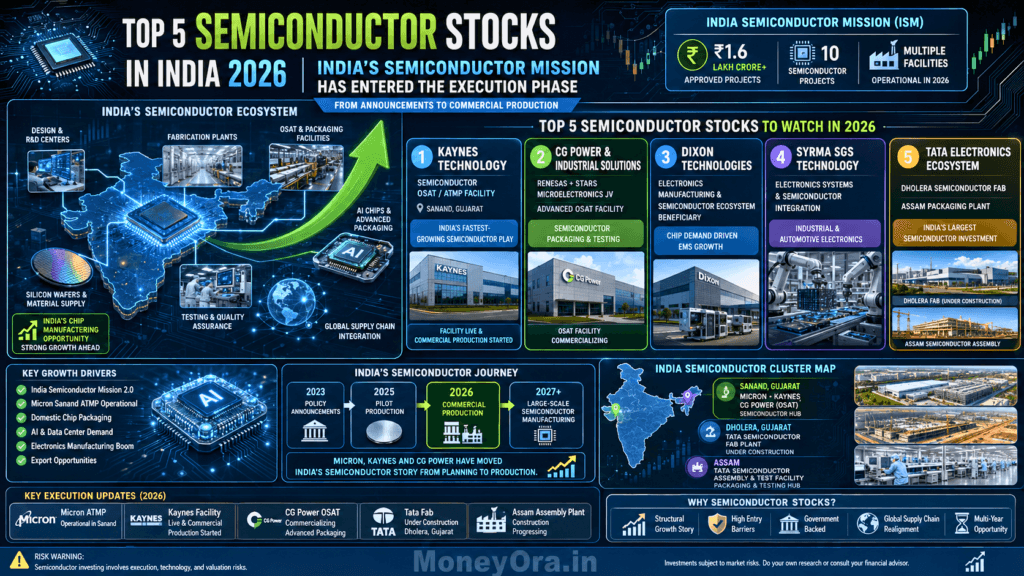

Here is something most semiconductor stocks articles will not tell you. India approved ₹1.64 lakh crore in semiconductor manufacturing investments by May 2026. Tata Electronics’ ₹91,000 crore fab is under construction in Dholera. CG Power’s OSAT with Renesas is commercially operational. Kaynes’ ATMP facility started shipping chips. Micron’s Sanand plant is already exporting memory chips globally. “semiconductor stocks serve the data center supply chain — see India’s top data center stocks”

And yet, the stock that most people bought as a “semiconductor play” — Kaynes Technology — fell 27% after its Q4 FY26 results. Dixon Technologies has barely 5% semiconductor revenue exposure despite the sector label. Several ETF articles still list companies with zero chip manufacturing revenue as “semiconductor stocks.”

The problem is not the theme. India’s semiconductor story is real and it is accelerating. The problem is the gap between narrative and numbers — between what companies have announced and what they are actually earning from semiconductor operations today. “semiconductor stocks serve the data center supply chain — and the same data centers are driving a historic surge in electricity demand, making solar power companies one of 2026’s most watched investment themes”

This article fixes that. Five semiconductor stocks in India. Real FY26 revenue numbers. Actual OSAT and fab status. Honest valuation. Specific risks. And exactly what you need to watch before putting money in.

India Semiconductor Mission — State of Play (June 2026)

ISM 1.0 budget:₹76,000 crore | 50% capital subsidy

ISM 2.0 (Budget 2026-27):₹1,000 crore | focus: equipment, materials, design IP

Approved projects:12 facilities across 6 states | ₹1.64 lakh crore total investment

Micron Sanand:Commercial production since Feb 2026 — shipping DRAM/NAND globally

CG Power-Renesas OSAT:Inaugurated Aug 2025 | Commercial operations underway

Kaynes ATMP Sanand:Commercial operations began late 2025

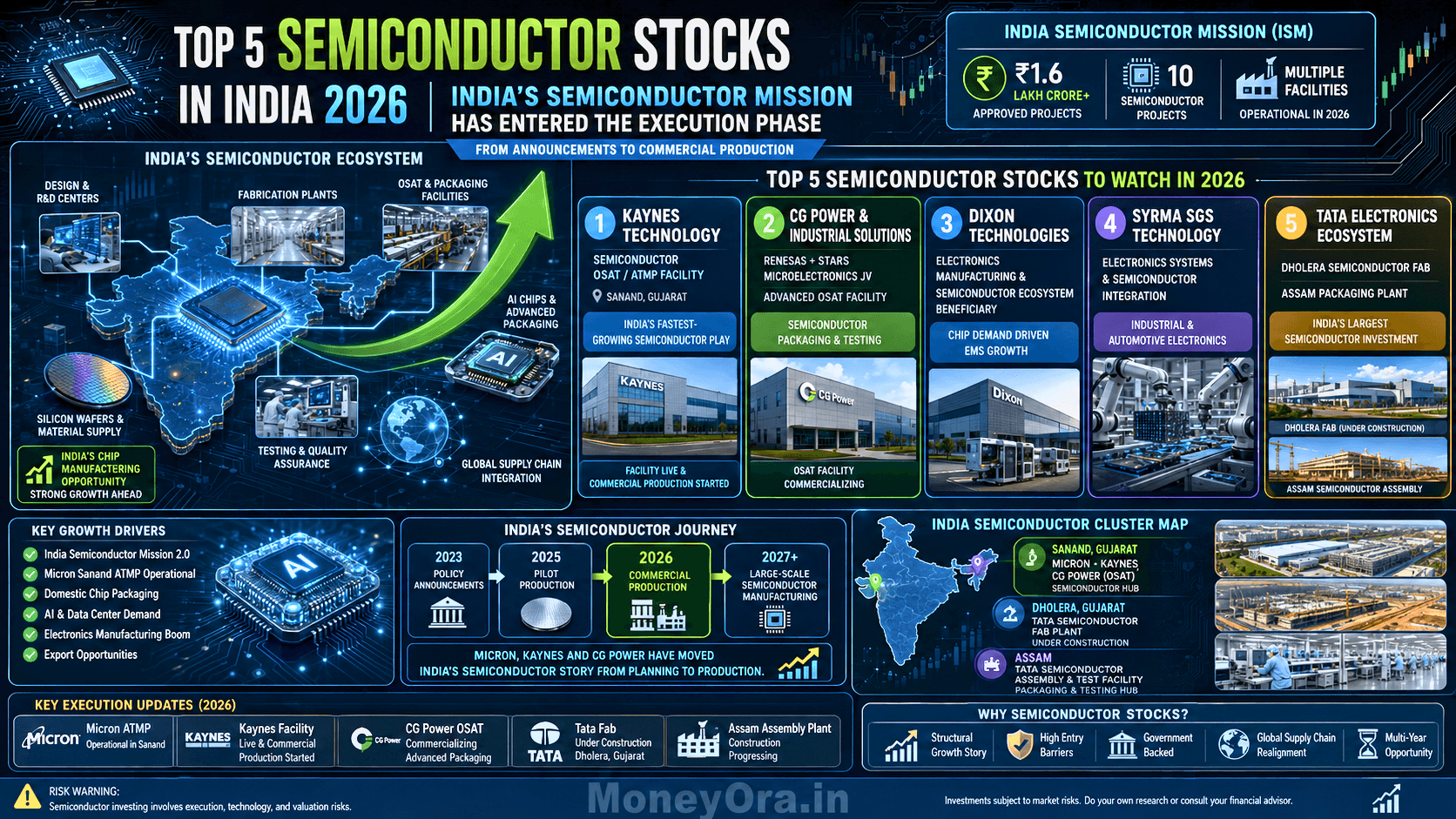

Tata Electronics fab (Dholera):First silicon target — late 2026

Tata OSAT (Assam):Pilot production mid-2026 | 48 million chips/day at full capacity

India semiconductor market by 2030:USD 100+ billion (12–13% CAGR)

Why India’s Semiconductor Stocks Moment Is Different in 2026

Every year since 2021, someone has written about India’s semiconductor opportunity. Most of those articles aged badly. Companies announced fabs. Stocks ran 200–400%. Then results disappointed. The stocks corrected. The “opportunity” was real but the timeline was wrong.

2026 is different because the transition from announcement to physical production has started.

Micron’s Sanand ATMP facility opened commercially in February 2026 — Prime Minister Modi inaugurated it personally. It is now shipping DRAM and NAND flash chips to global markets. CG Power-Renesas OSAT was inaugurated in August 2025 and has been in commercial operations since. Kaynes’ ATMP facility commenced production in late 2025. Tata’s Dholera fab is under active construction and on track for first silicon in late 2026.

Why the Semiconductor Value Chain Matters for Stocks

Quick Definition: The semiconductor value chain has three layers:

(2) Fabrication (Fab) — turning silicon wafers into chip dies;

(3) OSAT/ATMP — assembling, packaging and testing finished chips. India currently has OSAT/ATMP operations live, a fab under construction, and chip design strength (125,000 engineers, 20% of global total). Listed Indian semiconductor stocks are primarily in the OSAT/ATMP and EMS layers.

The reason this matters for stock selection: companies doing OSAT/ATMP today are earning semiconductor revenue now. Companies “building fabs” are 2–4 years from revenue. Investors who confuse announcements with earnings end up with stocks that look expensive without the growth to justify it.

The Numbers Behind India’s Semiconductor Sector

India Semiconductor Sector — Key Statistics (2026)

Metric

Value

Context

ISM 1.0 budget

₹76,000 crore

50% capital subsidy for approved projects

ISM 2.0 (FY27)

₹1,000 crore

Equipment, materials, design IP focus

Approved investments (12 projects)

₹1.64 lakh crore

Across 6 states

India semiconductor design engineers

125,000

20% of global total

India semiconductor market FY25

USD 45–53 billion

Growing to USD 100B by 2030

Total electronics production FY25

₹11.3 lakh crore

Exports up 37.5%

PLI electronics scheme

~$2.7 billion

Announced March 2025

Tata Electronics fab capacity

50,000 wafers/month

~3 billion chips/year at full capacity

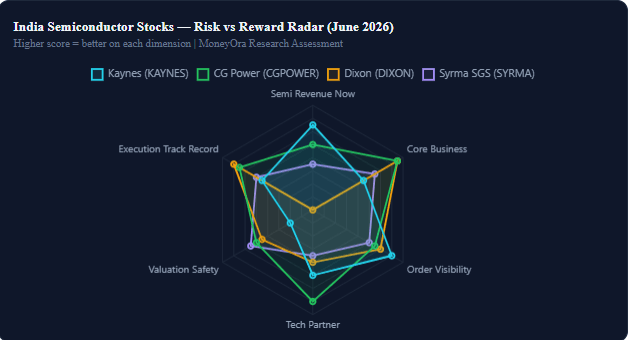

1: Kaynes Technology India (NSE: KAYNES)

Kaynes Technology is the most direct listed play on India’s semiconductor assembly story — and it is also the most frustrating one to own in 2026.

The ATMP facility in Sanand is live. Commercial operations began within 14 months of the groundbreaking — which, for a semiconductor facility, is genuinely fast. The HDI PCB plant in Chennai is nearing operational readiness. Kaynes now has capabilities across design, manufacturing, and advanced packaging. No other listed Indian company can say that.

FY26 Financial Results — Kaynes Technology

Kaynes Technology India — FY26 Full Year Results

Metric

FY26

FY25

YoY Change

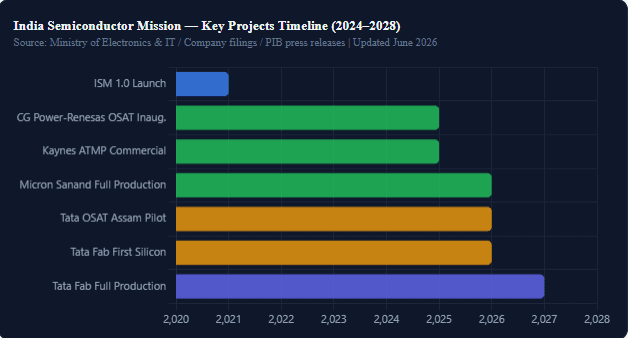

Revenue from Operations

₹3,626 Cr

₹2,724 Cr

+33.24%

Net Profit (PAT)

₹364 Cr

₹294 Cr

+24.01%

Order Book (FY26 end)

₹8,366 Cr

—

Record high

Market Cap (Jun 2026)

₹20,782–₹21,257 Cr

—

Down ~45% in 1Y

52-Week Range

₹2,995–₹7,705

—

Wide — high volatility

Promoter Holding

53.5%

—

Stable majority

P/B Ratio

4.49x

—

Moderate

The Semiconductor Story Within Kaynes

Kaynes Semicon — the ATMP subsidiary — received Union Cabinet approval for its ₹3,300 crore Sanand facility in September 2024. Capacity: 6 million chips per day. The project qualifies for 50% capex subsidy under ISM. Commercial operations commenced, and the company explicitly confirmed OSAT is “rapidly scaling up” in its FY26 annual results statement.

SEALSQ Corp and Kaynes Semicon have entered a final agreement to develop a Sovereign Indian Post-Quantum Semiconductor Joint Venture — adding a cutting-edge cryptographic chip angle to the existing ATMP operations.

Bull Case: Order book of ₹8,366 crore provides 2+ years of revenue visibility. OSAT revenue ramp-up + HDI PCB will add a high-margin layer in FY27–FY28. The 33% revenue CAGR is already being delivered. Analyst buy consensus with targets ₹5,500–₹6,200. Stock at ₹3,162 (June 1, 2026) is trading near 52-week lows, which is historically a compelling entry zone for long-term investors.

Bear Case: Q4 FY26 profit missed analyst estimates significantly — JP Morgan cited “weaker margins and unfavourable mix.” Stock fell 27% post-results. OSAT revenue ramp-up is slower than expected. Independent director resigned May 31, 2026. SEBI settlement order against former MD (₹23.43 lakh paid) adds governance noise. PE still elevated despite the correction.

“Kaynes Technology is the only pure-play listed Indian company directly in the semiconductor ATMP supply chain, a business that will grow 40 to 50 percent annually as Tata and Vedanta fabs require domestic testing and packaging services.” — Ankit Jaiswal, Senior Research Analyst, Univest (2026)

2: CG Power & Industrial Solutions (NSE: CGPOWER)

CG Power is the most underappreciated semiconductor stock in India. Here is why.

Most articles focus on Kaynes as the semiconductor play because it has “semiconductor” in its subsidiary name. But CG Power has a larger, more financially robust core business — power transformers, motors, switchgear — that generates reliable cashflow. And on top of that core, it has an operational semiconductor OSAT facility with Renesas Electronics Japan as its technology partner.

The CG Semi Story

CG Semi Private Limited — CG Power’s semiconductor subsidiary — inaugurated its OSAT facility in Sanand, Gujarat in August 2025. This facility was built in collaboration with Renesas Electronics Corporation (Japan) and Stars Microelectronics (Thailand). Total investment commitment: ₹7,600 crore across two facilities (G1 and G2) over five years. The G1 facility is operational. G2 is under planning.

Renesas is not a small partner. It is one of the world’s top 10 semiconductor companies with approximately $9 billion in annual revenue and strong positions in automotive, industrial, and IoT chips. Having Renesas as technology partner gives CG Semi immediate access to chip design, process knowledge, and — critically — commercial volume from Renesas’ production network.

CG Power Financial Snapshot (FY26)

CG Power & Industrial Solutions — Key Metrics (June 2026)

Metric

Value

Context

Market Cap

₹3.77 lakh crore

Large-cap; significant liquidity

Core Business Revenue (FY26)

₹9,000+ Cr (est.)

Power equipment, motors, switchgear

CG Semi OSAT status

Commercial operations

Inaugurated Aug 2025

Tech Partner

Renesas Electronics (Japan)

Top-10 global semiconductor company

Total investment (CG Semi)

₹7,600 Cr

G1 + G2 combined over 5 years

ISM Subsidy

50% capex

Cabinet approved

CMP (BSE, recent)

₹1,390

Market cap ~₹3.77 lakh crore

ROE / ROCE

Above 20% (core business)

Strong efficiency metrics

Why CG Power Has the Best Risk-Reward Among Semiconductor Stocks

The argument for CG Power as the primary Indian semiconductor stock is not the OSAT alone — it is the combination. The power equipment business is profitable, growing, and provides a very real earnings floor. If the semiconductor operations face delays or execute slowly, the core business still delivers returns. If CG Semi scales rapidly (aided by Renesas’ commercial volume), the semiconductor revenues add exponential upside.

That combination — profitable core plus semiconductor optionality from a commercially operational OSAT — is genuinely hard to find in any other listed Indian company.

Bull Case: CG Semi G2 facility development, Renesas volume ramp, automotive chip demand from India’s EV push. Core power business growing at 15–20%. ISM 2.0 adds more policy support. Analyst targets ₹900–₹1,600 for 12 months.

Bear Case: CG Semi FY27 commercial output still scaling — full revenue contribution likely FY28. High market cap means modest upside from current levels vs the valuation of the semiconductor option. CG Power’s management history (debt restructuring in 2020) is a reminder that corporate governance requires ongoing monitoring.

3: Dixon Technologies India (NSE: DIXON)

Dixon Technologies is India’s largest Electronics Manufacturing Services company. ₹21,000+ crore in FY26 revenue. Deals with Apple (iPhone components), Lenovo, Samsung, Motorola, and nearly every major consumer electronics brand that manufactures in India. It is a genuinely excellent company.

What Dixon Actually Does in Semiconductors

Dixon manufactures televisions, mobile phones, washing machines, CCTVs, and LED lights. It is the assembler of finished electronics, not the maker of chips inside them. The semiconductor angle comes from two directions:

PCB manufacturing: Dixon is investing in circuit board production — a component in the semiconductor supply chain but downstream from actual chip making

Lenovo partnership: Dixon secured a significant contract with Lenovo for electronics manufacturing — driving revenue but not semiconductor revenue specifically

India chip ecosystem beneficiary: As India’s domestic semiconductor supply chain builds, Dixon — as the largest domestic assembler — is well-positioned to source chips locally and potentially integrate backward into semiconductor components

Dixon FY26 Financial Data

Dixon Technologies India — FY26 Key Metrics

Metric

FY26

Context

Revenue

₹21,000+ Cr (est.)

+88% from FY24; fastest-growing EMS company

1-Year Stock Return

−14.5% YTD (2026)

Correction from peak despite strong operations

Semiconductor revenue %

<5%

Not a pure-play semiconductor stock

Key clients

Apple, Lenovo, Samsung

Global electronics brands

China+1 beneficiary

Strong positioning

As brands exit China manufacturing

Honest Assessment: Do not pay semiconductor PE multiples for Dixon Technologies. You are buying India’s best EMS company with a strong 5-year growth trajectory. The semiconductor optionality is real but distant. If you want direct semiconductor exposure today, Kaynes or CG Power are more accurate plays. If you want India’s electronics manufacturing boom with some semiconductor adjacency, Dixon is excellent.

“Dixon’s semiconductor plans are less than 1% of current operations. Do not pay semiconductor valuations for a TV assembler.” — Orunodoi.com Research (2026)

4: Syrma SGS Technology (NSE: SYRMA)

Syrma SGS is smaller than Dixon and less well-known than Kaynes, but as of 2026, it is JP Morgan’s top pick in the India EMS/semiconductor sector. That is worth paying attention to.

What Syrma Does in the Semiconductor Value Chain

Syrma SGS manufactures semiconductor modules, precision PCBA (Printed Circuit Board Assembly), RFID systems, and IoT electronics. It holds defence and aerospace electronics certifications — which give it quality credibility for semiconductor supply chain participation that most EMS companies cannot claim. Revenue growing at 30–35% annually. It provides semiconductor module manufacturing that sits between raw chip supply and finished product assembly.

Syrma SGS Financial Snapshot (2026)

Syrma SGS Technology — Key Metrics (2026)

Metric

Value

Context

Revenue Growth

30–35% YoY

Consistent multi-year track record

JP Morgan recommendation

Top Pick (EMS sector)

“Best risk-reward among EMS names”

1-Year return (YTD 2026)

+2%

Most resilient EMS stock; KAYN −10%, DIXO −14.5%

Key differentiator

Aerospace/Defence certifications

High-quality signal for semiconductor supply chain

RFID/IoT exposure

Growing

IoT drives semiconductor content per product

Bull Case: Best 2026 YTD performance among India’s EMS/semiconductor stocks (+2% vs peers −10 to −14%). JP Morgan top pick with “high conviction on revenue path, valuation discount and consumer electronics upcycle.” Defence electronics certifications provide a quality moat. Smaller scale means higher growth potential as it captures semiconductor ecosystem contracts.

Bear Case: Q3 FY26 profit of ₹76.6 crore missed analyst estimates of ₹112 crore — ICICI Securities flagged “muted growth and lack of traction in industrial segment.” Smaller scale means thinner margin for error. Less liquid stock than Kaynes or Dixon.

5: Tata Electronics Ecosystem Plays

Tata Electronics is the most important company in India’s semiconductor story. Its ₹91,000 crore fab at Dholera — partnered with Taiwan’s PSMC — will produce approximately 3 billion chips per year when at full capacity. Tata’s OSAT in Assam will produce 48 million chips per day. These are not marginal projects. They define whether India builds a semiconductor industry or just imports components forever.

But here is the problem: Tata Electronics is not listed. It is a private company within the Tata Group. You cannot buy its shares on NSE or BSE.

How to Get Tata Electronics Semiconductor Exposure

Option A: Tata Elxsi (NSE: TATAELXSI)

Tata Elxsi is a listed Tata Group company providing engineering R&D and chip design services. It designs the software stack for semiconductor products — automotive ADAS, medical devices, consumer electronics. It does not fabricate chips, but it is embedded in the design chain that feeds Tata Electronics’ fab. Risk: Tata Elxsi’s stock is down 28% from 52-week highs amid ER&D sector pressure. Analyst targets range ₹3,350 (Motilal Oswal Sell) to ₹4,110 (ICICI Securities Add). Our full analysis: see our tech stock deep dives on MoneyOra.

Option B: Vendor Companies in Tata’s Supply Chain

Kaynes Technology and Syrma SGS are mentioned in the context of Tata fab supply chain participation. As Tata Electronics’ OSAT in Assam and the Dholera fab start production, these companies may receive component and services contracts.

Option C: Wait for the Tata Electronics IPO

Market consensus: Tata Electronics files for IPO post-2027, likely 2028–2029, after the Dholera fab achieves commercial production and generates audited revenue. The IPO will likely be one of the largest in Indian history given the strategic importance and the Tata Group backing.

Tata Electronics Fab: Key Data Points

Tata Electronics Semiconductor Projects — Status (June 2026)

Project

Location

Investment

Capacity

Status

Dholera Fab (with PSMC)

Gujarat

₹91,000 Cr

50,000 wafers/month; ~3 Bn chips/year

Construction ongoing; First silicon late 2026

OSAT/ATMP (Tata TSAM)

Assam (Morigaon)

₹27,000 Cr

48 million chips/day

Pilot production mid-2026

Tata-Bosch MoU

Global

—

Advanced chip packaging

Signed July 2025

Tata-ASML MoU

—

—

Lithography equipment access

Recently signed

SEZ status (Dholera)

Gujarat

—

66-hectare facility + ICD

Notified April 9, 2026

Master Comparison: All 5 Semiconductor Stocks at a Glance

India’s Top 5 Semiconductor Stocks — Full Comparison (June 2026)

Stock

NSE

CMP (₹)

Mkt Cap

Semi Revenue %

OSAT/Fab Status

1Y Return

Analyst View

Risk Level

Kaynes Technology

KAYNES

~₹3,162

₹20,782 Cr

Growing (OSAT)

OSAT Commercial

−45% from high

Buy | Target ₹5,500–₹6,200

High

CG Power & Ind. Sol.

CGPOWER

~₹1,390

₹3.77 L Cr

CG Semi growing

OSAT Commercial

+Positive

Buy | Target ₹900–₹1,600

Medium

Dixon Technologies

DIXON

Market price

Large cap

<5% (EMS)

EMS — No fab/OSAT

−14.5% YTD

Mixed | Value EMS story

Medium-Low

Syrma SGS

SYRMA

Market price

Mid-cap

Semiconductor modules

EMS + Semi modules

+2% YTD

JP Morgan Top Pick

Medium

Tata Elxsi (proxy)

TATAELXSI

~₹4,650

~₹26,000 Cr

Design services

Design — No fab/OSAT

−28%

Mixed | Long-term hold

Medium

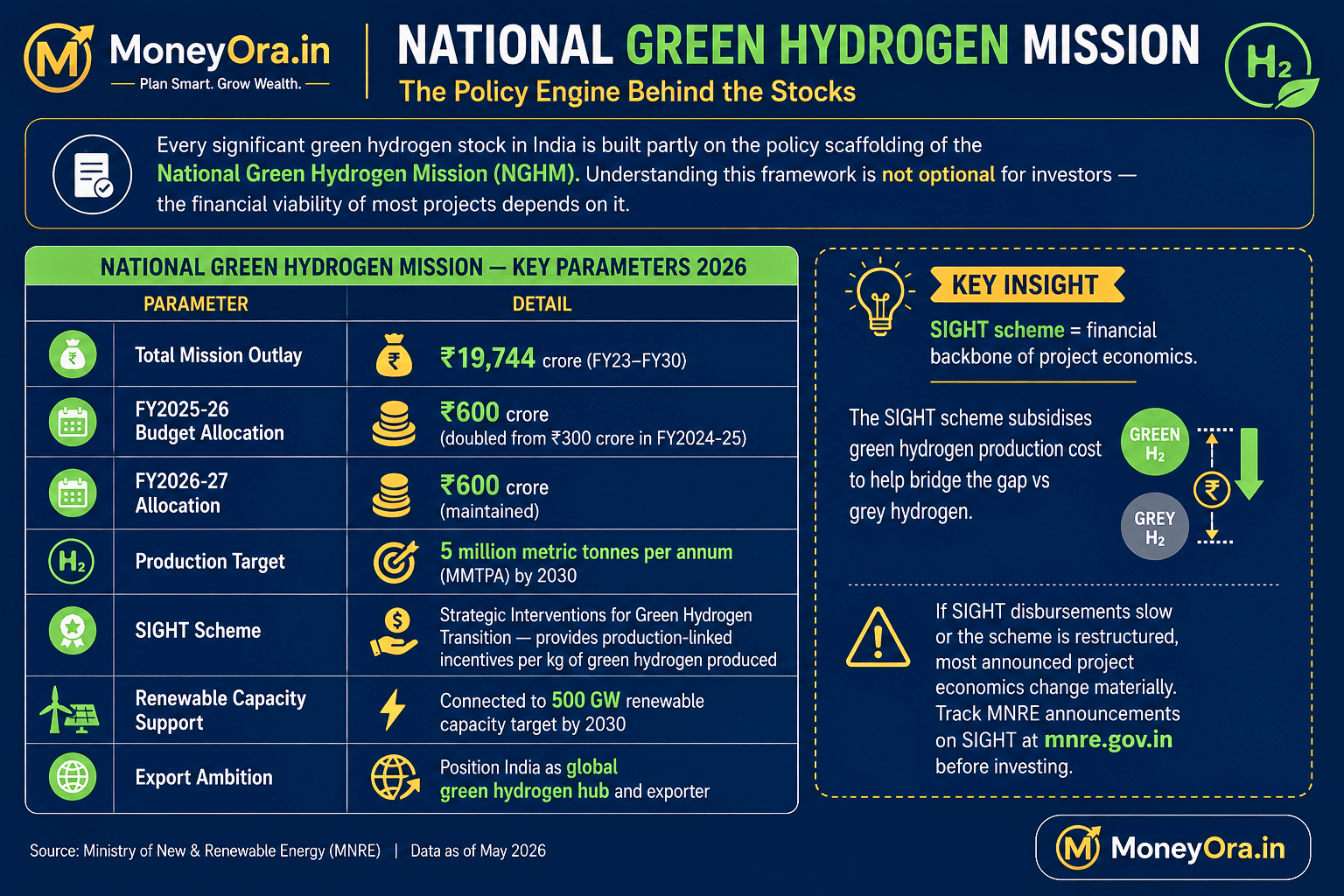

India Semiconductor Mission: What Every Investor in Semiconductor Stocks Needs to Know

The India Semiconductor Mission (ISM) is the policy backbone behind every semiconductor stock on this list. Without understanding it, you cannot assess the investment risk properly.

ISM 1.0: The Foundation (December 2021)

ISM 1.0 launched with a ₹76,000 crore incentive framework providing 50% capital subsidy for approved semiconductor projects. As of May 2026, 12 facilities across 6 states have been approved under ISM, with cumulative investment of ₹1.64 lakh crore. The key approved projects include:

Tata Electronics-PSMC fab, Dholera: ₹91,000 crore | First silicon late 2026

CG Power-Renesas-Stars Micro OSAT, Gujarat: ₹7,600 crore | Commercial since Aug 2025

Kaynes Semicon ATMP, Gujarat: ₹3,300 crore | Commercial since late 2025

Micron Technology ATMP, Sanand: Commercial since Feb 2026 | Full production

ISM 2.0: The Next Phase (Budget 2026-27)

The Union Budget 2026-27 announced ISM 2.0, shifting focus from attracting fabs to building the entire supporting ecosystem. According to PIB’s official release on ISM 2.0, the programme will:

Prioritise domestic manufacturing of semiconductor equipment and materials

Fund industry-driven research and advanced training centres

Allocation: ₹1,000 crore for FY2026-27

ISM 2.0 shifts money toward the semiconductor ecosystem companies rather than just the fabs themselves. This is positive for Kaynes, Syrma, and other supply chain players.

The Invest India Overview

For a comprehensive understanding of the semiconductor investment landscape, the Invest India official semiconductor overview provides the government’s perspective on which parts of the value chain India is targeting and why.

How to Invest in Semiconductor Stocks in India: A Practical Guide

Step 1 — Define Your Semiconductor Investment Thesis

Choose one of three positions:

Early OSAT play (higher risk, higher potential): Kaynes Technology — operational, growing, high PE, needs OSAT revenue ramp to justify valuation

Balanced core + semiconductor (medium risk): CG Power — profitable power business plus operational OSAT with Renesas

EMS with semiconductor adjacency (lower risk): Dixon or Syrma — strong EMS businesses, semiconductor exposure building over 3–5 years

Step 2 — Size Position Based on Risk, Not Conviction

Semiconductor stocks in India are high-PE, early-stage. For most portfolios, total semiconductor sector allocation should not exceed 10–15% of equity. Use our position size calculator to set the right rupee allocation based on your total portfolio and risk tolerance.

Step 3 — Track the Earnings That Actually Matter

For semiconductor stocks specifically, track:

OSAT/ATMP revenue as a separate line item (Kaynes, CG Power)

Order book from semiconductor clients specifically

Margin trend in semiconductor division vs EMS division

ISM project milestones — each milestone is a positive catalyst

Tata Electronics fab construction timeline updates

Step 4 — Set Stop-Losses Before Buying

Semiconductor stocks can fall 25–40% on single earnings misses (Kaynes fell 27% post-Q4 FY26). Define your maximum loss per position before entering. Use our stop loss calculator to set levels based on technical support and your portfolio risk budget.

Step 5 — Consider SIP Approach for Volatile Stocks

For high-volatility semiconductor stocks, entering in tranches rather than a lumpsum reduces timing risk. Use our stock average calculator to track your average cost as you build the position over 3–6 months.

Real Risks: What Can Go Wrong with Indian Semiconductor Stocks

Risk 1: Revenue Reality Gap

As Orunodoi’s research explicitly states: “When global headlines celebrate India’s semiconductor boom, they’re referring to government announcements, land allocations, and construction cranes — not commercial chip production.” Most semiconductor revenue in India’s listed stocks still comes from electronics assembly, not chip manufacturing. Watch actual semiconductor revenue as a segment, not aggregate revenue.

Risk 2: High PE Multiples on Distant Revenue

CG Power’s OSAT revenue visibility improves by FY28. Tata fab first silicon is targeted for late 2026 with commercial ramp in 2027–2028. Stocks are priced for these future revenues today. Any delay reprices the whole thesis.

Risk 3: Technology Execution

Running a semiconductor fab or OSAT requires precision, skilled engineers, and process stability that takes years to develop. India has the design talent but limited fab operations experience. Early-phase yield rates and quality metrics for Indian OSAT facilities are critical unknowns.

Risk 4: US Export Controls

Advanced semiconductor manufacturing equipment (EUV lithography from ASML, advanced etch tools) is subject to US and Dutch export controls. Tata Electronics-ASML MoU is a positive signal, but restrictions that apply to China could, under extreme scenarios, be applied more broadly. This affects the timeline for advanced node capability in India.

Risk 5: Policy Dependency

ISM economics depend on 50% capital subsidy disbursement. Any delay in government payments affects project cashflow and stock fundamentals. The semiconductor industry also relies on continued government procurement preference for domestically manufactured chips.

Stock Analysis Tools

PE Ratio Calculator — Compute forward PE for Kaynes or CG Power at different earnings growth scenarios

What are the best semiconductor stocks in India for 2026?

The top 5 semiconductor stocks in India for 2026 are:

(1) Kaynes Technology (NSE: KAYNES) — only listed company with live OSAT semiconductor assembly;

(2) CG Power (NSE: CGPOWER) — commercial OSAT with Renesas, profitable core business;

(3) Dixon Technologies (NSE: DIXON) — India’s largest EMS company with semiconductor adjacency;

(4) Syrma SGS (NSE: SYRMA) — JP Morgan’s top pick, semiconductor modules and precision PCBA; (5) Tata Electronics ecosystem plays via Tata Elxsi or supply chain companies.

What is India’s Semiconductor Mission (ISM)?

ISM was launched in December 2021 with ₹76,000 crore in incentives offering 50% capital subsidy. As of May 2026, 12 semiconductor projects worth ₹1.64 lakh crore are approved across 6 states. Major projects: Tata Electronics’ 28nm fab (₹91,000 crore), Tata OSAT Assam (₹27,000 crore), CG Power-Renesas OSAT (₹7,600 crore), Kaynes ATMP (₹3,300 crore). ISM 2.0 (Budget 2026-27) adds ₹1,000 crore for equipment and design IP. Official details: PIB ISM 2.0 release.

Is Kaynes Technology a good semiconductor stock?

Kaynes Technology is the most direct listed semiconductor play with an operational ATMP facility. FY26: revenue ₹3,626 crore (+33%), PAT ₹364 crore (+24%), order book ₹8,366 crore. But Q4 FY26 profits missed estimates and the stock fell 27% post-results. 52-week range: ₹2,995–₹7,705. Currently near 52-week lows. Long-term buy thesis intact; near-term volatility from OSAT revenue ramp-up pace.

What is OSAT in the semiconductor context?

OSAT (Outsourced Semiconductor Assembly and Test) takes chip die from wafer fabs and assembles them into packaged, tested finished chips. It is the downstream layer of the semiconductor value chain. CG Power (with Renesas) and Kaynes Technology operate OSAT facilities in India. OSAT requires less capital than a full fab and produces revenue faster — making it the most viable near-term semiconductor revenue generator for listed Indian stocks.

Which semiconductor stock has the highest multibagger potential?

CG Power has the most balanced multibagger profile: a profitable core power business provides earnings stability, while CG Semi’s operational OSAT with Renesas adds genuine semiconductor revenue upside. Kaynes has higher pure upside if OSAT scales rapidly but also higher risk if margins disappoint again. Tata Electronics (when it lists) will likely be the largest semiconductor multibagger — but that IPO is post-2027.

Will Tata Electronics list on the stock exchange?

Tata Electronics is expected to IPO post-2027, after its Dholera semiconductor fab achieves commercial production. Until then, the exposure is indirect via Tata Elxsi, supply chain companies, or Tata Group holding vehicles. The Tata Electronics IPO is likely to be one of India’s largest given the ₹91,000 crore fab investment and the strategic importance of the company.

How do I invest in semiconductor stocks in India?

Open a demat account, then buy listed semiconductor stocks directly: Kaynes Technology (KAYNES), CG Power (CGPOWER), Dixon Technologies (DIXON), Syrma SGS (SYRMA), or Tata Elxsi (TATAELXSI). Use MoneyOra’s PE ratio calculator to assess valuation, position size calculator to size your allocation, and stop loss calculator to define your downside before entering.

What is the India semiconductor market size by 2030?

India’s semiconductor market is projected to grow from USD 45–53 billion (FY25) to over USD 100 billion by 2030, at a 12–13% CAGR. India has 125,000 semiconductor design engineers — 20% of the global total. Electronics production reached ₹11.3 lakh crore in FY25 with exports up 37.5%. The government targets USD 500 billion in total electronics production by 2030.

What are the risks of Indian semiconductor stocks?

Key risks: (1) Revenue gap — semiconductor manufacturing revenue is minimal today; (2) High PE on future revenues 3–5 years out; (3) Technology execution — India is building fab expertise; (4) US export controls on chip equipment; (5) Government policy dependency; (6) Global chip cycle — the semiconductor industry is cyclical. Always consult a SEBI-registered advisor before investing.

Is CG Power a semiconductor stock or a power company?

CG Power is both. Its primary revenue comes from power equipment, motors, and switchgear — a profitable, growing business. Its CG Semi subsidiary is an operational OSAT facility with Renesas Electronics as a technology partner. As semiconductor revenue ramps, CG Power’s revenue mix will shift. Currently, the semiconductor business is a small but fast-growing fraction of total revenue. The core business provides financial stability that pure-play semiconductor stocks (Kaynes) lack.

India’s semiconductor mission moved from announcement to production in 2025–2026.

That is a meaningful inflection point. Micron is shipping DRAM from Sanand.

CG Power-Renesas OSAT is commercial. Kaynes’ ATMP is scaling.

Tata’s fab will produce first silicon by year-end. These are not press releases — they are production milestones.

But the gap between what is happening in semiconductor facilities and what is priced into semiconductor stocks is still wide.

Kaynes fell 27% on disappointing quarterly results even as its OSAT was operational.

Dixon still has under 5% semiconductor revenue despite the sector label.

CG Power’s semiconductor contribution is early-stage.

The honest framework for Indian semiconductor stocks in 2026:

you are buying 3–5 year revenue growth that has not fully arrived yet.

The companies with the best risk-reward are the ones where the core business already works

CG Power especially and the semiconductor operations are additive, not foundational to the thesis.

Size appropriately. Use stop-losses. Monitor OSAT revenue specifically, not aggregate revenue.

And remember that Tata Electronics’ IPO when it comes will likely be the largest single semiconductor

event in India’s stock market history. Patient investors who use this period to understand the sector

will be better positioned when it arrives.

Track Semiconductor Stocks & Plan Your Portfolio on MoneyOra

PE Ratio Calculator — Evaluate Kaynes, CG Power, Dixon at different earnings scenarios

CAGR Calculator — Calculate actual semiconductor stock returns vs promises

SIP Calculator — Build semiconductor sector position systematically

Disclaimer: This article is for informational and educational purposes only. All data is sourced from NSE/BSE filings, Screener.in, company press releases, and published news as of June 2026. This does not constitute investment advice. Semiconductor stocks carry high market risk including total loss of capital. Please consult a SEBI-registered investment advisor before making any investment decisions.

**Mukesh Rajbhar**

**Founder & Finance Writer at MoneyOra**Mukesh Rajbhar is the founder of MoneyOra, a finance-focused platform dedicated to helping Indian investors make informed decisions through data-driven research and market analysis.He covers Indian stock market trends, AI stocks, defence sector companies, banking and financial tools, IPOs, mutual funds, and long-term wealth-building opportunities. His content focuses on simplifying complex financial topics into actionable insights for retail investors.At MoneyOra, Mukesh researches company fundamentals, earnings reports, industry trends, government policies, and market developments to provide readers with accurate and up-to-date financial information.**Areas of Expertise*** Indian Stock Market Analysis

* AI & Technology Stocks

* Defence Sector Investments

* Banking & Financial Services

* Long-Term Investing Strategies

* Market News & Economic Trends**Connect with Mukesh Rajbhar*** Website: MoneyOra.in**Disclaimer:** The information provided is for educational and informational purposes only and should not be considered financial or investment advice. Investors should conduct their own research or consult a qualified financial advisor before making investment decisions.

Pingback: AI Stocks Picks 2026: Next 5 Best Multibagger AI Stocks

Pingback: Netweb Technologies Share Price Target 2026: Next AI Multibagger Stock? - MoneyOra

Pingback: Defence Index 2026: Top Investment Opportunity or Overvalued Risk for Investors?

Pingback: Share Market Today: Will Nifty & Sensex Continue Their Bull Run This Week 26? - MoneyOra

Pingback: Reliance Power Share: Honest Analysis After Q4 FY26 Results