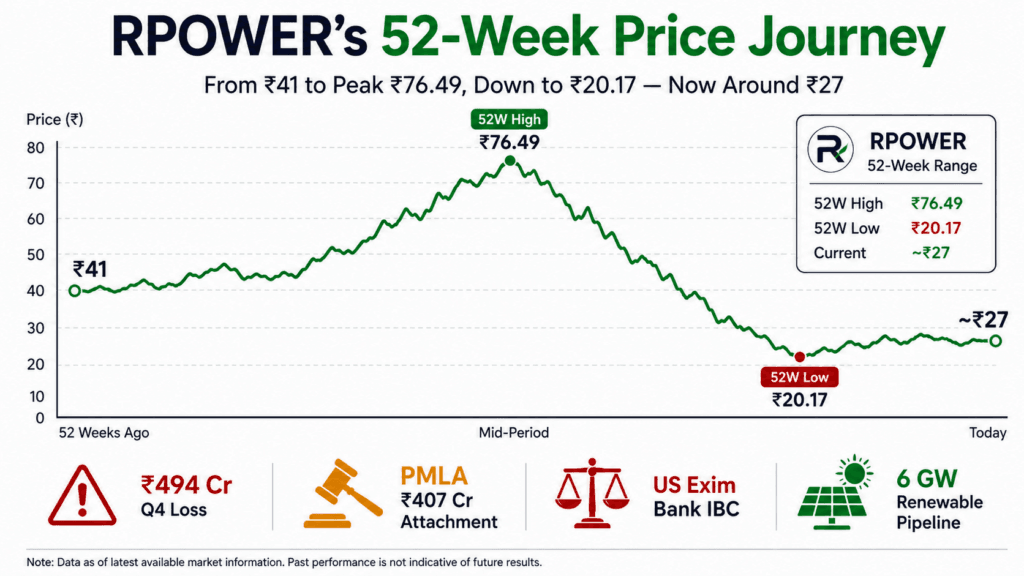

The Reliance Power share has given retail investors a wild decade. A ₹450 IPO in 2008 that’s now trading near ₹27. A stock that fell 96% from its listing price, then surged over 2,600% from its 2022 lows, then shed 65% in twelve months. A company that reported a ₹25 crore profit in Q3 FY2026, only to swing back to a ₹494 crore loss in Q4. If you’re trying to make sense of it, you’re not alone — and that’s exactly why this analysis exists.

The honest truth about the Reliance Power share is that it sits at a genuine crossroads. The thermal asset base is eroding. The renewable pipeline is real but early-stage. The debt overhang is shrinking but still meaningful. And the legal headwinds — PMLA attachment of ₹407.6 crore in assets, US Exim Bank filing an IBC plea over $165.4 million — don’t feature prominently enough in most coverage. This article covers all of it, with actual numbers, without either cheerleading or catastrophising.

Use MoneyOra’s Stock Return Calculator to model hypothetical returns from different entry points in the Reliance Power share price history — the results tend to clarify things quickly.

Key Takeaways

- Q4 FY2026: Net loss of ₹494 crore, EBITDA ₹570 crore (margin 30.5%). Full-year revenue: ~₹7,620 crore.

- Market cap: ~₹10,273 crore. 52-week range: ₹20.17–₹76.49. The stock has fallen ~65% in 12 months.

- Installed capacity: 5,305 MW (5,160 MW thermal + 145 MW renewable). Renewable pipeline under development: 6 GW solar + 6.5 GWh BESS.

- Key risk: PMLA asset attachment (₹407.6 crore), US Exim Bank IBC petition (Samalkot subsidiary, $165.4 million), persistent losses despite asset base of ₹1.11 lakh crore.

- Analyst median target: ~₹37. Book value: ~₹38.8 per share. The stock trades at a ~30% discount to book — not distressed, but not cheap on earnings either.

Quick Summary — What You Need to Know About Reliance Power Share Right Now

Quick answer : The Reliance Power share is a high-risk turnaround play with a massive thermal base, a genuine renewable energy pipeline, persistent losses, and active legal proceedings. It is not a buy-and-hold for conservative investors. Speculative interest is real, but fundamentals are not yet supportive of consistent gains.

| Metric | Value |

|---|---|

| NSE Symbol | RPOWER |

| BSE Code | 532939 |

| Current Price (approx.) | ₹27–29 |

| 52-Week High | ₹76.49 |

| 52-Week Low | ₹20.17 |

| Market Cap | ~₹10,273 crore |

| Book Value / Share | ~₹38.8 |

| P/B Ratio | ~0.7x |

| Revenue (FY2026) | ~₹7,620 crore |

| Net Profit (FY2026) | ~₹-337 crore (full year) |

| Q4 FY2026 Net Loss | ₹494 crore |

| Q4 FY2026 EBITDA | ₹570 crore (margin 30.5%) |

| Installed Capacity | 5,305 MW |

| Asset Base | ~₹1.11 lakh crore |

| Promoter Holding | ~25% |

Company Overview — What Reliance Power Actually Is

Reliance Power Limited (RPOWER) is part of the Anil Ambani-led Reliance Group and functions as its primary power generation vehicle. It’s listed on both NSE and BSE, and was incorporated to develop, construct, and operate power projects across India.

The context matters here. When the Reliance Power share listed in February 2008 at ₹450, it raised around ₹11,700 crore in what was then one of India’s largest IPOs. The company’s ambition was to build 28,000 MW of capacity across coal, gas, hydro, and solar. Reality intervened — fuel supply issues, regulatory delays, financing stress, and years of accumulated losses reduced that vision considerably.

Business segments and operational reality

The company currently operates three broad segments:

- Thermal Power (core, 5,160 MW): Includes the Sasan Ultra Mega Power Project in Madhya Pradesh (3,960 MW — India’s largest coal-based plant), Rosa Thermal in Uttar Pradesh (1,200 MW), and Butibori Thermal in Maharashtra (600 MW). These generate the bulk of revenue.

- Renewable Energy (early-stage, 145 MW operational): The Dhirubhai Ambani Solar Park (40 MW operational) and a small wind portfolio form the current renewable base. Minimal in the context of the pipeline that’s under development.

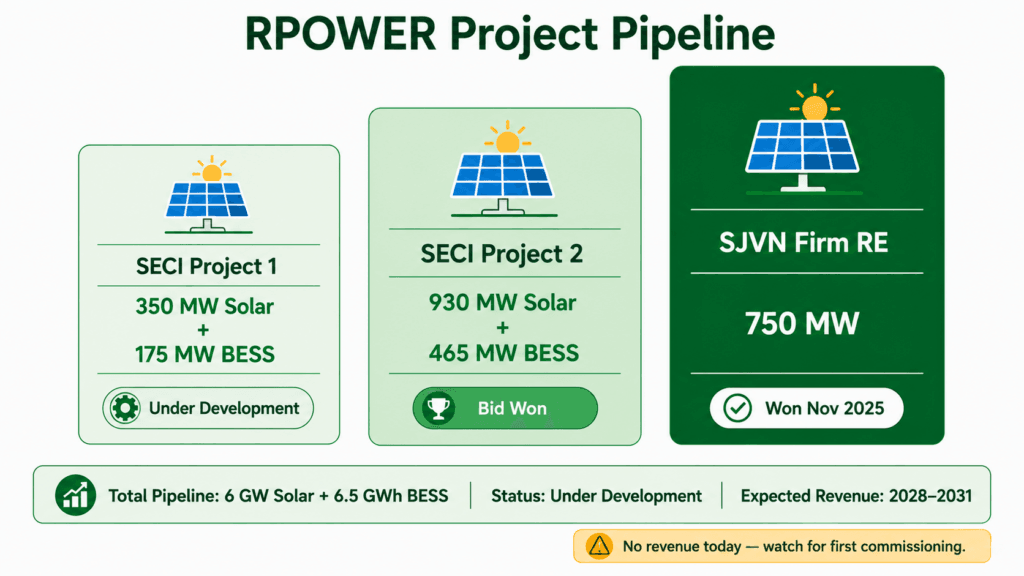

- Projects Under Development: This is where the potential lies — a 6 GW solar + 6.5 GWh Battery Energy Storage System (BESS) pipeline from recent SECI and SJVN bid wins. These won’t generate revenue for 2–4 years.

The total asset base stands at approximately ₹1.11 lakh crore (as of September 2025). That’s a significant physical foundation. The challenge has always been converting those assets into consistent, profitable cash flows — something the company has repeatedly struggled with.

Q4 FY2026 Results — Unpacking the Numbers

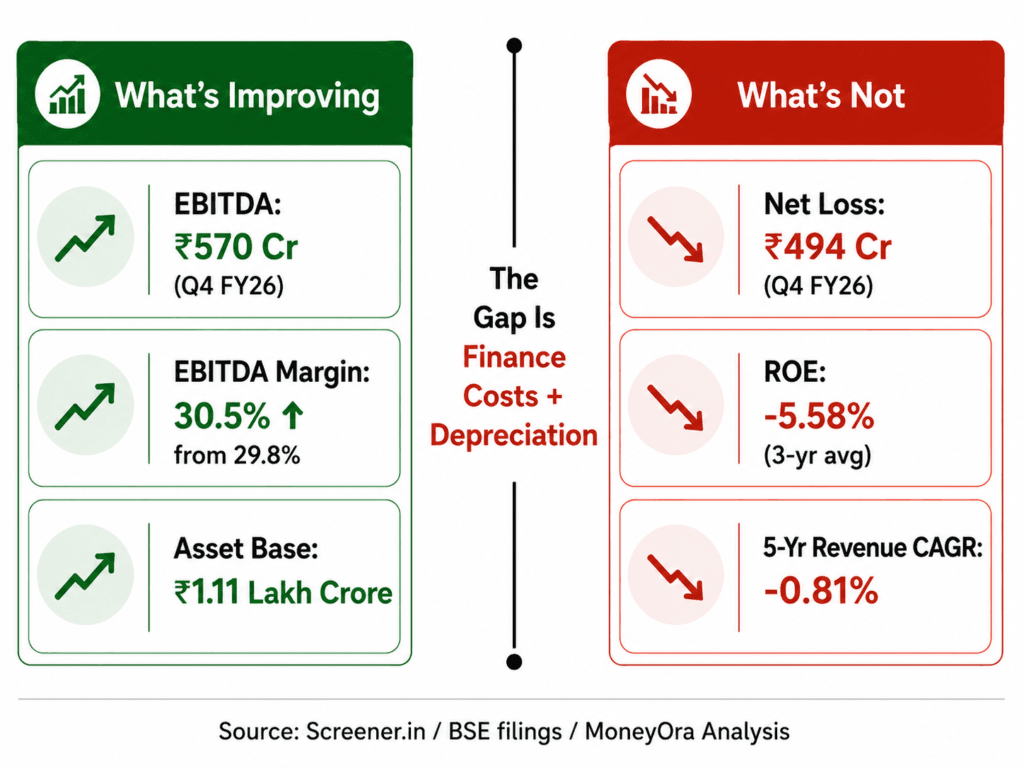

The Q4 FY2026 result was a sharp reversal from Q3. The company had swung to a small profit of ₹25 crore in Q3 FY2026 — which many retail investors read as a definitive turnaround signal. Then Q4 printed a ₹494 crore net loss. That’s not the whole story, but it’s the part that moved the Reliance Power share price lower.

| Metric | Q3 FY2026 | Q4 FY2026 | Q4 FY2025 (YoY) |

|---|---|---|---|

| Revenue (₹ crore) | 1,949.78 | ~1,868 | ~1,979 |

| EBITDA (₹ crore) | 471.39 | 570 | 590 |

| EBITDA Margin | 24.2% | 30.5% | 29.8% |

| Net Profit / (Loss) (₹ crore) | 25.11 | (494) | (~490) |

The critical observation here: Q4 EBITDA actually improved year-on-year (₹570 crore vs ₹590 crore, a modest decline) and EBITDA margin improved (30.5% vs 29.8%). The business at the operating level is not deteriorating. The losses are below the EBITDA line — driven by high depreciation on an aging thermal fleet, and finance charges on legacy debt.

That’s actually a meaningful distinction. The coal-fired plants are generating operating cash, just not enough to overcome the heavy fixed-cost burden. Whether that situation improves depends on three things: fuel cost management, continued debt reduction, and the pace at which cheaper renewable assets come online.

Financial Health — The Full Picture Most Investors Miss

A lot of people look at the Reliance Power share and see: large asset base + low price = deep value. The actual picture is more complicated.

| Indicator | Value | What It Signals |

|---|---|---|

| Return on Equity (3-yr avg) | -5.58% | Negative — equity is being eroded |

| Interest Coverage Ratio | Low | EBIT does not comfortably cover interest |

| 5-Year Revenue CAGR | -0.81% | Revenue is stagnant — no organic growth |

| P/B Ratio | ~0.7x | Trades at discount to book — optically cheap |

| P/E Ratio | N/A (losses) | Not applicable — no positive earnings |

| Dividend Yield | 0% | No dividends paid |

| Moneycontrol Stock Score | 46/100 | Below-average financial strength |

The debt picture — what’s improved and what hasn’t

Consolidated debt stood at approximately ₹17,812 crore as of June 2024. Since then, Reliance Power has taken meaningful steps: settling loans at discounted rates with three bank creditors, raising ₹1,524.6 crore via convertible warrants in a preferential issue (₹694.65 crore received by December 2025, funds utilised by March 2026), and pursuing further fundraising via QIP, FCCBs, or NCDs.

But debt reduction isn’t the same as debt resolution. Two open issues remain genuinely concerning:

- PMLA Asset Attachment: ED attached assets worth ₹407.6 crore. Reliance Power has clarified this relates to a specific subsidiary and is being contested. But it adds regulatory uncertainty at exactly the wrong time.

- US Exim Bank IBC Petition: The US Export-Import Bank has filed an insolvency petition under Section 7 of IBC against Reliance Power’s Samalkot subsidiary, alleging a $165.4 million debt guarantee default. This is an active legal proceeding — outcome uncertain.

Neither of these automatically sinks the parent company. But they do inject legal risk that most retail investors following the Reliance Power share price don’t adequately factor into their thesis.

Renewable Energy Pipeline — The Real Growth Story

This is where the genuine bull case lives. The thermal fleet is a legacy burden — old assets, low plant load factors, fuel cost exposure, increasing environmental regulation. The renewable pipeline is where Reliance Power’s actual future cash flow potential sits.

What’s been won and what it means

| Project | Scale | Type | Status |

|---|---|---|---|

| SECI Solar + BESS (Project 1) | 350 MW solar + 175 MW BESS | Hybrid renewable | Under development |

| SECI Solar + BESS (Project 2) | 930 MW solar + 465 MW BESS | Hybrid renewable | Won, under development |

| SJVN Firm & Dispatchable RE | 750 MW | Firm dispatchable RE | Won November 2025 |

| Additional pipeline (multiple bids) | Totalling ~6 GW solar | Solar + Storage | Various development stages |

| Total Pipeline | 6 GW solar + 6.5 GWh BESS | Solar + Storage | Under development |

A 6 GW solar + 6.5 GWh BESS pipeline is not trivial. For context, India’s total renewable energy capacity was approximately 200 GW as of early 2026, and the government is targeting 500 GW by 2030. Projects of this scale can generate predictable, long-term revenue through Power Purchase Agreements with government agencies like SECI and SJVN.

The critical qualifier: “pipeline” is not “operational.” None of these projects are generating revenue today. They won’t for 2–4 years at minimum, depending on land acquisition, grid connectivity, and financing arrangements. A 6 GW pipeline that doesn’t get funded and built is worth nothing. A 6 GW pipeline that successfully commissions through 2029–2031 could fundamentally re-rate the Reliance Power share price.

Shareholding Pattern and Promoter Dynamics

The promoter holding in the Reliance Power share stands at approximately 25% — a number that tells two stories simultaneously.

The positive read: no shares are currently pledged by promoters. Pledging was a significant risk factor during Reliance ADAG group’s period of maximum stress. The absence of pledging removes one specific overhang that has plagued several stocks in this group historically.

The less positive read: a 25% promoter stake is relatively low for a company that’s supposed to be in a turnaround phase led by its founding management. High promoter holding typically signals confidence in the business — it means management has skin in the game. At 25%, that signal is muted.

| Category | Approximate Holding |

|---|---|

| Promoters (Anil Ambani group) | ~25% |

| Domestic Institutions / Mutual Funds | Low |

| Foreign Portfolio Investors | Some interest noted |

| Retail / Public | Significant (the bulk of float) |

Institutional ownership is notably thin. Most established mutual funds in India don’t hold the Reliance Power share in their mainstream portfolios — a function of the ongoing losses and legal uncertainty. The primary market participant remains retail investors, many of whom trade it on momentum rather than fundamentals.

Valuation — What the Numbers Suggest

Valuing a loss-making company is not straightforward. Standard P/E ratios don’t apply when earnings are negative. Here’s how to think about the valuation of the Reliance Power share using the frameworks that do apply:

Price-to-Book Ratio

Book value per share: approximately ₹38.8. Current price: approximately ₹27–29. P/B: approximately 0.7x. This looks cheap — you’re buying ₹1 of book assets for ₹0.70. But book value for a power company includes thermal assets that are aging, potentially stranded in a decarbonising energy landscape, and have low utilisation rates. Book value doesn’t equal market value if those assets can’t generate adequate returns.

EV/EBITDA

With quarterly EBITDA running at approximately ₹470–570 crore, annualised EBITDA is roughly ₹2,000–2,200 crore. Adding net debt to market cap gives an Enterprise Value in the range of ₹25,000–30,000 crore. EV/EBITDA comes out at approximately 11–15x. For a thermal power company with these risks, that’s not screaming cheap.

Asset-Based Valuation (floor estimate)

The ₹1.11 lakh crore asset base at a 10–15% haircut gives an asset value of ₹94,000–1,00,000 crore. This is well above the current market cap of ₹10,273 crore. But this only matters if the assets can be monetised — through sale, lease, or operational improvement. The gap between asset value and market cap reflects the market’s scepticism about realising that asset value under current management and debt conditions.

Use MoneyOra’s PE Ratio Calculator and Stock Return Calculator to model different scenarios for when earnings might normalise and what that implies for the Reliance Power share price.

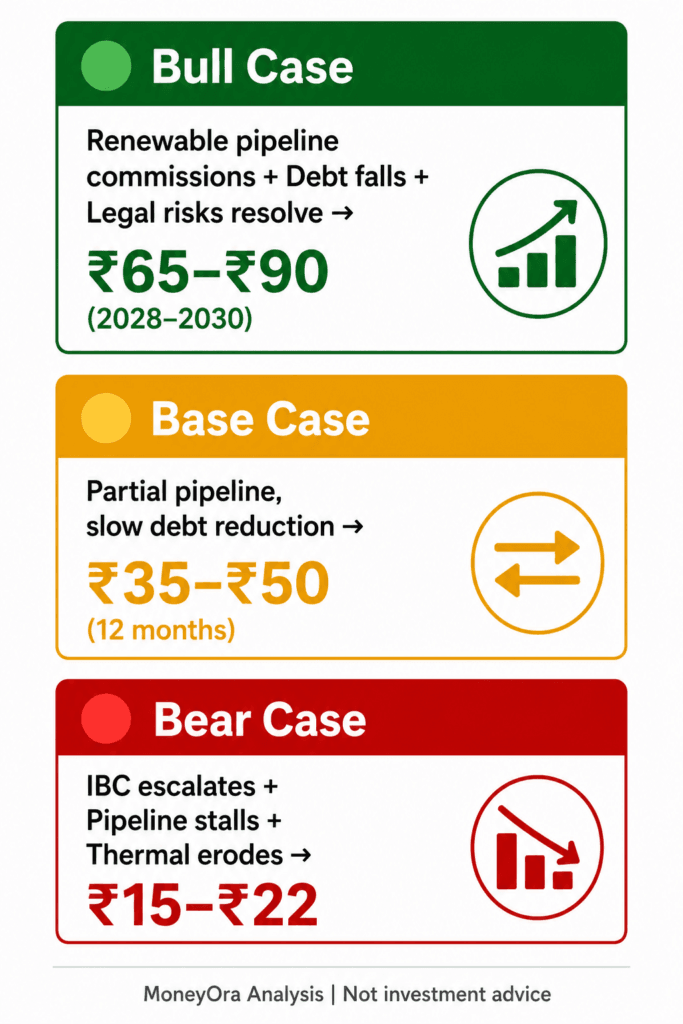

Bull Case vs Bear Case — Scenario Analysis

Bull Case — What Needs to Go Right

- Renewable pipeline executes on time: All or most of the 6 GW solar + 6.5 GWh BESS projects commission by 2029–2031, generating predictable PPA revenues. This fundamentally changes the revenue and margin structure.

- Debt falls below ₹10,000 crore: Continued repayment and QIP fundraising reduces the finance charge drag. Net profit becomes achievable on a sustainable basis.

- Legal headwinds resolve without material damage: PMLA attachment is successfully contested; US Exim Bank IBC plea is settled before triggering broader insolvency proceedings.

- Thermal PLF improves: Better fuel supply management and plant maintenance improve plant load factors across the Sasan and Rosa plants, lifting EBITDA toward ₹2,500–3,000 crore annually.

- Bull case Reliance Power share price target: ₹55–₹75 range by FY2028–2029, if even 30–40% of the above materialises. Still a 60–90% recovery from the current ~₹28.

Bear Case — What Could Go Wrong

- Renewable pipeline stalls: Land acquisition issues, funding gaps, or project delays push commissioning to 2033+. The equity story loses its growth catalyst.

- IBC proceedings escalate: If the US Exim Bank petition results in a broader insolvency order touching the parent company, the downside is severe and largely unquantifiable.

- Thermal assets get stranded: Regulatory tightening on coal plants, falling merchant power tariffs, and rising coal costs compress EBITDA margins below 20%. Cash generation falls below debt servicing requirements.

- Promoter dilution:: Further preferential issues and QIPs, needed for fundraising, dilute existing shareholders. The share count grows faster than earnings.

- Bear case Reliance Power share price: A return toward book value of ₹22–₹25 or below is possible if even two or three of these risks materialise simultaneously.

| Scenario | Key Trigger | Price Range Implied |

|---|---|---|

| Full bull case | Renewable pipeline + debt clean-up + legal resolution | ₹65–₹90 (2028–2030) |

| Base case | Partial pipeline execution, slow debt reduction | ₹35–₹50 (12 months) |

| Bear case | Legal escalation + pipeline delay + thermal erosion | ₹15–₹22 |

Risks Every Investor Must Understand Before Buying Reliance Power Share

- Legal and regulatory risk: The PMLA attachment and US Exim Bank IBC petition are active, unresolved legal proceedings. These are not remote tail risks — they’re current events with uncertain resolution timelines and potentially material financial consequences.

- Execution risk on renewables: The 6 GW pipeline sounds compelling. But Reliance Power has a long history of ambitious project announcements followed by execution delays. This pipeline needs financing, land, grid connectivity, and government support to deliver — none of which is guaranteed.

- Group entity contagion risk: The Reliance ADAG group has had serious financial difficulties across multiple entities — Reliance Capital, Reliance Communications, others. The company explicitly clarified in August 2025 it’s ring-fenced from those issues. That clarification was necessary precisely because the risk is real in perception.

- Thermal stranding risk: India’s push toward 500 GW renewable capacity by 2030 creates medium-term headwinds for pure-play thermal generators. As coal plants age and regulations tighten, thermal asset values could impair faster than current projections assume.

- Liquidity risk: The stock trades with significant retail participation and periodically sharp moves. Entry and exit in size is difficult during volatile periods. Don’t size positions in the Reliance Power share beyond what you can hold through a 30–40% drawdown without needing to sell.

- Dilution risk: The preferential allotment and planned QIP/NCD fundraising will expand the share count. If earnings don’t grow proportionally, EPS dilutes even when absolute profit improves.

MoneyOra Analysis — The Three Things That Actually Determine Where This Goes

After going through the quarterly numbers, the pipeline announcements, and the legal events, the Reliance Power share story comes down to three specific catalysts — none of which the market is currently pricing in, and all of which need monitoring more closely than the monthly price chart.

Catalyst 1 — IBC resolution.. The US Exim Bank petition against Samalkot Power is the single most significant near-term risk that could blow up the thesis entirely. If it progresses from a petition to an actual insolvency proceeding on the subsidiary, contagion risk to the parent becomes real regardless of management’s ring-fencing claims. Track this quarterly. If it resolves, that’s a meaningful positive catalyst.

Catalyst 2 — First renewable project commissioning. The market will not re-rate the Reliance Power share based on pipeline announcements alone — it’s heard project announcements from this company before and watched most of them stall. What changes the stock’s narrative is the first solar + BESS project actually going live, generating tariff revenues under a government PPA, and appearing in the revenue line of quarterly results. Until that happens, the renewable story is a promise, not a fact.

Catalyst 3 — Sustained quarterly profitability. One profitable quarter (like Q3 FY2026) is noise. Two consecutive profitable quarters would suggest the debt-reduction effect is actually flowing through to the bottom line. Three or more would constitute a fundamental re-rating signal. The market has been burned by premature profitability calls on this stock before — which is why it will require evidence, not promises.

What should a retail investor do with this? Think of the Reliance Power share as an option with expiry — the turnaround either shows tangible progress by 2027–2028, or the current price is where it will be again in 2029. It’s not a buy-and-forget retirement investment. It’s a speculative position that requires active monitoring of three specific events, with clear exit logic if those events don’t materialise on schedule.

If you do decide to explore a position, think about using a SIP approach across multiple tranches rather than a single lumpsum — the volatility profile of this stock makes tranche-based entry considerably less risky than going all-in at a single price. Use MoneyOra’s Position Size Calculator to determine how much of a portfolio this kind of speculative position should represent, and set a stop-loss level before entering.

What to Do With Reliance Power Share

The Reliance Power share is not a simple story. It’s not the next multibagger, and it’s not a certain zero. It sits in an uncomfortable middle ground that rewards investors who do their homework and punishes those who buy on hype cycles or quarterly profit headlines.

The fundamentals remain challenged: negative ROE, persistent losses at the bottom line, active legal proceedings, and a renewable pipeline that’s years away from generating revenue. The potential is equally real: a 6 GW solar + 6.5 GWh BESS pipeline in one of the world’s fastest-growing power markets, ongoing debt reduction, and an asset base worth multiples of the current market cap if operationally optimised.

Three actions for investors tracking the Reliance Power share:

- Watch the Samalkot IBC proceeding — quarterly. This is the event most likely to materially change the risk profile in either direction.

- Track SECI/SJVN project progress updates in the company’s quarterly earnings commentary, looking for actual land acquisition, financing, and construction timelines.

- Use MoneyOra’s Stock Return Calculator to model what different entry prices and holding periods imply for your actual return scenario — be honest about time horizon.

Model Your Own Return Scenario

Stock Return • CAGR • SIP • Position Size • Stop Loss — all free, no login required.

MoneyOra Tools

- Stock Return Calculator — Model returns at different entry prices and holding periods

- PE Ratio Calculator — Check valuation context against sector peers

- Position Size Calculator — Determine appropriate allocation for high-risk holdings

- Stop Loss Calculator — Set an exit level before you enter any position

- CAGR Calculator — Find the real annualised return on your power sector holdings

- Lumpsum Calculator — Project what different investment amounts produce over 3–7 years

- SIP Calculator — Model phased tranche-based entry versus single lumpsum for volatile stocks

- Margin Calculator — Understand margin exposure if trading RPOWER on leverage

- Brokerage Calculator — Calculate exact transaction costs before placing orders

- Dividend Calculator — Note: Reliance Power share currently pays zero dividend

MoneyOra Articles

- Top 5 Solar Power Companies in India — Sector context for Reliance Power’s renewable pivot

- Defence Index India 2026 — Another high-conviction, high-risk sector play

- AI Stock Picks 2026 — Comparing risk-reward across high-growth sectors

- Semiconductor Stock Picks — Alternative growth story for risk-tolerant investors

- Data Center Stocks India — Power sector adjacency — data centres drive electricity demand

- Hidden Brokerage Costs — What frequent RPOWER trades actually cost retail investors

- Share Market Category — All MoneyOra stock and sector analysis

- Share Market Calculator Hub — All stock analysis calculators in one place

Frequently Asked Questions — Reliance Power Share

What is the current Reliance Power share price?

The Reliance Power share was trading in the range of ₹27–₹29 as of early July 2026, with a 52-week range of ₹20.17–₹76.49. The stock has declined approximately 65% from its 52-week high as the market absorbed Q4 FY2026 losses, PMLA attachment news, and the US Exim Bank IBC filing. Always check live prices on NSE or BSE before acting on any figure.

Why did Reliance Power share fall so much in the last year?

Multiple factors converged: Q4 FY2026 showed a net loss of ₹494 crore after a brief Q3 profit of ₹25 crore, disappointing investors who read that profit as a permanent turnaround. The ED’s PMLA asset attachment of ₹407.6 crore and the US Exim Bank’s IBC petition against Samalkot subsidiary added regulatory and legal uncertainty. The stock’s 65% drop from its 52-week high reflects both the reversal of speculative sentiment from 2024–2025 and the actual deterioration in quarterly results.

What is the Reliance Power share price target for 2026?

Analyst median target is approximately ₹37, reflecting near-term stabilisation around book value (₹38.8). MoneyOra’s 12-month reference range is ₹30–₹45, assuming no major catalysts (either positive or negative). Price targets of ₹100+ circulating on social media are not grounded in current fundamentals. The share is more likely to remain range-bound until renewable project commissioning or debt-level improvements create a verifiable re-rating trigger.

Is Reliance Power share a good investment for long-term investors?

Not for conservative long-term investors. The company has negative ROE, persistent losses, low interest coverage, and active legal proceedings. For risk-tolerant investors with a 5–7 year horizon, the renewable pipeline (6 GW solar + 6.5 GWh BESS) offers genuine option value if executed successfully. But this is a speculative bet on turnaround execution, not a fundamentally sound long-term compounder. Size positions accordingly and use a stop-loss strategy.

What is the Reliance Power share 52-week high and low?

52-week high: ₹76.49. 52-week low: ₹20.17. The range reflects the stock’s extreme volatility — a high driven by speculative momentum on renewable energy announcements and a brief Q3 profit, and a low reached as that sentiment reversed on Q4 losses and legal events. The current price of ₹27–₹29 sits near the lower end of that range.

What happened to Reliance Power’s PMLA case?

The Enforcement Directorate attached assets worth ₹407.6 crore under the Prevention of Money Laundering Act (PMLA). Reliance Power stated this relates to a specific subsidiary matter and announced it would appeal the attachment. The company maintains no impact on business operations — but the attachment is an active legal proceeding. Investors should monitor quarterly filings for updates on its resolution.

What is Reliance Power’s renewable energy pipeline?

Reliance Power has a pipeline of 6 GW solar + 6.5 GWh BESS projects under development, following bid wins from SECI (Solar Energy Corporation of India) and SJVN. These include a 930 MW solar + 465 MW BESS project, a 350 MW solar + 175 MW BESS project, and a 750 MW firm dispatchable renewable energy project won in November 2025. None of these are currently generating revenue — commissioning is expected over 2028–2031 under realistic timelines.

How does Reliance Power compare to other power stocks in India?

Reliance Power is significantly riskier than most listed power peers. NTPC has strong government backing, consistent profitability, and a clear renewable ramp. Tata Power has a cleaner balance sheet and a diversified distribution business. Adani Power is profitable with strong PLFs. Reliance Power, by contrast, has negative ROE, persistent losses, and legal headwinds that its peers don’t face. The only comparable upside is the renewable pipeline — but peers are also building renewables, often from a stronger financial starting position.

What does the US Exim Bank IBC filing mean for Reliance Power share?

The US Export-Import Bank filed an insolvency petition under Section 7 of the Insolvency and Bankruptcy Code against Reliance Power’s Samalkot Power subsidiary, alleging a $165.4 million debt guarantee default. If this petition advances and results in formal insolvency proceedings against the subsidiary, it could complicate broader debt resolution and trigger cross-default clauses in other facilities. The parent company has stated it is ring-fenced from subsidiaries’ issues. Investors should track this proceeding closely — it is the single most important legal risk in the near term.

What’s the face value of Reliance Power share?

The face value of the Reliance Power share is ₹10 per share. The stock’s IPO in 2008 was at ₹450 — a significant premium to face value that raised ₹11,700 crore. That IPO was one of India’s largest, which is also why the subsequent decline has been so psychologically significant for retail investors who participated at the time.

Should I buy Reliance Power share now?

This is ultimately a personal decision based on your risk appetite, investment horizon, and portfolio context. The stock is not suitable for conservative investors or those with a short time horizon. For risk-tolerant investors, the current ₹27–₹29 level is near the 52-week low with a renewable pipeline as a potential catalyst — but active legal proceedings and persistent losses mean downside is real, not just theoretical. Use MoneyOra’s Position Size Calculator to determine an appropriate allocation and consult a SEBI-registered investment advisor before acting.

Pingback: Top 5 Solar Power Companies Why Are Investors Suddenly Buy

Pingback: AI Stocks Picks 2026: Next 5 Best Multibagger AI Stocks

Pingback: Data Center Stocks in India: 9 AI-Boom Picks with Returns Up to 477% Can You Still Join the Party? - MoneyOra

Pingback: Defence Index 2026: Top Investment Opportunity or Overvalued Risk for Investors?