Recurring Deposit Returns

Calculator

See how your monthly RD deposits grow with quarterly compounding over your chosen investment period.

RD Calculator – Free Recurring Deposit Calculator Online (2025)

MoneyOra’s free RD Calculator tells you exactly how much your recurring deposit will be worth at maturity — the total amount you’ll have invested, the interest earned on top of it, and a full month-by-month or year-by-year breakdown. Enter your monthly deposit, rate of interest, and tenure. Done. “₹100 per day investment challenge: FD vs SIP returns over 30 years”

Recurring deposits sound simple: put in a fixed amount every month, collect the maturity amount at the end. But the actual number you’ll receive depends on the rate your bank offers, the compounding frequency, and how many months you stay invested. Most people guess. This RD Calculator gives you the exact figure before you open the account.

Table of Contents

What Is an RD Calculator?

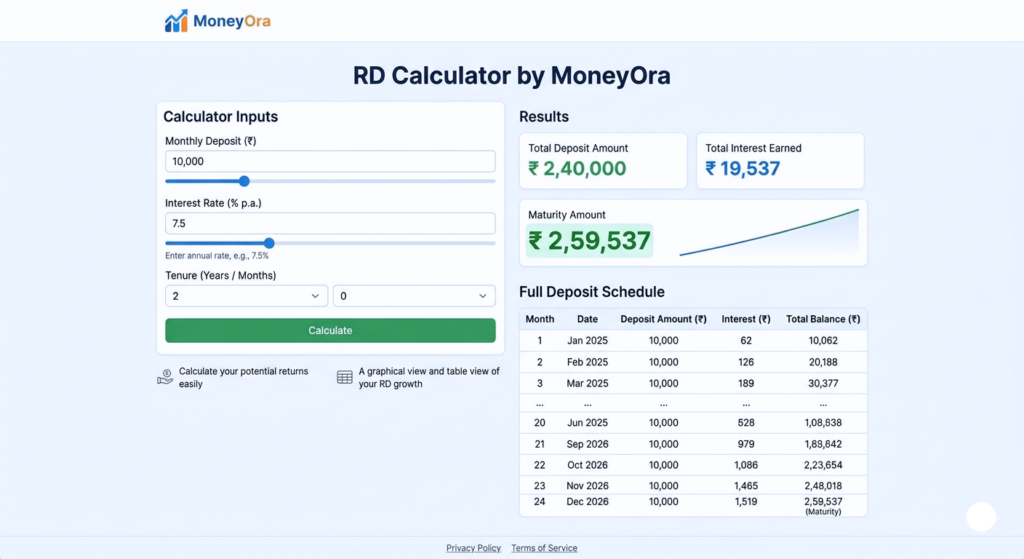

An RD Calculator takes three inputs — your monthly deposit amount, the annual interest rate, and the tenure in months — and calculates the maturity value of your recurring deposit. That’s it.

A recurring deposit is different from a fixed deposit in one key way: instead of investing a lump sum once, you deposit a fixed amount every month for the entire tenure. The interest compounds quarterly, which makes the manual calculation a series of individual calculations — one for each monthly instalment based on how many quarters remain.

Unless you enjoy solving 12 to 120 separate compound interest equations, you use an RD Calculator. MoneyOra’s version gives you the maturity amount, total interest earned, effective yield, and a full year-by-year deposit schedule — all in one place, free, no login needed.

How Does an RD Calculator Help?

The standard RD formula isn’t difficult to understand. Applying it correctly across 12, 24, or 60 months is where most people go wrong. Each monthly instalment earns interest for a different number of quarters, and they all need to be summed up. One wrong input and the whole calculation is off.

Here’s where an online RD Calculator actually saves you time and avoids the errors:

- Instant maturity amount. Enter your monthly deposit, rate, and tenure — the calculator returns the exact maturity value in under a second. No spreadsheet, no formula hunting.

- Compare banks before opening an account. SBI is offering 6.5%. HDFC is at 7.0%. Post Office RD is at 6.7%. Plug each rate into the RD Calculator and you see the actual rupee difference over your chosen tenure — not just a percentage that’s hard to put in context.

- Plan around a savings goal. Need ₹5 lakh in 3 years? Work backwards — use the calculator to find the monthly deposit that gets you there at the rate your bank is currently offering.

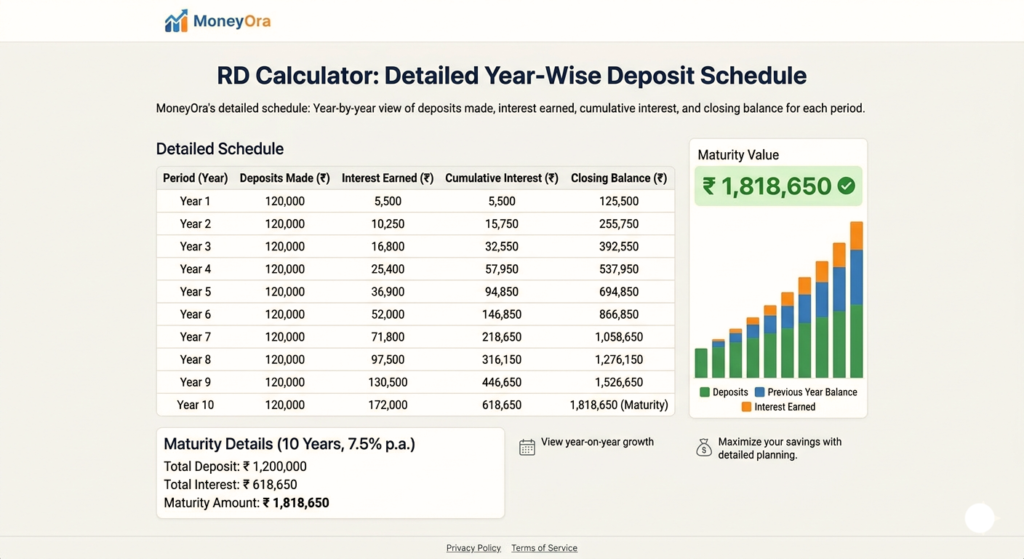

- See the deposit schedule. The year-by-year breakdown in MoneyOra’s RD Calculator shows exactly how much interest accrues each year. For longer tenures, the compounding effect is more pronounced in the later years — seeing that laid out changes how you think about the tenure you choose.

One thing the calculator doesn’t account for: TDS. As per RBI norms, TDS is applicable on RD interest above ₹40,000 per year (₹50,000 for senior citizens). The implementation varies across banks, so the calculator shows gross interest. Keep that in mind when planning around the maturity amount.

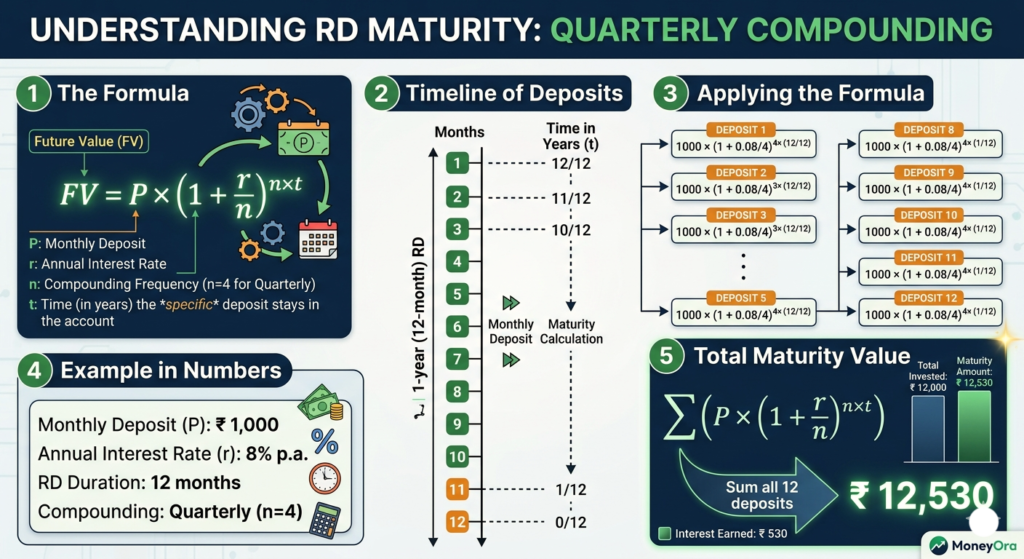

The RD Maturity Formula

Banks use quarterly compounding for RDs. The formula for each monthly instalment is:

A = P × (1 + R/400)4t/12

- A = Maturity value of that instalment

- P = Monthly deposit amount

- R = Annual interest rate (%)

- t = Number of months remaining for that instalment

The total maturity amount is the sum of this calculation for every single monthly instalment — from the first deposit (which compounds for the full tenure) down to the last one (which barely compounds at all).

Worked Example

Monthly deposit: ₹5,000 | Rate: 8% per annum | Tenure: 12 months

The first instalment of ₹5,000 compounds for 12 months (4 quarters):

A1 = 5000 × (1 + 8/400)4 = ₹5,425.44

The second instalment of ₹5,000 compounds for 11 months:

A2 = 5000 × (1 + 8/400)3.67 = ₹5,388.64

… and so on down to the last instalment, which barely earns anything.

Sum of all 12 calculations: Total maturity value = ₹62,730.85

Total deposited: ₹60,000. Interest earned: ₹2,730.85. Not enormous for a 1-year RD, but the compounding effect compounds (pun intended) significantly over longer tenures. Try a 5-year RD in the calculator to see the difference.

How to Use MoneyOra’s Free RD Calculator

Three inputs. That’s all it takes.

- Monthly deposit amount: Enter how much you plan to deposit each month — from ₹500 to ₹10 lakh. Use the slider or type the amount directly.

- Rate of interest: Enter the annual rate your bank is offering. Check the bank’s website or your RD offer letter for the exact rate. Post Office RD rates are updated quarterly by the government.

- Tenure in months: Enter the duration of your RD in months (6 to 120 months). The year-equivalent label updates automatically — so if you type 36, it shows “= 3 yrs”.

The RD Calculator updates instantly. You’ll see:

- Total maturity amount

- Total amount invested

- Total interest earned

- Effective yield as a percentage

- A bar chart showing growth year by year

- A full deposit schedule — switch between monthly and yearly view

If you’re also considering a lump sum investment instead of monthly deposits, compare with our FD Calculator to see which gives you better returns for your specific situation.

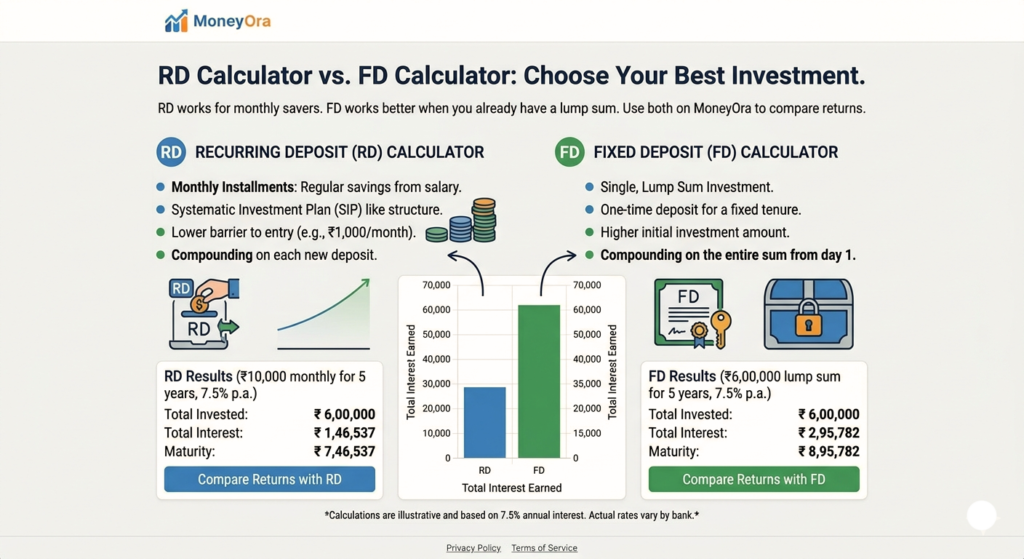

RD vs FD – Which One Makes More Sense?

This comes up a lot. The short answer: it depends on whether you have a lump sum or a monthly surplus.

An RD is for people who want to save a fixed amount every month — it builds the habit, locks the money away, and earns more than a savings account. An FD is for people who already have a lump sum and want to park it safely for a defined period.

| Factor | RD (Recurring Deposit) | FD (Fixed Deposit) |

|---|---|---|

| Investment type | Monthly instalments | One-time lump sum |

| Minimum amount | ₹500/month (most banks) | ₹1,000 (most banks) |

| Compounding | Quarterly | Quarterly or monthly |

| Tenure | 6 months to 10 years | 7 days to 10 years |

| Premature withdrawal | Allowed with penalty | Allowed with penalty |

| Interest rates | Slightly lower than FD | Generally higher |

| Best for | Monthly savers, salaried individuals | Lump sum investors |

The interest rate on RDs is typically 0.1%–0.25% lower than FDs from the same bank. That’s not a dealbreaker — the RD’s value isn’t in beating FD returns, it’s in making you save consistently. Use the FD Calculator alongside this one to compare both options for your specific numbers.

Getting More Out of Your RD

A few things worth knowing before you open one:

- Post Office RD often beats bank rates. The India Post Recurring Deposit currently offers 6.7% per annum (compounded quarterly), which is competitive with most major banks. It’s also government-backed. Worth checking the India Post RD page for the current rate before committing to a bank.

- Senior citizens get a rate bump. Most banks add 0.25%–0.50% on top of the standard RD rate for depositors over 60. Use the RD Calculator to see what that extra quarter-percent actually amounts to over 3 or 5 years — it’s more than you’d expect.

- Missed a payment? Don’t panic, but act fast. Missing a monthly RD instalment doesn’t automatically close the account, but banks charge a small penalty — typically ₹1–2 per ₹100 per month. If you miss multiple instalments, the bank can close the account. Set up a standing instruction or auto-debit to avoid this.

- TDS kicks in above ₹40,000 interest per year. The bank deducts TDS at 10% on RD interest once it crosses the threshold. This applies per bank, not per account. If you have multiple RDs at the same bank, total interest across all of them is counted. Submit Form 15G/15H if your income is below the taxable limit to avoid TDS deduction.

- Premature closure comes with a cost. Most banks will close your RD early but pay interest only at the rate applicable for the period the RD was actually held, minus a 0.5%–1% penalty. If you think you might need the money mid-way, either keep some in a liquid fund or check your bank’s premature withdrawal policy before opening.

Planning other investments alongside your RD? Check these calculators on MoneyOra:

- FD Calculator — for lump sum fixed deposit returns

- EMI Calculator — for home, car, and personal loan EMIs

- NPS Calculator — for National Pension Scheme projections

- Home Loan EMI Calculator — for housing loan planning

Before You Open That RD Account

An RD is a good instrument for what it does — building a savings habit with guaranteed returns. It’s not going to make you rich. But if you’re putting money in a savings account because you haven’t gotten around to doing something better with it, an RD at least earns you 6.5%–7% instead of 3%.

Use the RD Calculator above to try different monthly amounts and tenures. See how much the maturity amount changes when you go from 2 years to 3 years. Then check what the same money earns in an FD using the FD Calculator — and pick the one that fits how you actually want to invest.

More calculators on MoneyOra:

FAQs

Yes. Since June 2015, TDS applies to all recurring deposit interest in India.

The bank deducts TDS at 10% once your total RD interest from that bank crosses ₹40,000 in a financial year (₹50,000 for senior citizens).

If your income is below the taxable limit, submit Form 15G (or 15H for senior citizens) to avoid TDS.

MoneyOra's RD Calculator shows gross interest — TDS is not included.

It varies by institution.

Most banks allow you to start from ₹500 per month.

Post Office RD starts at ₹100 per month.

There is no maximum deposit limit, but the monthly amount must stay fixed.

Use the RD Calculator with ₹500 to see how small savings grow over time.

Yes, premature closure is allowed at most banks.

You will receive interest at the applicable rate for the actual tenure.

Banks also charge a penalty of 0.5%–1%.

For example, a 3-year RD at 7% closed after 18 months may earn around 6%–6.5%.

Always check your bank’s policy before opening an RD.

Most banks offer RD tenures from 6 months to 10 years.

After 6 months, tenure is usually available in multiples of 3 months.

This includes options like 9, 12, 15 months, and more.

MoneyOra's RD Calculator supports tenures from 6 to 120 months.

RD interest is compounded quarterly in India.

Each monthly instalment earns interest for the remaining quarters.

The first instalment earns the most interest.

The last instalment earns the least.

The RD Calculator uses quarterly compounding for accurate results.

For money you don’t need immediately, yes.

Savings accounts offer around 2.5%–4% interest.

RDs offer around 6%–7.5% depending on tenure.

The trade-off is liquidity, as RDs require fixed monthly deposits.

Use the RD Calculator to compare actual returns.

Missing one payment does not close your RD account.

Banks charge a penalty of ₹1–2 per ₹100 per month.

Missing 3–4 payments may result in account closure.

Set up auto-debit to avoid penalties.

If missed, pay dues as soon as possible.

Bank calculators are limited to their own products.

They show returns based only on their rates.

MoneyOra's RD Calculator is rate-agnostic.

It allows comparison across banks like SBI, HDFC, ICICI, Post Office, and NBFCs.

It also provides a detailed yearly schedule with interest breakdown.