A salary investment plan is a structured approach to allocating a portion of your monthly salary into investment instruments — like SIP, PPF, or EPF — to build long-term wealth systematically.

The big question most salaried Indians have: can ₹25,000 per month actually get you to ₹1 crore?

Yes. And this article shows you exactly how — with real numbers, three investor scenarios, and every calculator you need to verify it yourself.

The Real Question Behind This Search

Most people searching this topic are not just curious about math.

They earn ₹25,000 a month. Rent is due. Groceries are expensive. And someone told them to invest in mutual funds.

They want to know: is it even worth starting? Or is ₹1 crore a goal only for people earning ₹1 lakh+?

The honest answer: it depends entirely on when you start and how consistent you stay. financial planning mistakes to avoid

This article gives you the exact numbers — three real scenarios, a step-by-step allocation, and the tax math most guides skip.

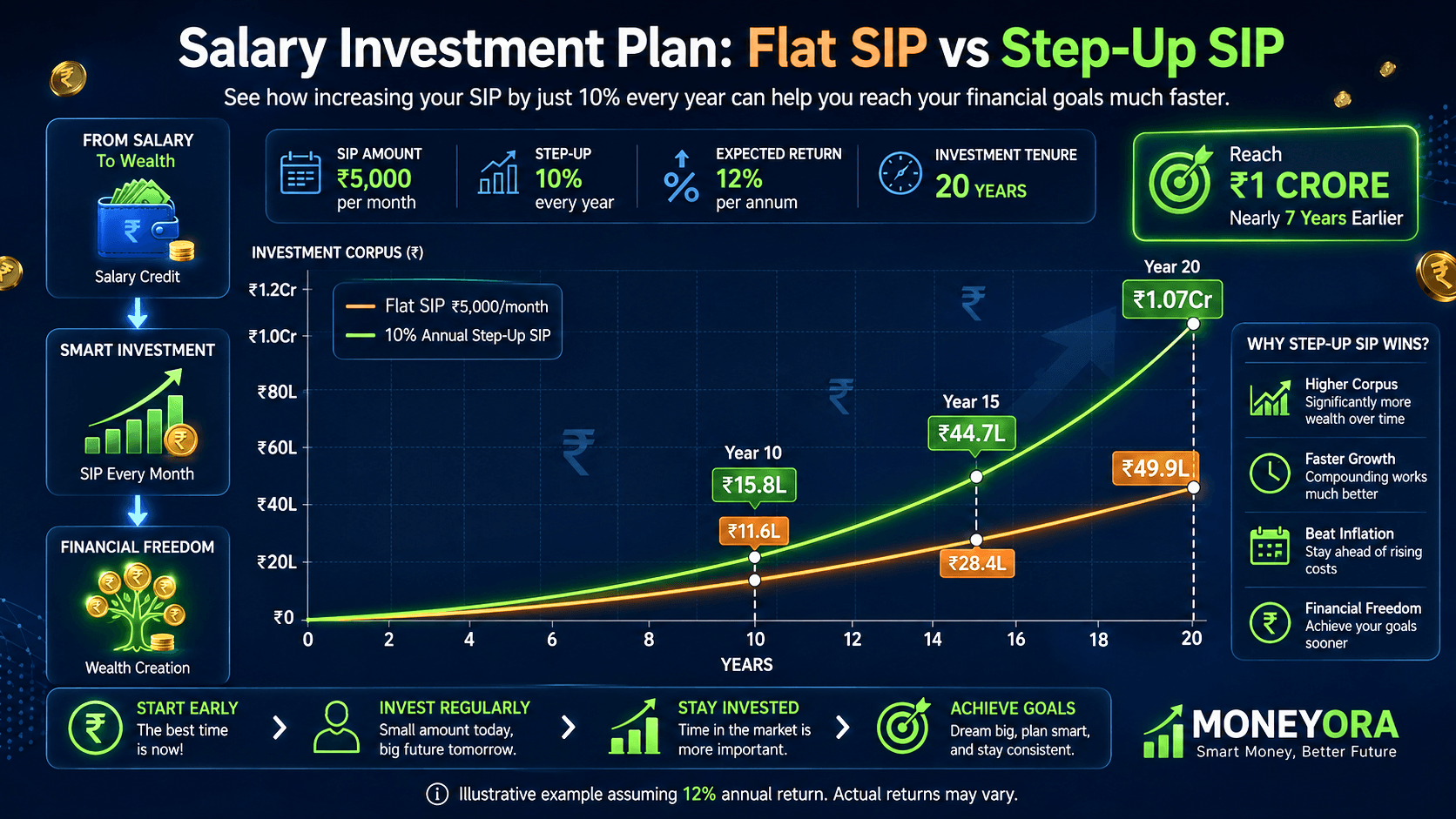

Flat SIP vs Step-Up SIP — the 7-year difference on the same starting amount

Flat SIP vs Step-Up SIP — the 7-year difference on the same starting amount

What Is a Salary Investment Plan?

A salary investment plan is a monthly budgeting and investment system where you divide your take-home salary into fixed buckets — expenses, emergency fund, and investments — and automate the investment portion so it happens before you can spend it.

The core idea: pay yourself first, spend what is left.

At ₹25,000 per month, this is not just possible. It is the single most effective wealth-building move available to most young Indians.

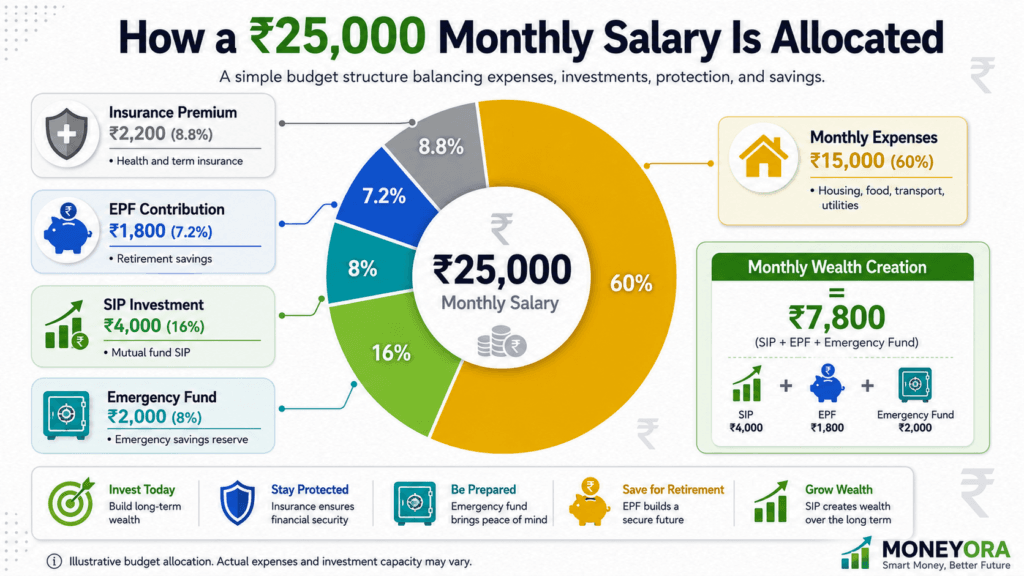

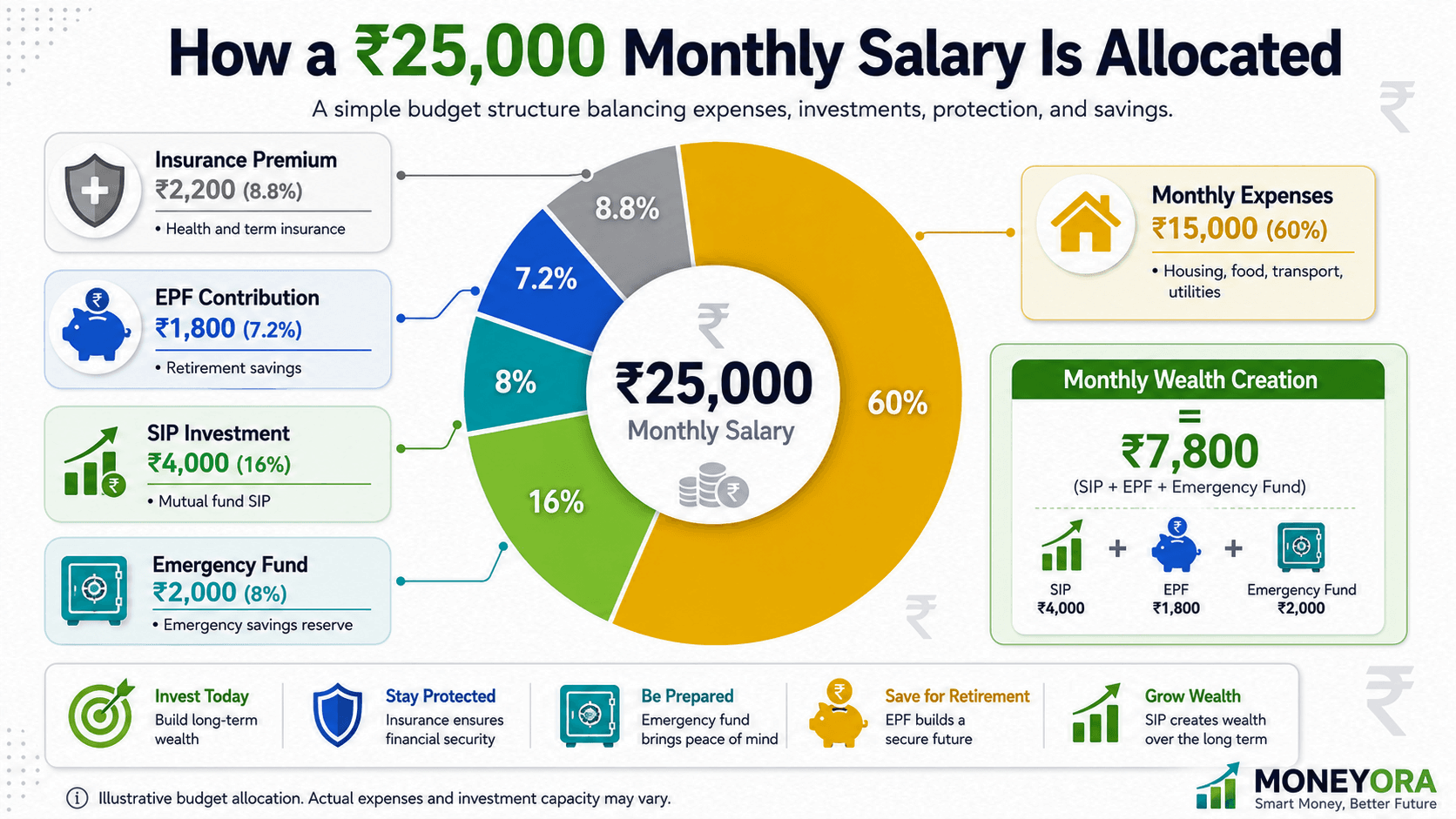

What a ₹25,000 Salary Actually Looks Like After Deductions

Before building any salary investment plan, you need to know what ₹25,000 actually means in hand.

| Deduction | Approximate Amount |

|---|---|

| EPF (Employee share — 12% of basic) | ₹1,800 |

| Professional Tax (varies by state) | ₹200 |

| TDS (if applicable) | ₹0 – ₹500 |

| Take-Home (approx.) | ₹22,500 – ₹23,000 |

Most people at this salary in Tier-2 and Tier-3 cities spend roughly:

| Expense Category | Monthly Amount |

|---|---|

| Rent / PG | ₹4,000 – ₹8,000 |

| Food & Groceries | ₹3,000 – ₹5,000 |

| Transport | ₹1,500 – ₹2,500 |

| Mobile / Internet | ₹500 – ₹800 |

| Misc / Personal | ₹1,500 – ₹2,000 |

| Total Expenses | ₹10,500 – ₹18,300 |

You have around ₹5,000 to ₹10,000 that you can invest every month.

This amount may seem small.. It is still important. It is not something you can ignore.

The money that is being deducted from your salary every month for the EPF account. which’s ₹1,800 is actually growing in your account. A lot of people forget about this money. We will talk about it again later.

How money should you invest when you are earning this amount of money?

There is a way to think about it. You can follow the 50/30/20 rule.

– 50% Of your money should go towards things you need

– 30% towards things you want

– 20% towards saving and investing

If you are earning ₹25,000, per month then 20% of that is ₹5,000. So you should try to save or invest at ₹5,000 every month.

One thing that a lot of people do not consider is that the money you are putting into the Employee Provident Fund is also a kind of investment. So if you are already putting ₹1,800 into the Employee Provident Fund and you also invest ₹5,000 every month then you are actually saving ₹6,800 or more every month for your future.

This changes everything. You can use the MoneyOra EPF Calculator to see how money you will have in your Employee Provident Fund account when you retire. The result is usually surprising.

How a ₹25,000 monthly salary breaks down — and where your investment surplus comes from

How a ₹25,000 monthly salary breaks down — and where your investment surplus comes from

Salary Investment Plan: The Easy Way to ₹1 Crore

Imagine investing ₹5,000 every month in an equity fund. Lets assume it gives a return of 12% per year. This is like the return of large-cap and flexi-cap equity funds in India over a long period of 15 years or more.

– ₹5,000 Per month is a starting point.

– 12% Return per year is what we expect.

– Equity mutual funds have done well in India over 15 years.

According to the data from AMFI India, which is checked by SEBI this 12% return is an estimate.

Now lets see how this ₹5,000 per month can add up to ₹1 Crore.

– ₹5,000 Per month for a time

– 12% return helps it grow

– ₹1 Crore in the end

This looks like a plan.

The ₹5,000 per month investment in equity funds can become ₹1 Crore over time with a 12% return.

SEBI-registered fund data on AMFI India, on AMFI India shows this.

₹5,000 And 12% return are the key.

Equity mutual fund investment grows this way.

₹1 Crore target seems achievable.

| Time Period | Total Invested | Estimated Corpus |

|---|---|---|

| 10 years | ₹6,00,000 | ₹11.6 lakh |

| 15 years | ₹9,00,000 | ₹25.2 lakh |

| 20 years | ₹12,00,000 | ₹49.9 lakh |

| 25 years | ₹15,00,000 | ₹94.9 lakh |

| 27 years | ₹16,20,000 | ~₹1.04 crore |

How Much Should You Invest?

The 50/30/20 Rule Applied to a ₹25,000 Salary

The most practical framework for a salary investment plan at this income level:

- 50% on needs (rent, food, transport) — ₹12,500

- 30% on wants (entertainment, clothes, subscriptions) — ₹7,500

- 20% on savings and investments — ₹5,000

At ₹25,000 gross, 20% = ₹5,000 per month to invest.

What Most Articles Miss

Your EPF (₹1,800/month) is already counted as savings. So when you add EPF + SIP, even a ₹3,200 SIP means you are saving ₹5,000+ per month total.

That changes the calculation — and makes ₹1 crore more achievable than it looks.

A flat ₹5,000/month SIP takes roughly 27 years to cross ₹1 crore.

That is a long time. But if you are 23 today, you hit ₹1 crore by age 50 — with a decade of earning life still ahead.

Now let’s look at ₹8,000 per month:

| Time Period | Total Invested | Estimated Corpus |

|---|---|---|

| 15 years | ₹14,40,000 | ₹40.2 lakh |

| 20 years | ₹19,20,000 | ₹79.8 lakh |

| 22 years | ₹21,12,000 | ~₹1.06 crore |

At ₹8,000/month, you cross ₹1 crore in about 22 years.

Run these numbers yourself on the MoneyOra SIP Calculator — try different amounts and time horizons to find your personal target.

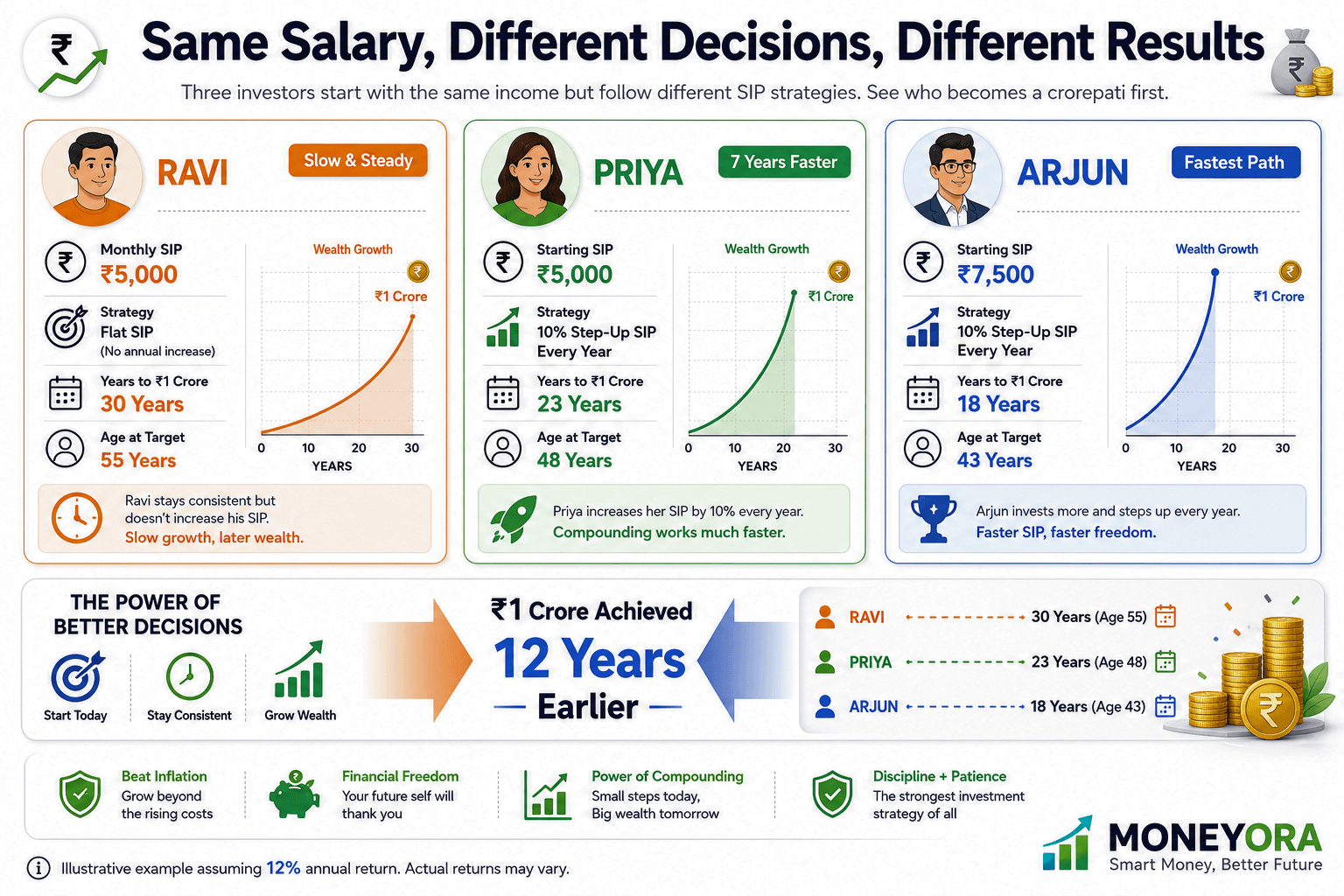

Same starting salary, three different strategies — the difference 7 years makes

Same starting salary, three different strategies — the difference 7 years makes

Salary Investment Plan: The Step-Up SIP Strategy: The Smarter Way

Here is where things get genuinely interesting.

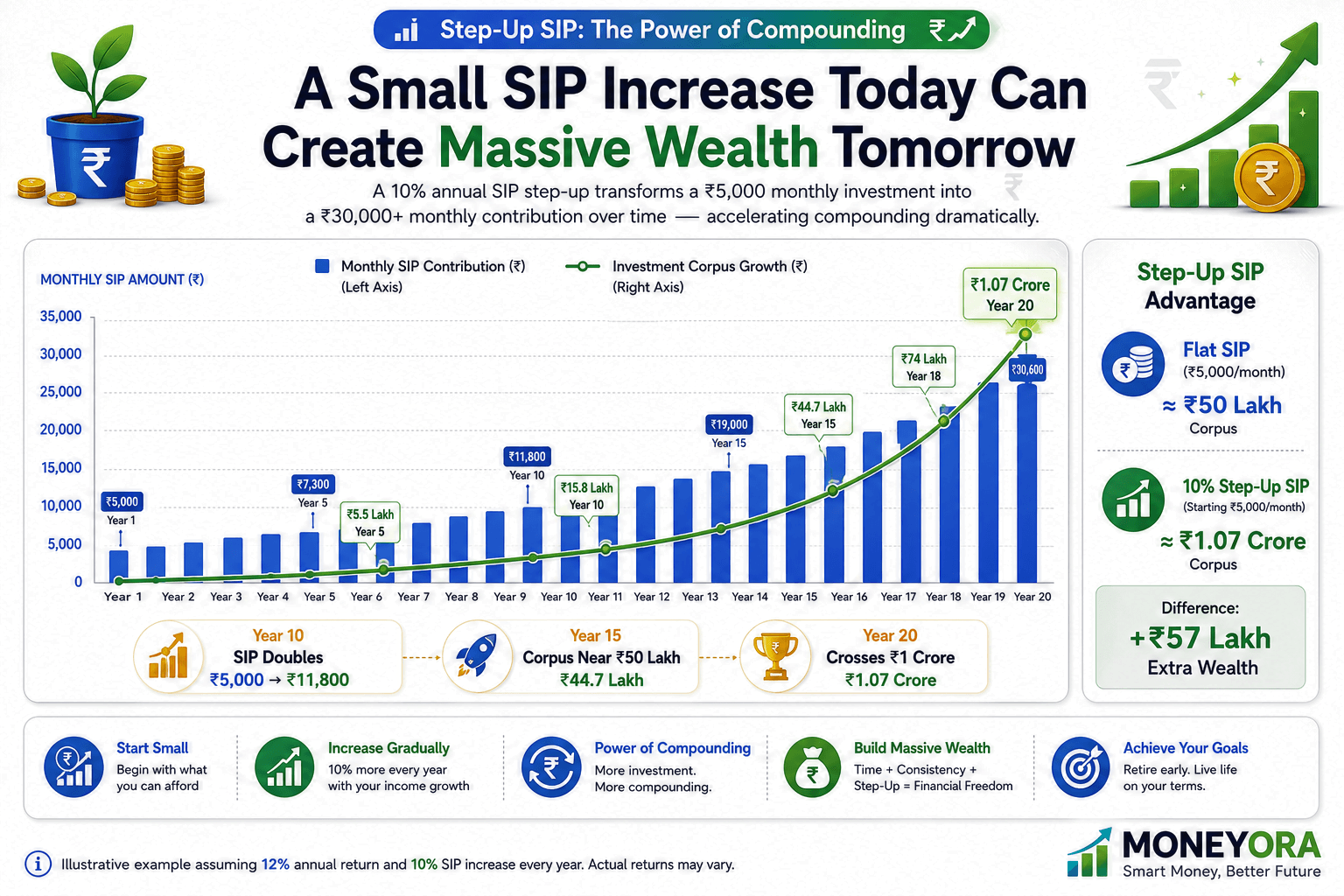

Most salaries grow over time. Even a 10% annual hike is normal in India. If you increase your SIP by 10% every year — what platforms call a Step-Up SIP — the results are dramatically different.

Starting SIP: ₹5,000/month Annual Step-Up: 10% Expected Return: 12% per annum

| Year | Monthly SIP at That Time | Corpus at Year End |

|---|---|---|

| Year 1 | ₹5,000 | ₹63,400 |

| Year 5 | ₹7,321 | ₹4.67 lakh |

| Year 10 | ₹11,789 | ₹15.4 lakh |

| Year 15 | ₹18,983 | ₹41.8 lakh |

| Year 20 | ₹30,577 | ₹1.06 crore |

A 10% annual SIP step-up — small annual increases, massive long-term difference

A 10% annual SIP step-up — small annual increases, massive long-term difference

With a step-up SIP starting at just ₹5,000, you reach ₹1 crore in 20 years — 7 years faster than a flat SIP.

And each increase matches your salary hike, so it never feels like a cut in lifestyle.

This is the most practical salary investment plan for anyone starting at ₹25,000.

To verify: check your CAGR on past investments using the MoneyOra CAGR Calculator — it helps you understand whether your existing portfolio is on track.

Scenario Comparison: Three Different Investors

All three start at age 25 with a ₹25,000 salary and the same goal: ₹1 crore.

| Investor | Monthly SIP | Strategy | Time to ₹1 Crore | Age at Target |

|---|---|---|---|---|

| Ravi | ₹5,000 | Flat SIP, 12% returns | 27 years | 52 |

| Priya | ₹5,000 | 10% Step-Up SIP, 12% returns | 20 years | 45 |

| Arjun | ₹8,000 | 10% Step-Up SIP, 12% returns | 17 years | 42 |

Arjun’s approach needs ₹8,000 to start — tight on ₹25,000, but doable with controlled living expenses in early career years.

Priya’s strategy is the most realistic for most people at this income level.

Ravi’s flat SIP works too. He just needs to stay patient and never stop — which, honestly, is harder than it sounds.

Salary Investment Plan: Where to Invest — Not Just How Much

A lot of salary investment plan guides stop at “invest in SIP.” That is incomplete.

Here is a practical monthly allocation for someone earning ₹25,000:

| Investment Type | Monthly Amount | Purpose |

|---|---|---|

| EPF (already deducted) | ₹1,800 | Retirement safety net — check your EPF corpus |

| Emergency Fund (Liquid Fund or savings account) | ₹1,000 – ₹2,000 | 3–6 months of expenses, built first |

| Equity SIP (Flexi-cap or Index Fund) | ₹3,000 – ₹5,000 | Primary wealth creation — SIP Calculator |

| PPF (optional, for 80C + guaranteed returns) | ₹1,000 – ₹2,000 | Tax saving + safe debt portion — PPF Calculator |

| Term Insurance Premium (annual ÷ 12) | ₹500 – ₹700 | Life cover — this is not an investment |

| Health Insurance (if employer doesn’t cover) | ₹500 – ₹800 | Medical protection |

Notice what is missing from your Salary Investment Plan: ULIPs, endowment plans, traditional LIC policies. These are not ways to grow your wealth at your income level. They take a lot of money in charges. Usually give you 4–6% returns, which is just a little more than the inflation rate.

When you are earning ₹25,000 every single rupee is important. You should always keep your insurance and investments separate.

If you have taken a loan like a loan, car loan or home loan you need to calculate your EMI first. This is something you have to do before you start investing. You can use the MoneyOra EMI Calculator to understand how much money is going out and how much you actually have to invest.

The Biggest Mistakes Salaried Investors Make

These mistakes are real and happen all the time.

1. Waiting until your salary grows to start investing

Some people think that ₹5,000 per month is too small to make a difference.. The numbers show that this is not true. If you start investing at the age of 23 with ₹5,000 you will be off than if you start at the age of 30 with ₹10,000 because your money will have more time to grow.

2. Mixing insurance and investment

ULIPs and endowment plans are often sold to salaried people. They are not good investments. They lock your money for years. Usually give you 4–6% returns. You should keep your insurance and investments separate.

3. Stopping SIPs when the market falls

Every time the Indian market has fallen, like in 2008, 2013 and 2020 it has always recovered quickly. If you stop investing during a downturn you will miss out on the chance to buy units at a lower price. This is the point of investing a fixed amount of money at regular intervals.

4. Not increasing your SIP when your salary increases

If you get a raise your lifestyle might become more expensive. You should still try to increase your SIP. If you keep your SIP at ₹5,000 for five years you will be losing out on a lot of wealth. Even if you increase your SIP by 5% every year it can make a big difference over 15 years.

5. Keeping your emergency money in equity SIP

If you have an emergency and the market is down you will lose money if you withdraw from your equity SIP. You should keep your emergency money in a fund or savings account not in an SIP. The MoneyOra FD Calculator can help you decide how much to keep in a fixed deposit for your emergency fund and what interest rate you can get.

Tax Impact on Your Salary Investment Plan

This is something that is not always explained clearly. Here is how it works.

EPF: If you have been working for 5 years or more you will not have to pay tax on your EPF when you withdraw it. You can also get a tax deduction of up to ₹1.5 lakh on your EPF contributions. However if your employer contributes than ₹7.5 lakh to your EPF in a year that amount will be taxable but this is not something you need to worry about if you are earning ₹25,000.

PPF: You can get a tax deduction of up to ₹1.5 lakh on your PPF contributions. The interest you earn on your PPF is also tax-free. You will not have to pay tax when you withdraw it after 15 years. You can use the MoneyOra PPF Calculator to see how your PPF will grow over time.

ELSS Mutual Funds: You can get a tax deduction of up to ₹1.5 lakh on your ELSS investments. You will have to keep your money in an ELSS fund for least 3 years which is the shortest lock-in period among all the tax-saving investments. If you earn than ₹1.25 lakh in a year from your ELSS investments you will have to pay a tax of 12.5% on the amount above ₹1.25 lakh.

Equity Mutual Funds (non-ELSS): If you hold your Equity Mutual Funds for than a year you will not have to pay tax on the gains until you withdraw them. If you earn than ₹1.25 lakh in a year from your Equity Mutual Funds you will have to pay a tax of 12.5% on the amount above ₹1.25 lakh. Income Tax India guidelines.

If you are investing ₹5,000 per month in an SIP you will not have to pay tax for the first 12 years. You will only have to pay tax when you start withdrawing amounts of money and at that point it is usually better to use a Systematic Withdrawal Plan (SWP). You can use the MoneyOra SWP Calculator. to see how this works.

New Tax Regime note: If you are earning up to ₹12 lakh per year you will not have to pay any income tax under the tax regime that starts from FY2025-26. Since you are earning ₹25,000 per month which’s ₹3 lakh, per year you will not have to pay any income tax at all which means you will have more money in your pocket than you think.

Risks to Consider

I want to talk about the risks of investing. This is not a post to motivate you. To tell you about the actual risks you face.

Market Risk: When you put your money in equity funds the value can go up and down a lot. On average over a time you might get 12% back but this is not a promise. Some years you will get 30%. Some years you will lose 20%. The 12% average only works if you keep your money in for 15 years or more not for one year.

Inflation Risk: If prices rise by 6 or 7% every year and your investments grow by 12% the real value of your money will be less. For example if you have ₹1 crore in 20 years it will not be able to buy much, as ₹1 crore can buy today. This is not a reason to avoid investing. A reason to invest in things that will grow faster than prices rise, like equity.

Income Disruption Risk: Sometimes things happen, like losing your job having an emergency or needing to take care of your family. These things can make you stop or withdraw your investments. This is why you should have an emergency fund before you start investing not after.

Behavioral Risk: This is the risk to understand. The biggest reason people lose money when investing is not because the market goes down. Because they stop investing when it does. Being able to stay invested when the market is volatile is a skill you can learn. You can build this skill by understanding why markets go up and down.

Fund Risk: If you choose a fund that’s not good with high fees and a poor track record you might end up with less money than if you had invested in a simple index fund. You can use the MoneyOra Stock Return Calculator to see how your fund is doing compared to the market.

Expert Perspective

The way people Salary Investment Plan in India has changed a lot over the five years.

Monthly investments through something called SIP have gone up to ₹25,000 crore in 2025. This is up from ₹16,600 crore in the year 2023-24 according to data from AMFI India data. A lot of investors are putting money into the market for the first time. They do not have anyone to guide them. They are not investing money that they inherited from their family. These people are usually the ones who earn a salary of around ₹25,000.

There are three things that separate people who are good at building wealth from the rest.

First it is better to start investing rather than investing a lot of money later. For example someone who starts investing ₹3,000 every month at the age of 22 will probably have money than someone who starts investing ₹10,000 every month at the age of 35. This is because the money invested early has time to grow.

Second it is more important to Salary Investment Plan in the types of assets rather than trying to pick the best investment fund. What matters most is whether you are investing in stocks when you are, in your 20s and 30s. It is better to invest for a time rather than trying to invest at the right time.

Third increasing your investments every year can make a difference. If you increase your SIP by 10% every year you can have ₹40-55 lakh more after 20 years compared to if you had not increased your investment. Most people do not take advantage of this option when they set up their SIP.

For people who invest in the stock market and want to keep track of their investments the MoneyOra Stock Average Calculator can be helpful. It can help you invest money when the market is down which is a good strategy if you have a plan and you are investing a fixed amount of money every month. position sizing.

SIP projections: MoneyOra SIP Calculator — enter your monthly amount, expected return (try 10%, 12%, 14%), and your time horizon. See the range of outcomes.

CAGR on existing investments: MoneyOra CAGR Calculator — reverse-calculate whether your portfolio is on track.

EPF at retirement: MoneyOra EPF Calculator — most people are surprised how much this silent savings compound to.

Lumpsum windfalls (bonus, gratuity): MoneyOra Lumpsum Calculator — see what a one-time investment grows to.

NPS alongside SIP: MoneyOra NPS Calculator — if your employer offers NPS, model the retirement corpus.

PPF vs SIP comparison: MoneyOra PPF Calculator — useful to see the safe-debt portion of your portfolio.

Monthly withdrawals once you hit the goal: MoneyOra SWP Calculator — so your ₹1 crore keeps working after you stop contributing.

EMI impact on investable surplus: MoneyOra EMI Calculator — your loan EMI directly reduces how much you can invest. Know the exact number.

A ₹25,000 salary can build ₹1 crore. The math is settled.

The real challenge is behavioral. Most people who do not reach this target on this Salary Investment Plan do not fail because of the income level. They fail because they wait, stop, or never start.

₹5,000 per month, started at 25, stepped up 10% annually, invested in a diversified equity fund — this is a plan that works. No finance degree required. No large starting capital. No perfect market timing.

Just one thing: start today, and keep going.

Use the free SIP Calculator now on MoneyOra.in to see your own numbers.

Q1. Can a person who earns ₹25,000 per month really build ₹1 crore?

Yes. If your Salary Investment Plan ₹5,000 every month and get 12 percent returns you will have ₹1 crore in 27 years if you do not increase your Salary Investment Plan. If you increase your Salary Investment Plan by 10 percent every year you can get ₹1 crore in 20 years. The math is simple. The problem is not about money it is about being patient and staying Salary Investment Plan when the market is going up and down.

Q2. How much of a ₹25,000 salary should go toward investment?

A good idea is to Salary Investment Plan 20 percent of your salary, which’s ₹5,000. You already save ₹1,800 in your Employee Provident Fund. Once you have money to cover your expenses for 3 to 6 months you can increase your Salary Investment Plan to ₹6,000 or ₹8,000 per month. This will help you create wealth faster.

Q3. Which mutual fund is best for a ₹25,000 salaried investor?

If you want to create wealth over a period like 15 years or more you can start with a large-cap index fund that tracks Nifty 50 or a flexi-cap fund that has done well over the last 10 years. Make sure the expense ratio is below 0.5 percent for index funds and below 1.5 percent for other funds. Salary Investment Plan

Q4. Is SIP safe for low-income investors?

SIP in equity funds can be risky in the term because of market ups and downs.. If you Salary Investment Plan for 10 years or more you are likely to get good returns. The risk is not with the SIP it is with selling your Salary Investment Plan when the market’s down.

Q5. What is a Step-Up SIP. How does it work?

A Step-Up SIP is a way to increase your Salary Investment Plan every year. You can choose to increase your Salary Investment Plan by a fixed percentage, 10 percent, every year. This way your Salary Investment Plan will grow as your Salary Investment Plan grows. It can help you reach your goal of ₹1 crore 5 to 7 years faster than a SIP.

Q6. Should I invest in PPF or SIP on a ₹25,000 salary?

Both PPF and SIP are good. They serve different purposes. PPF gives you 7.1 percent guaranteed returns, which’s good for saving taxes and creating conservative wealth. SIP on the hand can give you 10 to 14 percent returns over the long term but it carries market risk. You can use PPF for your tax savings and SIP for building wealth. Salary Investment Plan

Q7. What if I miss a SIP installment?

Missing one or two installments will not make a difference in the long run. There is no penalty, for missing a month.. If you stop and restart your SIP often you will break the cycle of compounding and might miss out on buying more when the market is low.

Q8. Can I invest in stocks directly of SIP?

You can Salary Investment Plan in stocks directly. It requires a lot of time, research and discipline. Salary Investment Plan in equity funds through SIP is easier because you get professional management, diversification and automatic rupee cost averaging. If you do want to MoneyOra PE Ratio Calculator you can use tools to screen for value and make Dividend Calculator informed decisions.

Pingback: 100 Per Day Investment: How Wealth Can You Build - MoneyOra

Pingback: SIP vs FD During Market Crashes: Which Performs Better? 2026