Most financial mistakes in India don’t happen because people are careless. They happen because nobody explained the words. Someone signs a loan without knowing what APR means. Someone breaks an FD not knowing the penalty clause. Someone invests in a mutual fund without understanding what LTCG tax will do to the return six years later.

These 50 financial terms are the ones that appear most often in loans, investments, tax filings, and bank statements — and where misunderstanding the most common financial terms actually costs real money. Each one here comes with the plain meaning, a one-line reason it matters, and a real-world example from Indian finance in 2026. No jargon piled on top of jargon. Where a MoneyOra calculator helps you act on the concept, we’ve included that too.

Key Takeaways

- Knowing financial terms isn’t about sounding smart — it’s about not getting taken advantage of when signing a loan, filing taxes, or choosing an investment.

- Most financial regret in India starts with a misunderstood term: people confuse CTC with take-home, interest rate with APR, or face value with market price.

- India’s financial literacy rate was 27% in the most recent global survey — among the lowest for a G20 economy. These 50 terms are a direct fix for that gap.

- The 50 terms here are grouped by category — banking, investment, loans, tax, markets, insurance — so you can use this as a reference guide any time you encounter an unfamiliar word.

- Every calculation-heavy term (EMI, SIP, CAGR, FD returns) links to a free MoneyOra calculator so you can move from definition to real number in under a minute.

Why These 50 Financial Terms — And How to Use This Guide

There are thousands of financial terms in use across banking, investing, and taxation. Most glossaries list them all alphabetically. That format is fine if you know what you’re looking for. It’s less useful if you’re trying to build a working understanding of personal finance from scratch.

This guide is structured differently. The 50 financial terms here are grouped by the financial decision they relate to — banking first, then investment returns, loans, tax, stock markets, and finally insurance and retirement. The order matters: each section builds on the one before it.

Each term follows the same structure:

- Plain meaning — what the word actually means

- Why it matters — the specific way not knowing this costs money

- Real example — an Indian context, 2026 figures where applicable

If you’re reading this as a beginner, start from term 1. If you’re looking up a specific term, use the table of contents. Bookmark this page — it’s the kind of reference you’ll come back to when filling out forms, comparing products, or doing tax planning.

Section 1 — Basic Money & Banking Financial Terms (1–10)

1. Interest Rate

Plain meaning: The percentage a lender charges you for borrowing money, or a bank pays you for depositing money. Expressed as an annual rate.

Why it matters: A 1% difference in interest rate on a ₹30 lakh home loan over 20 years adds up to roughly ₹4–5 lakh in extra payments. The number looks small; the impact doesn’t.

Real example: A savings account at SBI pays ~2.7% p.a. A liquid mutual fund returned ~7.2% in FY2025-26. Same money, very different outcome.

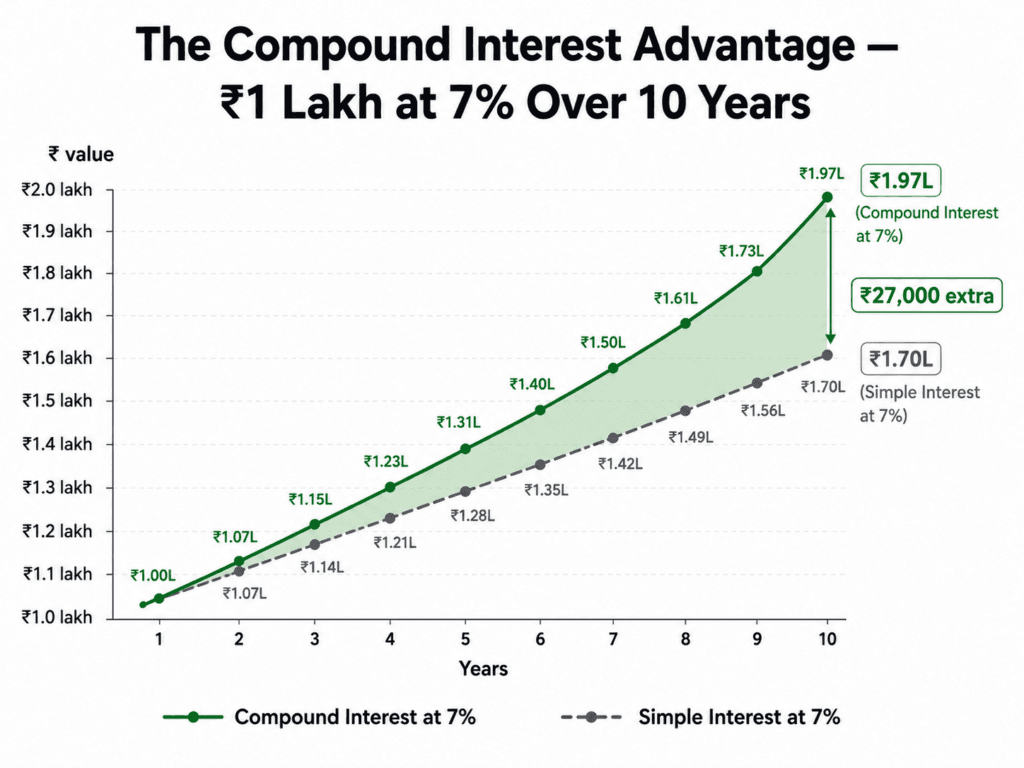

2. Compound Interest

Plain meaning: Interest earned not just on your original amount but also on the interest you’ve already earned. It grows faster the longer you leave it.

Why it matters: This is why ₹1,000/month started at 22 beats ₹5,000/month started at 40. Time is more powerful than amount when interest compounds.

Real example: ₹1 lakh in an FD at 7% compounded annually becomes ₹1.96 lakh in 10 years. In a PPF at 7.1% compounded annually over 15 years, it grows even further — use MoneyOra’s PPF Calculator to model your own numbers.

3. Inflation

Plain meaning: The rate at which prices rise over time, reducing what your money can buy.

Why it matters: India’s CPI inflation averaged 5–6% annually in recent years. An FD at 7% earns only 1–2% in real terms after inflation. Many people think they’re saving; they’re barely keeping pace.

Real example: ₹50,000 in 2016 bought what ₹72,000 bought in 2026, roughly. An investment that doesn’t beat inflation is losing ground in purchasing power, even as the number on paper grows.

4. Net Worth

Plain meaning: Total assets minus total liabilities. What you actually own free and clear.

Why it matters: Most people know their income but not their net worth. Net worth is the honest measurement of financial progress — salary tells you what’s coming in, not how much you’re keeping.

Real example: You earn ₹10 lakh/year. You own a flat worth ₹50 lakh (with ₹30 lakh outstanding loan), mutual funds worth ₹8 lakh, and have ₹3 lakh in savings. Your net worth: (50 − 30) + 8 + 3 = ₹31 lakh. That’s the real number.

5. Liquidity

Plain meaning: How quickly and easily you can convert an asset into cash without losing significant value.

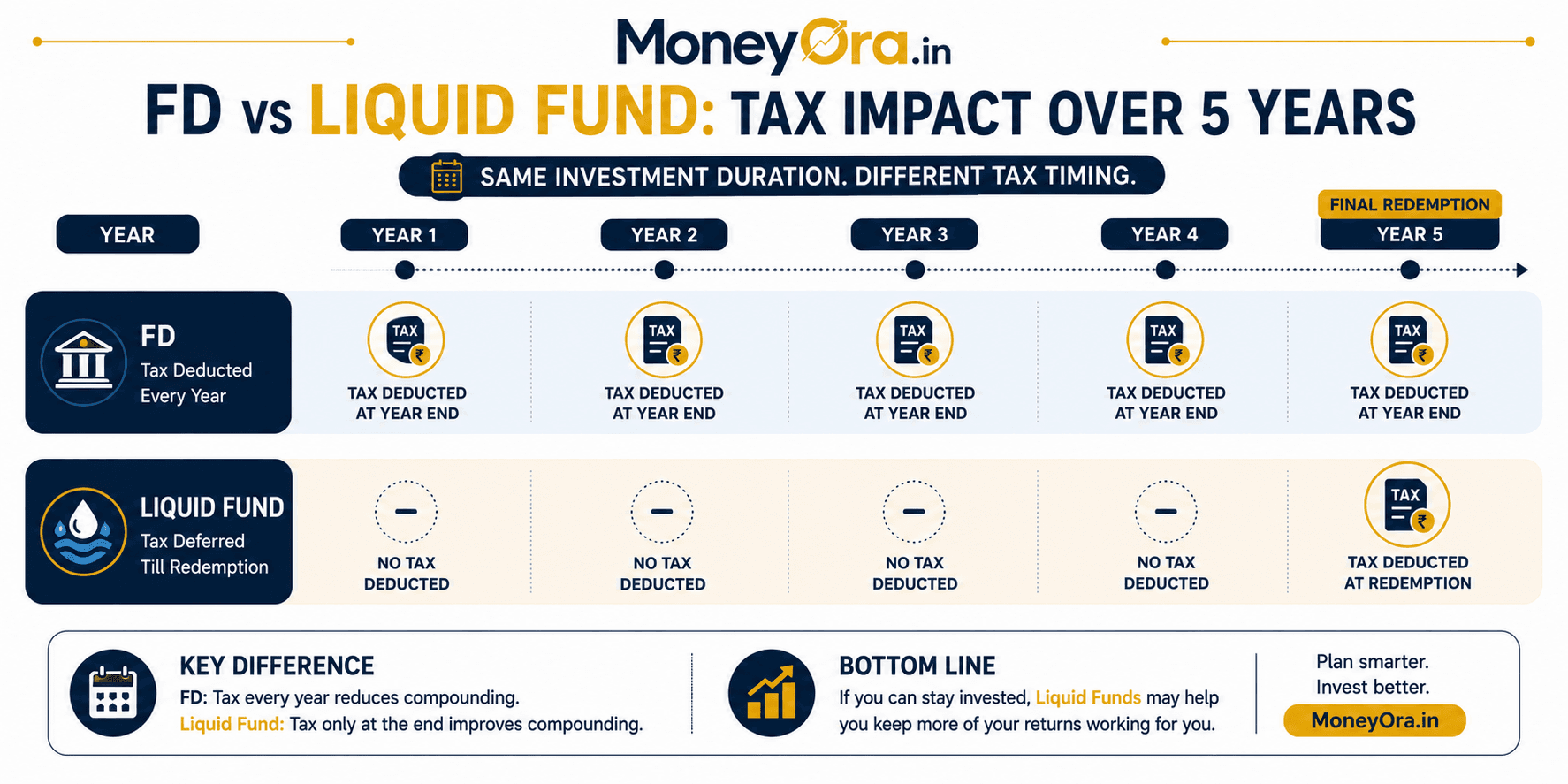

Why it matters: Real estate is high-value but low liquidity — you can’t sell part of a flat in a medical emergency. A liquid fund is accessible in 24 hours. Mixing these up leaves people cash-poor during crises.

Real example: Stocks are more liquid than property but less liquid than a savings account. A liquid mutual fund sits between them — typically redeemable within one business day.

6. Fixed Deposit (FD)

Plain meaning: A bank deposit at a fixed interest rate for a fixed period. Principal is guaranteed. Interest is paid at maturity or at intervals.

Why it matters: FDs feel safe and are safe — but interest income is taxable as per your slab, making the post-tax return lower than it appears, especially for those in the 20–30% bracket.

Real example: FD rate of 7.2%. At the 30% tax bracket, after-tax return is about 5.04%. With 5–6% inflation, that barely protects purchasing power. Calculate your exact maturity using MoneyOra’s FD Calculator.

7. Recurring Deposit (RD)

Plain meaning: A monthly deposit scheme at a bank where you put a fixed amount each month and earn interest. Like an FD, but built incrementally.

Why it matters: RDs suit people who want to save regularly but don’t have a lump sum. The effective return is roughly half an FD’s return because contributions come in over time, not upfront.

Real example: ₹5,000/month RD for 12 months at 7% doesn’t return 7% on ₹60,000 — it returns 7% on an average balance, because the first payment earns 12 months of interest but the last earns only 1. Try MoneyOra’s RD Calculator for exact figures.

8. UPI (Unified Payments Interface)

Plain meaning: India’s real-time digital payment system that moves money between bank accounts instantly, 24/7, using a mobile number or VPA.

Why it matters: India processes over 17 billion UPI transactions per month as of 2026. Understanding UPI limits, security features, and transaction types helps avoid fraud and optimise for different payment needs.

Real example: UPI handles P2P transfers, merchant payments, and increasingly, investments and insurance premiums. IMPS (for scheduled transfers), NEFT (batch transfers), and RTGS (high-value transfers above ₹2 lakh) each have different use cases — all three are relevant financial terms for basic banking.

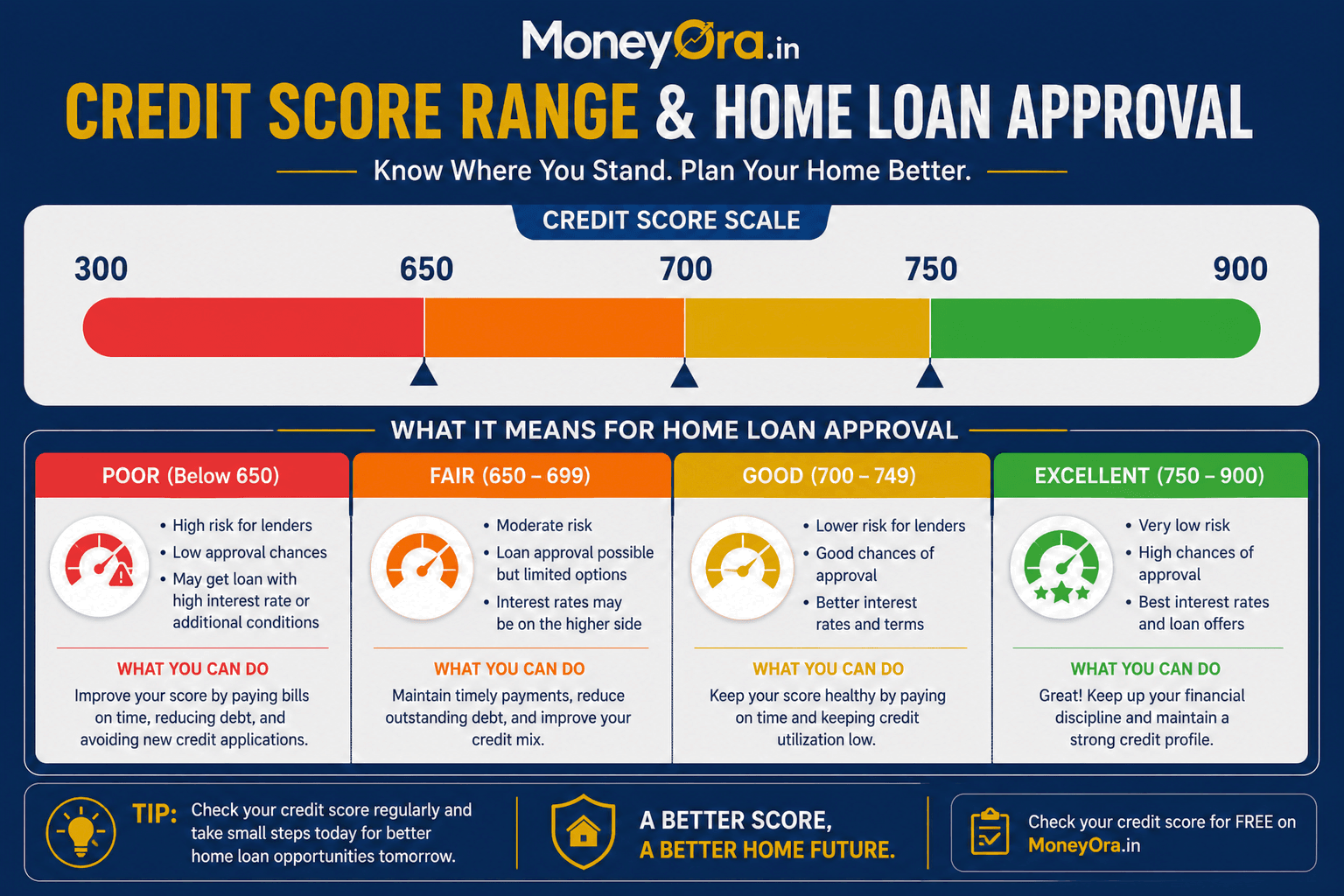

9. CIBIL Score (Credit Score)

Plain meaning: A 3-digit number between 300 and 900 representing your creditworthiness based on past loan and credit card behaviour. Maintained by TransUnion CIBIL and three other RBI-licensed credit bureaus in India.

Why it matters: Most banks require a score above 750 for prime-rate loans. A score of 680 might get you a loan, but at a 1–2% higher interest rate — costing lakhs extra over a 20-year home loan.

Real example: Same loan, same bank, two borrowers. Score 800: 8.5% interest rate. Score 680: 9.8%. On ₹40 lakh over 15 years, that 1.3% difference costs roughly ₹7–9 lakh more in total interest.

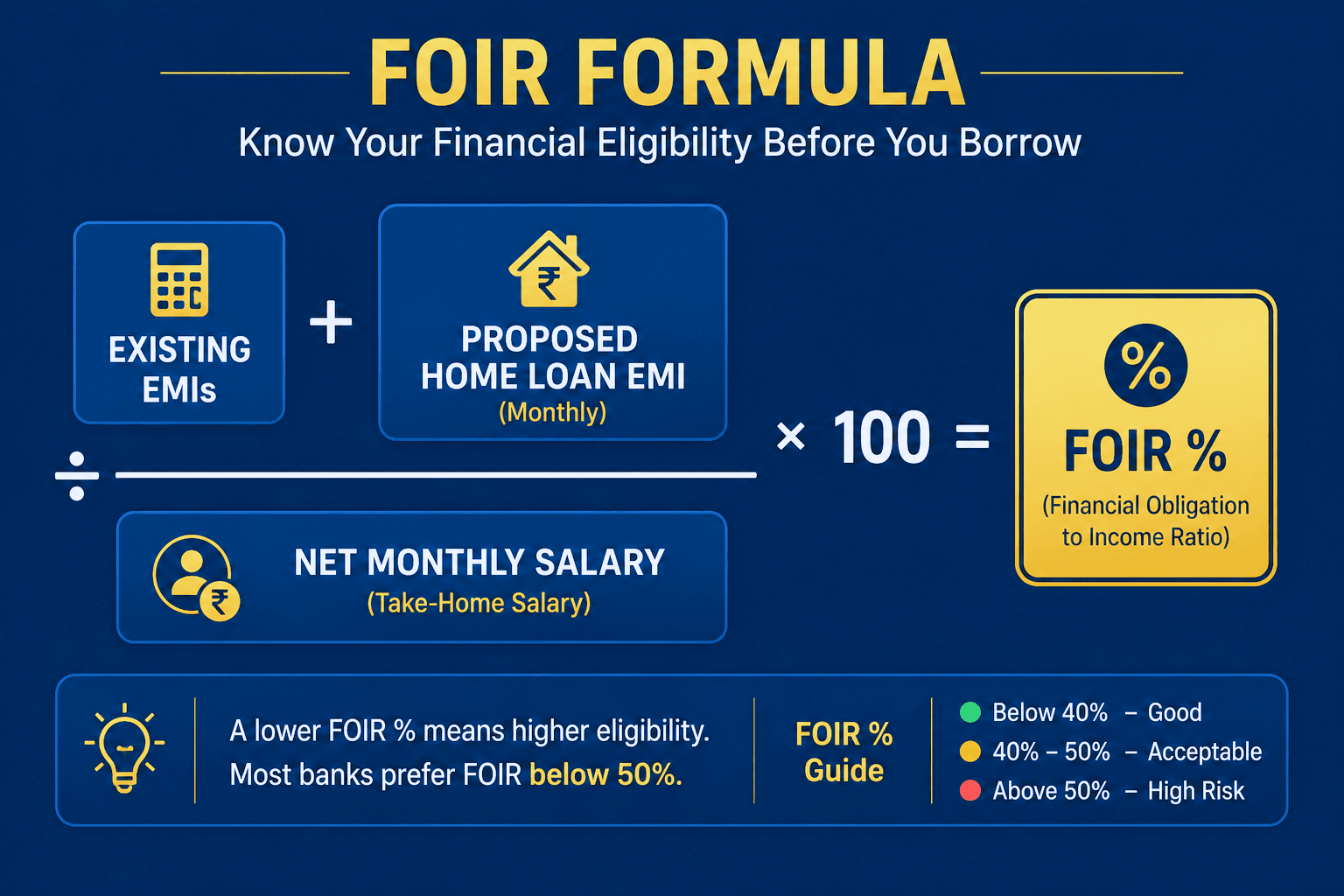

10. FOIR (Fixed Obligation to Income Ratio)

Plain meaning: The percentage of your monthly income consumed by all fixed EMIs and financial commitments combined. Most banks cap this at 40–50% before approving a new loan.

Why it matters: If your monthly income is ₹60,000 and your existing EMIs total ₹25,000, your FOIR is 41.7%. Adding another EMI of ₹12,000 pushes it to 61.7% — above most banks’ comfort zone. Your loan gets rejected even with a good credit score.

Real example: Check your FOIR before applying for a car or personal loan. Calculate what EMI you can actually afford using MoneyOra’s EMI Calculator.

Section 2 — Investment & Returns Financial Terms (11–20)

11. Mutual Fund

Plain meaning: A pooled investment vehicle where many investors contribute money, managed by a professional fund manager who invests in stocks, bonds, or a combination.

Why it matters: Mutual funds let investors access diversified portfolios with amounts as low as ₹500/month. The expense ratio (fund management fee) matters — a 1.5% expense ratio on a 10% returning fund effectively gives you 8.5%.

Real example: The Nifty 50 index fund category delivered approximately 12–14% CAGR over the last 10-year period. Actively managed large-cap funds have often delivered similar or lower returns after expenses. This is why comparing categories matters, not just picking the “top performing” fund from last year.

12. NAV (Net Asset Value)

Plain meaning: The per-unit value of a mutual fund, calculated daily as total assets minus total liabilities divided by the number of units.

Why it matters: Beginners often think a lower NAV fund is “cheaper” or “better.” It isn’t. A fund with NAV ₹15 is not better than one with NAV ₹150. What matters is the fund’s percentage return, not the absolute NAV number.

Real example: Fund A has NAV ₹20 and returned 18% last year. Fund B has NAV ₹200 and returned 14%. Fund A is better despite the lower NAV. This is one of the most common financial terms misunderstood by beginners.

13. SIP (Systematic Investment Plan)

Plain meaning: A method of investing a fixed amount in a mutual fund at regular intervals — monthly being the most common. The investment buys more units when prices are low and fewer when prices are high, smoothing the average cost over time.

Why it matters: SIP removes the need to time the market. ₹5,000/month over 20 years at 12% CAGR grows to approximately ₹50 lakh. The same amount as a lumpsum invested once at the start grows differently depending on entry point. Regular SIP removes that timing risk.

Real example: India had over 9.65 crore active SIP accounts in early 2026, with monthly inflows crossing ₹26,000 crore. Model your own SIP target using MoneyOra’s free SIP Calculator.

14. CAGR (Compound Annual Growth Rate)

Plain meaning: The steady annual growth rate that gets you from a starting value to an ending value over a specified period, assuming compounding. The most honest way to compare investment returns.

Why it matters: Simple returns mislead. A fund that went up 80% one year and down 40% the next isn’t a “20% average” — the CAGR is actually about 4%. Always compare financial products using CAGR, not simple average returns.

Real example: ₹1 lakh grew to ₹2.5 lakh in 8 years. The CAGR is (2.5/1)^(1/8) − 1 = 12.1%. Use MoneyOra’s CAGR Calculator to find the exact rate from any two values.

15. Lumpsum Investment

Plain meaning: Investing a large single amount at once, rather than in instalments. The opposite of SIP.

Why it matters: Lumpsum investing generates higher returns than SIP if timed well (buying at market lows). It’s riskier if timed poorly. Most retail investors are better off in SIP; lumpsum suits investors who have surplus cash and a long horizon.

Real example: ₹10 lakh lumpsum at 12% CAGR for 15 years grows to approximately ₹54.7 lakh. Compare with a SIP of similar total contribution using MoneyOra’s Lumpsum Calculator.

16. Rupee Cost Averaging

Plain meaning: The natural outcome of investing a fixed amount regularly — you buy more units when the price is low and fewer when the price is high, resulting in a lower average cost per unit over time.

Why it matters: This is the core mechanism that makes SIP work in volatile markets. When markets fall, your SIP buys more units. When they recover, those extra units multiply your gains. People who stop SIPs during downturns lose this benefit entirely.

Real example: If you invest ₹1,000/month and the NAV fluctuates between ₹10, ₹12, and ₹8 over three months, your average cost is ₹9.68 — lower than the simple average of ₹10. That difference, compounded over 20 years, is significant.

17. PPF (Public Provident Fund)

Plain meaning: A government-backed, 15-year savings scheme with a fixed interest rate (7.1% for FY2025-26) that offers tax exemption at contribution, on interest earned, and at maturity — called EEE (Exempt-Exempt-Exempt) status.

Why it matters: PPF is one of the very few truly tax-free wealth creation instruments in India. The 15-year lock-in is also a forced savings mechanism that stops impulsive withdrawals from eroding long-term wealth.

Real example: ₹1.5 lakh/year (the annual maximum) invested in PPF for 15 years at 7.1% grows to approximately ₹40.7 lakh — fully tax-free. Model your own corpus using MoneyOra’s PPF Calculator.

18. EPF (Employees’ Provident Fund)

Plain meaning: A mandatory retirement savings scheme for salaried employees in India. Both employee and employer contribute 12% of basic salary each month. Managed by EPFO. Interest rate for FY2024-25: 8.25%.

Why it matters: EPF is the guaranteed retirement base for most salaried Indians. The employer’s 12% contribution is essentially free money. Withdrawing EPF at job changes breaks this compounding — a ₹3 lakh EPF balance at 28, if left to compound at 8.25% until 58, becomes over ₹35 lakh.

Real example: Model your EPF retirement corpus using MoneyOra’s EPF Calculator.

19. NPS (National Pension System)

Plain meaning: A government-run, market-linked retirement savings scheme. Open to all Indian citizens aged 18–70. Contributions are invested across equity, government bonds, and corporate bonds based on your chosen allocation.

Why it matters: NPS offers an additional ₹50,000 tax deduction under Section 80CCD(1B) beyond the standard ₹1.5 lakh 80C limit — available under the old tax regime. At the 30% bracket, that saves ₹15,600 in tax annually, making NPS tax-efficient even before investment returns are counted.

Real example: Estimate your pension corpus at retirement using MoneyOra’s NPS Calculator.

20. SWP (Systematic Withdrawal Plan)

Plain meaning: A facility in mutual funds that lets you withdraw a fixed amount at regular intervals from your existing investment — the reverse of SIP. Used mostly by retirees to create regular income from a lump corpus.

Why it matters: SWP can be more tax-efficient than FD interest for retirees — only the capital gains portion of each withdrawal is taxed, not the full amount withdrawn. This is a less-known benefit of this financial term.

Real example: ₹50 lakh corpus in a balanced fund. SWP of ₹30,000/month. If the fund earns 9% annually, the corpus actually grows while withdrawals are being made for many years before depletion. Model this using MoneyOra’s SWP Calculator.

Section 3 — Loans & Credit Financial Terms (21–28)

21. EMI (Equated Monthly Instalment)

Plain meaning: The fixed monthly payment for a loan, combining both principal repayment and interest. Calculated using the loan amount, interest rate, and tenure.

Why it matters: In early EMIs, most of your payment goes toward interest. Very little reduces principal. This is why prepaying a loan early saves disproportionately large amounts of interest.

Real example: ₹30 lakh home loan at 8.5% for 20 years has an EMI of approximately ₹26,035. The total repayment: ₹62.5 lakh — more than double the borrowed amount. Calculate your exact EMI using MoneyOra’s Home Loan EMI Calculator.

22. Principal

Plain meaning: The original amount borrowed or invested, before any interest is added.

Why it matters: When your bank shows your “outstanding loan balance,” that’s the remaining principal. Your EMI reduces the principal slowly at first and faster toward the end of the loan term. This is called amortisation.

23. APR (Annual Percentage Rate)

Plain meaning: The true annual cost of a loan including all fees, not just the interest rate. Always higher than the stated interest rate because processing fees, insurance charges, and other costs are factored in.

Why it matters: Lenders advertise interest rates. Borrow ₹5 lakh at 12% interest with a ₹10,000 processing fee — the APR is actually 12.7%+. Comparing loans by APR rather than stated rate is the only honest comparison.

Real example: A personal loan with 14% interest and 2% processing fee has an APR closer to 15.5–16%. A BNPL (Buy Now Pay Later) product with “0% interest” often has an APR above 20% once fees are included.

24. Mortgage

Plain meaning: A loan secured against property. If you stop paying, the lender can take possession of the property.

Why it matters: Mortgages (home loans) are typically the largest financial commitment most Indians ever make. Understanding terms like LTV ratio, floating vs fixed rates, and prepayment penalties before signing is not optional — it’s financially essential.

Real example: Most Indian banks offer LTV (Loan to Value) of 75–90% on home loans. A ₹80 lakh property may get an 80% LTV = ₹64 lakh loan. The remaining ₹16 lakh is the down payment you need. Use MoneyOra’s Mortgage Calculator.

25. Collateral

Plain meaning: An asset pledged as security for a loan. If the borrower defaults, the lender takes the collateral.

Why it matters: Secured loans (with collateral) have lower interest rates than unsecured loans (without collateral), because the lender’s risk is lower. Knowing what collateral you have changes which loan products you qualify for and at what rate.

26. Prepayment

Plain meaning: Repaying part or all of a loan before the scheduled due date.

Why it matters: Prepaying even a small amount early in a loan dramatically reduces total interest paid. On a ₹30 lakh home loan at 8.5%, prepaying ₹3 lakh in year 3 can save ₹7–9 lakh in interest and reduce the tenure by 3–4 years.

Real example: Most home loans now allow partial prepayment without penalty under RBI guidelines for floating-rate loans. Check your specific loan agreement before prepaying.

27. Debt-to-Income Ratio

Plain meaning: The percentage of your monthly gross income that goes toward debt payments (EMIs).

Why it matters: Similar to FOIR, this ratio determines whether lenders see you as creditworthy. A high debt-to-income ratio signals financial stress. Keeping it below 35–40% gives you financial flexibility and better loan terms.

28. Moratorium

Plain meaning: A temporary pause in loan repayments permitted by the lender. Interest still accrues during this period.

Why it matters: During COVID-19, RBI offered a 6-month moratorium on all term loans. Many borrowers didn’t realise interest was still running — they came out of the moratorium with a larger outstanding balance than when they entered it.

Real example: Moratorium is not a payment waiver. On a ₹50 lakh loan at 8%, a 6-month moratorium adds approximately ₹2 lakh to your outstanding balance. This is the kind of financial term where misunderstanding is expensive.

Section 4 — Tax & Compliance Financial Terms (29–36)

29. TDS (Tax Deducted at Source)

Plain meaning: Tax deducted directly from your payment before it reaches you. Your employer deducts TDS from salary; banks deduct TDS from FD interest above ₹40,000/year for regular customers (₹50,000 for senior citizens).

Why it matters: TDS is not your final tax liability — it’s an advance payment. If TDS deducted exceeds your actual tax, you get a refund when you file your ITR. If it’s less, you owe more. Not filing ITR means you can’t claim TDS refunds.

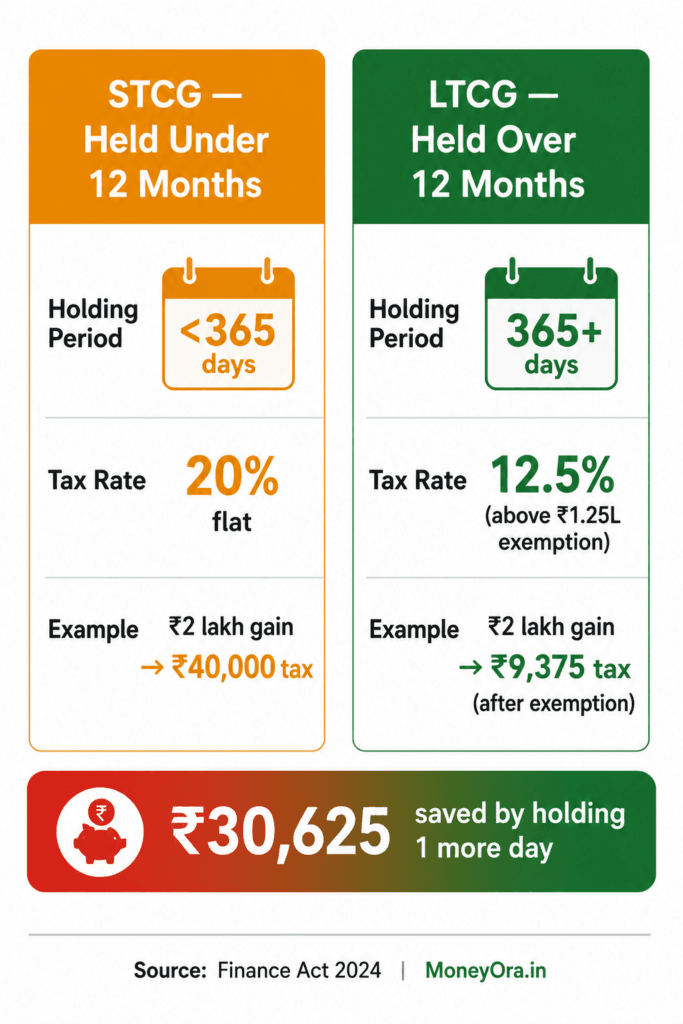

30. LTCG (Long-Term Capital Gains)

Plain meaning: Profit from selling an investment held for over a specified period. For equity mutual funds and stocks: over 12 months. Tax rate in 2026: 12.5% on gains above ₹1.25 lakh per financial year.

Why it matters: The ₹1.25 lakh annual exemption means most retail investors with moderate equity SIP redemptions pay zero LTCG tax. Knowing this changes how you plan large redemptions — spreading them across two financial years can reduce your tax bill significantly.

Real example: You redeem ₹5 lakh from an equity fund in March with ₹1.8 lakh in gains. Tax on ₹0.55 lakh (above the exemption) = ₹6,875. Had you split the redemption across March and April (two different tax years), you may have paid zero.

31. STCG (Short-Term Capital Gains)

Plain meaning: Profit from selling equity assets held for under 12 months. Taxed at 20% flat in 2026 (changed from 15% in the July 2024 Union Budget).

Why it matters: Frequent trading of equity mutual funds within a year is expensive — each redemption under 12 months triggers 20% STCG. Long-term holding is almost always more tax-efficient than active switching.

32. 80C Deduction

Plain meaning: A section of the Income Tax Act that allows deductions up to ₹1.5 lakh per year from taxable income for eligible investments and expenses — including EPF, PPF, ELSS, LIC premiums, and home loan principal.

Why it matters: Under the old tax regime, full utilisation of 80C saves ₹15,600/year at the 10% bracket, ₹31,200 at 20%, and ₹46,800 at 30% (including cess). Under the new regime, this deduction doesn’t apply — regime choice matters enormously.

33. HRA (House Rent Allowance)

Plain meaning: A component of salary that can be partially or fully exempt from income tax if you live in rented accommodation, subject to specific limits.

Why it matters: HRA exemption is calculated as the minimum of: actual HRA received, 50% of basic salary (for metro cities / 40% for others), or actual rent paid minus 10% of basic salary. Missing this exemption by not submitting rent receipts to your employer is a common avoidable tax loss.

34. ELSS (Equity Linked Savings Scheme)

Plain meaning: A type of mutual fund that qualifies for the ₹1.5 lakh 80C deduction. Has the shortest lock-in among all 80C instruments — 3 years per investment, with no upper limit on the total investment (only the deduction is capped).

Why it matters: ELSS gives you both tax saving and equity market exposure. The 3-year lock-in (vs PPF’s 15-year lock-in or LIC endowment’s 10–20 years) makes it the most flexible 80C option for investors comfortable with equity risk.

35. GST (Goods and Services Tax)

Plain meaning: India’s unified indirect tax on the supply of goods and services, replacing multiple older taxes. Structured in slabs: 0%, 5%, 12%, 18%, and 28%.

Why it matters: Financial services attract 18% GST on fees and premiums. Insurance premiums include 18% GST. Mutual fund brokerage on direct transactions through a broker includes GST. Understanding where GST is embedded helps calculate the true cost of financial products.

36. Form 26AS and AIS

Plain meaning: Form 26AS is a consolidated tax credit statement showing all TDS deducted against your PAN. AIS (Annual Information Statement) is a newer, more comprehensive version that shows all financial transactions reported against your PAN — investments, interest, dividends, property registrations, and more.

Why it matters: Always check AIS before filing ITR. If AIS shows income you didn’t declare, the Income Tax Department will. Errors in AIS can be corrected online — but only if you check first.

Section 5 — Stock Market & Trading Financial Terms (37–44)

37. PE Ratio (Price-to-Earnings Ratio)

Plain meaning: The ratio of a stock’s current price to its earnings per share (EPS). A PE of 30 means investors are paying ₹30 for every ₹1 of annual earnings.

Why it matters: PE ratio is the most commonly cited stock valuation metric. A high PE suggests investors expect strong future growth; a low PE might indicate undervaluation or distress. Comparing PE within a sector is more meaningful than comparing across sectors — banks and software companies have structurally different PE ranges.

Real example: Calculate and compare PE ratios for your stock holdings using MoneyOra’s PE Ratio Calculator.

38. Market Capitalisation

Plain meaning: The total market value of a company’s outstanding shares. Calculated as current share price × total shares outstanding.

Why it matters: Market cap determines how a company is classified — large-cap (top 100), mid-cap (101–250), or small-cap (beyond 250) by SEBI definition. Fund categories like “large-cap fund” must invest at least 80% in large-cap stocks. Knowing this helps you understand the risk profile of different funds.

39. Dividend

Plain meaning: A portion of a company’s profits distributed to shareholders. Paid per share. Some companies pay quarterly, semi-annually, or annually; many don’t pay dividends at all.

Why it matters: Dividends are now taxable at the recipient’s income tax slab rate in India (post-2020 change). A high dividend yield doesn’t mean high return — a declining stock price can wipe out several years of dividend income. Estimate dividend income with MoneyOra’s Dividend Calculator.

40. Brokerage

Plain meaning: The fee charged by a stockbroker for executing buy or sell transactions on your behalf.

Why it matters: Frequent trading with high brokerage eats returns. A 0.5% brokerage on both buy and sell means a stock needs to rise 1%+ just to break even, before factoring in STT, GST, and exchange charges. The total cost per trade is almost always higher than the stated brokerage rate.

Real example: Calculate your exact transaction costs using MoneyOra’s Brokerage Calculator before placing trades.

41. Stock Return

Plain meaning: The total gain or loss from a stock investment over a specified period, usually expressed as a percentage. Includes price appreciation and any dividends received.

Why it matters: Measuring your actual return (rather than the stock’s movement alone) requires accounting for dividends reinvested, brokerage paid, and taxes owed. Your “profit” is often lower than the simple price difference suggests. Use MoneyOra’s Stock Return Calculator for accurate figures.

42. Stop Loss

Plain meaning: A pre-set price level at which you automatically sell a stock to limit your loss on a trade.

Why it matters: “I’ll sell if it drops 10%” is not a stop loss — it’s an intention. An actual stop loss order sits with your broker and executes automatically. Many retail investors lose far more than intended because they watch a stock fall without acting, hoping it’ll recover. Set your stop loss before entering a trade, not after. Use MoneyOra’s Stop Loss Calculator.

43. Stock Average (Averaging Down)

Plain meaning: Buying more shares of a stock you already hold at a lower price, reducing your average cost per share.

Why it matters: Averaging down in a fundamentally strong company can improve long-term returns. Averaging down in a failing company can multiply losses. It requires honest assessment of why the price fell, not emotional attachment to your original buy price. Calculate your new average using MoneyOra’s Stock Average Calculator.

44. IPO (Initial Public Offering)

Plain meaning: When a private company first offers its shares to the public on a stock exchange. Investors apply through their broker or bank using an ASBA process.

Why it matters: IPO allotment isn’t guaranteed — oversubscribed IPOs (where applications exceed shares available) are allotted by lottery. IPO price doesn’t equal fair value — some IPOs list at a premium; others fall below the issue price within days. Historical data shows that long-term IPO returns in India are mixed — many underperform the Nifty 50 over 5 years.

Section 6 — Insurance & Retirement Financial Terms (45–50)

45. Term Insurance

Plain meaning: Pure life insurance that pays a lump sum to your nominee if you die within the policy period. No maturity benefit — if you survive the term, no money is returned. The most affordable and straightforward life insurance.

Why it matters: A ₹1 crore term cover for a 30-year-old non-smoker costs approximately ₹8,000–12,000/year. The equivalent endowment or ULIP policy with similar cover costs 5–10× more and delivers poor investment returns. Most financial advisers recommend pure term + separate investment over any bundled product.

46. Sum Assured

Plain meaning: The guaranteed amount an insurance policy pays on claim. For term insurance, this is the cover amount. For ULIPs and endowment plans, this is often different from the maturity amount.

Why it matters: Your sum assured in life insurance should be 15–20× your annual income to adequately cover dependants’ financial needs. Most Indians are significantly underinsured — holding ₹5–10 lakh covers from employer policies that end the day they change jobs.

47. Claim Settlement Ratio

Plain meaning: The percentage of life insurance claims paid out by an insurer in a given year. Published annually by IRDAI.

Why it matters: A high claim settlement ratio (95%+) doesn’t guarantee your specific claim gets paid — claim rejection usually happens due to non-disclosure at purchase, not insurer fraud. But a consistently low ratio (below 90%) is a genuine red flag. Always check this before buying a policy.

48. Floater Policy (Health Insurance)

Plain meaning: A single health insurance policy covering the entire family under one sum insured. The full cover amount is available to any member who needs it, in any year.

Why it matters: A family of four with a ₹10 lakh floater can use the full ₹10 lakh for any one member in one year. Individual ₹2.5 lakh policies for four members cap each person at ₹2.5 lakh. Floater is usually more cost-effective and gives better individual coverage for most families.

49. Waiting Period (Insurance)

Plain meaning: The time after buying a health insurance policy during which specific conditions are not covered. Typically 30 days for general illness, 1–4 years for pre-existing conditions.

Why it matters: Buying health insurance after you’re diagnosed with a condition doesn’t solve the problem — the policy excludes that condition for 2–4 years. The lesson: buy health insurance when you’re healthy and young, before you need it, to minimise waiting period impact.

50. Emergency Fund

Plain meaning: A dedicated pool of liquid savings covering 3–6 months of living expenses, kept in accessible instruments (savings account or liquid fund). Not invested in equity. Not a general savings account that gets spent.

Why it matters: An emergency fund is the difference between a financial inconvenience (medical bill, job loss, car repair) and a financial crisis (forced loan, SIP redemption at a loss, or EMI default). It’s the most important financial term in this list that doesn’t involve any investment return calculation — it’s purely about protection.

How These Financial Terms Connect in Real Life

Reading definitions in isolation only goes so far. Here’s how these financial terms actually chain together in a real financial life scenario:

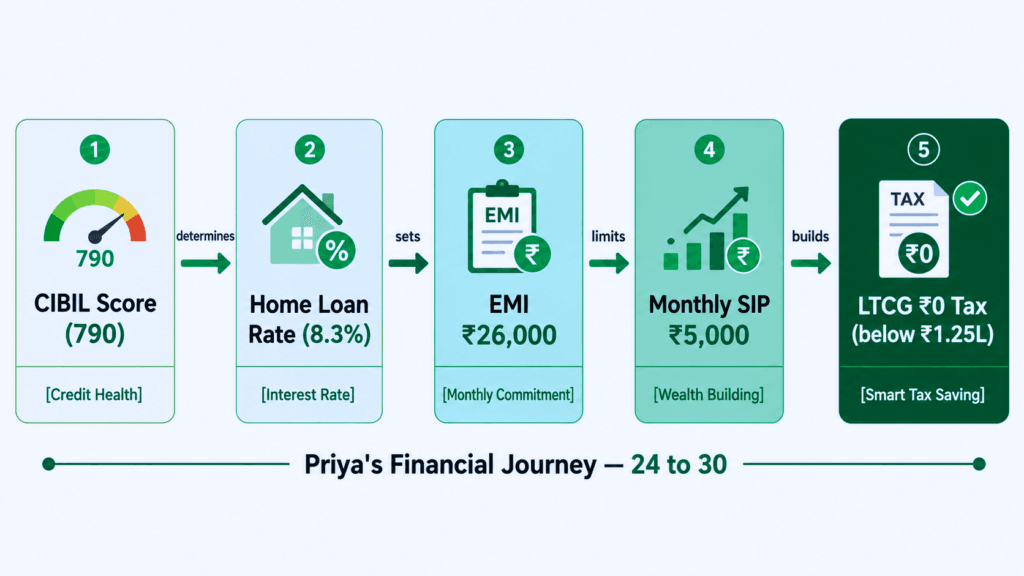

The Financial Terms Chain — Priya’s journey from first job to financial clarity

Priya joins her first job at 24 with a ₹7 lakh CTC. Her take-home after TDS (#29) and EPF (#18) deductions is ₹47,000/month. She checks her FOIR (#10) before taking a personal loan for a laptop — it’s already 28% from an ongoing RD (#7), so she skips the loan.

She builds 3 months of emergency fund (#50) in a liquid fund, then starts a ₹5,000/month SIP (#13) in an ELSS (#34) fund — ticking 80C (#32) and building wealth simultaneously through rupee cost averaging (#16). Her compound interest (#2) works for her, not against her.

At 28, she checks her CIBIL score (#9) before applying for a home loan — it’s 790. She gets an 8.3% rate. She uses MoneyOra’s Home Loan EMI Calculator to confirm the EMI (#21) fits within 35% FOIR. When she sells her ELSS after 3 years, the LTCG (#30) is below ₹1.25 lakh — she pays zero tax. These aren’t separate decisions. They’re one connected plan.

MoneyOra Analysis — Financial Literacy in India in 2026

India’s financial literacy rate of 27% puts it significantly below the global average of 42% and well behind peer economies like China (48%) and South Africa (42%), according to the S&P Global Financial Literacy Survey. This isn’t a surprise to anyone who has watched a bank branch queue — the gap between product availability and product understanding is enormous.

What’s changed in 2026 is the consequence. A decade ago, most retail Indians were underinvested but not misallocated — they kept money in savings accounts and FDs and occasionally lost money on chit funds or “scheme” investments. Today, India has over 9.65 crore SIP accounts, 16 crore demat accounts, and BNPL credit embedded in every e-commerce checkout. The volume of financial product exposure has multiplied; the understanding has not kept pace.

The specific financial terms that cost people the most money in India in 2026 are:

- APR vs interest rate — causing people to take the wrong loan

- LTCG vs STCG — causing premature fund redemptions with unnecessary tax

- CTC vs take-home — causing people to overcommit on EMIs in the first month of a new job

- NAV as quality signal — causing people to choose inferior funds because of a lower number

- Moratorium as forgiveness — causing people to assume their loan was paused without realising interest was accruing

None of these are exotic, advanced financial terms. They’re the basics. The gap between knowing these terms and not knowing them is often the gap between making a good decision and a costly one.

The single most impactful financial literacy intervention for most young Indians in 2026: understand the difference between an interest rate and a return on investment, and the difference between what a product’s marketing says and what the actual cost is. Every other financial term builds from those two.

Risks of Not Knowing Your Financial Terms

- Loan risk: Signing loans without understanding APR, prepayment penalties, or floating rate clauses can cost lakhs over the tenure. Read every term before signing.

- Investment risk: Choosing financial products based on marketing language (“high returns,” “safe investment”) without understanding the underlying mechanics is how mis-selling happens. Ask what the actual return was over 5 years, net of all charges and taxes.

- Tax risk: Not filing ITR, missing TDS refunds, and incorrect LTCG/STCG classification all result in either paying more tax than required or attracting notices. Check AIS (#36) before every ITR filing.

- Insurance risk: Being underinsured is a financial risk most people only discover during a crisis. Sum assured that seems adequate at 28 (₹50 lakh) may not be adequate at 38 with a home loan and dependants. Review annually.

- Inflation risk: Treating FD returns as real returns without adjusting for inflation and tax results in a false sense of wealth accumulation. Model inflation-adjusted returns before assuming any instrument is “safe.”

Financial Terms — The Practical Next Step

Fifty financial terms is not an exhaustive dictionary. It’s a working vocabulary. These are the specific words that appear in loan agreements, investment documents, tax filings, and bank statements — and where not understanding them most consistently costs money.

The goal isn’t to memorise all 50 at once. Read through the section that applies to your current financial decision: taking a loan, starting an investment, planning tax, or buying insurance. Use the terms as a checklist before signing anything.

And when a calculation is involved — whether it’s your EMI, your SIP corpus, your EPF balance, or your CAGR — use the calculators linked throughout this article to turn the theory into actual numbers that apply to your specific situation.

Calculate. Don’t Guess.

SIP • EMI • FD • PPF • NPS • CAGR • EPF — all free, no login required.

Use the free calculator now on MoneyOra.in →MoneyOra Tools

- SIP Calculator — Plan your monthly investments toward any financial goal

- EMI Calculator — Calculate monthly loan payments before you commit

- FD Calculator — Find your exact FD maturity value with any tenure and rate

- RD Calculator — Model recurring deposit growth month by month

- PPF Calculator — Project your tax-free PPF corpus over 15–25 years

- EPF Calculator — See your retirement PF corpus at 8.25% compounding

- NPS Calculator — Model your pension and lump-sum from NPS Tier 1

- Lumpsum Calculator — Project one-time investment growth over any period

- CAGR Calculator — Find the real compound annual growth rate of any investment

- SWP Calculator — Plan regular income from your mutual fund corpus

- Home Loan EMI Calculator — Plan your home loan repayment before signing

- Personal Loan EMI Calculator — Compare personal loan costs before borrowing

- PE Ratio Calculator — Check stock valuation with price-to-earnings analysis

- Stock Return Calculator — Measure actual returns from any stock holding

- Brokerage Calculator — Calculate true transaction costs per trade

- Stop Loss Calculator — Set intelligent loss limits before entering positions

- Stock Average Calculator — Find your average cost when averaging down

- Dividend Calculator — Estimate dividend income from your stock portfolio

- Mortgage Calculator — Plan your total home loan cost including all charges

- All Financial Calculators — Complete MoneyOra calculator hub

MoneyOra Articles

- Financial Planning Meaning — How to build a complete plan using these financial terms

- ₹25,000 Salary Investment Plan — Apply these terms to a real starter salary budget

- ₹100/Day Investment Plan — How compound interest (term #2) works with small amounts

- Hidden Bank Charges — What financial terms like APR don’t always show

- Financial Mistakes Freshers Make — How misunderstanding financial terms costs freshers lakhs

- EPF vs PPF vs NPS — Three retirement financial terms compared for freshers

- Hidden Brokerage Costs — What brokerage and STT mean in real rupee terms

- All Education Articles — MoneyOra’s complete financial literacy library

Frequently Asked Questions — Financial Terms

What are the most important financial terms for beginners in India?

For most Indian beginners, the five most impactful financial terms to understand first are: compound interest (how money grows), EMI (what you actually pay on a loan), CIBIL score (what controls your borrowing ability), CAGR (how to honestly compare investment returns), and TDS (how tax is deducted before you receive income). Misunderstanding any of these five costs real money within the first year of financial activity.

What is the difference between interest rate and APR?

Interest rate is what the lender charges on the principal loan amount annually. APR (Annual Percentage Rate) is the total annual cost of borrowing including interest plus all other charges — processing fee, insurance, administrative costs. APR is always equal to or higher than the interest rate. When comparing loans, compare APR, not just the stated interest rate. A loan at “14% interest” with a 2% processing fee has an APR closer to 15.5–16%.

What is the difference between LTCG and STCG?

LTCG (Long-Term Capital Gains) is profit from equity assets held for over 12 months, taxed at 12.5% (above ₹1.25 lakh exemption in FY2025-26). STCG (Short-Term Capital Gains) is profit from equity assets held for under 12 months, taxed at 20% flat. The 1-day difference between short and long-term holding can change your tax liability significantly on large gains — making holding period one of the most impactful financial terms in equity investing.

What is the difference between SIP and lumpsum investment?

SIP (Systematic Investment Plan) invests a fixed amount at regular intervals (typically monthly) in a mutual fund. Lumpsum investing puts a single large amount in at once. SIP benefits from rupee cost averaging — buying more units when prices are low. Lumpsum benefits from full compounding from day one, but is riskier if the entry point is poor. For most salaried investors, SIP is more suitable because investment timing is automated and matches salary cycles.

What does CIBIL score mean and why does it matter?

A CIBIL score is a 3-digit number between 300 and 900 that represents your credit history. It’s calculated based on your repayment behaviour on loans and credit cards. Scores above 750 typically get the best loan interest rates. A 1–2% interest rate difference from a poor CIBIL score can cost ₹7–10 lakh extra over a 20-year home loan. Building and maintaining a good score requires paying all EMIs and credit card bills on time, every month, without exception.

What is an emergency fund and how much should I have?

An emergency fund is a dedicated pool of liquid savings covering 3–6 months of your total monthly expenses — not income, expenses. If your monthly expenses are ₹35,000, your emergency fund target is ₹1.05–2.1 lakh. It should be kept in a liquid mutual fund or high-yield savings account — accessible within 24–48 hours, not tied up in FDs or equity. Without this, a job loss or medical emergency forces you to break investments or take high-interest loans at the worst possible time.

What is the difference between PPF and EPF?

PPF (Public Provident Fund) is voluntary — you choose to open it, contribute up to ₹1.5 lakh/year, earn 7.1% tax-free, with a 15-year lock-in. It’s available to all Indian citizens regardless of employment. EPF (Employees’ Provident Fund) is mandatory for salaried employees at covered organisations — both you and your employer contribute 12% of basic salary, earning 8.25% tax-free. Both are EEE instruments, but EPF has a higher rate and employer contribution; PPF has the advantage of self-control and continuation beyond employment.

What is TDS and when does it apply?

TDS (Tax Deducted at Source) is the government’s mechanism to collect tax at the point of income, before it reaches you. Your employer deducts TDS from salary every month. Banks deduct TDS on FD interest above ₹40,000/year (₹50,000 for senior citizens) at 10%. TDS is not your final tax liability — it’s an advance payment against your annual tax calculation. If TDS exceeds your actual tax, you get a refund on ITR filing. If it’s less, you pay the balance. Always file ITR to reconcile, even if TDS covers your full liability.

What is the 80C deduction and how much can I save?

Section 80C allows deductions up to ₹1.5 lakh per year from taxable income under the old tax regime. Eligible instruments include EPF, PPF, ELSS mutual funds, LIC premiums, and home loan principal. The tax saving depends on your bracket: 10% bracket saves ₹15,000; 20% bracket saves ₹30,000; 30% bracket saves ₹46,800 (including 4% cess). Under the new tax regime (default from FY2024-25), this deduction is not available — making regime selection one of the most financially significant annual decisions for salaried individuals.

What is the meaning of financial terms like PE ratio and market cap?

PE ratio (Price-to-Earnings) is a stock’s current price divided by its annual earnings per share — indicating how much investors pay per rupee of earnings. A PE of 30 means ₹30 paid for every ₹1 of earnings. Market capitalisation is a company’s total stock market value: share price × total shares. These two financial terms together give a quick valuation picture — a company with a very high PE and very large market cap relative to its earnings growth rate may be expensive; one with a low PE in a stable sector might be reasonably valued.

What does compound interest mean in simple terms?

Compound interest means you earn interest not just on your original money, but also on all the interest you’ve already earned. ₹1 lakh at 7% simple interest earns ₹7,000/year = ₹70,000 in 10 years. At 7% compound interest, the same ₹1 lakh grows to ₹1.97 lakh in 10 years — adding ₹97,000, not ₹70,000. The longer the period, the bigger the gap. This compounding is why starting early matters so much, and why it’s the first financial term most money guides explain.

You’re about to transfer money. You have the account number. You need the IFSC code — and you need to be sure it’s correct. Getting it wrong means the transaction fails, gets delayed, or in rare cases goes somewhere it shouldn’t.

MoneyOra’s IFSC Code Finder solves this in under 10 seconds. Enter any 11-character IFSC code and instantly get the bank name, branch name, full address, MICR code, district, and state — all verified against RBI data. No login, no subscription, no ads.

This page explains exactly how the IFSC code finder works, what details it shows you, which banks it covers, and why verifying before you transfer is worth those extra 10 seconds. You can also use the Bank Details Finder to search by bank name and branch instead of by IFSC code.

Pingback: Hidden Bank Charges: 9 Fees Costing You ₹2,000+ - MoneyOra

Pingback: Salary Investment Plan: The Proven Way to Build ₹1 Crore

Pingback: EPF vs PPF vs NPS: Which Is Best for Freshers? (2026)

Pingback: Financial Mistakes Freshers Make in First Job (2026)

Pingback: Financial Planning Meaning: Brilliant Guide for Indians 2026