SIP & Lumpsum

Calculator

Estimate wealth creation from systematic & one-time investments — with year-by-year projections.

| Year | Invested | Returns | Corpus | CAGR |

|---|

Lumpsum Calculator – Calculate Investment Returns Online

A lumpsum calculator helps you understand exactly how much your one-time investment could grow over time. Instead of guessing, you can see real numbers—what your ₹15 lakh, ₹50 lakh, or whatever amount might become in 5, 10, or 20 years. “prefer regular investing? Start with a ₹100 per day SIP challenge”

This is different from investing small amounts every month (that’s SIP). With lumpsum, you invest all the money at once and let compound growth work for you. The calculator shows you different returns—absolute, annualized, trailing—so you can make informed decisions about your mutual funds or other investments. “model your gold lumpsum investment — India’s RBI holds 880 tonnes for good reason”

Whether you’re planning for retirement, a down payment, or just want to grow your savings, knowing your potential returns changes how you invest. That’s what makes this lumpsum investment calculator so valuable.

How a Lumpsum Calculator Works

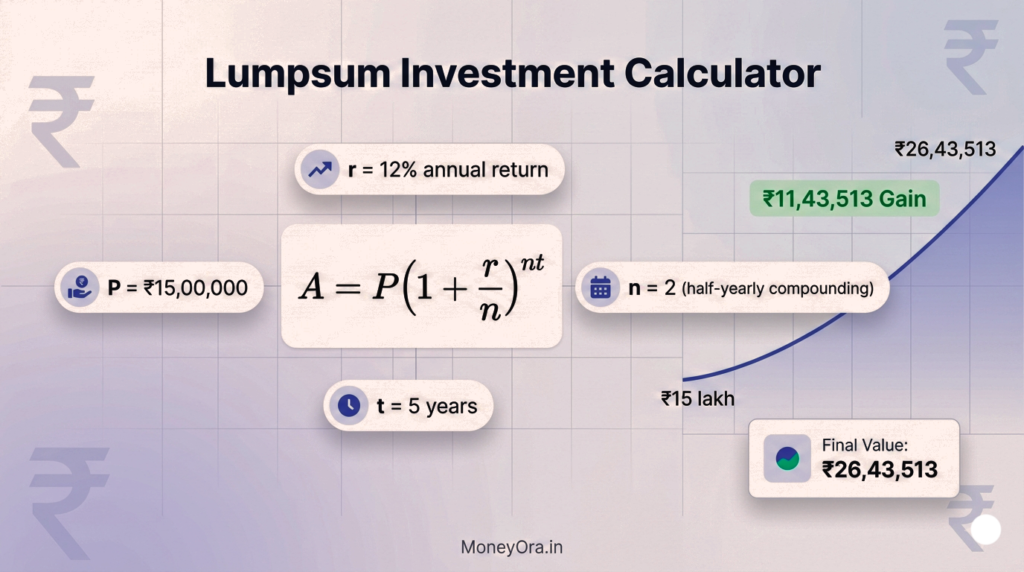

A lumpsum calculator uses one simple formula to give you big clarity: A = P(1 + r/n)^nt

That looks complex, but here’s what it actually means:

– P = the money you invest right now

– r = how fast it grows annually (the return rate)

– n = how often growth is added (monthly, quarterly, yearly)

– t = how many years you’re investing

– A = what you’ll have at the end

Let’s say you invest ₹15 lakh at 12% annual return for 5 years, compounding every 6 months. The formula spits out ₹26,43,513. That’s over ₹11 lakh more than you started with—pure compound growth. “why staggered investing suits early-stage sectors like green hydrogen”

You don’t need to do this math yourself. The calculator does it instantly.

What Returns Will You Actually See?

When you use our lumpsum calculator, you’ll see several types of returns. Here’s what each one means:

Absolute return: Total profit from your investment, start to finish. If you invested ₹15 lakh and ended with ₹26 lakh, that’s ₹11 lakh absolute return.

Annualized return: How much you earn each year on average. This makes it easy to compare different investments—some fund earned 12% annualized, another earned 8%.

Point-to-point return: The return over a specific time period (like exactly 5 years).

Trailing return: Performance from a set date until today.

Rolling return: Average performance over multiple overlapping periods.

Most people care about annualized and absolute returns—they show the real picture of growth. “why staggered gold buying beats a single lump-sum purchase at record highs”

Why Use MoneyOra’s Lumpsum Calculator?

Instant answers. Enter your amount, rate, and time frame. Get results in seconds instead of wrestling with spreadsheets.

Accurate estimates. Our calculator uses the proven compound interest formula. It won’t predict every market move (nothing can), but it shows you the most likely scenario.

Plan your actual life. Know what you might have in 5 years, 10 years, or at retirement. Then you can decide if you need to invest more or adjust your strategy.

Online, anytime. No software to install, no downloads. Calculate from your phone, laptop, or tablet—whenever you’re thinking about money.

Free and transparent. See exactly how your investment grows, year by year. No hidden calculations.

Lumpsum vs SIP – Which Is Right for You?

Lumpsum and SIP (Systematic Investment Plan) are two completely different approaches:

Lumpsum: You have money now. Invest it all at once. Get it working immediately.

– Good if you have a large amount sitting around

– Takes advantage of the market immediately (no averaging)

– Simpler—one action, done

– Works best when markets are down (you buy at lower prices)

SIP: You invest small amounts regularly—₹5,000 or ₹10,000 monthly.

– Good if you don’t have a large sum right now

– Spreads risk across different market conditions

– Forces disciplined saving

– Easier psychologically (smaller payments)

Use our lumpsum calculator to see how a one-time investment could grow. Then ask yourself: Do I have the money right now? Can I handle volatility? How soon do I need these returns? Your answers guide whether lumpsum or SIP makes sense.

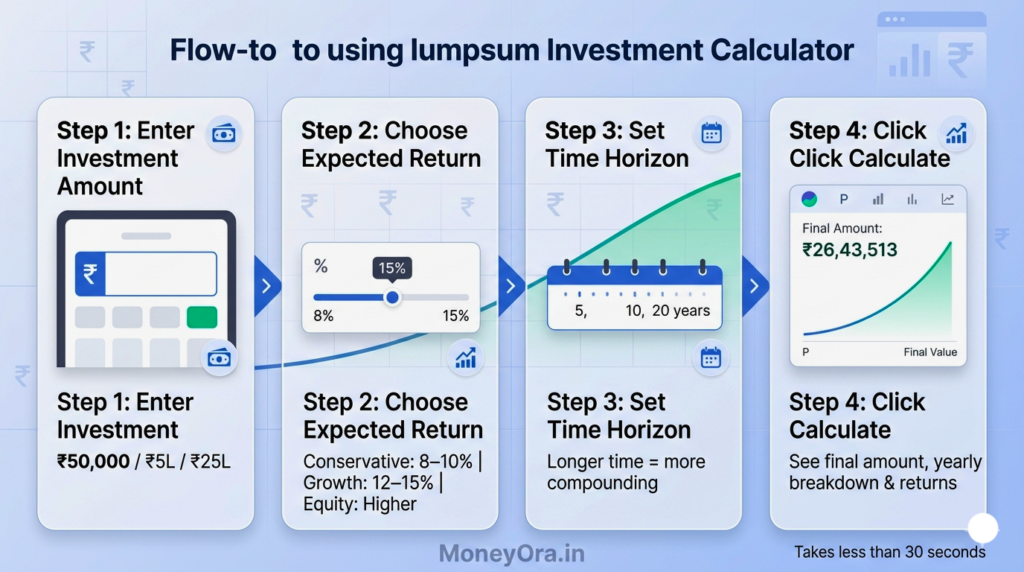

How to Use the Lumpsum Calculator (Step-by-Step)

Step 1: Enter your investment amount

Type the exact sum you’re investing—₹50,000, ₹5 lakh, ₹25 lakh, whatever you have.

Step 2: Choose your expected annual return

This depends on what you’re investing in. Conservative funds earn 8-10%, growth funds 12-15%, equity funds can be higher. Unsure? Check your fund’s past performance or ask your advisor.

Step 3: Set your time horizon

How many years before you need this money? 5 years, 10 years, 20 years? Be realistic—the longer you stay invested, the better compound growth works.

Step 4: Click calculate

We’ll show you your estimated final amount, year-by-year breakdown, and total returns.

That’s it. Takes 30 seconds.

Common Questions About Lumpsum Calculators

Are these numbers guaranteed?

No. Markets move unpredictably. The calculator shows a realistic estimate based on the return rate you enter. Think of it as “most likely” not “definitely.”

What return rate should I use?

Check your mutual fund’s past 5 or 10-year performance. That’s a decent starting point. For conservative investments (bonds, savings), expect 6-8%. For growth stocks, 12-18% is possible but not guaranteed.

Can I adjust the calculation later?

Absolutely. Change your amount, rate, or timeline whenever you want. See how adding ₹10,000 more changes things. See what 2 extra years of compounding does.

Why does compound growth matter?

Because you earn returns on your returns. Year 1 you earn ₹1.2 lakh (on ₹10 lakh at 12%). Year 2 you earn ₹1.34 lakh (on ₹11.2 lakh). The growth accelerates. That’s what makes long-term investing powerful.

What if the market drops?

Markets go up and down. The calculator assumes your chosen return rate on average. Some years will be better, some worse. Staying invested through both gives you the long-term return rate.

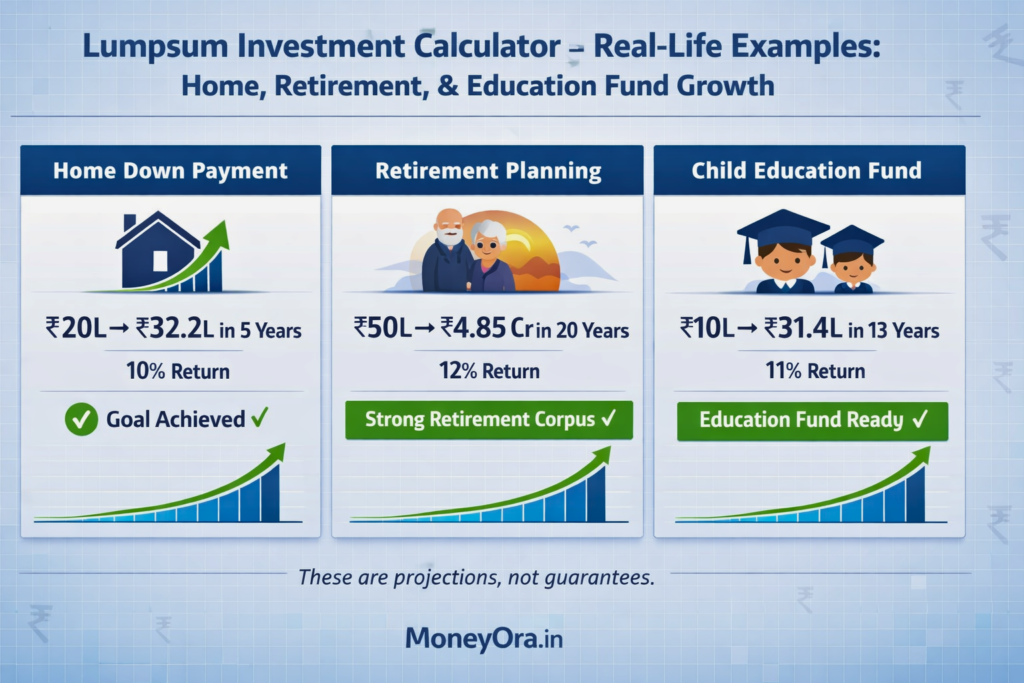

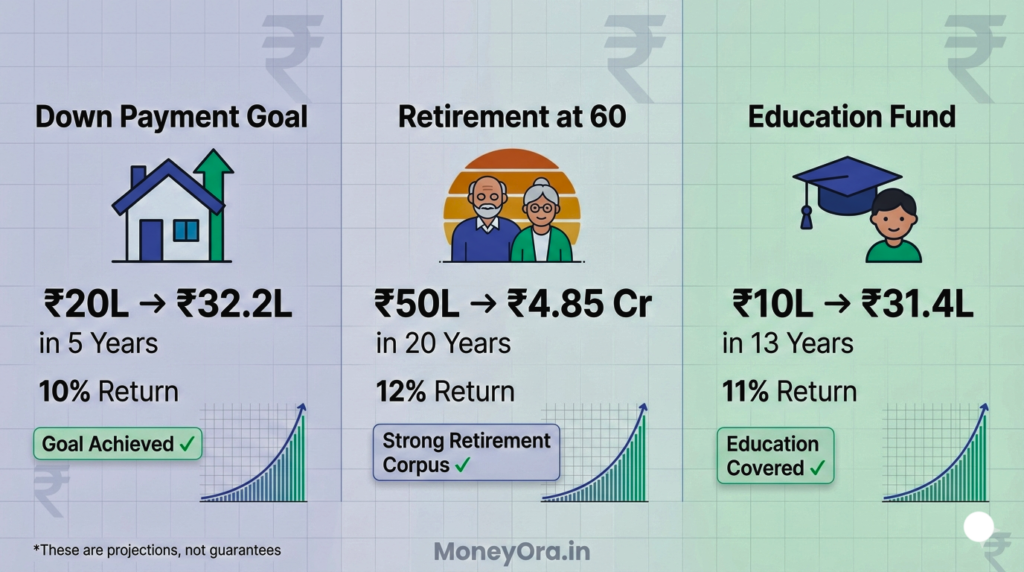

Real-World Examples with the Lumpsum Calculator

Example 1: Building a Down Payment

You have ₹20 lakh and want it to become ₹30 lakh for a house down payment.

– Amount: ₹20 lakh

– Expected return: 10% annually

– Time horizon: 5 years

– Result: ₹32.2 lakh (exceeds your goal ✓)

Example 2: Retirement Planning at 40

You’re 40, have ₹50 lakh, want to retire at 60.

– Amount: ₹50 lakh

– Expected return: 12% (balanced portfolio)

– Time horizon: 20 years

– Result: ₹4.85 crore (substantial retirement corpus ✓)

Example 3: Creating a Child’s Education Fund

Child is 5, starting school at 18 (13 years away).

– Amount: ₹10 lakh

– Expected return: 11% (education fund target)

– Time horizon: 13 years

– Result: ₹31.4 lakh (covers quality education ✓)

These aren’t promises. But they show what’s possible with compound growth.

Why Choose MoneyOra Over Groww, Finology, and Other Calculators?

We keep it simple. No unnecessary complexity, no app bloat. Just enter numbers, get answers.

Built for Indians. Shows returns in rupees. References Indian investment options (mutual funds, SIPs, NPS). Understands India’s tax brackets if you dig deeper.

Fast and reliable. Calculations happen instantly without lag or loading delays.

Part of a larger platform. Beyond the calculator, you have access to EMI calculators, bank details finder, and investment tracking tools—everything you need.

Actually free. No hidden sign-ups, no premium tiers, no selling your data.

Other calculators are fine, but MoneyOra was built by people who understand how Indians actually invest. Use it and see the difference.

How to Maximize Your Lumpsum Investment

Start early. Time is your biggest advantage. An investment at 25 has 40 years to compound. At 45, only 20 years. The earlier dollar compounds far more.

Stick with it. Don’t panic sell when markets drop. That’s when your money buys more shares at lower prices. The longest investors see the best results.

Diversify. Don’t put all ₹50 lakh in one fund. Spread across large-cap, mid-cap, small-cap, international, and bonds. Lower risk, steadier growth.

Increase when you can. If you get a bonus, inheritance, or windfall, add it to your lumpsum. That extra amount compounds for years.

Rebalance annually. Check if your allocation still matches your goals. Markets move around your original percentages. Rebalance once a year.

Know your goal. Are you investing for retirement, a home, education, or just wealth building? Different goals need different timeframes and risk levels. The calculator adapts to whatever you’re saving for.

- /emi-calculator – “For large purchases like homes, also check our EMI calculator to understand monthly payments”

- /nps-calculator/ – “If retirement is your goal, also explore our NPS calculator for long-term tax benefits”

- /fd-calculator – “Want more conservative returns? Compare with our fixed deposit calculator

- SEBI (Securities and Exchange Board of India): “Learn about mutual fund regulations from SEBI” – sebi.gov.in

- Why: Official regulatory body, trusted source

- RBI Official Site: “For understanding interest rates on savings” – rbi.org.in

- Why: Central Bank authority

- BSE/NSE Educational Resources: “Understand how markets work” – bseindia.com or nseindia.com

- Why: Stock exchange authority, educational credibility

- Wikipedia on Compound Interest: “Read more about compound interest mathematics”

- Why: Neutral, trusted, widely cited

Frequently Asked Questions

A lumpsum investment calculator estimates how much your one-time investment will grow over time.

It uses your expected annual return rate and time period.

Use the formula A = P(1 + r/n)nt.

P is your investment.

r is the annual return rate.

n is how often it compounds.

t is the number of years.

Our calculator does this instantly.

Yes. Lumpsum works well for long-term goals of 10+ years.

Compound growth gets more time to work.

For shorter periods, SIP may be safer.

It spreads market risk over time.

Check your chosen fund or investment's past 5-year or 10-year performance.

Conservative: 6–8%.

Balanced: 10–12%.

Growth: 12–18%.

Past performance does not guarantee future returns.

Yes. You can add lump sums periodically.

You can also start a SIP alongside it.

Many investors combine both strategies.

Check annually to ensure your investment is on track.

Market fluctuations happen monthly.

Annual reviews give you a clearer picture.

They also help you avoid reacting to short-term noise.

Our basic calculator shows nominal returns.

For inflation-adjusted returns, subtract India's inflation rate from your expected return rate.

Inflation is typically around 5–6%.

The calculator shows mathematical projections.

A financial advisor considers your full financial situation.

They also consider taxes, risk tolerance, and life goals.

Use both.

Use the calculator for estimates.

Use an advisor for a personalized strategy.

That depends on your emergency fund.

Keep 6–12 months of expenses aside first.

It also depends on your immediate needs and risk tolerance.

Never invest money you may need within 2–3 years.

Do not invest borrowed money.

It is as accurate as the inputs you provide.

If you enter realistic return rates and time horizons, yes.

If you assume 25% returns, the math will work.

But the prediction may not match reality.