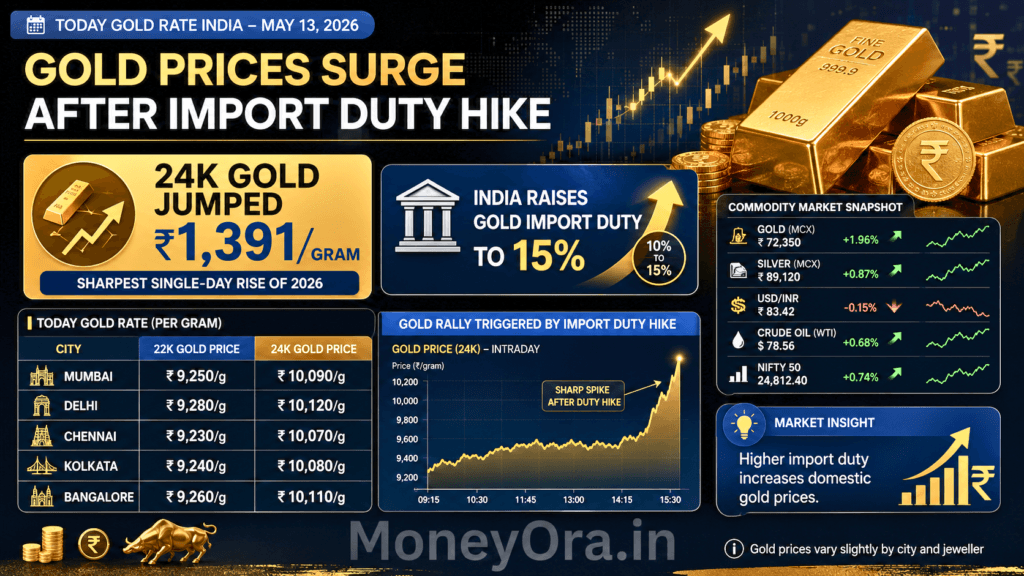

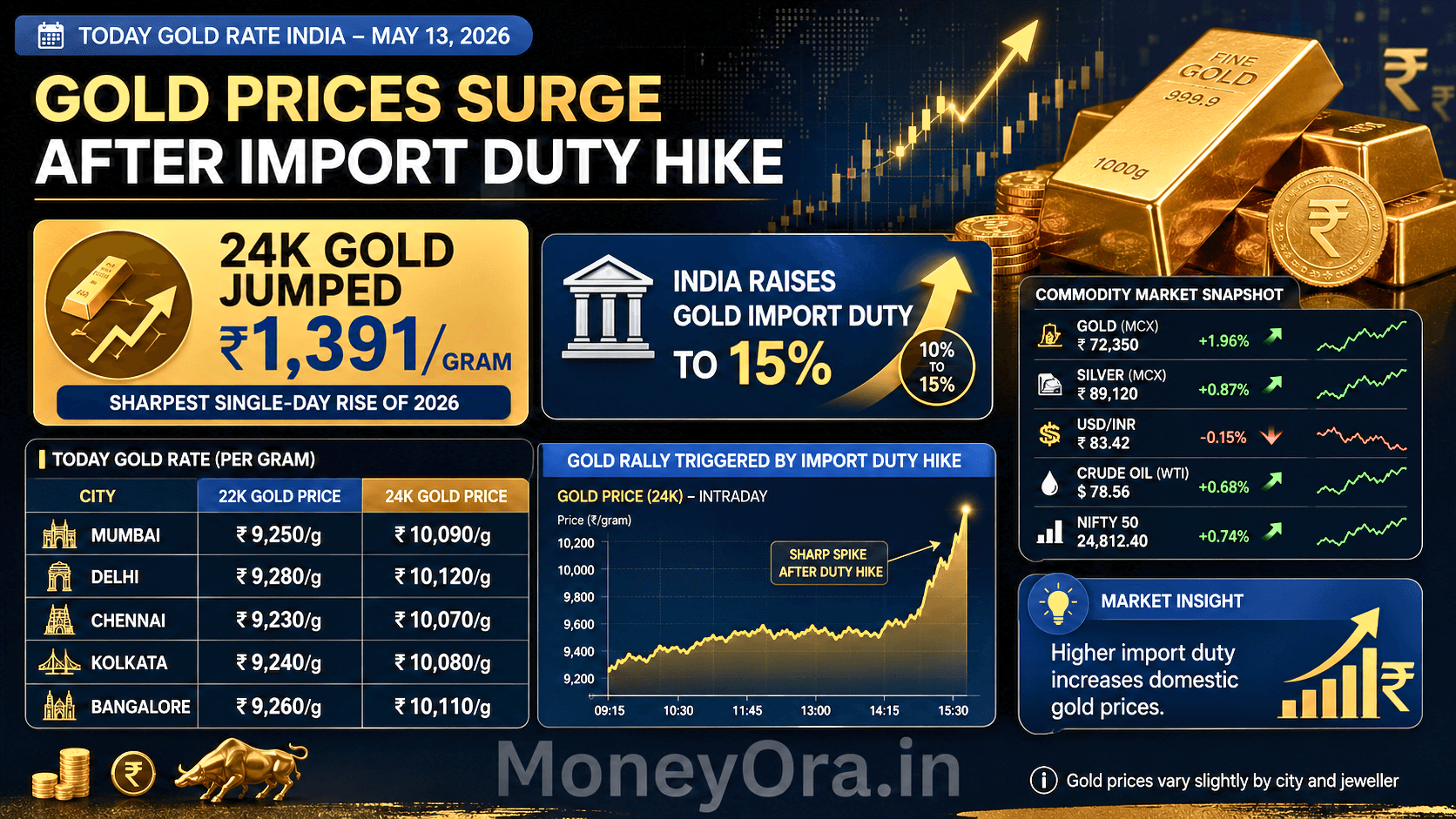

24K gold: ₹16,789/gram (₹1,67,890 per 10g) | 22K gold: ₹15,390/gram (₹1,53,900 per 10g) | 18K gold: ₹12,592/gram

Today’s gold rate in India just made history — in the worst way for buyers. On May 13, 2026, the Indian government quietly released government orders raising the import duty on gold and silver from 6% to 15%. The announcement came through on Wednesday morning, and gold prices jumped by over ₹1,391 per gram within hours. That is one of the steepest single-day spikes in domestic gold prices this year.

If you were planning to buy gold today — for a wedding, for investment, or just to complete a jewellery set — the today gold rate you’re checking is significantly higher than yesterday. And this is not temporary market noise. The duty hike is structural. Unless the government reverses it (which rarely happens quickly), these prices are the new normal for the foreseeable future.

This guide explains today’s live city-wise gold rates, exactly why prices jumped, what the new import duty means for your gold purchase, whether you should buy now or wait, and what smarter alternatives like Sovereign Gold Bonds or gold ETFs look like given today’s numbers. At the bottom, you’ll also find a pro tips section and common mistakes to avoid.

Today gold rate — May 13, 2026 (live city-wise)

Gold prices vary slightly across Indian cities due to local taxes, transportation costs, jeweller margins, and state-level levies. Here are today’s rates for the major cities.

Today gold rate per gram — May 13, 2026

| City | 24K (per gram) | 22K (per gram) | 18K (per gram) |

|---|---|---|---|

| Delhi | ₹16,726 | ₹15,331 | ₹12,545 |

| Mumbai | ₹16,789 | ₹15,390 | ₹12,592 |

| Chennai | ₹16,800 | ₹15,400 | ₹12,860 |

| Kolkata | ₹16,789 | ₹15,390 | ₹12,592 |

| Bengaluru | ₹16,800 | ₹15,395 | ₹12,600 |

| Hyderabad | ₹16,789 | ₹15,390 | ₹12,592 |

| Ahmedabad | ₹16,800 | ₹15,395 | ₹12,595 |

| Jaipur | ₹16,726 | ₹15,331 | ₹12,545 |

| Lucknow | ₹16,726 | ₹15,331 | ₹12,545 |

| Pune | ₹16,789 | ₹15,390 | ₹12,592 |

*Rates are indicative as of morning May 13, 2026 and exclude GST, making charges, and hallmarking premium. Source: GoodReturns, BusinessToday, Latestly. Verify with your local jeweller before purchasing.

Today gold rate per 10 grams — May 13, 2026

| Purity | Yesterday (May 12) | Today (May 13) | Change |

|---|---|---|---|

| 24K (10 grams) | ₹1,53,980 | ₹1,67,890 | +₹13,910 |

| 22K (10 grams) | ₹1,41,150 | ₹1,53,900 | +₹12,750 |

| 18K (10 grams) | ₹1,15,490 | ₹1,25,920 | +₹10,430 |

| Silver (per kg) | ₹2,90,000 | ₹3,10,000 | +₹20,000 |

That ₹13,910 jump on 10 grams in a single day is extraordinary. To put it in perspective — a typical year of gold price appreciation might bring ₹15,000–20,000 gain on 10 grams. This import duty shock delivered nearly a full year’s price appreciation in a few hours.

Why gold price jumped ₹1,391 today — import duty explained

This is the question everyone is asking right now. The short answer: the government more than doubled the gold import duty overnight.

On Wednesday, May 13, 2026, the Central Government issued formal orders raising the import duty on gold and silver from 6% to 15%. The announcement followed Prime Minister Narendra Modi’s public appeal on Sunday urging Indians to avoid buying gold for a year — a rare statement that telegraphed what was coming. When the duty hike was officially confirmed Wednesday morning, bullion prices surged immediately.

Here’s the chain of events:

- India imports nearly all its gold from international markets — it produces almost none domestically

- Gold imports are a major contributor to India’s trade deficit, second only to crude oil in foreign currency spending

- The rupee has weakened to around ₹95.67 per USD — described by Reuters as one of Asia’s worst-performing currencies in 2026

- The West Asia conflict (Israel–Iran tensions) is creating oil price shocks, worsening India’s current account further

- The government needed a lever to reduce forex outflows fast — gold import duty was the lever it reached for

The logic: higher duty → gold becomes more expensive in India → demand drops → fewer imports → less forex outflow → rupee gets some relief. Whether it actually works depends on whether smuggling networks reactivate — and industry insiders are already warning that they will.

“Grey markets are likely to become active, as the incentives to bring in gold illegally are high. At current price levels, smugglers could make significant profits,” a Mumbai bullion dealer told BusinessToday.

It is a familiar cycle. India cut gold duties sharply in the Union Budget 2024, which successfully formalised trade and suppressed smuggling. Wednesday’s reversal risks undoing that progress entirely.

How Much Home Loan Can I Get on My Salary? (2026 Eligibility Guide)

New gold import duty structure — 15% breakdown

The 15% is not a single tax. It’s a combination of two components — both of which are back in place as of today.

| Component | Rate | Note |

|---|---|---|

| Basic Customs Duty (BCD) | 10% | Standard import tariff on gold |

| Agriculture Infrastructure and Development Cess (AIDC) | 5% | Reinstated — was specifically removed in Budget 2024 |

| Total Import Duty | 15% | Up from 6% (effective May 13, 2026) |

| GST on consumer purchase | 3% | Paid by buyer at jewellery counter |

| IGST on imports | 3% | Applied at import stage |

| Effective total tax burden | ~18–21% | Varies by transaction type |

The reintroduction of the AIDC is particularly significant. It was explicitly removed in the Union Budget 2024 to encourage formal gold trading and reduce smuggling. Bringing it back signals the government chose currency defence over trade formalisation — prioritising short-term forex relief over long-term market structure improvements.

For context on how this affects your financial planning: gold purchases become meaningfully less attractive as a savings tool when the embedded tax burden crosses 18%. You’re essentially paying an 18% premium on day one before the metal can appreciate even one rupee. This changes the comparison between physical gold and financial gold instruments like SGBs significantly. More on that in the SGB vs physical gold section.

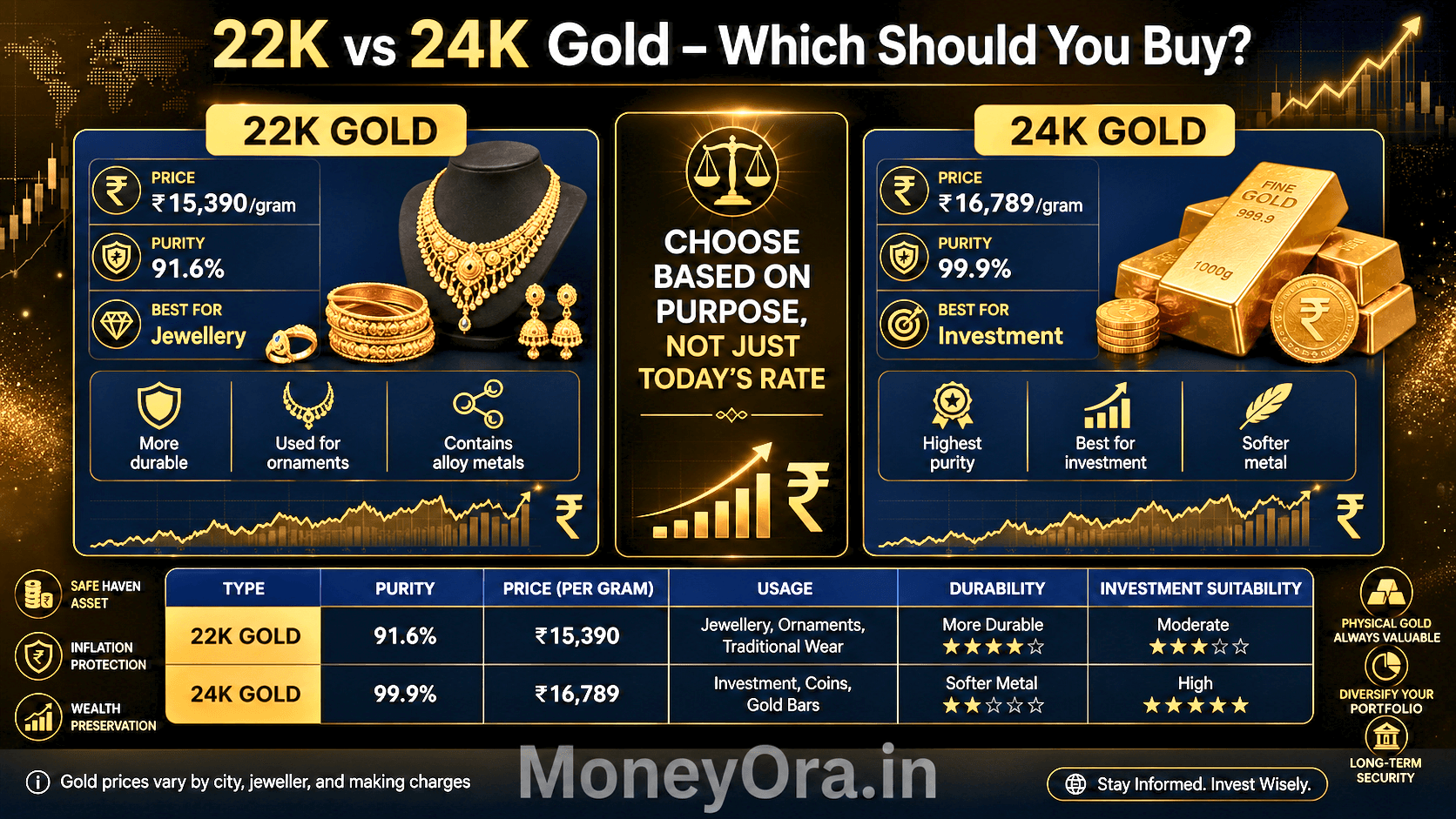

22K vs 24K gold — which to buy and when

Most Indians buying gold for jewellery never think about this — they just ask for the best price. But the difference between 22K and 24K matters both

for purity and for investment value.

| Feature | 22 Karat Gold (916) | 24 Karat Gold (999) |

|---|---|---|

| Purity | 91.6% | 99.9% |

| Hardness | Harder (suitable for jewellery) | Very soft (not suitable for jewellery) |

| Best for | Jewellery, bangles, chains | Coins, bars, ETFs, digital gold |

| Today’s price (per gram) | ₹15,390 | ₹16,789 |

| Price difference (per gram) | ₹1,399 lower than 24K | |

| Investment suitability | Lower (making charges dilute return) | Higher (pure return tracking) |

| Hallmark code | 916 | 999 |

| Widely available in India? | Yes | Yes (coins, digital) |

For jewellery — 22K is the standard in India and will remain so. No jeweller works in 24K because pure gold is too soft to hold design details and stone settings.

For investment — 24K in the form of coins or bars, or better yet, through Gold ETFs or Sovereign Gold Bonds, is the cleaner choice. The problem with buying 24K physical gold coins today is the 3% GST on top of today’s already-elevated price. You’re starting your investment 3% in the hole immediately. Digital gold and gold ETFs avoid this GST disadvantage.

Taxes on buying gold in India in 2026

This is something most buyers discover only at the jeweller’s counter — and by then it’s too late to factor into the budget. Here’s every tax and charge you pay when buying gold jewellery in India today.

At the jeweller (what you pay directly)

- Gold price: Based on today’s market rate (already includes the 15% import duty embedded in the supply chain price)

- Making charges: 8–25% of gold value, depending on design complexity. Plain bangles: 8–12%. Intricate necklaces: 20–25%.

- 3% GST: Applied on the total of gold value + making charges

- Hallmarking premium: Minor (₹35–50 per article), mandatory for BIS hallmarked jewellery

- TCS (1%): Tax Collected at Source applies on purchases above ₹2 lakh in cash or above ₹2 lakh via cheque/UPI at certain jewellers

Quick example — buying a 20-gram necklace today

- Gold value: 20g × ₹15,390 = ₹3,07,800

- Making charges (15%): ₹46,170

- Subtotal: ₹3,53,970

- GST (3%): ₹10,619

- Final bill: ₹3,64,589

The import duty isn’t visible on your bill — it’s already baked into the ₹15,390/gram price the jeweller uses. But it’s real. On those 20 grams, approximately ₹43,200 of what you’re paying is pure import duty cost that wouldn’t have existed before the July 2024 duty cut.

If you’re planning to buy gold as a financial investment rather than jewellery, it’s worth running the numbers through the CAGR calculator to understand what annual return gold needs to deliver just to recover your purchase costs (GST + making charges + effective duty) before you’re in profit.

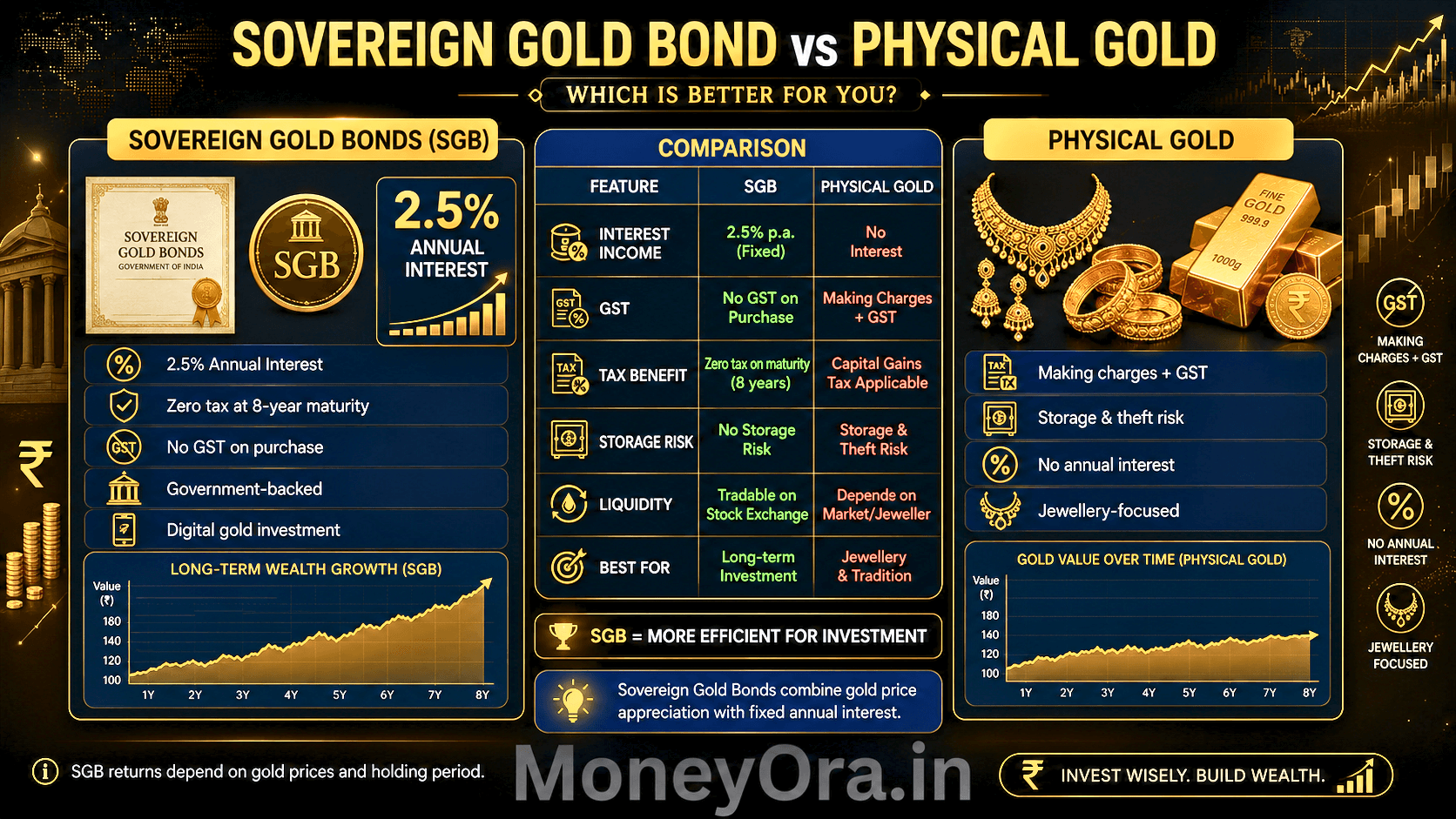

Sovereign Gold Bond vs physical gold — which is smarter?

With today gold rate at ₹16,789/gram, this question deserves a serious answer — especially for people thinking about gold as a long-term investment rather than as jewellery.

| Feature | Physical Gold (coins/bars) | Sovereign Gold Bond (SGB) | Gold ETF |

|---|---|---|---|

| Based on today’s gold price? | Yes | Yes (issue price linked to market) | Yes (real-time) |

| GST at purchase | 3% | None | None |

| Making charges | 0% (coins) to 25% (jewellery) | None | None |

| Interest earned | None | 2.5% per year (paid semi-annually) | None |

| Capital gains tax at maturity | LTCG 20% with indexation (after 3 years) | Fully tax-free at 8-year maturity | LTCG 20% with indexation |

| Storage risk | Theft, locker costs | None — government security | None |

| Liquidity | Good (jewellers, gold loan) | Limited before maturity (can sell on exchange) | Very high (stock exchange) |

| Backed by government? | No | Yes — RBI-issued, GOI-guaranteed | No (AMC-managed) |

| Import duty impact | Full 15% embedded in price | Embedded in issue price but recovered through gold return | Embedded in NAV |

For investment purposes, SGBs issued by the Reserve Bank of India are almost always superior to physical gold coins or bars. You get the same gold price exposure, earn 2.5% annual interest on top, and pay zero tax on capital gains if you hold for 8 years. The only downside is liquidity — you can sell on the exchange but secondary market prices can vary.

Physical gold makes sense when you need the metal itself — for jewellery, for gifting, or for situations where digital instruments aren’t practical. For everything else, the financial instruments win on net return after tax.

For long-term wealth planning alongside gold investment, the SIP calculator and lumpsum calculator on MoneyOra help model how equity mutual funds compare to gold over 10–20 year horizons.

Gold ETF and digital gold — how they work

Gold ETFs (Exchange Traded Funds) are mutual fund units backed by physical gold stored in bank vaults. One unit of a Gold ETF = approximately 1 gram of gold at 24K purity. They trade on NSE and BSE like any other stock — you can buy and sell during market hours at real-time prices.

Why Gold ETF can be smarter than physical gold today

- No GST at purchase (unlike physical gold coins or jewellery)

- No storage risk — gold is held by the custodian bank

- Highly liquid — sell in seconds on the exchange at real-time price

- Can buy very small amounts (even 0.01 unit = less than ₹168 today)

- No purity concern — standardised 24K quality

Digital gold

Platforms like Google Pay, PhonePe, Paytm, and MMTC-PAMP allow buying digital gold starting from ₹1. Digital gold is backed by physical 24K gold stored in secure vaults. You can take physical delivery of accumulated gold when you want. Unlike SGBs, there’s no lock-in. Unlike ETFs, no demat account is required.

The catch with digital gold: GST at 3% still applies at purchase on most platforms, and there are small storage charges. But the flexibility and low minimum investment make it accessible for people who want to accumulate small amounts regularly.

For tracking your gold investment returns over time, the stock return calculator and CAGR calculator on MoneyOra work well for Gold ETF returns just as they do for equity — you just input the entry price, current price, and time period.

Today gold rate vs historical — how far we’ve come

Put today’s rate in perspective. If you bought gold 10 years ago, you’ve done very well. If you’re buying today, the bar is high.

| Year | 24K gold (per 10 grams) | % change from previous |

|---|---|---|

| 2016 | ~₹28,000 | — |

| 2018 | ~₹31,000 | +10.7% |

| 2020 | ~₹50,000 | +61.3% |

| 2022 | ~₹51,000 | +2% |

| 2023 | ~₹60,000 | +17.6% |

| 2024 | ~₹74,000 | +23.3% |

| 2025 | ~₹1,10,000 | +48.6% |

| May 13, 2026 | ₹1,67,890 | +52.6% |

Gold has compounded at roughly 15–16% annually in rupee terms over the past decade. That is a strong return — better than FDs, roughly comparable to equity indexes in some years. But that return includes the tailwind of a weakening rupee. In dollar terms, the gold return has been more modest.

The important thing to know: buying gold after a sharp duty-shock rally (like today) means you’re not starting at a neutral base. You’re starting ₹13,910 per 10 grams higher than yesterday. For long-term investors, that ₹13,910 premium will eventually be absorbed — but it’s still 8.3% of yesterday’s price paid in one day for no fundamental change in gold’s underlying value.

According to Wikipedia’s article on gold as an investment, gold has served as a store of value for thousands of years and continues to serve as a hedge against inflation and currency debasement — exactly the conditions India is experiencing in 2026.

Jewellery stocks impact — Titan, Kalyan, Senco in focus

When gold import duty jumps 9 percentage points overnight, jewellery company stocks feel it immediately — but in two opposite directions, which is worth understanding.

Short-term negative — volume impact

Higher gold prices suppress consumer demand, particularly in the mass market and tier-2/tier-3 cities. Titan Company, Kalyan Jewellers, and Senco Gold all depend on volume sales. A sharp price spike typically causes buyers to postpone purchases — especially for discretionary jewellery. These stocks were flagged in focus lists by multiple brokerages on May 13, 2026.

Longer-term complex — inventory gains possible

Companies that held existing gold inventory (purchased at ₹15,400/gram yesterday) are now sitting on inventory marked at ₹16,789/gram today. That’s a short-term inventory gain. But it comes with the risk that consumers resist prices and demand drops sharply.

For investors who hold or are considering these jewellery stocks, the PE ratio calculator and dividend yield calculator on MoneyOra help evaluate whether the current stock price fairly reflects the changed business environment after today’s duty hike. The stop loss calculator and position size calculator are useful for traders sizing positions in these volatile stocks after a policy shock.

Common mistakes when buying gold in India

After a day like today — with prices jumping ₹1,391/gram — panic and confusion run high. These are the mistakes that cost buyers real money.

1. Buying in a panic immediately after a price spike

The instinct after a sharp price jump is to buy quickly before it goes higher. That fear-of-missing-out buying amplifies the initial shock. Duty-shock rallies often see some stabilisation in the days following as initial panic subsides. Unless you have an immediate need (a wedding in two days), waiting 1–2 weeks to see how prices settle is usually sensible.

2. Comparing prices without checking GST inclusion

Some jewellers quote rates excluding GST; others include it. A ₹15,390 quote excluding GST becomes ₹15,852 with GST at 3%. Always ask explicitly: “Is this price inclusive of GST?” before comparing quotes across jewellers.

3. Ignoring hallmarking

The BIS hallmark on Indian gold jewellery guarantees purity. After the import duty hike, the incentive to sell lower-purity gold as 22K or 24K increases significantly. Always insist on BIS-hallmarked jewellery (the six-digit HUID number) and verify it on the BIS Care app if possible.

4. Choosing physical gold for investment when SGBs exist

Physical gold at today’s prices comes with 3% GST, making charges (if jewellery), storage risk, and capital gains tax on resale. SGBs have none of these — plus they earn 2.5% annual interest and are tax-free at maturity. For any investment purpose, SGBs are almost always the better choice unless you need physical possession.

5. Not considering the gold loan as an alternative

If you need cash urgently and own gold, a gold loan is often faster and cheaper than selling gold and re-buying. Gold loan interest rates are typically 9–14% per annum — lower than personal loan rates. The personal loan EMI calculator helps you compare the cost of a gold-secured loan against an unsecured personal loan.

6. Not tracking purchase price for capital gains purposes

When you eventually sell gold, capital gains tax applies. If you buy today at ₹16,789/gram, keep documentation of the purchase price, date, and weight. This is your cost basis for future capital gains calculation. Losing this paperwork causes complications at resale time.

Pro tips before you buy gold today

- Wait 5–7 working days if your purchase is non-urgent. Policy shock rallies like today’s often see partial pullback as trade adjusts. The initial 8–9% jump may normalise by 2–3% over the following week.

- Check the MCX gold futures price before visiting any jeweller. MCX futures give you a real-time benchmark. If a jeweller’s quoted rate is more than 0.5–1% above MCX spot, negotiate or look elsewhere. The margin calculator and brokerage calculator are useful if you’re trading gold futures on MCX.

- For weddings, consider silver as a partial substitute. Silver import duty also jumped to 15% today, but silver at ₹3,10,000/kg is still massively cheaper than gold gram-for-gram. Some wedding traditions are flexible on the metal.

- If investing ₹50,000+, seriously evaluate SGBs. The next SGB tranche opening date will be announced by the RBI. At today’s gold price, ₹50,000 buys about 2.98 grams of physical 24K gold (after GST). In an SGB, the same ₹50,000 buys the same gold exposure, plus earns 2.5% annual interest, plus is fully tax-free at maturity. The financial math strongly favours SGB for any investment horizon above 5 years.

- Consider diversifying beyond gold. Gold is a good hedge but not a primary wealth builder. The SIP calculator shows how even ₹5,000/month in a diversified equity fund can produce significantly larger returns than gold over 15–20 years. Balance is important.

- Use the CAGR calculator to set return expectations. At ₹1,67,890 per 10 grams today, gold needs to reach ₹2,14,000 per 10 grams just for you to earn a 27% return (covering GST + notional opportunity cost). Use the CAGR calculator to know what annual return you need gold to deliver to break even on today’s elevated price.

- For retirement savers: gold as 5–10% of your portfolio is reasonable for inflation protection. Running the EPF calculator, PPF calculator, and NPS calculator helps you see your total retirement corpus across guaranteed instruments alongside a modest gold allocation.

How gold planning fits your complete financial picture

Gold is one asset class. A sound financial plan uses multiple. If today’s elevated gold rate makes you hesitate, it’s worth checking how your other savings are growing.

For fixed-income savings, the FD calculator and RD calculator show what bank deposits earn at current rates. The PPF calculator models government-backed 7.1% tax-free returns. These are lower-risk options for the conservative portion of a portfolio.

For equity-linked wealth building, the SIP calculator and lumpsum calculator model mutual fund growth. The SWP calculator helps plan income from an accumulated corpus in retirement — a phase where gold’s fixed supply could be converted to liquid instruments.

If you’re carrying loans, the home loan EMI calculator and car loan EMI calculator help ensure your EMI commitments don’t crowd out investment capacity. High-interest consumer debt should generally be cleared before allocating money to gold at today’s prices.

For stock traders and investors: the stock average calculator, option price calculator, and PE ratio calculator complete the analytical toolkit for evaluating gold-related stocks like Titan, Kalyan Jewellers, or MCX.

For banking needs — whether verifying an account before a gold loan transfer or setting up SGB redemption — MoneyOra’s IFSC code finder and bank details finder are quick utility tools.

Conclusion

Today’s gold rate story is not normal market movement. It’s a policy shock — the government doubling import duty to protect the rupee and current account, with gold buyers bearing the cost immediately. A ₹13,910 jump on 10 grams in one day is extraordinary, and it will reshape buying behaviour in the jewellery market for months.

The smartest move right now depends on your situation. If you need gold for a wedding or ceremony within days, buy it — the pain is real but so is the timeline. If you’re buying for investment, Sovereign Gold Bonds remain significantly more efficient than physical gold even at today’s elevated prices. If you’re a long-term wealth builder, remember that gold’s 10-year CAGR in India has been roughly 15% — but that includes a once-in-a-decade rupee collapse and a policy shock like today’s. The next 10 years may not give the same tailwind.

Use MoneyOra’s free calculators to put these numbers in context for your own situation. The CAGR calculator shows what annual return gold needs to deliver from today’s price to beat alternatives. The SIP calculator shows what a regular monthly investment in mutual funds could build over 10–20 years. And the lumpsum calculator shows what the same rupee amount you’re considering for gold would grow to in a diversified fund over the same horizon.

Know the numbers before you decide. Calculate free at MoneyOra — no login needed.

Check your gold investment returns with the CAGR calculator →

Pingback: Sensex Jumps 2,300 Points: 5 Best Stocks After Ceasefire

Pingback: Netweb Technologies Share Price Target 2026: Next AI Multibagger Stock? - MoneyOra

Pingback: AI Stocks Picks 2026: Next 5 Best Multibagger AI Stocks

Pingback: Share Market Today: Will Nifty & Sensex Continue Their Bull Run This Week 26? - MoneyOra

Pingback: Gold Reserve in India Hits 880 Tonnes: Why Is RBI Bringing Gold Back Home - MoneyOra