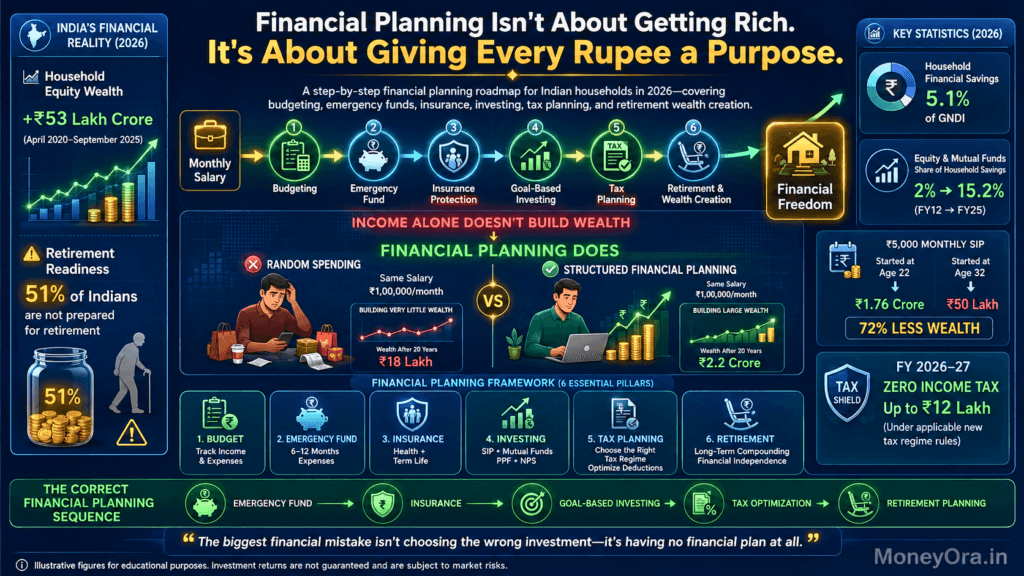

India’s household equity wealth grew by roughly ₹53 lakh crore between April 2020 and September 2025, according to the Economic Survey 2025-26. At the same time, 51% of Indians are unprepared for retirement. Both facts are true — and the gap between them is almost entirely explained by one thing: the absence of a real, personal financial planning process. financial terms that make up a complete plan

Most people think financial planning meaning is about picking mutual funds or saving tax. It’s not. It’s about building a system — one that converts your income, at any level, into the life you actually want. And it looks completely different at ₹25,000/month versus ₹1 lakh/month.

This guide breaks down the true financial planning meaning for Indian households in 2026 — with actual numbers, real goal calculations, instrument-by-instrument comparisons, and the eight mistakes that derail even disciplined planners. Use MoneyOra’s free SIP Calculator alongside this guide to run your own goal projections as you read.

Key Takeaways

- Financial planning meaning = a structured process to convert income into specific life goals through budgeting, saving, investing, protecting, and reviewing — not a one-time product purchase.

- India’s household financial savings rebounded to 5.1% of GNDI in FY24, per RBI data. Equity and mutual fund share in household savings rose from 2% in FY12 to 15.2% in FY25 — a structural shift.

- The most expensive financial planning mistake is not starting. ₹5,000/month at age 22 compounding at 12% becomes ₹1.76 crore by 52. Starting at 32 with the same SIP gets you ₹50 lakh — 72% less.

- Good financial planning has a strict sequence: emergency fund → insurance → goal-based investment → tax optimisation. Most people invert this and wonder why their plan doesn’t work.

- India now has zero-tax income up to ₹12 lakh under the new tax regime (FY 2026-27). Not integrating current tax rules into your financial plan means overpaying tax for no reason.

Financial Planning Meaning — The Real Definition

Quick answer (40 words): Financial planning meaning is the structured process of identifying your income, expenses, goals, and timelines — then systematically using savings, investments, insurance, and tax tools to close the gap between where you are financially today and where you need to be tomorrow.

Here’s what that actually means in practice. Financial Planning Meaningis not:

- Buying an LIC policy at the end of March to save tax

- Moving money into a fixed deposit every year

- Asking a mutual fund agent which scheme is “best” right now

- Making a budget spreadsheet once and never looking at it again

The financial planning meaning that actually builds wealth is a living process. It answers four questions, revisited annually:

- Where am I today? — Net worth, income, expenses, liabilities, existing investments

- Where do I need to be? — Specific goals with specific numbers and timelines

- What’s the gap? — How much do I need to save and invest each month to close it?

- Am I on track? — Annual review to adjust for salary changes, life events, market shifts

That’s the complete loop. And it’s simpler than most people think. The complexity isn’t in the theory — it’s in the consistency.

Financial planning meaning across life stages

| Life Stage | Age Range | Primary Financial Planning Focus |

|---|---|---|

| Early career | 22–30 | Emergency fund + term insurance + first SIP. Build habits. |

| Growth phase | 30–40 | Home, children’s education fund, salary step-up SIPs, tax optimisation |

| Consolidation | 40–50 | Retirement corpus acceleration, debt reduction, portfolio review |

| Pre-retirement | 50–60 | Shift to lower-risk assets, finalise corpus, SWP planning, estate basics |

| Retirement | 60+ | Capital protection, inflation-proof income, healthcare corpus, succession |

Why Financial Planning Meaning Matters More in India Than Anywhere Else

India doesn’t have universal social security. There’s no government pension that automatically replaces your salary at retirement. No unemployment benefit if you lose your job. Healthcare costs are borne almost entirely by individuals.

That makes personal Financial Planning Meaningis not just a wealth-building strategy but a survival strategy. The data backs this up hard.

- Indian household financial savings fell to a multi-decade low of around 5.1% of GNDI in FY24, then partially rebounded, per RBI annual data. Liabilities, meanwhile, rose sharply.

- Only 27% of Indians understand basic financial concepts, compared to a global average of 42%, per financial literacy surveys.

- 51% of Indians have no retirement plan in place — with most expecting children to provide for them, a plan that is increasingly failing as urban migration separates families.

- The share of equity and mutual funds in household financial savings rose from 2% in FY12 to 15.2% in FY25. More Indians are investing. But many are doing so without a plan — which means they buy when markets are high and stop when they fall.

Financial planning meaning in the Indian context also includes accounting for factors most Western guides ignore: joint family financial obligations, education costs running ₹20–50 lakh for professional courses, gold’s role as savings and cultural obligation, and the complete absence of employer-sponsored retirement benefits beyond EPF for most private sector employees.

The urgency isn’t abstract. It’s mathematical. And Financial Planning Meaningis is the only structured answer.

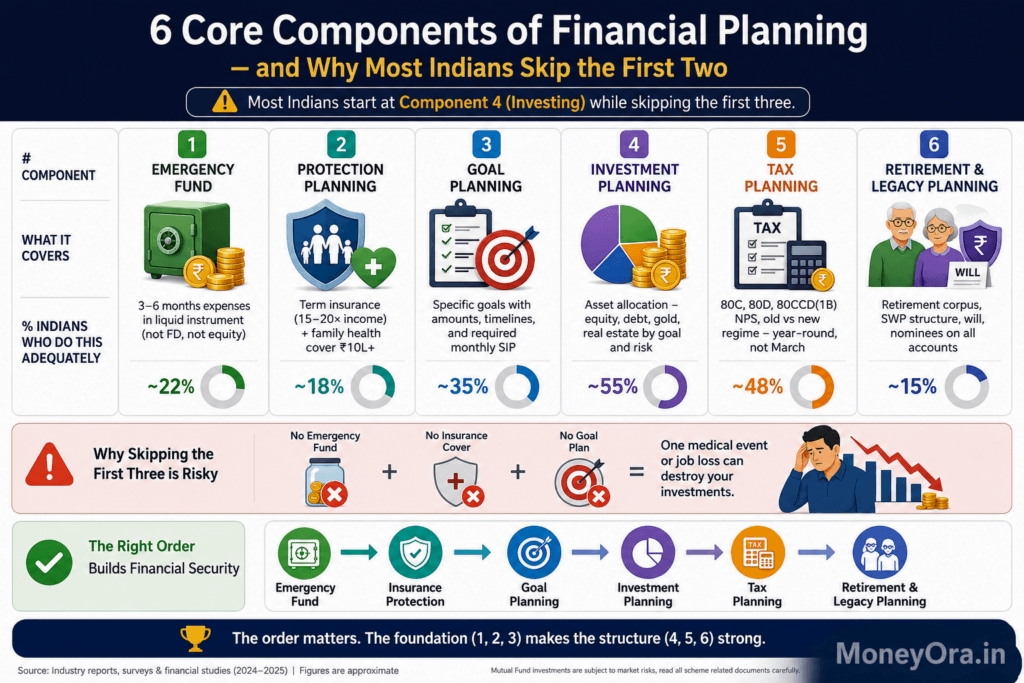

6 Core Components of Financial Planning — and Why Most Indians Skip the First Two

Every complete Financial Planning Meaningis framework has six components. The problem is that most Indians start at component 4 (investing) while skipping 1, 2, and 3 entirely.

| Component | What It Covers | % Indians Who Do This Adequately | |

|---|---|---|---|

| 1 | Emergency Fund | 3–6 months expenses in liquid instrument (not FD, not equity) | ~22% |

| 2 | Protection Planning | Term insurance (15–20× income) + family health cover ₹10L+ | ~18% |

| 3 | Goal Planning | Specific goals with amounts, timelines, and required monthly SIP | ~35% |

| 4 | Investment Planning | Asset allocation — equity, debt, gold, real estate by goal and risk | ~55% |

| 5 | Tax Planning | 80C, 80D, 80CCD(1B) NPS, old vs new regime — year-round, not March | ~48% |

| 6 | Retirement & Legacy Planning | Retirement corpus, SWP structure, will, nominees on all accounts | ~15% |

The order matters. An investor with ₹5 lakh in mutual funds but no emergency fund and no term insurance is one medical event or job loss away from liquidating those investments at the worst time. The emergency fund and insurance aren’t boring — they’re structural.

Why the sequence is non-negotiable

Think of it like building a house. You don’t install the chandelier before the foundation. Emergency fund is the foundation. Insurance is the roof. Everything else — SIPs, PPF, equity — is the furniture. Furniture without a roof gets ruined in the first storm.

The 7-Step Financial Planning Meaningis Process — With Real Indian Examples

Step 1 — Know your current financial position

List everything: monthly take-home salary, all expenses (rent, EMIs, food, utilities, subscriptions), existing savings and investments, all loans outstanding with interest rates and remaining tenure. Net worth = assets − liabilities. Most people have never calculated this number. It’s the most clarifying 30 minutes in financial planning.

Step 2 — Identify your financial goals with specific numbers

“I want to retire comfortably” is not a goal. “I want a retirement corpus of ₹2 crore by age 60, with a monthly withdrawal of ₹60,000” is a goal. The difference is that the second one can be planned. Use MoneyOra’s SIP Calculator to reverse-engineer the required monthly investment for any corpus goal.

Step 3 — Build your emergency fund first

3–6 months of expenses in a liquid fund or savings account — not locked away in FDs or invested in equity. If your monthly expenses are ₹40,000, your emergency fund target is ₹1.2–2.4 lakh. Don’t start any long-term investment until this is in place.

Step 4 — Get protection right

Term insurance: 15–20× your annual income. At ₹8 lakh annual income, that’s ₹1.2–1.6 crore cover. A pure term plan for a 30-year-old costs roughly ₹8,000–12,000/year for ₹1 crore cover. Health insurance: family floater at minimum ₹10 lakh for a family of three, or individual ₹5 lakh. These aren’t investments — they’re protection. Never mix the two.

Step 5 — Goal-based investment planning

Once emergency fund and protection are in place, start investing — one SIP per goal, not one pooled SIP for everything. This keeps your planning clear and prevents you from breaking long-term investments for short-term needs.

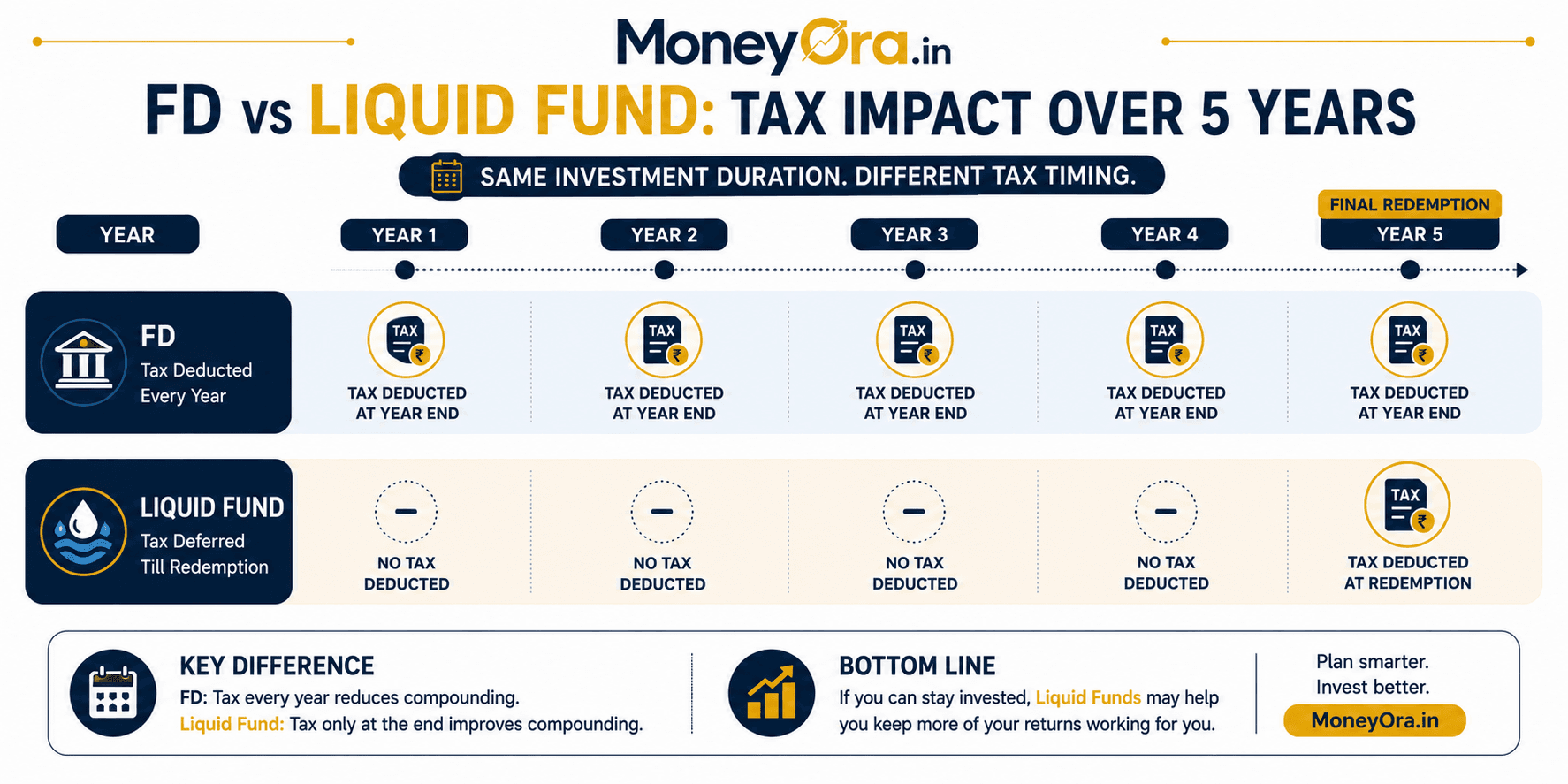

- Short-term goals (1–3 years): Liquid funds, RD, FD — not equity

- Medium-term goals (3–7 years): Balanced/hybrid funds, debt funds

- Long-term goals (7+ years): Equity SIPs, ELSS, NPS Tier 1

Step 6 — Tax optimisation (year-round, not just March)

Under the new regime for FY 2026-27, income up to ₹12 lakh is effectively zero-taxed (with the Section 87A rebate and ₹75,000 standard deduction). Not choosing the right regime based on your actual deductions is one of the most common and most avoidable financial planning mistakes. Compare regimes using MoneyOra’s NPS Calculator for 80CCD(1B) benefit scenarios.

Step 7 — Annual review and rebalancing

A plan is not a set-and-forget instruction. Review it every April: did your income change? Did your goals shift? Is your asset allocation still appropriate for your remaining horizon? Rebalance if equity has drifted more than 10 percentage points from your target allocation.

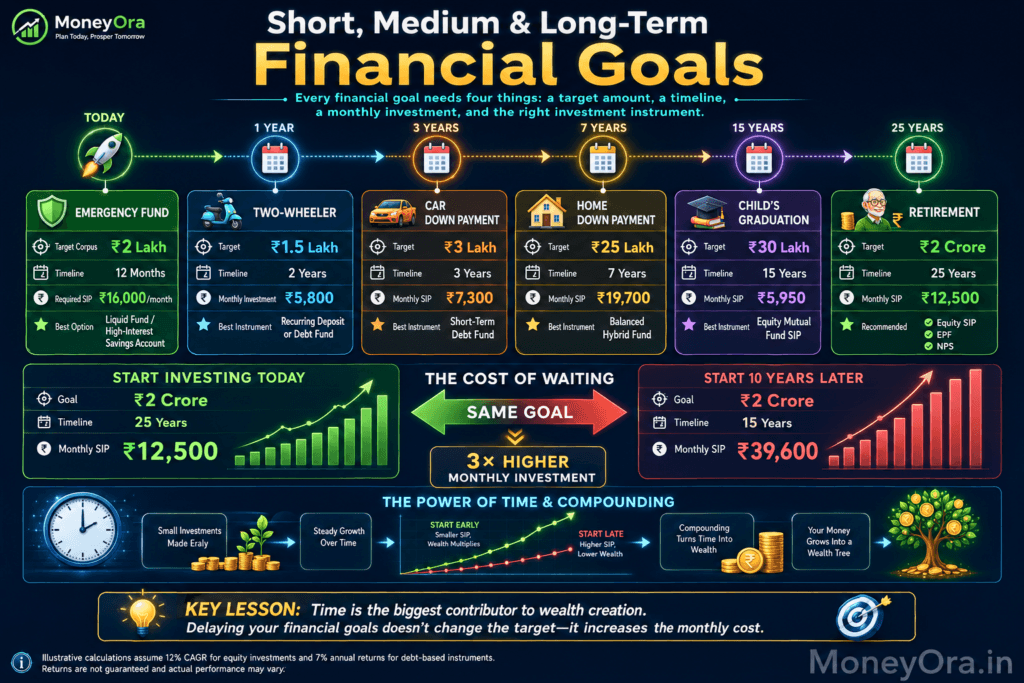

Short, Medium, and Long-Term Goals — With Actual Numbers

The financial planning meaning only becomes actionable when goals have numbers. Here’s how to map common Indian financial goals to investment requirements.

All calculations use 12% CAGR for equity SIP (illustrative, not guaranteed) and 7% for debt/FD instruments. Use MoneyOra’s SIP Calculator and FD Calculator to run your own scenarios.

| Goal | Target Amount | Horizon | Required Monthly SIP | Best Instrument |

|---|---|---|---|---|

| Emergency fund | ₹2 lakh | 12 months | ₹16,000/month | Liquid fund / savings |

| Two-wheeler | ₹1.5 lakh | 2 years | ₹5,800/month | RD or debt fund |

| Car down payment | ₹3 lakh | 3 years | ₹7,300/month | Short-term debt fund |

| Home down payment | ₹25 lakh | 7 years | ₹19,700/month | Balanced hybrid fund |

| Child’s graduation | ₹30 lakh | 15 years | ₹5,950/month | Equity SIP |

| Retirement corpus | ₹2 crore | 25 years | ₹12,500/month | Equity SIP + EPF + NPS |

| Same retirement (started 10 yrs later) | ₹2 crore | 15 years | ₹39,600/month | Equity SIP + PPF |

The retirement row says everything about the financial planning meaning that matters most: the same goal, the same rate — but starting 10 years later requires three times the monthly commitment. Every year you delay doubles the difficulty somewhere down the line.

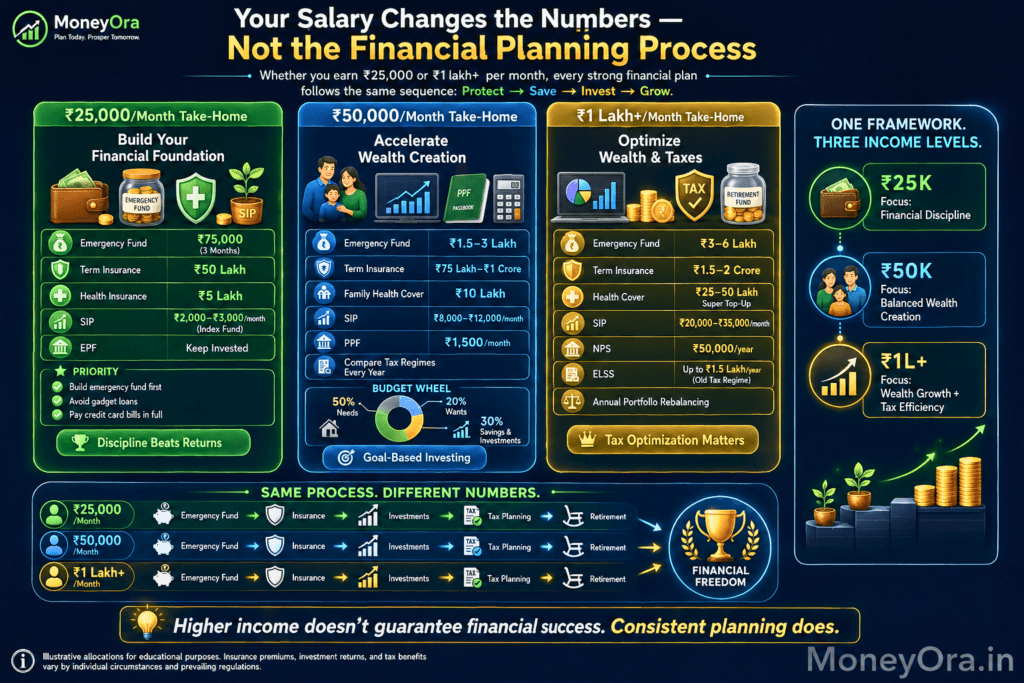

Financial Planning by Salary Level — ₹25K, ₹50K, ₹1L+

The financial planning meaning doesn’t change with salary. But the numbers and priorities do. Here’s a practical framework for three common salary brackets.

₹25,000/month take-home

- Emergency fund target: ₹75,000 (3 months) — build over 6–9 months first

- Term insurance: ₹50 lakh cover at roughly ₹4,500–6,000/year

- Health insurance: Individual ₹5 lakh cover at ~₹3,500–5,000/year

- SIP allocation: ₹2,000–3,000/month in an index fund (Nifty 50) to start

- EPF: Let it run — don’t withdraw at job change

- Priority rule: No equity SIP until emergency fund is 1 month complete

At this salary, the biggest financial planning win isn’t picking the right fund — it’s not taking a personal loan for a gadget, not using credit cards beyond what you repay fully each month, and starting even ₹500 in a SIP. Discipline is the edge, not returns.

₹50,000/month take-home

- Emergency fund: ₹1.5–3 lakh — target before any aggressive investment

- Term insurance: ₹75 lakh–1 crore cover at ~₹6,000–9,000/year

- Health insurance: Family floater ₹10 lakh at ~₹12,000–18,000/year

- SIP allocation: ₹8,000–12,000/month — split between large-cap and flexi-cap

- PPF: ₹1,500/month (₹18,000/year) to start building EEE base

- Tax regime check: Compare old vs new regime with your actual deductions every April

At ₹50,000 take-home, the typical 50-30-20 budget (₹25K needs, ₹15K wants, ₹10K savings) works — but a 50-20-30 (₹10K wants, ₹15K savings) is meaningfully better given India’s retirement corpus requirements. Track your goals using MoneyOra’s PPF Calculator and SIP Calculator together.

₹1 lakh+/month take-home

- Emergency fund: ₹3–6 lakh — complete in 3–6 months

- Term insurance: ₹1.5–2 crore cover at ~₹12,000–18,000/year

- Health insurance: Super top-up ₹25–50 lakh base

- SIP allocation: ₹20,000–35,000/month across large-cap, mid-cap, and international

- NPS Tier 1: ₹50,000/year under 80CCD(1B) if on old regime — saves ₹15,600/year at 30% bracket

- ELSS: ₹1.5 lakh/year to max the 80C bucket (if on old regime)

- Portfolio rebalancing: Annually, if equity drifts beyond 5% from target allocation

At this level, tax optimisation becomes a significant part of financial planning. Use MoneyOra’s EPF Calculator to model how EPF + NPS + ELSS interact to reduce your effective tax outgo.

Which Financial Planning Instruments to Use and When

| Instrument | Risk | Expected Return | Tax | Best For |

|---|---|---|---|---|

| Savings account / liquid fund | Nil | 3.5–7% | As per slab | Emergency fund, parking money |

| Fixed Deposit (FD) | Nil | 6.5–7.5% | As per slab | Short-term goals < 3 years |

| PPF | Nil | 7.1% (tax-free) | EEE — 100% tax-free | 15+ year horizon, guaranteed return |

| EPF | Nil | 8.25% (tax-free) | EEE after 5 years | Retirement — mandatory salaried base |

| NPS Tier 1 | Low-medium | 9–12% (market-linked) | 60% tax-free exit; 40% annuity | Extra retirement savings, 80CCD(1B) tax |

| Equity mutual fund SIP | Medium-high | 10–14% historical CAGR | LTCG 12.5% > ₹1.25L | All goals 7+ years |

| ELSS (Tax-saving MF) | Medium-high | 10–14% historical CAGR | 80C + LTCG 12.5% | Tax saving + long-term wealth |

| Gold (sovereign gold bonds) | Medium | 8–10% (price + 2.5% interest) | Maturity tax-free (SGBs) | 5–8% of portfolio; inflation hedge |

The key rule in financial planning: match instrument risk to goal timeline. Equity is wonderful for long horizons. It’s destructive for short ones. Compare instrument-specific projections using MoneyOra’s PPF Calculator, FD Calculator, and EPF Calculator.

8 Financial Planning Mistakes Indians Make — And How to Avoid Each

Mistake 1 — Treating insurance as investment

ULIP and endowment policies are the most common version of this. They deliver poor insurance coverage and poor investment returns simultaneously — typically 4–5% IRR over 20 years, versus 10–12% from equity SIPs. Buy term insurance for protection. Invest separately. Never mix the two.

Mistake 2 — No emergency fund before investing

When markets crashed in March 2020, investors who had no emergency fund were forced to redeem equity SIPs — often at 30–40% losses — to cover household expenses. The emergency fund protects your investments as much as it protects you.

Mistake 3 — Planning in round numbers without goals

Starting a ₹5,000 SIP because it feels right is not financial planning. Calculate the SIP you actually need. If your child’s engineering degree in 2038 costs ₹25 lakh in today’s money, inflation-adjust it to ~₹48 lakh at 5% inflation. Then work backwards to the required SIP. The number might be ₹4,200 — or ₹8,900. You won’t know without calculating.

Mistake 4 — Stopping SIP during market downturns

SIP’s single biggest advantage is that it buys more units when prices fall. Stopping a SIP in a bear market eliminates that advantage entirely — and restarts at higher prices when sentiment improves. Long-term SIP wealth is disproportionately built during market corrections.

Mistake 5 — Skipping annual financial review

A plan made at 28 with a ₹40,000 salary and no dependents isn’t the right plan at 34 with a ₹1 lakh salary, a home loan, and two children. Financial planning meaning includes annual recalibration. Set a recurring April reminder — review portfolio, insurance coverage, tax regime, and goal timelines.

Mistake 6 — Withdrawing EPF at every job change

This one shows up in data. EPF withdrawal before 5 years makes the entire amount taxable. But worse — a ₹2 lakh EPF balance withdrawn at 28 could have been ₹19+ lakh by 58 at 8.25% compounding. That’s ₹17 lakh in retirement wealth traded for ₹1.8 lakh after TDS. Model the impact on MoneyOra’s EPF Calculator.

Mistake 7 — Over-concentrating in real estate

Real estate isn’t a bad asset — but a 70–80% concentration in one property is terrible financial planning. It’s illiquid, generates no monthly income until sold or rented, has high transaction costs, and is difficult to partially redeem for goal-based needs. Treat property as a lifestyle decision with some investment upside — not as your entire retirement plan.

Mistake 8 — Ignoring inflation in goal calculations

₹1 crore in 2026 and ₹1 crore in 2046 are not the same. At 6% average inflation, you’ll need ₹3.2 crore in 2046 to have the purchasing power of ₹1 crore today. Always inflate your retirement target. Always use the SIP Calculator with the inflation-adjusted corpus, not the nominal number.

MoneyOra Analysis — What 2026 Data Actually Tells Us About Indian Financial Planning

Something genuinely interesting is happening in Indian household finance. The Economic Survey 2025-26 documented a structural shift: equity and mutual fund share in annual household savings rose from 2% in FY12 to 15.2% in FY25. That’s a 7× expansion in 13 years. And unlike previous cycles, this shift held through the 2022 market correction and the 2023–24 volatility period.

This suggests Indian retail investors are maturing. But the same survey data shows that household liabilities have grown sharply alongside savings. Personal loan books at banks and NBFCs expanded at 20%+ annually for several years. Consumer credit is rising faster than financial savings for a meaningful cohort of households.

The picture that emerges is this: a segment of India’s salaried population is doing genuine financial planning — systematic SIPs, EPF contributions, term insurance, and now increasingly NPS. A larger segment is borrowing for consumption (consumer durables, personal loans, credit cards) while starting small investments — but without a plan connecting the two sides of their balance sheet.

The dangerous version of this is the person who has a ₹8,000/month SIP, a ₹15,000/month personal loan EMI at 18% interest, no term insurance, and no emergency fund. They feel like they’re investing. They’re actually treading water.

The core insight: The financial planning meaning most worth understanding in 2026 is the sequencing principle. Debt at 18% costs you more than equity at 12% earns you. You don’t invest your way out of high-interest debt. The mathematically correct order is: clear high-cost debt → emergency fund → protection → goal-based investment. Anyone who inverts this sequence is paying a significant hidden cost.

The opportunity: India’s mutual fund AUM crossed ₹80 lakh crore in April 2026 with 27.53 crore folios. The infrastructure for systematic financial planning is better than it has ever been — low-cost index funds, zero-commission direct plans, EPFO digital access, NPS mobile access, and free calculators. The raw inputs for a complete financial plan have never been cheaper or more accessible. The gap isn’t tools. It’s the plan itself.

Risks Every Financial Planning Must Account For

- Inflation risk: At 6% average inflation, ₹1 crore in purchasing power today requires ₹3.2 crore in 20 years. Every financial plan must use inflation-adjusted targets for goals more than 5 years out.

- Job loss risk: India has no unemployment insurance. A 3–6 month emergency fund is the only buffer. Without it, a job loss forces portfolio liquidation at whatever the market price is at that moment.

- Health risk: A single hospitalisation without insurance can cost ₹5–25 lakh in a private hospital. This is the most common reason Indian families liquidate long-term investments mid-tenure.

- Market risk: Equity mutual funds can fall 30–50% in a bear market. SIP reduces but does not eliminate this risk for goal-based investors with tight timelines.

- Longevity risk: Life expectancy in India has risen to 72 years. A retirement at 60 may need to fund 30+ years of expenses. Most Indian retirement plans underestimate how long the corpus must last.

- Tax law changes: Both tax regimes, LTCG rates, and 80C limits have changed in recent years. Any financial plan must be re-evaluated after each Union Budget. Verify current provisions at the Income Tax Department portal.

- Sequence-of-returns risk: A 30% market fall in the year you retire — with most assets in equity — can permanently impair your retirement income even if markets recover later. Shift to more stable instruments in the 5 years before retirement.

Financial Planning Meaning — Start With One Number, Not a Perfect Plan

The biggest misconception about financial planning meaning is that it requires a complex, fully optimised system from day one. It doesn’t. The most financially successful Indians built their plans incrementally — one emergency fund, then one SIP, then one term plan, reviewed once a year.

If you’re starting today, do three things:

- Calculate your net worth (assets minus liabilities). Write it down. This is your baseline.

- Open a liquid fund and start transferring 20% of each month’s salary into it until you have 3 months of expenses saved.

- Pick one financial goal, calculate the required monthly SIP using MoneyOra’s calculator, and start a SIP for that exact amount.

That’s it. Three steps. Everything else — tax optimisation, rebalancing, NPS, estate planning — comes after these three are in place. Financial planning meaning starts not with the perfect strategy but with the first concrete action.

Plan Your Financial Goals With Free Calculators

SIP • EPF • PPF • NPS • FD • EMI • CAGR — all free, no login required.

Use the free calculator now on MoneyOra.in →Related MoneyOra Tools

- SIP Calculator — Reverse-engineer the monthly SIP for any financial goal

- PPF Calculator — Model guaranteed, tax-free 15-year corpus growth

- NPS Calculator — Project retirement corpus and pension from NPS Tier 1

- EPF Calculator — See what your PF becomes at 8.25% by retirement

- FD Calculator — Calculate FD maturity for short-term goal planning

- RD Calculator — Plan recurring deposits for 1–3 year goals

- Lumpsum Calculator — Project one-time investment growth over any horizon

- CAGR Calculator — Find the real compound annual growth rate of any investment

- SWP Calculator — Plan systematic monthly withdrawals from your retirement corpus

- EMI Calculator — Calculate monthly instalments for any loan before committing

- Home Loan EMI Calculator — Plan home loan within your financial plan

- All Financial Calculators — Complete MoneyOra calculator hub

Related MoneyOra Articles

- ₹25,000 Salary Investment Plan — Build wealth from a starter salary with a complete allocation framework

- ₹100/Day Investment Plan — Small daily investments and what compounding does to them

- Hidden Bank Charges — 9 fees that quietly drain your financial plan

Frequently Asked Questions — Financial Planning Meaning India

What is financial planning meaning in simple terms?

Financial planning meaning is the structured process of identifying where you are financially today and where you want to be in the future — and building a step-by-step plan using budgeting, saving, investing, insurance, and tax tools to close that gap. It’s not about picking products. It’s about building a system that converts your income into specific life outcomes: retirement security, children’s education, home ownership, and financial independence.

What are the main components of financial planning?

A complete financial plan covers six components in order: (1) Emergency fund — 3–6 months of expenses in a liquid instrument; (2) Protection planning — term insurance and health insurance before any investment; (3) Goal planning — specific financial goals with amounts and timelines; (4) Investment planning — asset allocation by goal and horizon; (5) Tax planning — 80C, 80D, 80CCD(1B) and regime selection; (6) Retirement and legacy planning — corpus calculation, SWP structure, will, and nominees.

How much salary should I save for financial planning?

Target 20–30% of take-home salary for savings and investment. At ₹50,000 take-home, that’s ₹10,000–15,000/month. At ₹1 lakh, it’s ₹20,000–30,000. The exact split depends on your goals, debt obligations, and timeline. Start with any amount — even ₹500/month invested consistently from age 22 builds meaningful wealth through compounding. Use MoneyOra’s SIP Calculator to see what your current saving rate becomes at retirement.

What is the difference between financial planning and investing?

Investing is a component of financial planning — not the same thing. Financial planning covers your entire money picture: income, expenses, insurance, debt, taxes, goals, and investments. Investing is what you do after you’ve identified the goal, timeline, and risk appetite. Many people invest without a plan — they pick funds randomly, contribute sporadically, and have no clarity on what the corpus is supposed to achieve. Financial planning meaning starts before the first investment decision.

Is financial planning only for rich people?

No. Financial planning meaning applies at every income level. A person earning ₹25,000/month who has a 3-month emergency fund, a ₹50 lakh term plan, and a ₹2,000/month index fund SIP is better financially planned than a ₹2 lakh/month earner with no insurance, no emergency fund, and a scattered portfolio. The tools are the same. The amounts change. What matters is the structure — goals, protection, systematic investing, and annual review — not the income level.

What is the 50-30-20 rule in financial planning?

The 50-30-20 budget rule allocates take-home salary as: 50% to needs (rent, food, EMIs, utilities), 30% to wants (dining out, entertainment, travel), and 20% to savings and investments. For Indian salaried employees, financial planners often recommend a 50-20-30 version — 30% savings — because there’s no social security, retirement corpus needs are large, and lifestyle costs are rising. Even 10–15% saved consistently from an early age builds significant wealth through compounding.

How do I start financial planning from scratch?

Start with three steps: (1) Calculate your net worth — list all assets and subtract all liabilities. This is your baseline. (2) Build your emergency fund first — 3 months of expenses in a liquid fund before any investment. (3) Pick one specific goal, calculate the required SIP on MoneyOra’s calculator, and start that SIP. Everything else — tax optimisation, NPS, estate planning — can follow once these three basics are in place. Financial planning meaning doesn’t require perfection to start.

What is the importance of financial planning for salaried employees?

For salaried employees, financial planning is critical because India has no universal retirement safety net beyond EPF — which alone rarely funds a comfortable 25–30 year retirement. Without a plan, salary rises typically disappear into lifestyle inflation, and employees reach 55–60 with EPF and perhaps a flat, but no liquid retirement income. Financial planning meaning for salaried employees specifically covers: term insurance, goal-based SIPs, 80C/80CCD optimisation, EPF continuity across job changes, and retirement corpus calculation from the first paycheck.

Old tax regime vs new tax regime — which is better for financial planning?

The new tax regime is default from FY 2024-25 and offers zero tax on income up to ₹12 lakh (with 87A rebate + ₹75,000 standard deduction). But if you have significant deductions — HRA, 80C (EPF+PPF+ELSS = ₹1.5L), 80D health insurance premium, NPS 80CCD(1B) ₹50,000 extra — the old regime may save more tax at higher incomes. The comparison changes every year and with every salary change. Recalculate in April using actual deduction numbers, not assumptions. Never pick a regime without calculating both.

How does inflation affect financial planning?

Inflation is the silent destroyer of financial plans. At 6% average inflation, ₹1 crore in purchasing power today requires ₹3.2 crore in 20 years and ₹5.7 crore in 30 years. Most people set a corpus target in today’s rupees and invest for that — they’ll be significantly short. Always inflate your goal target by the likely inflation rate over your investment horizon. For retirement, use 6% inflation as the base assumption when calculating the required corpus in future rupees.

What is goal-based financial planning?

Goal-based financial planning assigns each investment to a specific goal with a specific timeline and target amount — rather than building one pooled investment portfolio. For example: SIP 1 for child’s education in 14 years, SIP 2 for retirement in 25 years, FD 1 for car in 2 years. This approach prevents short-term needs from disrupting long-term investments, makes tracking progress easier, and creates natural discipline — you know exactly what each investment is for and why you shouldn’t touch it early.

Pingback: Salary Investment Plan: The Proven Way to Build ₹1 Crore

Pingback: 50 Financial Terms Every Indian Must Know (2026) - MoneyOra

Pingback: 50 Financial Terms Every Indian Must Know (2026)