Option Price Calculator: Calculate Fair Option Value Using Black-Scholes

What Is an Option Price Calculator? (Black-Scholes Model)

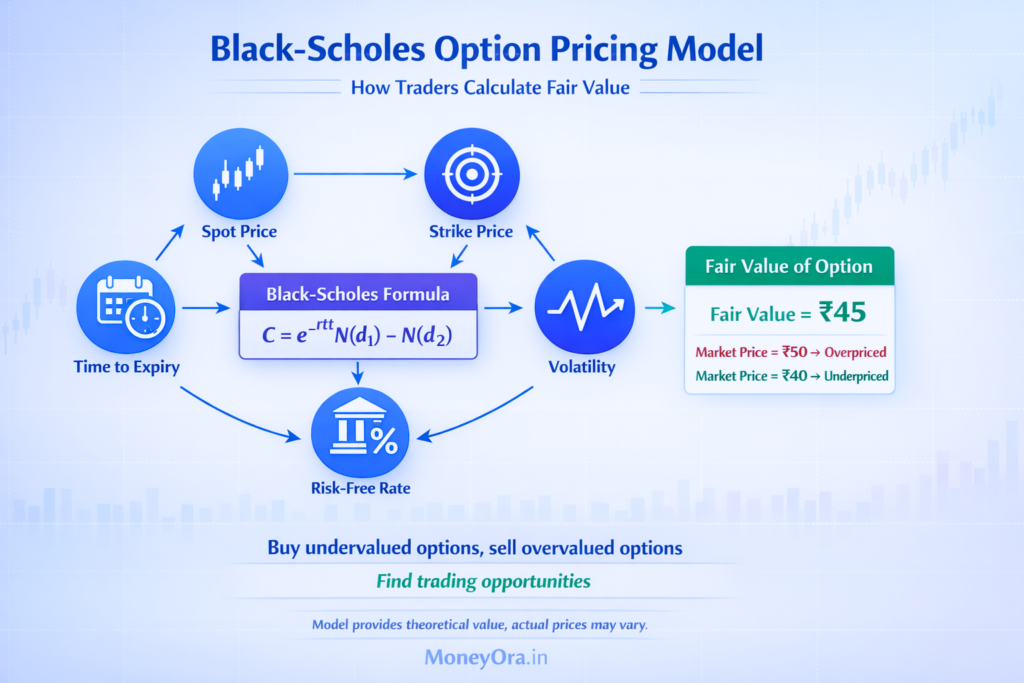

The option price calculator is software that computes what an option should cost. The Black-Scholes model is the formula behind it. In 1973, two economists—Fischer Black and Myron Scholes—created it. The option price calculator accounts for five things:

Spot price (current stock/index price)

Strike price (the agreed price to buy/sell)

Time to expiry (days remaining)

Volatility (how much the underlying moves)

Risk-free rate (interest rates)The option price calculator spits out what the option should be worth right now. In real markets, options trade above or below that fair value. That's where traders make money.

Why use an option price calculator?

Without it, you don't know if something's overpriced or underpriced.

With an option price calculator, you have a mathematical baseline.

Professional traders compare actual prices to what the option price calculator says.

That's how they find opportunities.

How Does an Option Price Calculator Work? (Step-by-Step)

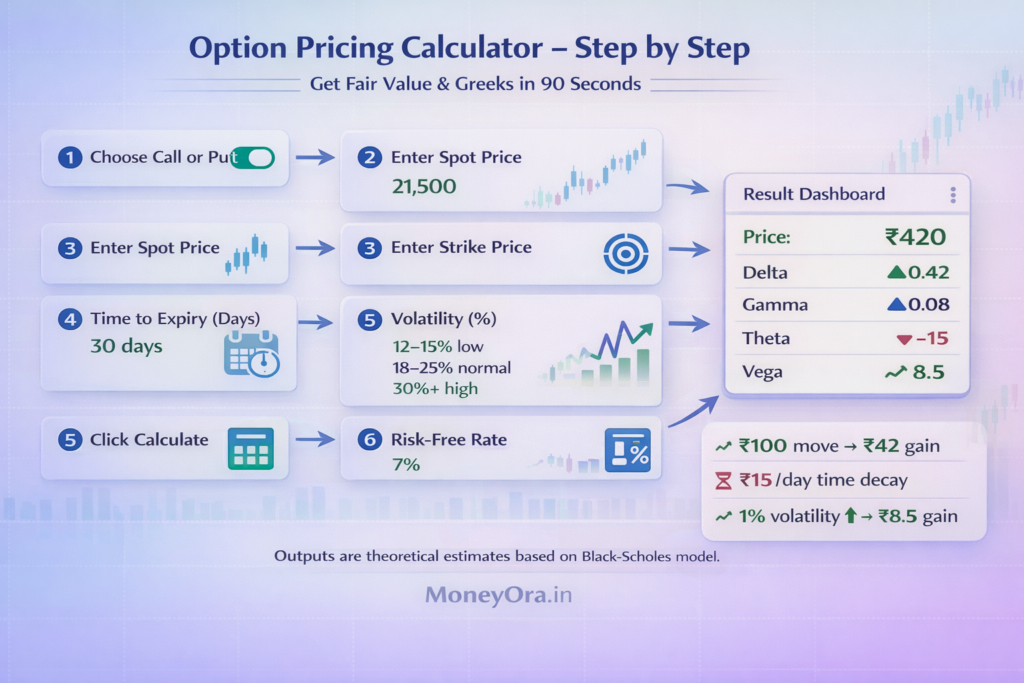

Using an option price calculator takes 90 seconds. Here's the exact process:

Step 1: Choose Call or Put

Click the radio button for "Call" or "Put." This determines which option you're pricing with the option price calculator.

Step 2: Enter Spot Price

Type the current price of the underlying. For Nifty: 21,500. For a stock: current market price.

Step 3: Enter Strike Price

Type the strike price of the option you're pricing. This is the key input for the option price calculator.

Step 4: Enter Time to Expiry (Days)

How many days until the option expires? Weekly options: 1-7 days. Monthly options: 20-30 days.

Step 5: Enter Volatility

This is the tricky input. Historical volatility is what the underlying has moved. Implied volatility is what the market expects. If unsure, use implied volatility from the current options chain. The option price calculator is sensitive to this input.

Step 6: Enter Risk-Free Rate

This is the interest rate (usually 6-7% in India). The option price calculator defaults to 7%. Adjust if you want precision.

Step 7: Click Calculate

Results appear instantly. The option price calculator outputs:

Theoretical Price: Black-Scholes fair value

Delta: How the price changes with ₹1 stock move

Gamma: How delta changes

Theta: Daily time decay

Vega: Price change if volatility moves 1%Now you know what the option should cost. Compare to actual market price.

Real Example Using the Option Price Calculator:

Nifty call, 22000 strike, current price 21,500, 30 days to expiry, 18% volatility. Using the option price calculator: Input: Spot 21500, Strike 22000, Days 30, Vol 18%, Rate 7%Output: Price ₹420, Delta 0.42, Gamma 0.08, Theta -15, Vega 8.5Fair value is ₹420. Market price: ₹475. The option is overpriced by ₹55.

Understanding Greeks From Your Option Price Calculator

The option price calculator outputs more than just the price. It shows four Greek letters. These Greeks tell you how the option behaves under different market conditions.

Delta From the Option Price Calculator

Delta = How much the option price changes when the underlying moves ₹1.

Delta of 0.6 means if the stock goes up ₹1, the option goes up ₹0.60.Deeper in-the-money options have delta near 1.0 (move like the stock).

Deeper out-of-the-money options have delta near 0 (barely move).At-the-money options have delta around 0.5.Use your option price calculator to check delta before every trade.

Gamma From the Option Price Calculator

Gamma = How much delta changes when the underlying moves ₹1.

High gamma = Delta changes fast (explosive price moves).Low

gamma = Delta changes slowly (predictable moves).Out-of-the-money options have high gamma. In-the-money options have low gamma. Your option price calculator shows gamma. Check it to understand position acceleration.

Theta From the Option Price Calculator

Theta = How much the option loses per day (time decay).Theta is always negative for long positions (time works against you).Theta is positive for short positions (time works for you).Near expiry, theta accelerates. Days have more impact. At-the-money options have the highest theta. The option price calculator shows your daily bleed. Use it to decide if the trade is worth it.

Vega From the Option Price Calculator

Vega = How much the option price changes if volatility goes up 1%.Vega of 5 means if volatility increases 1%, the option price goes up ₹5.Long-dated options have higher vega. Out-of-the-money options are vega-sensitive. In-the-money options are less vega-sensitive. Your option price calculator shows this. Check vega before earnings or volatile events.

Why Check Greeks From the Option Price Calculator?

These Greeks tell you your actual risk. Selling a call with theta +5 means you make ₹5 per day from time decay. Holding a call with gamma 0.05 means your delta accelerates. A call with vega 10 means volatility spikes destroy your position. The option price calculator gives you the full picture.

Call Option vs Put Option - Option Price Calculator Differences

The option price calculator prices both calls and puts. But they behave differently.

Calls: What Does the Option Price Calculator Show?

Spot price goes UP

Volatility goes UP

Time goes UP (more time for stock to rise)

Strike price is LOWER (cheaper to buy)

Example using option price calculator:

Nifty 22000 call

Current Nifty: 21,500

Days to expiry: 30

Volatility: 18%

Option price calculator shows: ₹450

If Nifty moves to 22,000, the option price calculator would show ₹600. Profit ₹150 instantly.

If volatility spikes to 22%, the option price calculator shows ₹520. Profit without price move.

Puts: What Does the Option Price Calculator Show?

A put is worth more when:

Spot price goes DOWN

Volatility goes UP

Time goes UP (more time for stock to fall)

Strike price is HIGHER (better to sell)

Example using option price calculator:

Nifty 22000 put

Current Nifty: 21,500

Days to expiry: 30

Volatility: 18%

Option price calculator shows: ₹350

If Nifty drops to 21,000, the option price calculator would show ₹700. Profit ₹350 instantly.

Key Difference:

Calls profit from UP moves. Puts profit from DOWN moves. Both are harmed by time decay. That's where sellers make money. Your option price calculator handles both. Input a call or put, get fair value and Greeks instantly.

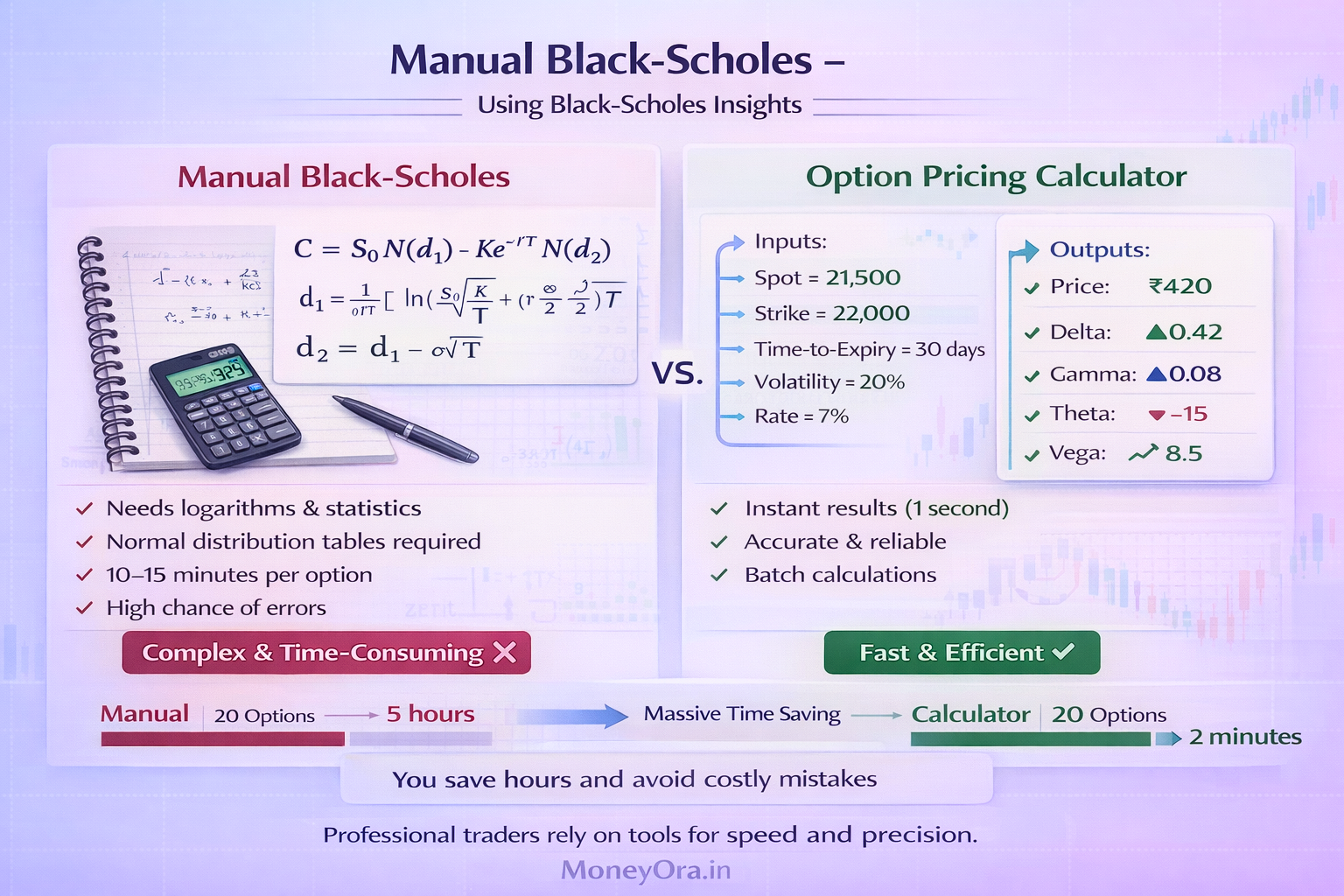

Option Price Calculator vs Manual Spreadsheet—Why Use Ours

You could calculate option prices manually. Here’s why traders don’t.

Black-Scholes Formula (The Math):

C = S₀ × N(d₁) – K × e^(-rT) × N(d₂)

Where:

– d₁ = [ln(S₀/K) + (r + σ²/2)T] / (σ × √T)

– d₂ = d₁ – σ × √T

– N(d₁), N(d₂) = Normal distribution values (need a statistical table or calculator)

– S₀ = Spot price

– K = Strike price

– r = Risk-free rate

– σ = Volatility

– T = Time in years

– e = 2.71828…

– ln = Natural logarithm

You need:

– A calculator that does logarithms

– A table of normal distribution values (or software)

– Knowledge of the formula

– 10-15 minutes per option

– Mental energy to avoid mistakes

Our Calculator:

– Input 5 numbers

– Click calculate

– Get answer in 1 second

– Greeks included

– No errors

Time Comparison:

Calculate 1 option manually: 15 minutes

Calculate 20 options: 5 hours

Calculate 20 options with our calculator: 2 minutes

You save ~5 hours per day.

Accuracy:

Manual calculation: Error-prone (logarithm mistakes, distribution lookup errors)

Our calculator: Verified, tested, used by professional traders

Plus:

Our calculator lets you:

– Vary volatility to see sensitivity

– Compare calls vs puts instantly

– Input different expirations

– Batch multiple options

– Export results

That’s why it’s indispensable for serious option traders