CIBIL Score for Home Loan: What You Actually Need in 2026

Most articles on the CIBIL score for home loans give you one number — 750 — and stop there. That’s not wrong, exactly, but it hides the more useful truth: your actual score requirement depends on which lender you approach, and the gap between a 699 and a 750 can cost you lakhs over a 20-year loan, not just a rejected application.

This guide breaks down what banks and NBFCs actually require in 2026, what a low CIBIL score really costs you in rupees, and a sequenced plan to fix it before you apply — not the generic “pay your bills on time” advice you’ve already read ten times.

Before you apply anywhere, it’s worth checking what loan amount you’d actually qualify for using MoneyOra’s home loan EMI calculator — that number, combined with your score, tells you which lenders are realistically in play. https://www.cibil.com

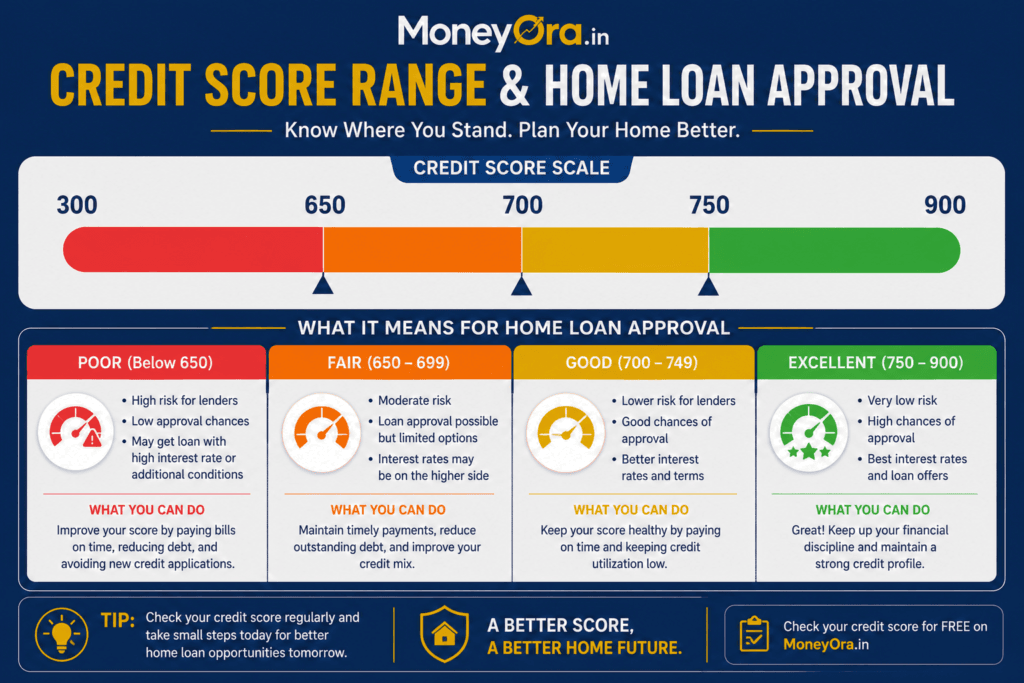

1. What CIBIL Score Do You Actually Need for a Home Loan?

Quick answer: Most Indian banks and housing finance companies want a score of 700–750 for smooth approval, with 750+ getting the best interest rates. Below 650, approval becomes difficult but isn’t automatically impossible.

Your CIBIL score is a three-digit number between 300 and 900, generated by TransUnion CIBIL from your repayment history, credit utilisation, and the CIBIL score and type of loan accounts you hold. It’s not the only thing lenders check — income, job stability, existing EMIs, and the property itself all matter — but it’s usually the first filter applied before anything else is reviewed.

Score bands, in plain terms:

| Score Range | What It Means |

|---|---|

| 750–900 | Excellent — best rates, fastest approval, strongest negotiating position |

| 700–749 | Good — approval likely, but rate may be 0.25–0.75% higher than the best tier |

| 650–699 | Fair — approval possible but with tougher terms, lower loan amount, or added conditions |

| Below 650 | Poor — high rejection risk unless backed by strong income, collateral, or a guarantor |

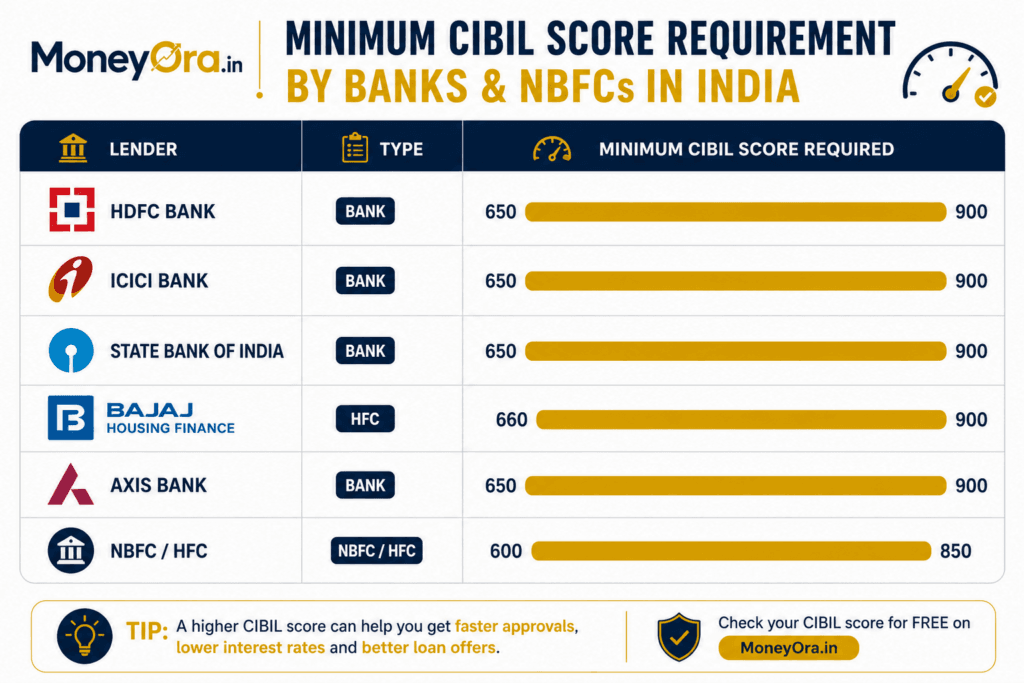

2. Bank-Wise Minimum CIBIL Score for Home Loans (2026)

This is the part most generic guides skip — different lenders genuinely set different bars.

| Lender | Minimum Score for Smooth Approval | Notes |

|---|---|---|

| HDFC | ~720 | Up to 750 preferred for renovation and certain loan types |

| ICICI Bank | 700+ (750+ preferred) | Some flexibility down to 650 via ICICI Home Finance programmes |

| SBI | 700+ for best rates | Will lend in the 650–699 band with tougher terms |

| Bajaj Housing Finance | 725 | 725–749 reviewed alongside income and employment details |

| Axis Bank | 650–750 considered “standard”; 750+ “excellent” | Below 650 needs strong compensating factors |

| Smaller NBFCs / HFCs | Often 650 or below accepted | Higher interest rates and more documentation scrutiny in exchange |

Custom calculation example: A salaried applicant with a ₹50 lakh home loan requirement and a score of 699 versus a score of 750 can see a rate difference of roughly 0.75%. On a 20-year loan, that gap alone can add over ₹3.5 lakh in total interest — a genuinely large cost for the same loan amount, just because of the CIBIL score difference.

Beginner trap: Assuming “my bank told me 700 is fine” means every lender uses the same CIBIL score cutoff. Shop your CIBIL score against 2–3 lenders before assuming you’re stuck with one rate.

Decision framework — which lender tier fits your number:

- 750+: You’re in a position to negotiate. Approach 2–3 large banks and compare processing fees and rate offers directly, since they’ll be competing for your business.

- 700–749: You’ll likely get approved at most major banks, but expect a slightly higher rate than the headline number advertised. Ask specifically what rate applies to your band before signing anything.

- 650–699: Approval is realistic but terms tighten. Be ready to show 6+ months of consistent bank statements and possibly accept a marginally lower loan-to-value ratio.

- Below 650: Treat this as a “fix first, apply later” situation unless you have a strong co-applicant or urgent timeline — see Sections 4 and 5 for the practical path forward.

Documents That Matter Alongside Your Score

A strong number alone doesn’t complete an application. Lenders will typically also want salary slips or ITRs for the last 2–3 years, bank statements showing consistent income, property documents, KYC proof, and existing loan statements if applicable. A high score paired with messy or inconsistent income documentation can still slow down or complicate approval — the two work together, not as substitutes for each other.

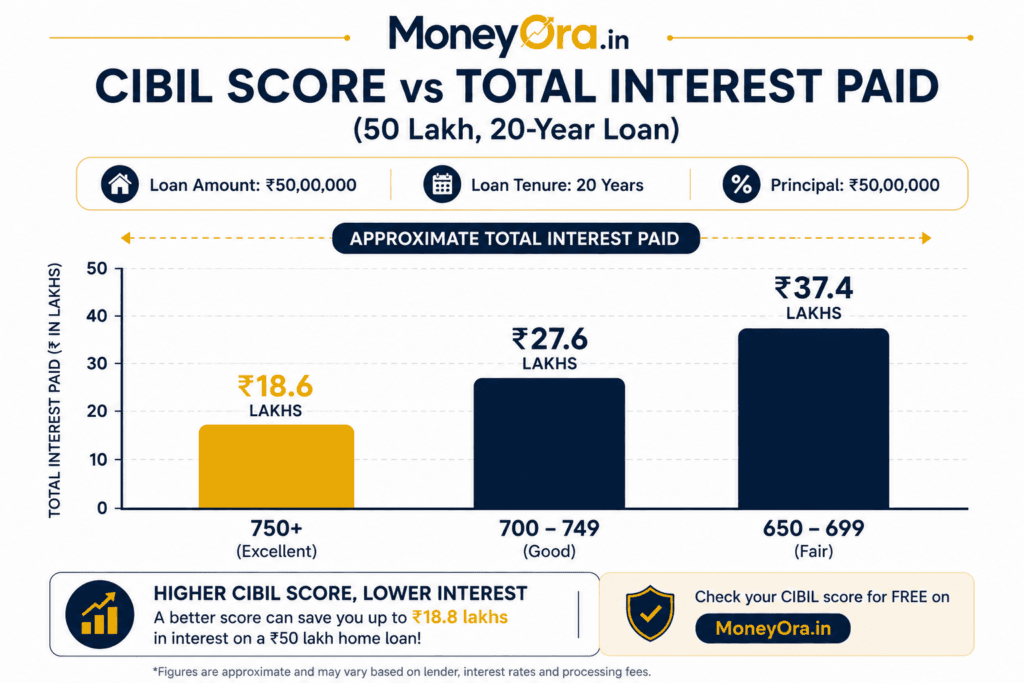

3. How Much Your CIBIL Score Actually Costs You in Interest

This is the section most home loan content skips entirely — everyone talks about approval odds, almost nobody shows the actual rupee cost of a mediocre CIBIL score.

Scenario comparison — ₹50 lakh loan, 20-year tenure:

| CIBIL Score | Approx. Interest Rate | Approx. Total Interest Paid | Difference vs. 750+ Score |

|---|---|---|---|

| 750+ | 8.40% | ₹53.9 lakh | — |

| 700–749 | 8.90–9.15% | ₹58.1–60.2 lakh | +₹4.2–6.3 lakh |

| 650–699 | 9.90–10.5%+ | ₹65.8–71.4 lakh | +₹11.9–17.5 lakh |

Assumptions stated: figures are illustrative, based on typical 2026 market rate spreads by score band; actual rates vary by lender, loan amount, tenure, and individual profile. Always confirm current rates directly with the lender before applying.

The takeaway isn’t “panic if you’re below 750.” It’s that spending three to six months improving your CIBIL score before applying is often the single highest-return financial move available to a home loan applicant — arguably better than negotiating the property price itself.

Real-world scenario: Consider two colleagues at the same company, both applying for a ₹40 lakh home loan in the same month. One had checked their CIBIL score six months earlier, cleared a small overdue credit card balance, and brought utilisation down to 20%. Their score sat at 761 by application time. The other applied without checking anything in advance and discovered a forgotten, unpaid utility-linked loan installment had dragged their score to 668. The first colleague locked in a materially better rate; the second had to either accept a higher rate or delay the purchase by several months to fix the issue first. Neither had done anything dramatic — the only difference was a few months of lead time.

Try This Calculation Yourself: Use MoneyOra’s home loan EMI calculator to plug in your loan amount at two different interest rates — say, 8.4% and 9.9% — and compare the monthly EMI and total interest side by side. Seeing the actual rupee gap tends to make the case for improving your score before applying far more concrete than any percentage figure on its own.

4. Can You Get a Home Loan With a Low CIBIL Score?

Yes, but the path changes. A score below 650 doesn’t automatically mean rejection — it means you’ll likely need one or more of the following to compensate:

- A co-applicant with a strong CIBIL score — lenders assess the combined profile, and a spouse or family member with a healthy CIBIL score can meaningfully shift the outcome.

- A larger down payment — reducing the loan-to-value ratio lowers the lender’s risk exposure.

- Strong, stable income documentation — especially consistent salary credits or, for the self-employed, clean ITRs for the last 2–3 years.

- NBFC or HFC programmes built for lower scores — several housing finance companies specifically underwrite low-score applicants, usually at a materially higher rate in exchange for approval.

Pro tip: If you’re in this position, it’s usually cheaper long-term to spend 3–6 months improving the score first than to lock into a low-score-tier interest rate for 20 years. The math in Section 3 makes this trade-off explicit — run your own numbers before deciding to apply now versus wait and improve.

5. How to Improve Your CIBIL Score Before Applying

Action checklist, roughly in order of impact:

- Clear all overdue dues first. Any active default or overdue account has the single biggest negative pull on your score — settle these before anything else.

- Bring credit utilisation below 30%. If your credit card limit is ₹2 lakh, keep outstanding balances under ₹60,000 at any given time, ideally lower closer to your application date.

- Don’t close old credit cards. A longer credit history helps your score; closing an old, well-managed card can shorten your average account age and hurt more than it helps.

- Avoid new loan or credit card enquiries for 3–6 months before applying. Each hard enquiry causes a small dip, and multiple enquiries in a short window can signal financial stress to lenders.

- Check your CIBIL report for errors and dispute them. Misreported settlements, incorrect account statuses, or someone else’s data appearing on your file are more common than people expect, and disputing them can recover points quickly.

- Maintain a healthy credit mix. A combination of secured credit (like an existing car loan) and unsecured credit (credit cards) managed responsibly over time tends to score better than either extreme alone.

Realistically, minor issues can show improvement in 3–6 months; a genuinely poor score with past defaults often needs 12–24 months of consistent, clean repayment behaviour to recover meaningfully. https://www.cibil.com/freecibilscore

6. Common CIBIL Mistakes That Sink Home Loan Applications

- Applying to multiple banks simultaneously “just to see.” Each application triggers a hard enquiry; several in a short window can drop your score right when you need it stable.

- Settling instead of fully closing old debt. A loan marked “settled” rather than “closed” is read by lenders as a red flag — it signals you didn’t repay in full, and it stays visible on your report for years.

- Ignoring a spouse’s or co-applicant’s poor score. If you’re applying jointly, the weaker profile can drag down the combined assessment even if your own CIBIL score is excellent.

- Assuming salary alone offsets a weak CIBIL score. Lenders weigh both — a high income with a poor credit history is still treated as elevated risk, not overridden by income.

- Checking your score for the first time on application day. By then, there’s no runway left to fix anything; check 3–6 months ahead of a planned application.

- Co-signing a loan for a relative and forgetting about it. As a guarantor or co-applicant on someone else’s loan, their missed payments can show up against your own credit profile too — a common and often overlooked mistake.

Comparison matrix — quick-fix vs slow-fix issues:

| Issue | Typical Fix Time | Action |

|---|---|---|

| High credit utilisation | 1–2 months | Pay down balances, request a limit increase |

| A single missed payment (recent, minor) | 3–6 months | Resume on-time payments consistently |

| Multiple recent hard enquiries | 3–6 months | Pause new applications, let the dip age out |

| Settled (not closed) old account | 12–24 months | Where possible, negotiate to reclassify as closed; otherwise wait it out |

| Active default or long overdue account | 12–24 months | Clear the dues fully first — this is non-negotiable before anything else helps |

7. Home Loan Without a CIBIL Score: First-Time Borrowers

A surprisingly common concern: what if you’ve never taken credit before and simply don’t have a CIBIL score yet? This isn’t the dead end many first-time buyers assume.

Lenders can still assess first-time borrowers using income stability, employment history, bank statement patterns, and existing financial obligations instead of a credit score. Options that specifically help here include:

- Adding a co-applicant with an established, healthy credit profile, which strengthens the combined assessment.

- Government-backed schemes like Pradhan Mantri Awas Yojana (PMAY), which are designed partly with first-time, thin-credit-file borrowers in mind.

- Bank programmes built for new-to-credit applicants, which some lenders offer specifically to avoid excluding otherwise creditworthy first-time buyers.

Real-world use case: A young salaried professional buying their first home with no prior loans or credit cards isn’t necessarily “risky” from a lender’s point of view — they’re simply unscored. Clean, consistent salary credits and a stable job history often do the heavy lifting here in place of a CIBIL number. https://pmaymis.gov.in

8. MoneyOra Analysis: What RBI’s 2026 Reporting Changes Mean for You

Reserve Bank of India guidance pushing banks and NBFCs toward faster, more frequent credit reporting has a practical consequence most borrowers haven’t fully absorbed yet: a payment delay now reflects on your credit file sooner than it used to. Under earlier reporting cycles, a borrower might have a few extra weeks of buffer before a missed payment showed up; that buffer is shrinking.

For home loan applicants specifically, this cuts both ways. On the downside, there’s less room for a slip-up to go unnoticed before you apply. On the upside, positive repayment behaviour — clearing dues, reducing utilisation — should also start reflecting in your score faster than in previous years, which is good news if you’re actively working to improve your number before an application.

Assumptions stated: this reflects general regulatory direction reported industry-wide as of early 2026 and is not a substitute for checking current RBI notifications or your specific lender’s reporting cycle. https://www.rbi.org.in

9. Risks to Consider

- Rate risk: The rates cited in Section 3 are illustrative and change with RBI policy rate movements; always confirm current rates directly with the lender.

- Multiple-enquiry risk: Shopping around for the best rate is sensible, but each application is a hard enquiry — space out applications and avoid applying to more than 2–3 lenders in a short window.

- Over-leveraging risk: A higher sanctioned loan amount from a strong score doesn’t mean you should borrow the maximum — keep total EMI obligations comfortably below 40–50% of net monthly income.

- Settlement-vs-closure risk: A “settled” account can quietly undermine an otherwise strong score; always fully close old debts rather than settling if you can afford to.

- Documentation risk: Even with a good CIBIL score, incomplete or inconsistent income documentation (especially for self-employed applicants) can delay or derail approval independent of the credit score itself.

This is general educational information, not personalised financial or credit advice — actual loan terms, eligibility, and required scores vary by lender and individual profile. https://investor.sebi.gov.in

There’s no single magic CIBIL number that guarantees approval everywhere, but the pattern is consistent: 750+ gets you the best terms nearly everywhere, 700–749 keeps most doors open at a slightly higher rate, and below 650 means you’ll need a stronger supporting profile or a specialised lender. If your CIBIL score isn’t where you want it yet, the math in this guide makes a strong case for spending a few months fixing it before you apply — the interest savings alone are usually worth the wait. Use the free calculator now on MoneyOra.in.

FREQUENTLY ASKED QUESTIONS

1. What is the minimum CIBIL score for a home loan in India? Most banks and housing finance companies want a score of 700–750 for smooth approval, with scores above 750 qualifying for the best interest rates. Below 650, approval becomes harder but some NBFCs and HFCs still consider applicants with strong income or a co-applicant.

2. Does CIBIL score affect my home loan interest rate? Yes, significantly. A score of 750+ can get you materially lower rates than a score in the 650–699 range — on a ₹50 lakh, 20-year loan, that gap can mean over ₹10 lakh in extra interest over the loan term.

3. Can I get a home loan with a CIBIL score below 650? It’s possible but harder. You’ll likely need a co-applicant with a stronger score, a larger down payment, solid income documentation, or an NBFC/HFC programme specifically built for lower-score applicants, usually at a higher interest rate.

4. How can I improve my CIBIL score before applying for a home loan? Clear overdue dues first, keep credit utilisation below 30%, avoid new loan enquiries for 3–6 months, don’t close old credit cards, and check your credit report for errors to dispute. Minor issues can improve in 3–6 months; past defaults often take 12–24 months.

5. Is CIBIL score mandatory for a home loan? It’s not a strict legal requirement, but nearly all banks and most NBFCs check it as their primary risk-assessment tool. First-time borrowers without a credit history can still qualify based on income, employment stability, and sometimes a co-applicant.

6. What CIBIL score is needed for a ₹50 lakh home loan specifically? The score requirement doesn’t usually change with loan amount, but the interest-rate impact gets larger in absolute rupee terms on bigger loans — the same 50-point score gap that costs a few lakh on a small loan can cost significantly more on a ₹50 lakh loan over 20 years.

7. Do multiple loan applications hurt my CIBIL score? Yes. Each application triggers a hard enquiry, and several enquiries in a short period can signal financial stress to lenders and lower your score. It’s better to shortlist 2–3 lenders rather than applying broadly.

8. Can a co-applicant help if my CIBIL score is low? Yes. Lenders assess the combined financial profile in a joint application, so a co-applicant with a strong credit history and stable income can meaningfully improve approval chances and loan terms even if your own score is weak.

9. How long does it take to improve a CIBIL score before a home loan application? Minor fixes — clearing a small overdue balance, lowering utilisation — can show improvement within 3–6 months. A history with actual defaults or settlements typically needs 12–24 months of clean, consistent repayment to recover meaningfully.

10. Is a settled loan account bad for a home loan application? Yes, more than most borrowers expect. A “settled” status (rather than “closed”) signals you didn’t repay the full amount owed, and lenders often treat it as a red flag even years later. Fully closing debts, rather than settling them, protects your score better long-term.