How to Build a ₹10 Lakh Emergency Fund in India: A Real Step-by-Step Plan for 2026

A month-by-month savings plan, instrument comparison, and the tax and mistake traps most guides skip.

Most people don’t think about an emergency fund until the day they actually need one. A car that won’t start. A hospital bill that lands after insurance has already paid its share. A layoff email that shows up on a random Tuesday morning. That is usually when people start paying attention, and by then it is too late to plan calmly.

India doesn’t have unemployment insurance or free universal healthcare the way several other countries do. So your emergency fund is, in a very real sense, your own private safety net. This guide is built specifically for readers who are targeting the ₹10 lakh mark — not the generic “save three months of salary” advice you’ve probably already read a dozen times. If you’re also running SIPs, it’s worth checking your numbers on the SIP calculator before you decide how much to redirect toward this fund first.

Key Takeaways

- ₹10 lakh is not a random number — it’s the right target only for specific income and expense profiles, not everyone.

- Splitting the fund across a savings account, sweep-in FD, and a liquid fund balances access with returns.

- Interest from every one of these instruments is fully taxable at your slab rate — most guides skip this.

- Building it in three phases (₹50,000 → 3 months → full target) keeps the goal from feeling impossible.

- Your emergency fund should always come before your first SIP, not after.

How Much Emergency Fund Do You Actually Need?

Every financial planner repeats some version of the 3-6-12 rule, and honestly, it holds up. The disagreement is really about which multiplier applies to you.

| Employment Type | Recommended Months | Why |

|---|---|---|

| Salaried, stable sector (govt., PSU, large MNC) | 3–4 months | Lower job-loss risk, notice period, severance norms |

| Salaried, private sector | 6 months | Layoffs can happen with little warning |

| Self-employed / business owner | 9 months | Income itself fluctuates, not just expenses |

| Freelancer / gig worker | 9–12 months | No fixed pay cycle, client dependency risk |

| Sole earner with dependents | +1–2 months per dependent | More people relying on one income stream |

Here’s the part most calculators skip: your “expenses” figure should only include the essentials. Rent or home loan EMI, groceries, school fees, insurance premiums, utility bills, and other loan EMIs. Leave out dining out, OTT subscriptions, and vacation budgets — in a genuine emergency, those disappear on day one anyway. Including them just inflates your target and makes the goal feel further away than it really is.

Who Actually Needs a ₹10 Lakh Emergency Fund

A ₹10 lakh emergency fund isn’t a universal goal — it’s a specific number that fits a specific expense profile. Run the math backward and it becomes obvious who this applies to.

- Salaried professional, 6-month rule: ₹10 lakh ÷ 6 ≈ ₹1.67 lakh in monthly essential expenses. That’s typically a dual-income urban household with a home loan, or a single senior professional in a metro city.

- Self-employed, 9-month rule: ₹10 lakh ÷ 9 ≈ ₹1.11 lakh a month. Common for small business owners and consultants carrying business-related fixed costs alongside personal ones.

- Freelancer, 12-month rule: ₹10 lakh ÷ 12 ≈ ₹83,000 a month. This fits a mid-level freelancer or gig-economy professional whose income can vanish for months at a stretch.

If your monthly essentials are lower than these, ₹10 lakh is probably overkill — you’d be locking up money that could otherwise be working in a SIP or PPF. If they’re higher, ₹10 lakh is a starting milestone, not the finish line. “why liquid funds usually beat FDs for emergency money”

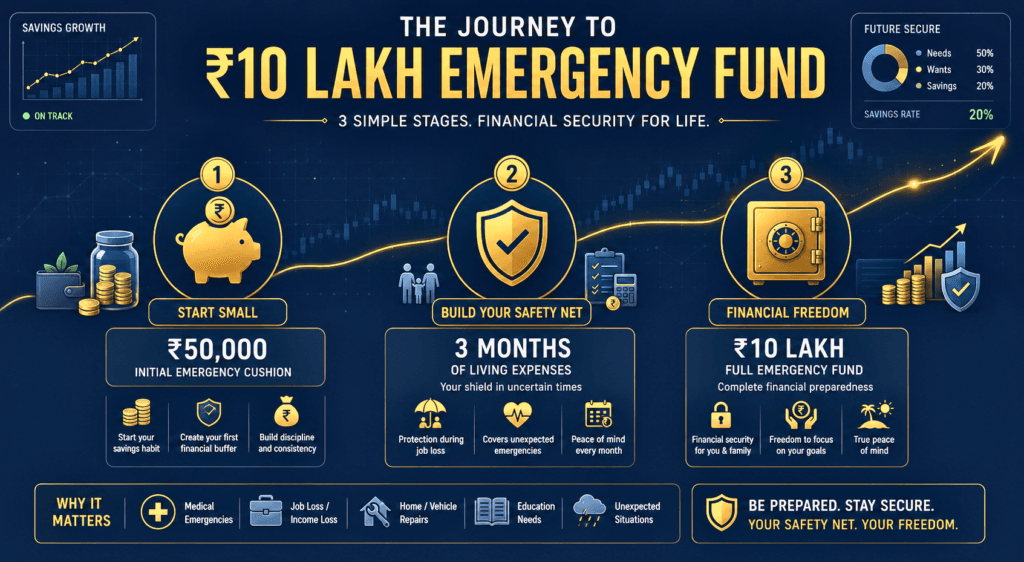

Step-by-Step: Building a ₹10 Lakh Emergency Fund From Zero

Phase 1: The ₹50,000 starter buffer (Months 1–4)

Don’t wait to save the full ₹10 lakh before you start feeling the benefit. A ₹50,000 starter fund already covers a bike repair, a short hospital stay co-payment, or a month without pay. This phase is about proving to yourself the habit works.

Phase 2: Three months of expenses (Months 5–14)

Once the starter buffer is in place, push toward three months of essential expenses. This is usually where the excitement of “saving for it” wears off and it starts feeling like a chore. Automate it — set up a standing instruction the day your salary is credited, before you have a chance to spend it.

Phase 3: The full ₹10 lakh target (Months 15–36)

The last stretch is the slowest, and that’s normal. This is where windfalls matter most — a Diwali bonus, an annual increment, a tax refund, or freelance side income. Redirect all of it here first, before a single rupee goes into your lumpsum investments.

| Timeline | Monthly Saving Needed | Best Suited For |

|---|---|---|

| 12 months | ≈ ₹83,300/month | High earners, aggressive savers, DINK households |

| 18 months | ≈ ₹55,600/month | Dual-income households with moderate fixed costs |

| 24 months | ≈ ₹41,700/month | Single-income salaried households |

| 36 months | ≈ ₹27,800/month | Early-career professionals, self-employed with variable income |

These figures ignore interest for simplicity. In practice, if the bulk of the fund sits in a FD or liquid fund earning 5.5–7% a year, you’ll reach the target slightly faster than the table suggests — a small but real tailwind.

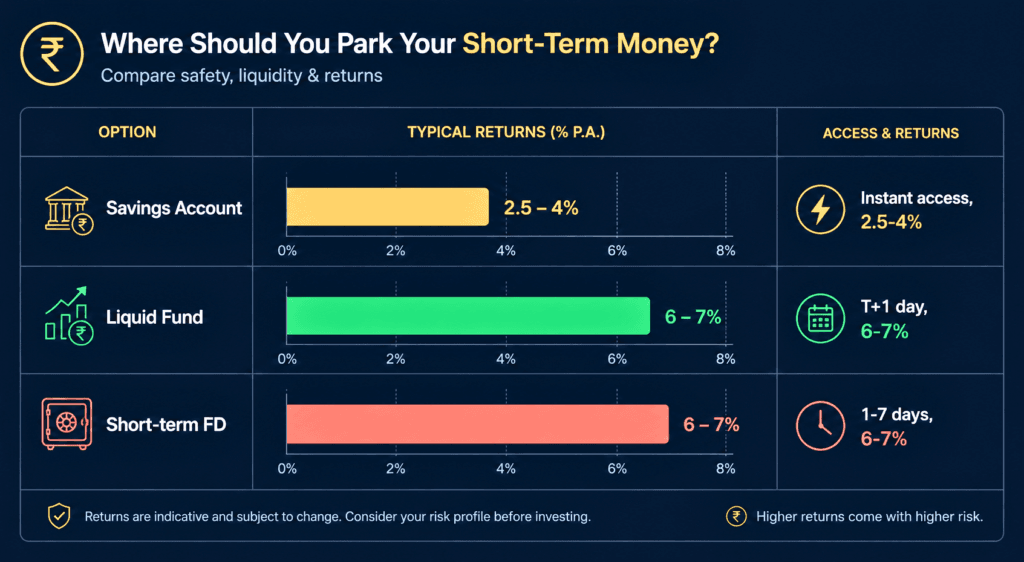

Where to Keep a ₹10 Lakh Emergency Fund

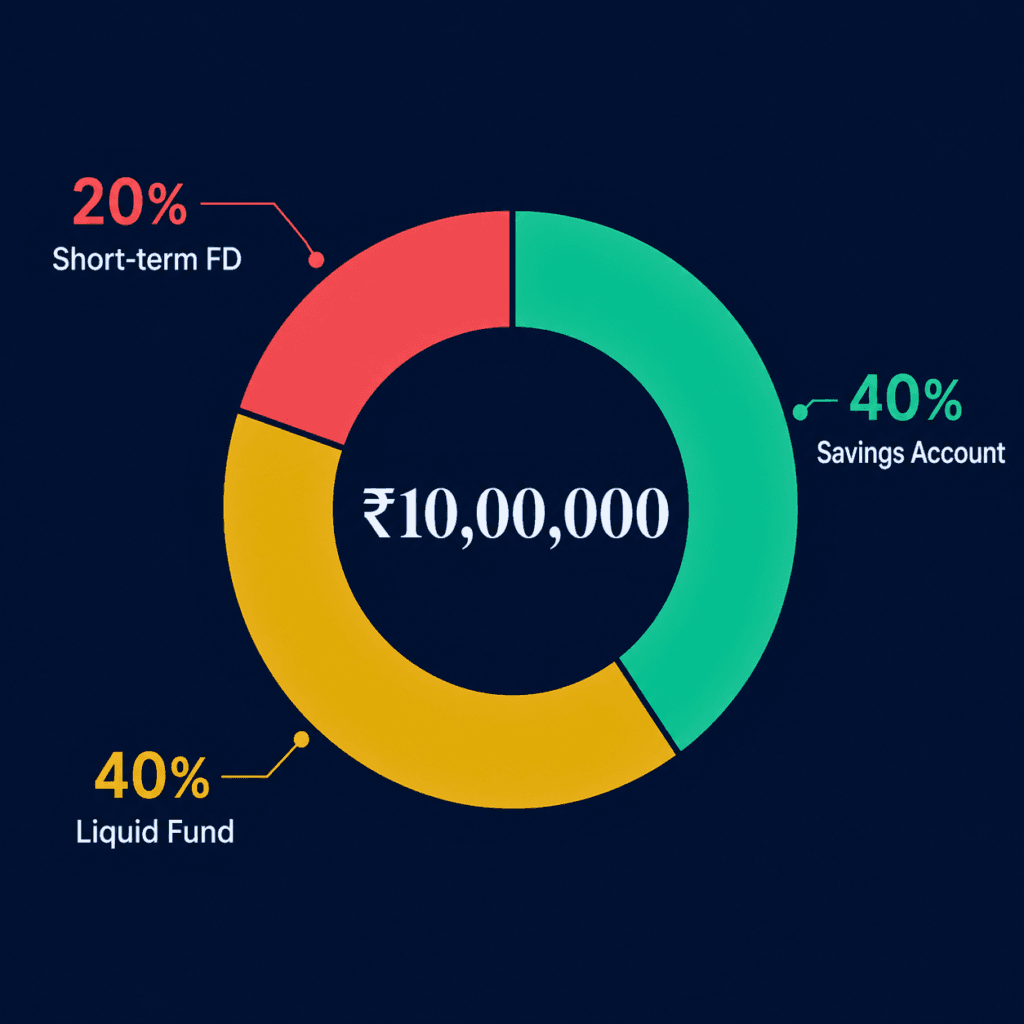

This is the tiered approach that most personal finance advisors — and RBI’s own guidance on deposit safety — point toward. No single instrument does everything well, so you split by purpose.

| Instrument | Typical Returns (2026) | Access Speed | Taxation | Best For |

|---|---|---|---|---|

| Savings account | 2.5–4% p.a. | Instant | Interest taxable; ₹10,000 exemption under Sec 80TTA (non-seniors) | Tier 1 — genuine same-day emergencies |

| Sweep-in / auto-FD | 5.5–6.5% p.a. | Same day, in slabs | Fully taxable as “Income from Other Sources” | Tier 1–2 — a middle ground |

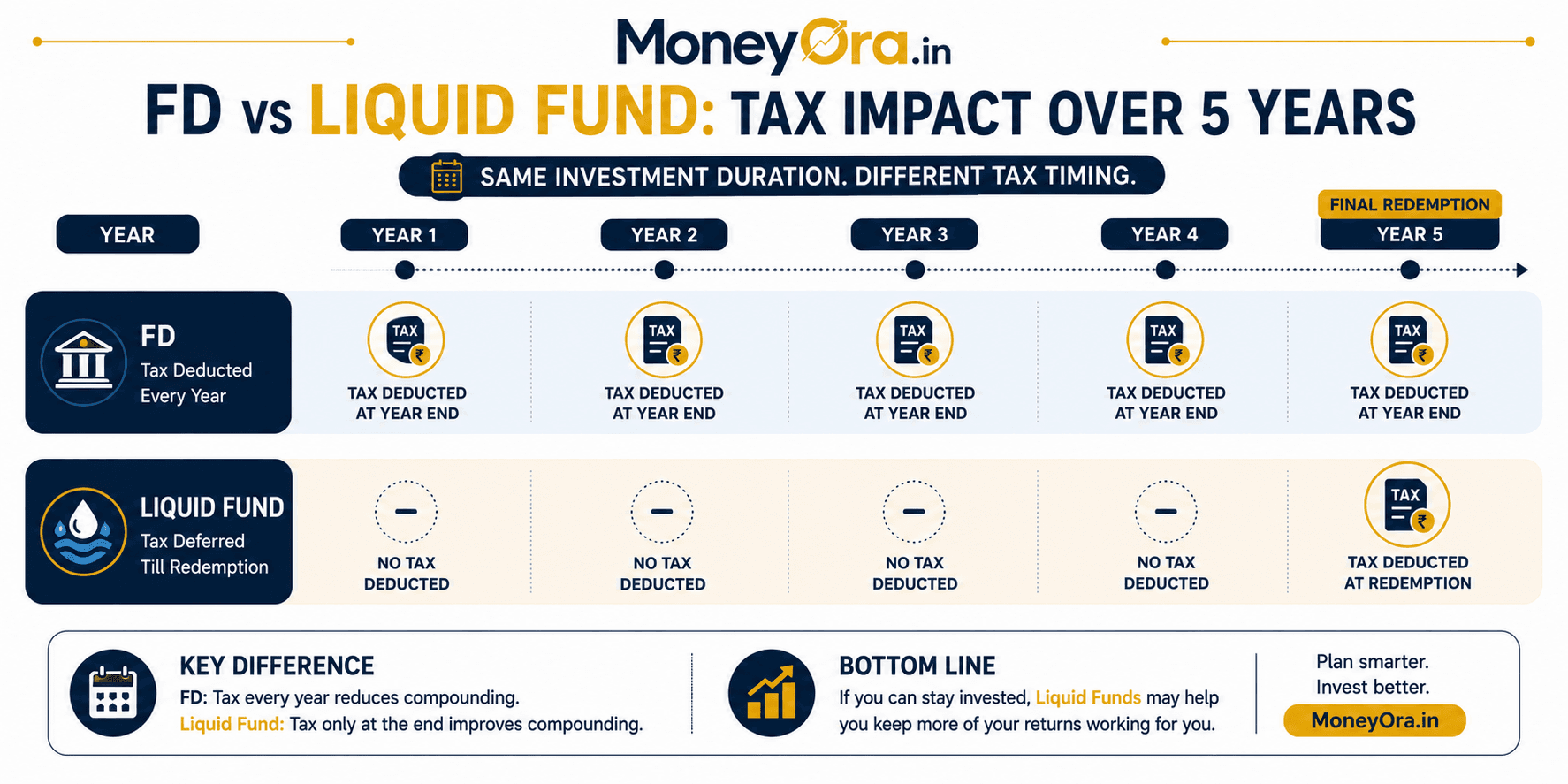

| Liquid mutual fund | 6–7% p.a. (indicative) | T+1 day | Gains taxed at your slab rate (debt fund rules) | Tier 2 — bulk of the fund |

| Short-term FD (no premature penalty) | 6–7% p.a. | 1–7 days, or on maturity | Fully taxable as “Income from Other Sources” | Tier 3 — the portion you hope never to touch |

Two things competitors’ guides routinely leave out. First, DICGC deposit insurance covers only up to ₹5 lakh per depositor per bank — if your entire ₹10 lakh sits in one bank’s FD, half of it is technically uninsured against bank failure. Spreading the fixed-deposit portion across two banks closes that gap. Second, interest income from every one of these instruments is added to your total income and taxed at your slab rate; there’s no special low-tax treatment for “emergency” money, so factor that into your real, after-tax return before assuming a 7% FD beats a 6.5% liquid fund.

Never put emergency money into equities, stocks, or crypto. It defeats the entire purpose — you need the value there and stable exactly when markets tend to be at their most unpredictable.

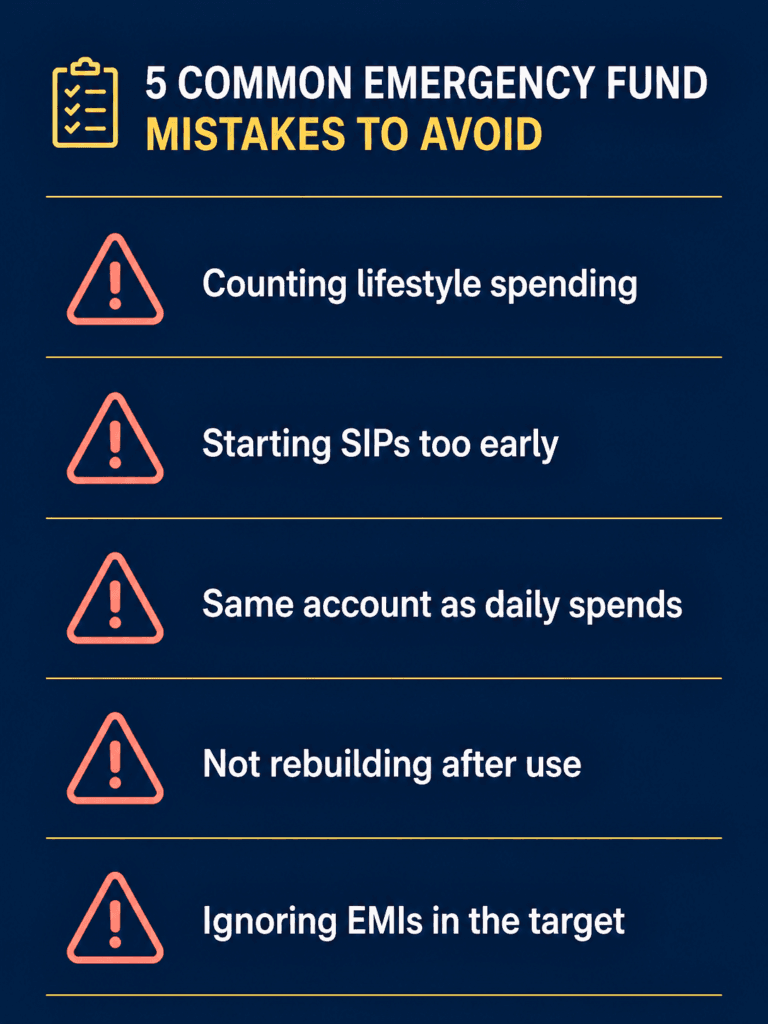

Common Mistakes That Wreck an Emergency Fund

Try This Calculation Yourself

Numbers land better when you run your own. Take your actual monthly essential expenses — rent or EMI, groceries, school fees, insurance, utilities — and run three quick checks on MoneyOra:

- Use the FD Calculator to see how much a lump sum like ₹4 lakh would grow to in 24 months at today’s FD rates.

- Use the RD Calculator to plan a fixed monthly contribution toward Phase 2 and Phase 3 of your roadmap.

- Once your fund is complete, switch to the SIP Calculator to see how quickly your long-term wealth-building can restart.

- If you’re weighing a one-time bonus toward the fund versus investing it, the Lumpsum Calculator shows the trade-off in real numbers.

Related MoneyOra Tools: Also check the PPF Calculator and SWP Calculator once yours is built, since they’re the natural next step after your safety net is in place.

MoneyOra Analysis

Most emergency fund content treats the goal as a single lump number sitting in one account. In practice, the ₹10 lakh figure only makes sense as a moving target that you revisit every year. Healthcare costs in India have been climbing well above headline inflation for several years running, and rent in most metros resets upward every renewal cycle. A ₹10 lakh fund built in 2024 doesn’t buy the same protection in 2026 — treat April as your annual “recalculate the number” month, right after your appraisal cycle typically finishes.

Our independent view: the 40/40/20 split (savings + sweep-in FD / liquid fund / short-term FD) works well for most households, but if you’re within 2–3 years of a major expense you already know is coming — a planned surgery, a child entering college — shift more weight toward the savings-account tier, even at the cost of slightly lower returns. Liquidity should always outrank yield here. That’s the whole point of the exercise.

Expert Perspective

Here’s what actually separates people who keep this fund intact from people who quietly drain it: a written rule, decided in advance, about what counts as an emergency. Job loss, medical crisis, or an unavoidable essential repair — yes. A “too good to pass up” gadget deal or a discounted holiday package — no. Write the rule down before you need it, because in the moment, almost everything can be rationalized as urgent.

Watch two things over the next few quarters: the RBI’s policy stance on the repo rate, since it directly moves FD and liquid fund yields, and your own city’s rent and school-fee inflation, since those are the two line items most likely to push your real target above ₹10 lakh without you noticing.

- Inflation risk: Money sitting in a low-yield savings account loses real purchasing power over time if returns don’t keep pace with rising costs.

- Concentration risk: Holding the entire fund with a single bank exposes the portion above ₹5 lakh to uninsured risk under DICGC norms.

- Liquidity risk: Locking too much into long-tenure FDs with high premature-withdrawal penalties defeats the purpose of an emergency fund.

- Behavioural risk: Easy access (a linked debit card, a same-bank savings account) increases the temptation to use the fund for non-emergencies.

- Tax risk: All interest and gains from savings, FDs, and liquid funds are taxable at your slab rate — a high earner in the 30% bracket keeps meaningfully less than the quoted rate suggests.

Emergency Fund vs Investment: Getting the Order Right

This is where the order of operations genuinely matters. If a market crash and a job loss hit at the same time — and history shows they often do — an investor without one has no choice but to redeem SIP units at a loss to cover rent. An investor with the fund in place rides out the downturn untouched. One of these people is buying units cheap during the crash; the other is being forced to sell them at the worst possible price. It’s the same market event, but a completely different financial outcome, and the only variable that changed was whether that safety net existed first.

If you’re carrying high-interest debt — credit cards at 36–42% or a personal loan above 18% — build a mini ₹50,000–₹1 lakh buffer first, then attack that debt aggressively, and only then complete the rest of this target. Debt at those rates is a bigger drag on your finances than leaving this goal unfinished a little longer. If you’d rather understand what’s quietly eating into your bank balance before you start saving aggressively, our piece on hidden bank charges is a good starting point — plugging those leaks alone can fund a meaningful chunk of Phase 1.

Final Verdict

A ₹10 lakh emergency fund is a strong, specific target for salaried professionals with sizeable metro expenses, self-employed individuals with meaningful fixed costs, and single-income households carrying a large home loan. It isn’t a number to chase blindly — run your own monthly essentials through the multipliers in this guide first. Build it in three deliberate phases, split it across savings, sweep-in FD, and a liquid fund, account for tax on every rupee of interest, and revisit the number every year as costs rise. Get this right, and every SIP, PPF contribution, or lumpsum investment you make afterward is protected from the one event that forces good investors into bad decisions: needing cash at exactly the wrong moment.

Ready to see your own numbers? Run your monthly essentials through the FD and RD calculators to build your personal ₹10 lakh roadmap.

Use the free calculator now on MoneyOra.in

Related reading: Salary investment planning · Brokerage charges guide · Bank Calculators hub · Financial Calculators India

This article is for educational purposes only and does not constitute financial advice. These targets vary by individual circumstances, income stability, and dependents. Interest rates and tax rules cited reflect indicative figures as of 2026 and are subject to change — verify current rates with your bank or the RBI, and consult a SEBI-registered financial advisor or chartered accountant for advice specific to your situation. Source references: RBI monetary policy statements, DICGC, Income Tax Department, and AMFI investor guidelines.

Frequently Asked Questions

Is ₹10 lakh always the right emergency fund target?

No. ₹10 lakh only fits households with roughly ₹1–1.7 lakh in monthly essential expenses, depending on employment type. If your essentials are lower, a smaller emergency fund is enough; if higher, ₹10 lakh is a milestone rather than the final number.

How long does it realistically take to build a ₹10 lakh emergency fund?

Most households take 18 to 36 months, saving between ₹28,000 and ₹56,000 a month depending on income and existing commitments. Windfalls like bonuses and tax refunds can meaningfully shorten this timeline without disrupting monthly cash flow.

Should I invest my emergency fund in mutual funds for better returns?

Only the liquid-fund portion, and even then, keep it capped at around 40% of the total. Equity or hybrid mutual funds carry market risk and aren’t suitable for money you may need on short notice during a genuine emergency.

What expenses should I include when calculating my emergency fund target?

Include only essentials: rent or home loan EMI, groceries, school fees, insurance premiums, utility bills, and other loan EMIs. Exclude discretionary spending like dining out, OTT subscriptions, and travel, since these are the first things to disappear in a real emergency.

Is FD interest from my emergency fund taxable?

Yes. FD and savings account interest is added to your total income and taxed at your applicable slab rate under “Income from Other Sources.” There is no special exemption for money earmarked as an emergency fund, so factor this into your real, after-tax returns.

Can I keep my entire ₹10 lakh emergency fund in one bank?

It’s not advisable. DICGC deposit insurance covers only up to ₹5 lakh per depositor per bank, so splitting the fixed-deposit portion across two banks keeps the full ₹10 lakh protected against bank failure.

Should self-employed professionals target more than ₹10 lakh?

Often, yes. Self-employed individuals and freelancers face income volatility on top of expense volatility, so a 9–12 month buffer is standard advice. If monthly essentials exceed roughly ₹85,000–₹1.1 lakh, the true target moves above ₹10 lakh.

What should I do first — build my emergency fund or start a SIP?

Build the emergency fund first, or at minimum a ₹50,000–₹1 lakh starter buffer. Starting a SIP before this exists risks forced, loss-making redemptions if a job loss coincides with a market downturn, which has happened to Indian investors before.

How often should I revisit my ₹10 lakh emergency fund target?

Review it annually, ideally around April after appraisal season, and after any major life event — marriage, a new home loan, a child, or a career change. Rising rent and healthcare costs mean a fund that was adequate two years ago may already be under-sized.

What is the biggest mistake people make with their emergency fund?

Keeping it in the same account used for daily spending. Without friction, it’s tempting to dip into the fund for near-emergencies like a discounted gadget or a spontaneous trip, which defeats its purpose over time.

Pingback: 100 Per Day Investment: How Wealth Can You Build - MoneyOra