank or NBFC has quoted you. If you have not applied yet, use a range — typically 8.5% to 12% for new cars and 12% to 18% for used cars.

Running the car loan EMI calculator at both ends of the range shows you exactly how much the rate affects your monthly outgo.

Step 3 — Select the tenure

Most car loans in India run for 1 to 7 years. Shorter tenure means higher EMI but less total interest paid. Longer tenure reduces the monthly burden but costs more overall.

The result shows your monthly car loan EMI, total interest payable, total amount payable, and a full month-by-month amortization table.

Car Loan EMI Table — Quick Reference

If you want a fast estimate without entering numbers, the table below shows approximate EMIs for common loan amounts at 9.5% interest across different tenures.

| Loan Amount | 3 Years | 5 Years | 7 Years |

|---|---|---|---|

| Rs 3 Lakh | Rs 9,610 | Rs 6,296 | Rs 4,934 |

| Rs 5 Lakh | Rs 16,017 | Rs 10,494 | Rs 8,223 |

| Rs 8 Lakh | Rs 25,627 | Rs 16,790 | Rs 13,157 |

| Rs 10 Lakh | Rs 32,034 | Rs 20,988 | Rs 16,446 |

| Rs 15 Lakh | Rs 48,051 | Rs 31,482 | Rs 24,669 |

Rates vary by lender and applicant profile. Use the calculator above for the exact figure based on your quoted rate.

Understanding Your Amortization Schedule

An amortization schedule breaks down every single monthly payment into its principal and interest portions, from month one to the final month of the loan.

Here is the amortization for a car loan of Rs 8 lakh at 9.5% for 5 years (60 months), showing the first 12 months:

| Month | Principal (Rs) | Interest (Rs) | EMI (Rs) | Balance (Rs) |

|---|---|---|---|---|

| 1 | 10,469 | 6,333 | 16,801 | 7,89,531 |

| 2 | 10,552 | 6,250 | 16,801 | 7,78,979 |

| 3 | 10,635 | 6,166 | 16,801 | 7,68,344 |

| 4 | 10,720 | 6,082 | 16,801 | 7,57,625 |

| 5 | 10,805 | 5,997 | 16,801 | 7,46,820 |

| 6 | 10,890 | 5,911 | 16,801 | 7,35,930 |

| 7 | 10,976 | 5,826 | 16,801 | 7,24,954 |

| 8 | 11,063 | 5,739 | 16,801 | 7,13,892 |

| 9 | 11,150 | 5,651 | 16,801 | 7,02,742 |

| 10 | 11,239 | 5,563 | 16,801 | 6,91,503 |

| 11 | 11,328 | 5,474 | 16,801 | 6,80,176 |

| 12 | 11,418 | 5,384 | 16,801 | 6,68,758 |

After 12 months, you have paid Rs 2,01,612 in total (12 × Rs 16,801).

Of that, Rs 1,31,842 went toward reducing the principal and Rs 69,770 went to interest.

The complete 60-month schedule is available in the calculator output when you use the tool above.

Why does this matter practically?

If you get a bonus in year two and want to make a lump-sum partial prepayment, the schedule tells you the exact outstanding principal.

Most lenders calculate prepayment charges on the outstanding principal — so knowing this number prevents surprises at the time of foreclosure.

You can also use this to compare whether it is better to prepay in year two versus year four. The interest saving is dramatically higher in year two.

Factors That Determine Your Car Loan EMI

1. Loan Amount

The more you borrow, the higher your car loan EMI. This sounds obvious, but many buyers focus only on making the loan amount as large as possible to reduce the upfront payment.

A larger down payment — even Rs 50,000 to Rs 1 lakh more than the minimum — meaningfully reduces the total interest outgo over the tenure.

2. Interest Rate

This is the single biggest lever on your car loan EMI.

The difference between 8.5% and 12% on a Rs 8 lakh loan over 5 years is roughly Rs 2,500 per month and over Rs 1.5 lakh in total interest paid.

Your credit score, income stability, and whether you are buying a new or used vehicle all influence the rate a lender offers. Check your CIBIL score at CIBIL’s official portal before applying. A score of 750 or above generally gets you the best rate the lender offers. Anything below 700 typically results in a higher rate or outright rejection.

3. Loan Tenure

Longer tenure reduces the monthly car loan EMI but increases total interest paid. Here is the comparison on a Rs 10 lakh loan at 9.5%:

| Tenure | Monthly Car Loan EMI | Total Interest Paid |

|---|---|---|

| 3 years | Rs 32,034 | Rs 1,53,224 |

| 5 years | Rs 20,988 | Rs 2,59,280 |

| 7 years | Rs 16,446 | Rs 3,81,464 |

Going from 3 years to 7 years saves Rs 15,588 every month.

But it costs Rs 2,28,240 extra in total interest over the full term.

Neither is right or wrong — it depends entirely on your monthly cash flow.

4. Down Payment

The down payment reduces the principal and therefore both the car loan EMI and total interest.

On a Rs 12 lakh car, the difference between a 10% down payment (Rs 1.2 lakh) and a 20% down payment (Rs 2.4 lakh) is a Rs 1.2 lakh reduction in principal. At 9.5% over 5 years, that saves approximately Rs 2,008 per month and around Rs 31,000 in total interest.

5. Fixed vs. Floating Rate

Most car loans in India use a fixed interest rate — the car loan EMI does not change throughout the tenure.

Some lenders offer floating rates, which move with RBI’s repo rate changes. Fixed rates give certainty. Floating rates can work in your favor if rates fall, but they carry the risk of higher EMIs if rates rise.

New Car vs. Used Car Loan EMI — Key Differences

A used car loan EMI calculator works identically to a new car EMI calculator — same formula, same inputs. But the loan terms are typically different.

| Parameter | New Car Loan | Used Car Loan |

|---|---|---|

| Typical interest rate | 8.5% – 11% | 12% – 18% |

| Maximum tenure | 7 years | 5 years |

| Loan-to-value | Up to 90% | 70% – 85% |

| Processing fee | 0.5% – 1% | 1% – 2% |

The higher rate on used car loans reflects the lender’s higher risk. Older vehicles depreciate faster and are harder to recover if the borrower defaults.

This means the total interest cost on a used car loan can be significantly higher even if the principal is smaller.

Use Moneyora’s car loan EMI calculator for both scenarios. Enter the respective interest rates and compare the monthly commitment before deciding.

Car Loan EMI vs. Car Lease — What to Compare

Car subscriptions and leases have become more common in India over the last few years.

The monthly payment on a lease is often lower than a car loan EMI for the same car — but there is one critical difference.

With a loan, you own the car outright once the last EMI is paid. With a lease, you return the vehicle at the end of the term and start over.

Over a 10-year horizon, ownership via a loan is almost always cheaper — unless you drive very high annual kilometers and want a newer car every 3–4 years.

The car loan EMI calculator helps you establish the full ownership cost so you can make a fair side-by-side comparison.

6 Proven Tips to Reduce Your Car Loan EMI

1. Improve your CIBIL score before applying.

Even moving from 700 to 750 can get you a rate that is 1–1.5% lower. On a Rs 8 lakh loan over 5 years, that difference saves around Rs 80,000 over the tenure. Check your score free at CIBIL’s official website before approaching any lender.

2. Make a larger down payment.

Every rupee of down payment is a rupee you do not pay interest on for 5–7 years. Even an extra Rs 50,000 upfront meaningfully reduces the total cost.

3. Choose a shorter tenure if cash flow allows.

You pay more each month but significantly less overall — often Rs 1–2 lakh less in total interest on a mid-size car loan.

4. Negotiate the rate, not just the price.

Most buyers spend hours haggling over the car’s on-road price but accept the first interest rate the dealer’s finance desk offers. Banks often have room to drop the rate — especially if you have a salary account with them or an existing relationship.

5. Compare at least 3 lenders.

Your own bank, one NBFC, and the manufacturer’s finance arm (Maruti Finance, HDFC Bank auto loans, ICICI Bank auto loans). Rate differences of 2–3% are common and can translate to Rs 1.5–2 lakh in total savings.

6. Watch the processing fee carefully.

A “0% processing fee” offer at 10.5% interest can cost more total than a 1% processing fee at 9%. Use the car loan EMI calculator with total cost as the comparison metric — not just the monthly EMI.

Common Car Loan Questions

Does searching for a car loan affect my CIBIL score?

Checking your own score (a “soft enquiry”) does not affect it at all.

A lender pulling your score when you formally apply (a “hard enquiry”) does register a small negative mark. Multiple hard enquiries in a short window can lower your score by 10–15 points.

Practical advice: use a loan comparison platform that does a soft pull to shortlist lenders, then formally apply to only one or two.

Can I get a car loan with a low credit score?

Yes, but at higher rates. Some NBFCs specifically lend to borrowers with scores between 650 and 700, though rates can reach 15–18%.

If you can wait 6–12 months to improve your score first, the interest saving on a 5-year car loan is usually worth the wait.

What happens if I miss a car loan EMI?

Missing even one EMI triggers a late payment fee (typically Rs 500–2,000) and a negative mark on your CIBIL report.

Missing three or more consecutive EMIs can lead to recovery proceedings and possible repossession.

If you anticipate difficulty making a payment, contact your lender in advance — many will restructure or offer a one-time moratorium.

Is a co-applicant mandatory?

No. Most salaried and self-employed borrowers qualify independently.

A co-applicant is only required if you do not meet the income or credit criteria on your own. A co-applicant with a strong credit profile can also help you get a better interest rate.

Can I foreclose the car loan early?

Yes. Most banks and NBFCs allow part-prepayment and full foreclosure.

RBI rules prohibit foreclosure penalties on floating-rate loans, but car loans typically use fixed rates — so foreclosure charges of 2–6% of the outstanding principal usually apply. Always check this clause before signing.

Does the loan amount include insurance and accessories?

Some lenders allow you to fold in car insurance, extended warranty, and accessories. This raises the principal but reduces the upfront cash outflow.

Use the car loan EMI calculator to compare the total interest cost of including insurance in the loan versus paying it separately.

Car Loan Tax Benefits — What You Can Claim

For individual borrowers buying a car for personal use, there is no income tax deduction on car loan interest under the Income Tax Act.

If you are self-employed or a business owner and the car is used for business purposes, you can claim the interest component as a business expense under Section 37(1).

Depreciation on the vehicle can also be claimed separately under the Income Tax Act.

Salaried employees cannot claim any deduction on car loan interest — even for official use — unless their employer has structured a car lease benefit under the company’s CTC. If you are unsure about your eligibility, consult a tax professional or refer to the Income Tax Department’s guidelines.

Summary

A car loan EMI calculator is the fastest way to go from “I want that car” to “here is exactly what I will pay every month and what it will cost me in total.” The calculation is straightforward — principal, rate, tenure — but the implications of choosing different combinations can run into lakhs of rupees over the life of the loan.

Use the Moneyora calculator to run your numbers before you walk into a dealership or apply with a lender. Know your maximum comfortable EMI, work backward to the loan amount that fits, and you are in a much stronger position to negotiate both the car price and the financing terms.

Disclaimer: All EMI figures shown on this page are indicative and calculated using the standard reducing balance formula. Actual EMI from your lender may vary based on processing fees, rounding, insurance add-ons, and lender-specific terms. Moneyora is not a bank or NBFC and does not offer loans directly. Please verify all figures with your lender before committing to a loan agreement.

How Moneyora’s Car Loan EMI Calculator Compares

Most car loan EMI calculators give you three numbers — EMI, total interest, total amount payable. That is the minimum.

Moneyora’s car loan EMI calculator adds a complete month-by-month amortization breakdown and lets you adjust all three variables in real time to see how each one changes the outcome.

No registration. No data stored. No ads interrupting the calculation.

If you are comparing multiple loan offers, our loan comparison tool lets you put two lenders side by side with full cost breakdowns. For larger borrowings, the home loan EMI calculator applies the same logic to longer tenures and higher principal amounts.

Frequently Asked Questions

Most banks require a minimum monthly net salary of Rs 15,000 to Rs 25,000.

This varies by lender and the loan amount requested.

NBFCs are often more flexible on income criteria but typically charge higher interest rates.

Lenders typically finance up to 90% of the on-road price for new cars.

For a Rs 15 lakh on-road car, the maximum loan is usually Rs 13.5 lakh.

Some lenders offer 100% financing for customers with strong credit profiles and an existing salary account with the bank.

No. Your EMI repays only the loan principal and interest.

Car insurance is a separate annual payment.

It is only included in the EMI if you specifically added it to the loan amount at the time of disbursement.

You cannot directly change the EMI amount after disbursement.

However, you can make partial prepayments to reduce the outstanding principal.

The lender will then either reduce your EMI or shorten the loan tenure — some lenders let you choose which benefit you prefer.

A flat rate calculates interest on the original principal for the entire loan tenure.

A reducing balance rate — used by all scheduled banks in India — calculates interest only on the remaining balance after each payment.

A 10% flat rate is roughly equal to a 17–18% reducing balance rate.

As per RBI's fair lending guidelines, lenders must disclose the annualised rate on a reducing balance basis.

Generally yes, the base rate applies across most models.

However, some lenders offer preferential rates through manufacturer partnerships.

Brands like Maruti Suzuki, Hyundai, and Tata Motors sometimes provide special loan rates through specific banks — worth asking about at the dealership.