The $450 billion solar shift is here. Smart money is moving fast — here’s exactly where it’s going, and why, backed by Q1 2026 earnings, Goldman Sachs data, and India’s explosive growth numbers.

Utility-scale solar farms like this are at the heart of why institutional investors are buying solar power companies at record pace in 2026.

Utility-scale solar farms like this are at the heart of why institutional investors are buying solar power companies at record pace in 2026.

Something unusual is happening in the stock market right now. While most sectors face headwinds from interest rate uncertainty, solar power companies are attracting institutional capital at a speed that’s turning heads on Wall Street — and in Dalal Street, Mumbai.

Here’s the problem most investors face: the Solar power companies sector contains both spectacular winners and dangerous traps. Some companies like Sunnova have already filed for Chapter 11 bankruptcy in 2025. Others, like First Solar, are delivering record revenue quarters and 47-gigawatt order backlogs. Knowing which is which could be the difference between a 10x return and a total wipeout.

This guide covers exactly why investors are suddenly piling into specific solar power companies in 2026, which companies are worth watching (globally and in India), what the real financial numbers look like, and where the sector is headed by 2030. Whether you’re tracking NSE/BSE solar stocks or global names like FSLR and NEE, this is the most current, data-backed breakdown available today.

Why are investors buying solar power companies in 2026?

Three forces converge: AI data center electricity demand is forecast to rise 165% by 2030 (Goldman Sachs), Solar power companies is now the cheapest form of new electricity generation globally, and both India and the US are flooding the sector with policy-driven capital. First Solar power companies posted record Q1 2026 revenue of $1.04 billion. Goldman Sachs projects global solar installations reaching 914 GW by 2030.

The AI boom and solar investment boom are two sides of the same story: data centers need electricity, and solar is now the cheapest way to generate it.

The AI boom and solar investment boom are two sides of the same story: data centers need electricity, and solar is now the cheapest way to generate it.

The 3 Unstoppable Forces Driving Solar Investment in 2026

Before we get to the specific companies, you need to understand why the timing matters so much right now. These three macro catalysts are creating a convergence that sophisticated investors haven’t seen in renewable energy before.

1. The AI Data Center Electricity Crisis

This is the story that changes everything. The same AI revolution that’s disrupting every industry is also creating a colossal, insatiable demand for electricity. And that demand is landing squarely in Solar power companies’s lap.

Goldman Sachs forecasts that global data center power demand will surge 165% by 2030 compared to 2023 levels. To put that in perspective: the power needs of AI data centers by 2030 will equal the entire current electricity consumption of Portugal, Greece, and the Netherlands combined.

Where does solar fit?

Goldman estimates that roughly 27.5% of this new capacity will come from Solar power companies. Tech giants signing long-term Power Purchase Agreements (PPAs) with solar operators is no longer a PR exercise — it’s core infrastructure strategy. Companies like First Solar power companies already have signed PPAs with data center operators at $35 per megawatt-hour for 15-year terms.

2. Solar Is Now Definitively Cheaper Than Fossil Fuels

This wasn’t true five years ago. It is today. The levelized cost of solar electricity has fallen over 90% in the past decade. Utility-scale solar farms in Sun Belt states are generating internal rates of return of 8–12% annually in 2026 — comparable to premium real estate — without the geopolitical risk of oil and gas.

The global Solar power companies market was on track to see $450 billion in investment in 2025, surpassing every other power generation technology. That figure will grow in 2026 and beyond, driven by AI demand, electrification, and government mandates.

3. Government Policy Tailwinds on Two Continents

In the US, the 45X Advanced Manufacturing Production Tax Credit under the Inflation Reduction Act continues to benefit domestic solar manufacturers like First Solar power companies, which explicitly cited this program in its 2025 full-year results. In India, the Union Budget 2026–27 included customs duty exemptions to strengthen domestic solar manufacturing competitiveness. India’s national target of 500 GW renewable energy by 2030 — with solar as the dominant pillar — is creating a decade-long investment runway.

The Top 5 Solar Power Companies Investors Are Buying Right Now

These aren’t just the biggest by market cap. They’re the companies with the strongest financial fundamentals, clearest growth visibility, and most defensible market positions as of mid-2026. We’ve analyzed Q1 2026 earnings, analyst ratings, backlog data, and institutional positioning.

First Solar, Inc.

If there is one solar power company that has genuinely separated itself from the pack in 2026, it is First Solar. The Arizona-based thin-film manufacturer is doing something no other solar company has fully replicated: manufacturing at scale, in the United States, using technology that is completely independent of the Chinese silicon supply chain.

Think about that backlog number: 47.9 gigawatts of contracted orders stretching to 2030. This isn’t speculative demand — it’s signed contracts. First Solar’s CEO Mark Widmar described Q1 2026 as delivering “record first-quarter revenue, record sales in India, meaningful margin expansion.” The company is investing $800M–$1B in 2025 capex, including a $330 million sixth US facility in South Carolina.

Why Investors Are Bullying Into FSLR Right Now

Three specific reasons drive institutional buying: (1) The company’s thin-film CdTe technology sidesteps US–China trade tensions entirely, making it uniquely resilient to tariff escalation; (2) its $2.0 billion net cash position as of March 2026 means it is self-funding its growth without dilution risk; and (3) the AI data center PPA pipeline means revenue visibility is unusually high for a manufacturing company.

INVESTMENT STRENGTHS

- No Chinese supply chain exposure

- Record revenue & margins Q1 2026

- 47.9 GW backlog — revenue clarity to 2030

- US manufacturing — tariff-proof

- Strong balance sheet: $2B net cash

RISKS TO MONITOR

- High valuation relative to peers

- Technology limited to thin-film (not silicon)

- Policy change risk on 45X tax credits

- Global execution risk as India operations scale

NextEra Energy, Inc.

NextEra bills itself as the world’s largest producer of wind and solar energy — and the numbers back that claim. What makes it compelling for investors who want solar exposure with a safety net is that it operates through Florida Power & Light, a regulated utility serving Florida (stable, predictable cash flows), and NextEra Energy Resources, its competitive renewables arm that builds and operates the world’s largest clean energy portfolio.

NextEra is the closest thing to a “sleep well at night” solar stock. Its regulated utility base generates predictable earnings regardless of energy prices. Meanwhile, NextEra Energy Resources is aggressively signing new contracts with AI companies and data centers looking for long-term clean power solutions. The company’s scale — it has developed more wind and solar projects than any other company in the world — gives it procurement advantages, interconnection priority, and bankability that smaller players simply cannot match.

INVESTMENT STRENGTHS

- Regulated utility = stable cash flows

- World’s largest renewables portfolio

- Preferred partner for AI company PPAs

- Dividend growth track record

- S&P 500 component — institutional backing

RISKS TO MONITOR

- Higher rates increase financing costs

- Regulatory risk in Florida

- Large market cap limits upside vs smaller plays

- Hurricane exposure in Florida operations

Brookfield Renewable Partners

Brookfield Renewable is the globally diversified option for investors who want solar power company exposure without betting on a single market or technology. Its portfolio spans hydroelectric, solar, and wind assets across North America, South America, Europe, and Asia — all backed by long-term power purchase agreements with creditworthy utilities and corporations.

For income-focused investors, Brookfield’s over-4% dividend yield as of mid-2026 is unusually attractive in a sector where most pure-play solar stocks pay nothing. The company’s business model — build or acquire assets, sign long-term fixed-rate contracts, collect steady cash — is purpose-built for capital preservation with growth upside.

Brookfield also benefits from its parent company’s (Brookfield Asset Management) deal-making muscle, giving it access to acquisition opportunities and project financing that independent solar companies cannot match.

INVESTMENT STRENGTHS

- 4%+ dividend — rare in solar sector

- Globally diversified — no single market risk

- PPAs provide cash flow predictability

- Backed by Brookfield Asset Management

- Available as both LP (BEP) and Corp (BEPC)

RISKS TO MONITOR

- Interest rate sensitivity on yields

- Hydro assets face drought/climate risk

- Complex corporate structure

- Limited upside vs pure-play manufacturers

Array Technologies, Inc.

Array Technologies is the most interesting “picks and shovels” play in the solar power sector. Rather than generating electricity itself, Array makes the solar tracking systems that allow solar panels to follow the sun throughout the day — increasing energy output by 15–25% compared to fixed-tilt installations. As of mid-2026, Array’s trackers have helped deliver 99 GW of power worldwide.

The 2025 acquisition of APA Solar for $179 million was a strategic masterstroke. APA is a leading provider of engineered foundation solutions for solar projects. Combined with Array’s trackers, the deal lets Array offer an integrated tracker-plus-foundation system that no competitor currently matches at this scale — expanding their total addressable market by 40% and pulling in the $1.2 billion US utility-scale tracker foundations segment.

That acquisition drove 15% volume growth in Q1 2026 alongside improved profitability — exactly what you want to see post-acquisition.

INVESTMENT STRENGTHS

- B2B model — sells to every solar farm

- Post-acquisition TAM expanded by 40%

- 15% volume growth Q1 2026

- Not exposed to end-consumer pricing risk

- Integrated tracker+foundation = moat

RISKS TO MONITOR

- Smaller market cap = more volatile

- Depends on new solar farm construction rates

- Competition from Nextracker, Arctech

- Integration risk from APA Solar deal

Enphase Energy, Inc.

Enphase is the most complex story on this list — and that’s precisely why there may be an opportunity here. The company’s microinverter-based solar-plus-storage systems are the gold standard for residential solar. Its technology converts DC power to AC at the individual panel level, delivering better efficiency, safety, and monitoring than conventional string inverters. But Enphase’s 2026 story is a turnaround narrative, not a momentum trade.

Q1 2026 was a mixed report: revenue dropped 20.6% year-over-year to $282.9 million, and operating margins turned negative at -10.5%. However, adjusted EPS of $0.47 beat analyst forecasts, and management guided next-quarter revenue in line with expectations. The stock jumped 3.2% when First Solar’s record Q1 results lifted the whole sector — suggesting the market still respects Enphase’s franchise.

The catalyst to watch: Enphase published a technical white paper in May 2026 on GaN (Gallium Nitride) technology for next-generation distributed power electronics. This isn’t marketing fluff — GaN enables meaningfully more efficient, smaller, and cheaper microinverters. Enphase is also targeting AI data centers with its new solid-state transformer (SST) platform, which could open an entirely new enterprise revenue stream beyond residential solar.

INVESTMENT STRENGTHS

- Premium brand in residential solar

- GaN technology = next-gen edge

- AI data center pivot (SST platform)

- Beaten-down valuation creates entry opportunity

- Software + hardware ecosystem = customer lock-in

RISKS TO MONITOR

- Revenue in active decline (-20.6% YoY)

- Negative operating margins Q1 2026

- Tariff headwinds from supply chain

- Residential solar market slowdown

- 34% below 52-week high as of May 2026

Top Solar Power Companies in India Listed on NSE/BSE

The Indian market for solar stocks is structurally different from the US. You’re not just investing in energy — you’re investing in infrastructure development at a national scale, backed by government policy, international climate commitments, and a rapidly growing domestic power demand base driven by urbanization and manufacturing growth.

| Company | Exchange | Segment | Key Strength | Watch For |

|---|---|---|---|---|

| Adani Green Energy | NSE/BSE | Generation (Utility Scale) | Largest solar portfolio in India | Capacity expansion milestones |

| Tata Power Solar | NSE: TATAPOWER | Generation + Rooftop + EV | Diversified clean energy play; Navi Mumbai presence | Rooftop solar order book |

| JSW Energy | NSE/BSE | Generation + Storage | Heavy investment in green pipeline | Storage capacity additions |

| Waaree Renewable Technologies | BSE Listed | EPC + Project Development | Fast-growing EPC player | Order pipeline growth |

| Sterling & Wilson Renewable | NSE/BSE | Global Solar EPC | International project execution | Global margin recovery |

| Premier Energies | NSE/BSE | Manufacturing (TOPCon Cells) | Mission 2028: 10 GW integrated capacity | JV with Sino-American Silicon |

| Borosil Renewables | NSE/BSE | Solar Glass Manufacturing | Only large-scale low-iron solar glass maker in India | Capacity utilization rates |

| Insolation Energy | BSE SME | Module Manufacturing (North India) | First listed solar module company in India; 4.5 GW plant | Channel partner expansion |

Solar Power Companies Near Navi Mumbai, Maharashtra

If you’re looking for solar power companies with operational presence near Navi Mumbai — including the Vashi corridor — Tata Power Solar is the most prominent listed company with active installations in the region. Maharashtra has been an early mover on state-level solar rooftop and industrial solar policy, making the MMR (Mumbai Metropolitan Region) a growing market for rooftop solar installations on commercial and industrial buildings.

Sterling & Wilson Renewable Energy, headquartered in Mumbai, also has project development activity in Maharashtra. For investors specifically seeking geographic concentration in the Navi Mumbai / Vashi market, these two companies offer the most direct exposure via listed stocks on NSE/BSE.

Head-to-Head: Top 5 Solar Stocks Compared (2026)

| Company | Ticker | Type | Revenue (TTM) | Key Risk | Best For |

|---|---|---|---|---|---|

| First Solar | FSLR | Manufacturer | ~$5.2B (FY2025) | 45X credit policy risk | Growth investors |

| NextEra Energy | NEE | Utility + Generator | Large-cap utility | Interest rate sensitivity | Conservative/dividend |

| Brookfield Renewable | BEP/BEPC | Asset Manager | Diversified global | Complex structure | Income + diversification |

| Array Technologies | ARRY | Tracker Supplier | ~$1.4B (est.) | Construction cycle risk | Picks-and-shovels play |

| Enphase Energy | ENPH | Microinverter/Storage | $282.9M (Q1 2026) | Revenue decline, margins | Turnaround / speculative |

The 2030 Solar Outlook: What “People Also Ask” Actually Wants to Know

Millions of people are searching for the same core question: is solar a safe long-term investment, or is this another tech bubble? Here’s what the data says about where solar power companies are headed through 2030. Goldman Sachs Research — Data center power demand forecasts: goldmansachs.com

Trend 1: The AI-Solar Industrial Complex

This is the dominant theme for the next four years. AI infrastructure requires enormous, reliable, cheap power. Solar delivers cheap power. Battery storage (increasingly integrated with solar projects) delivers reliability. The US alone will need $50 billion in new generation capacity for data centers, per Goldman Sachs estimates. Solar will capture a significant portion of that spend because it’s faster to build and cheaper to operate than any fossil fuel alternative. SEC EDGAR (First Solar) — Q1 2026 earnings press release: sec.gov

Trend 2: India Becomes the World’s Fastest-Growing Solar Market

India’s 500 GW renewable target by 2030, combined with its relatively young power grid, makes it arguably the most exciting market in global solar over the next decade. First Solar has already reported record sales in India in Q1 2026. Domestic manufacturers like Waaree Energies and Premier Energies are racing to build vertically integrated capacity before international competition arrives at scale. The Motley Fool — Best Solar Energy Stocks for 2026: fool.com

Trend 3: Solar + Storage Becomes the Default Infrastructure Choice

Standalone solar projects are giving way to solar-plus-battery installations, which solve the intermittency problem that has historically limited solar’s grid contribution. As battery prices fall (following the same cost-reduction curve as solar panels did a decade ago), this combination becomes investable at scale. Companies with storage capabilities — NextEra, Enphase, Brookfield — are positioned for this. SEBI (India) — Securities and Exchange Board of India investment guidance: sebi.gov.in

Trend 4: Domestic Manufacturing Premiums Will Expand

US–China trade tensions are not going away. The tariff environment of 2025 significantly increased costs for solar companies dependent on Chinese silicon supply chains. Companies like First Solar, which manufacture domestically using non-silicon technology, command a strategic premium that is growing, not shrinking. Indian manufacturers like Premier Energies (with its Taiwan JV) are making similar moves to secure supply chain independence. Ministry of New and Renewable Energy (India) — Solar energy policy: mnre.gov.in

Trend 5: The Bifurcation Between Winners and Losers Will Accelerate

Not all solar power companies are created equal. The bankruptcy of Sunnova in early 2025 (despite serving 410,000 customers) is a reminder that high debt + rising rates = catastrophic for capital-intensive solar businesses. The winners share common characteristics: strong balance sheets, long-term contracted revenue, technology differentiation, and manufacturing independence. The losers are over-leveraged, commodity-exposed, and policy-dependent. This gap will widen through 2030. IEA (International Energy Agency) — Global energy outlook: iea.org

The Solar power companies investment thesis in 2026 is not a bet on environmentalism Solar power companies

it’s a bet on the cheapest, fastest-to-deploy electricity infrastructure at a moment Solar power companies

when electricity demand is entering its most significant growth phase in modern history. Solar power companies

The convergence of AI data center demand, Solar power companies

government manufacturing incentives, supply chain reshoring, and India’s 500 GW ambition is creating a generational window. Solar power companies

Solar power companies with strong balance sheets, contracted revenues, and technology differentiation are the ones capturing institutional capital right now. Solar power companies

First Solar power companies leads on fundamentals. Solar power companies

NextEra leads on stability. Solar power companies

Brookfield leads on income and diversification. Solar power companies

Array Technologies leads on the picks-and-shovels infrastructure angle. Solar power companies

And Enphase, for patient investors, represents a beaten-down technology franchise with a credible comeback story. Solar power companies

In India, the story is simpler and perhaps even more exciting: Solar power companies

a government-backed, decade-long buildout of the world’s largest greenfield solar market, Solar power companies

accessible through listed stocks on NSE and BSE that most global investors are still underweight. Solar power companies

The sun is not running out of fuel. The question is only which solar power companies are positioned to capture the most value as the world races to harness it.

MoneyOra Calculators for Gold Investors and Economy Watchers

Gold Investment Tools

- Lumpsum Calculator — Model a one-time gold investment at 12–15% CAGR over 5–10 years

- SIP Calculator — Monthly systematic gold buying through digital gold or gold fund

- CAGR Calculator — Calculate gold’s actual return between any two dates

- FD Calculator — Compare guaranteed FD returns against gold’s historical CAGR

- SWP Calculator — Plan systematic withdrawals from a gold fund or gold ETF position

- RD Calculator — Safe recurring deposits as portfolio anchor alongside gold holdings

Long-Term Savings & Retirement

- PPF Calculator — Tax-free savings as the risk-free core of your financial plan, alongside gold

- NPS Calculator — National Pension System corpus planning; NPS equity+debt balance

- EPF Calculator — Provident fund as the foundation alongside gold as a hedge

Stock Market Tools

- Stock Return Calculator — Compare equity CAGR to gold’s 12–13% rupee CAGR

- PE Ratio Calculator — Evaluate gold-adjacent stocks like Solar Industries or Bharat Forge

- Dividend Calculator — Income from equity alongside your zero-dividend gold holdings

- Position Size Calculator — Size your gold allocation within total portfolio risk budget

- Stop Loss Calculator — For gold ETF or gold stock traders

- Margin Calculator — MCX gold futures margin requirements

- Brokerage Calculator — Transaction costs on gold ETF trades

- Option Price Calculator — MCX gold options pricing

Loan & Banking Tools

- EMI Calculator — Gold loan EMI calculation (banks lend up to 75% of gold value)

- Home Loan EMI Calculator — Balance property investment with gold allocation

- Personal Loan EMI Calculator

- Car Loan EMI Calculator

- Stock Average Calculator — For gold ETF accumulation over time

- IFSC Code Finder — Bank branch codes for SGB or gold fund investments

- Bank Details Finder — Verify bank details before any transfer

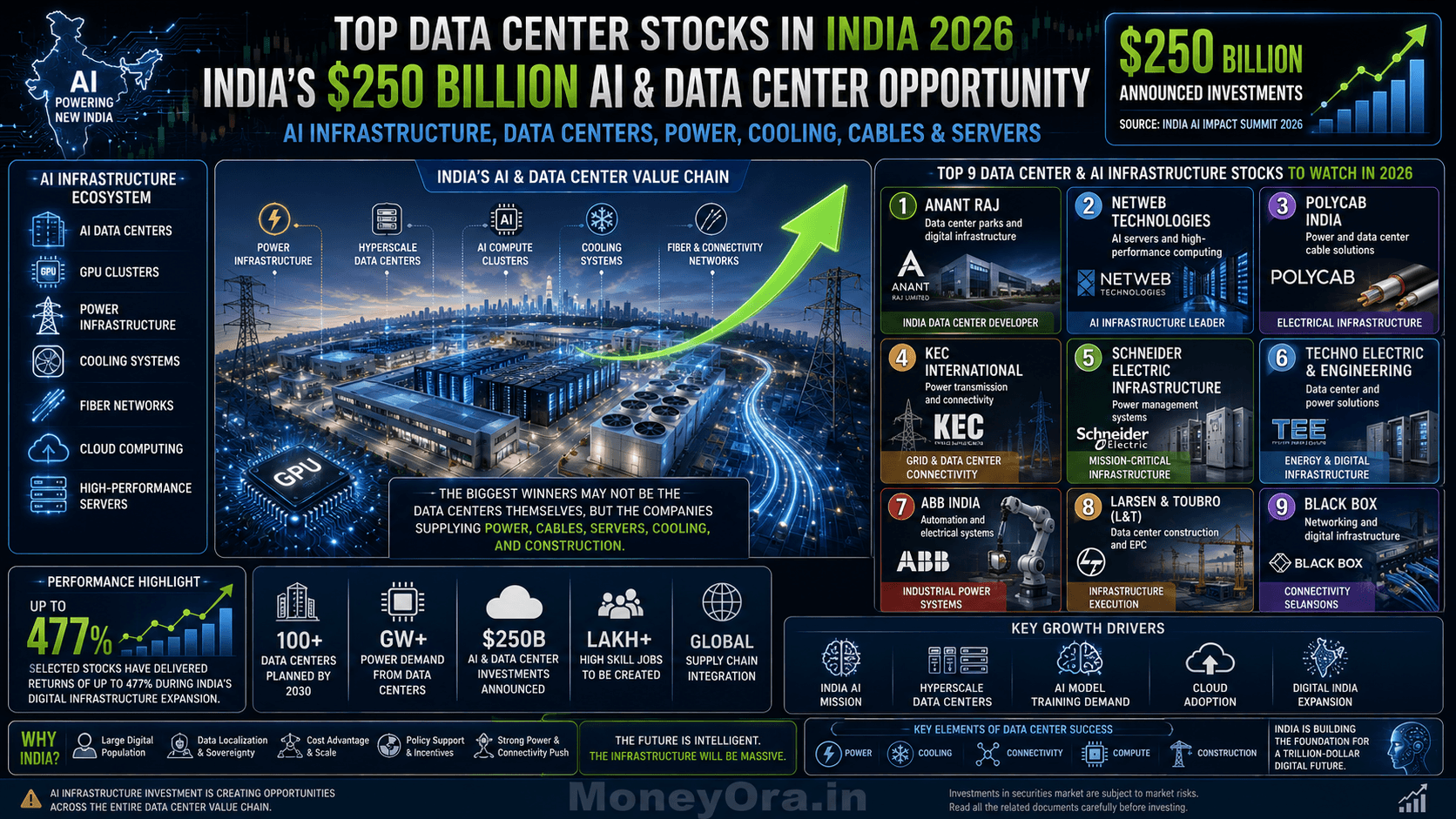

Pingback: Netweb Technologies Share Price Target 2026: Next AI Multibagger Stock? - MoneyOra

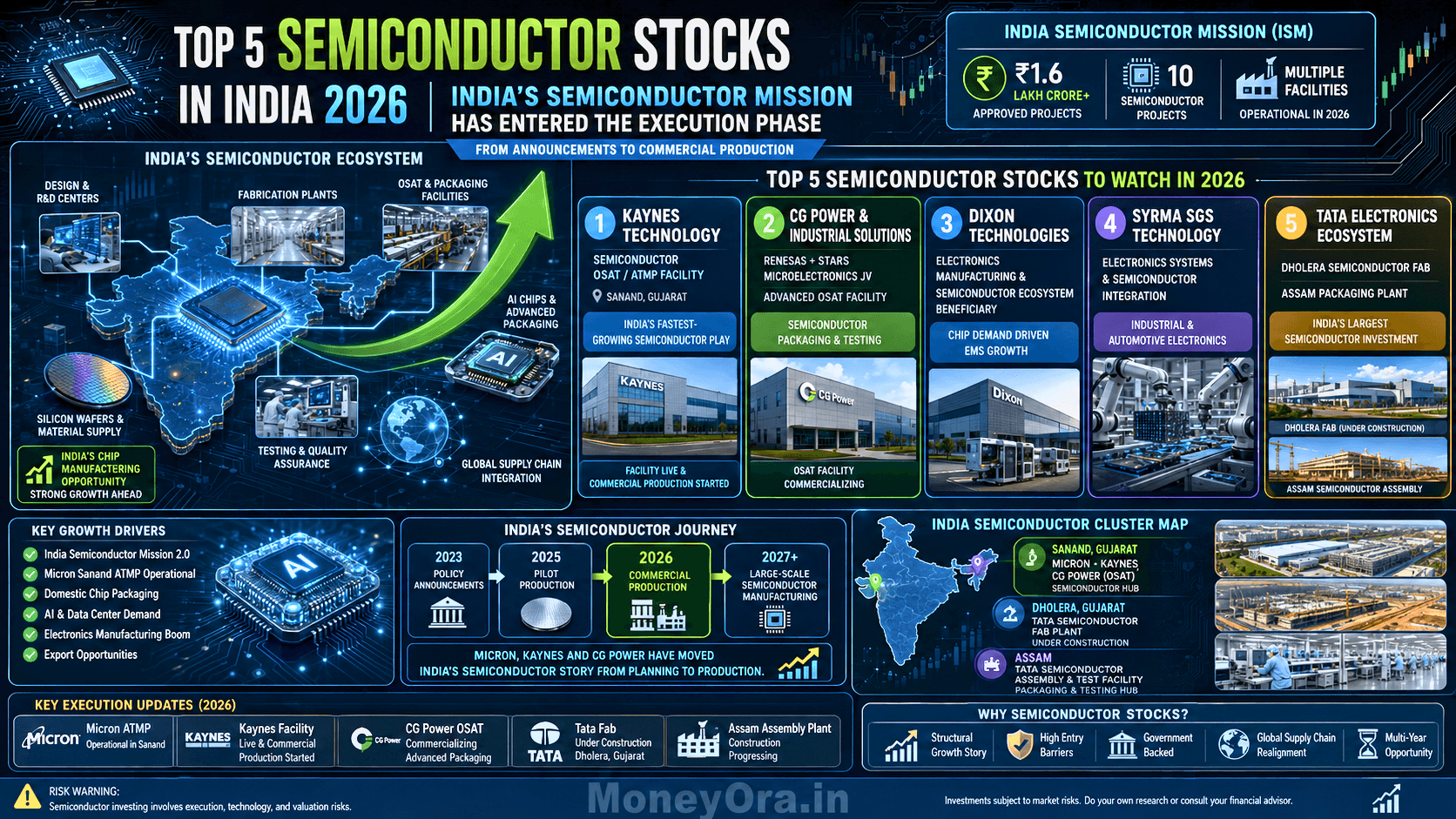

Pingback: Semiconductor Stock:Best 5 Multibagger Pick with Real Revenu

Pingback: AI Stocks Picks 2026: Next 5 Best Multibagger AI Stocks

Pingback: Share Market Today: Will Nifty & Sensex Continue Their Bull Run This Week 26? - MoneyOra