EPF, PPF and NPS each serve a different retirement job — understanding the difference is worth lakhs over a career

EPF, PPF and NPS each serve a different retirement job — understanding the difference is worth lakhs over a career

You just started your first job. HR drops three terms on you in the same week — EPF, PPF, NPS. Your first instinct is probably to nod and move on. Most freshers do. That’s actually the first financial mistake.

The EPF vs PPF question isn’t just about which one pays more interest. It’s about understanding that these three instruments do completely different things. Use the wrong one, ignore the right one, or mess up the sequencing — and you could be ₹15–30 lakh short at retirement compared to someone who made the exact same salary as you.

This guide breaks down EPF vs PPF vs NPS specifically for freshers in India in 2026 — with real numbers, tax implications under both regimes, and a clear answer on what to prioritise first. You can also run your own projections using MoneyOra’s EPF Calculator, PPF Calculator, and NPS Calculator.

Key Takeaways

- EPF is not optional if you’re salaried at a 20+ person company — and your employer matches your contribution. That match is free money most freshers don’t appreciate.

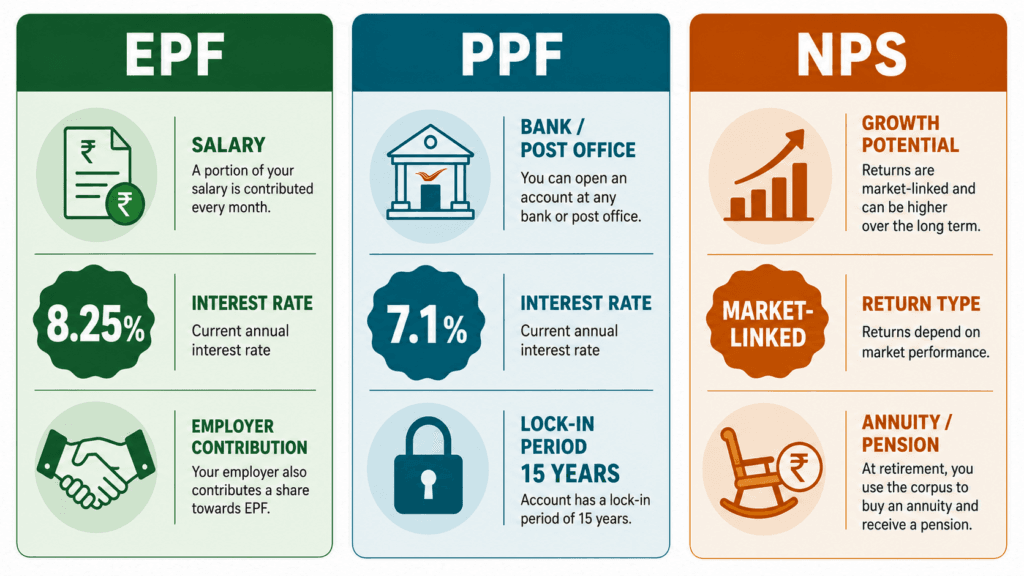

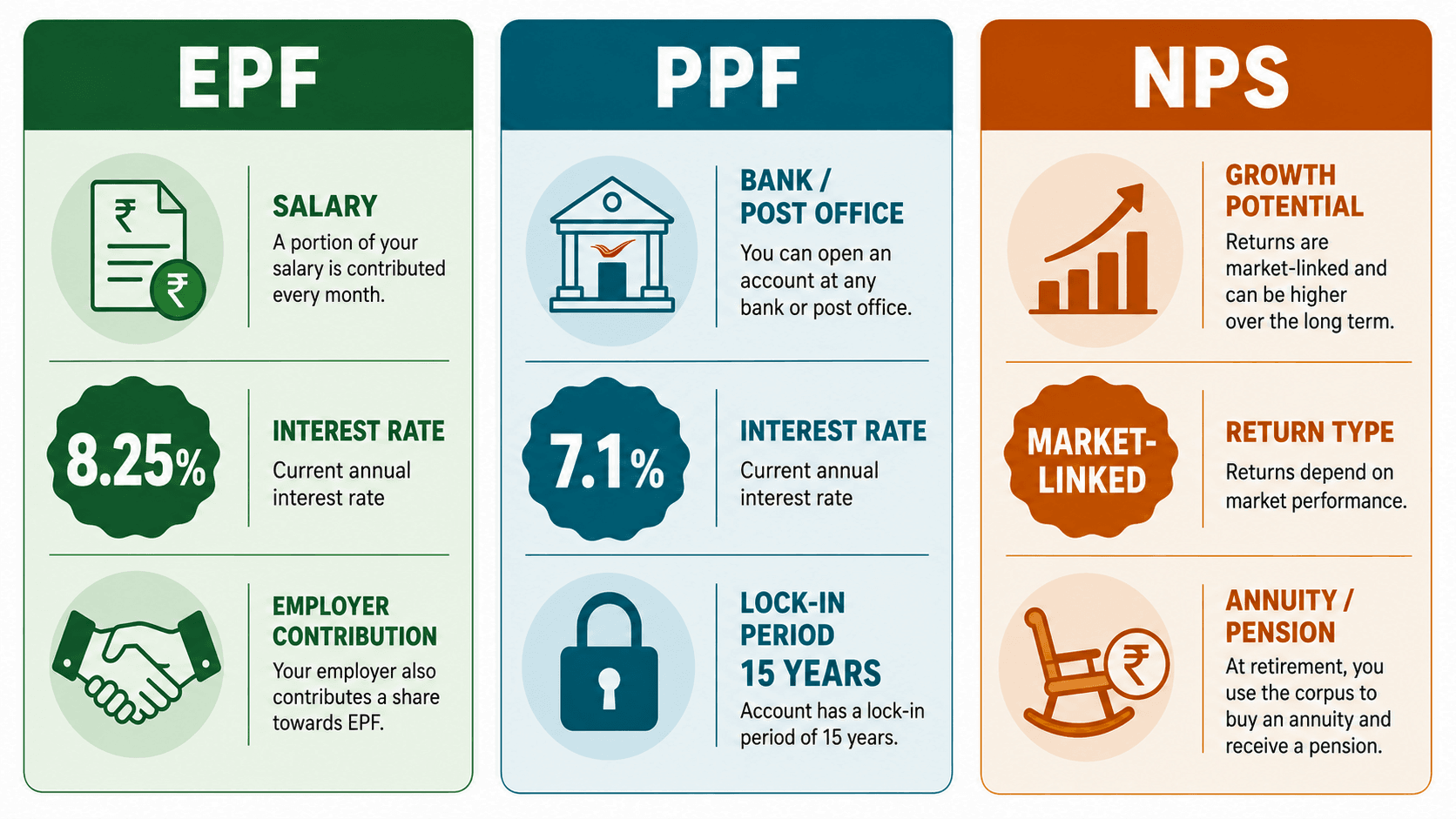

- EPF pays 8.25% tax-free (FY 2024-25 rate, EPFO). PPF pays 7.1% tax-free (Q1 FY 2026-27 rate). NPS returns are market-linked and not guaranteed.

- Under the new tax regime (default from FY 2024-25), the 80C deduction on EPF vs PPF contributions doesn’t apply. But their returns remain tax-free.

- The smartest strategy for most freshers isn’t choosing one — it’s using all three in the right order and proportion.

- Never withdraw EPF when switching jobs. Transferring it preserves compounding that could be worth ₹10–40 lakh over a career.

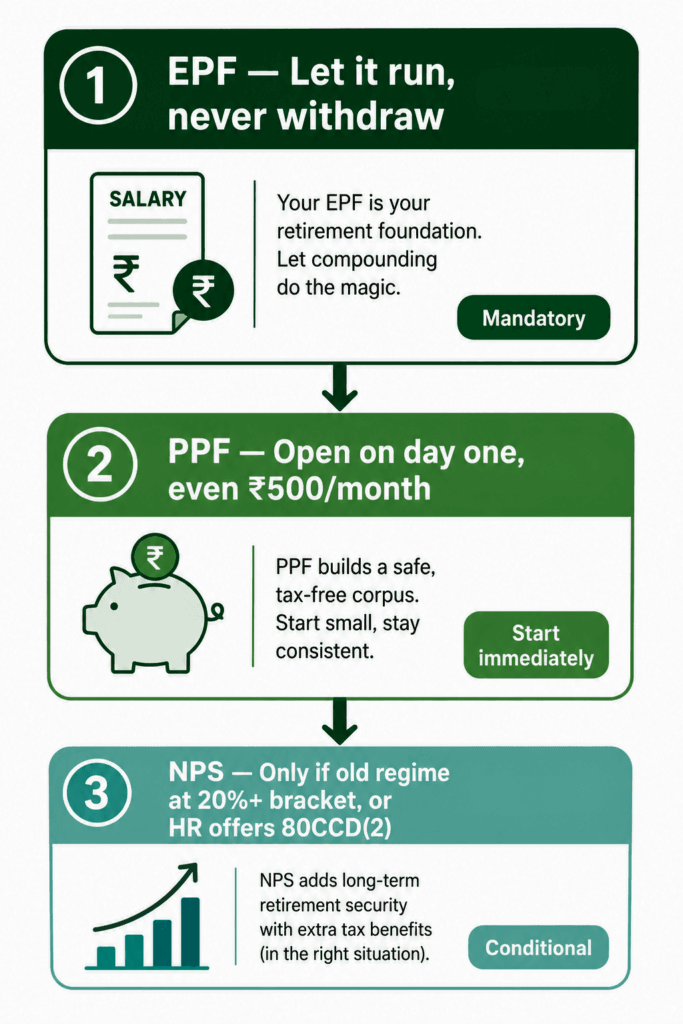

EPF vs PPF vs NPS for Freshers — the Short Answer

Quick answer (40 words): EPF is your automatic base — let it run and never withdraw it. Add PPF if you want a separate stable bucket you control. Add NPS only if you’re in the old tax regime at 20%+ bracket, or your employer routes contributions through 80CCD(2).

That’s the framework. Everything below is the reasoning behind it. financial terms like EEE, 80C, and CAGR The mistake most freshers make is treating EPF, PPF, and NPS as competitors. They’re not. They’re three different tools with three different jobs. Understanding that difference is worth more than the interest rate on any of them.

What Is EPF and How Does It Actually Work?

EPF stands for Employees’ Provident Fund. It’s mandatory for all salaried employees in establishments with 20 or more workers, regulated by the Employees’ Provident Fund Organisation (EPFO).

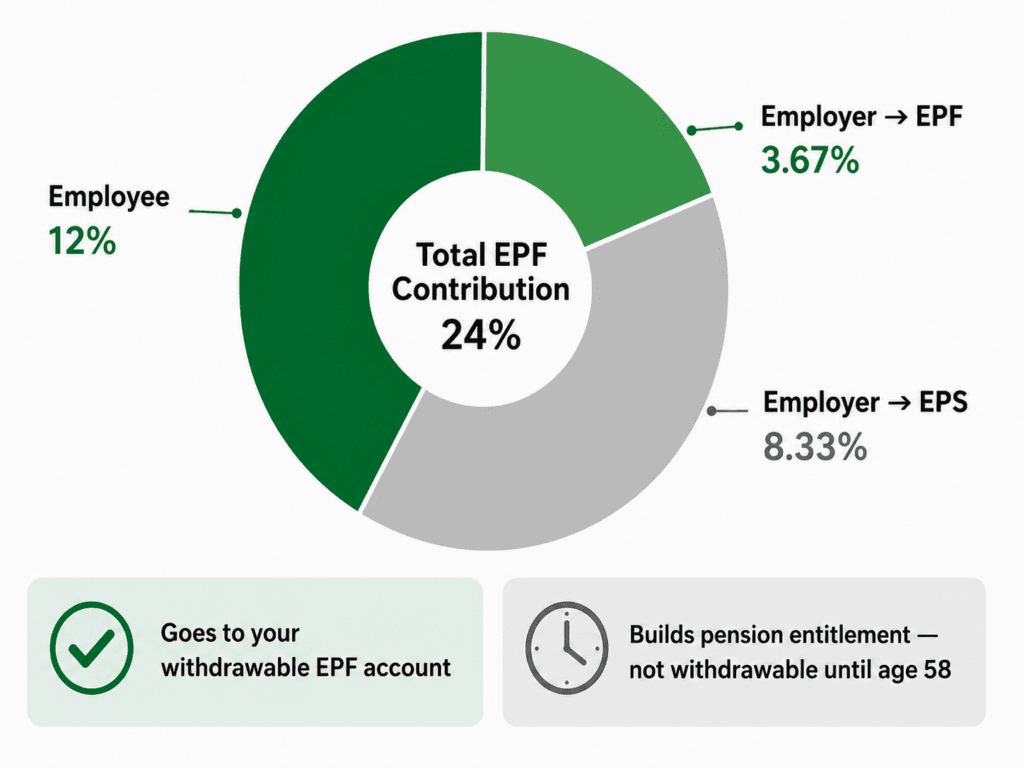

Here’s how the contribution split works — and most freshers get this wrong:

| Who Contributes | % of Basic+DA | Where It Goes |

|---|---|---|

| Employee | 12% | 100% to your EPF account |

| Employer (Part 1) | 3.67% | To your EPF account |

| Employer (Part 2) | 8.33% | To EPS (Pension Scheme) — NOT your EPF balance |

Important: Only 3.67% of the employer’s 12% goes into your EPF balance. The rest builds pension service, not a withdrawable corpus. | ||

This is the part most freshers miss entirely. Your EPF passbook shows a combined 15.67% flowing in each month (12% from you + 3.67% from employer), not 24%. The EPS portion builds your pension entitlement — but that’s accessible only after 10 years of service and from age 58. EPFO 3.0 changes to EPF access for freshers

EPF interest rate and tax treatment in 2026

- Interest rate: 8.25% for FY 2024-25 (declared by EPFO Central Board of Trustees)

- Tax on contributions: Eligible for 80C deduction up to ₹1.5 lakh — but only under the old tax regime

- Tax on interest: Tax-free, as long as your annual EPF contribution stays below ₹2.5 lakh. Above that threshold (introduced in Finance Act 2021), interest on the excess becomes taxable at slab rates

- Tax on withdrawal: Fully tax-free after 5 years of continuous service. Before 5 years — the entire amount (principal + interest) gets taxed, and TDS at 10% is deducted on withdrawals above ₹50,000

Most freshers assume the full employer 12% goes into their EPF balance — only 3.67% does. The rest builds pension service (EPS), not a withdrawable corpus

Most freshers assume the full employer 12% goes into their EPF balance — only 3.67% does. The rest builds pension service (EPS), not a withdrawable corpus

What Is PPF and Who Should Use It?

PPF (Public Provident Fund) is a voluntary, government-backed savings scheme open to all Indian citizens — salaried, self-employed, homemakers, even students. You’re not tied to any employer. You control how much you contribute each year, between ₹500 and ₹1.5 lakh.

The current PPF interest rate is 7.1% per annum for Q1 FY 2026-27 (April–June 2026), set quarterly by the Ministry of Finance. It’s been stable at 7.1% since January 2023. The rate is reviewed every quarter — so it can change, though movement has been rare recently.

PPF tax treatment — the genuine EEE status

PPF is one of the very few instruments in India with absolute EEE status:

- Exempt at contribution: Up to ₹1.5 lakh qualifies for 80C deduction (old regime only)

- Exempt on interest: 100% tax-free, no ceiling, no conditions

- Exempt at maturity: The full maturity amount — principal plus 15 years of compounded interest — is tax-free with no documentation

That last point matters more than most people realise. EPF’s tax-free status on withdrawal has conditions (5-year service, ₹2.5L contribution limit on interest). PPF’s maturity is unconditionally tax-free. If your EPF contributions are large, your PPF account actually becomes the cleaner tax shelter.

PPF lock-in, liquidity, and extension

- Lock-in: 15 years from the financial year of account opening

- Partial withdrawal: Available from the 7th financial year — once per year, up to 50% of the balance at the end of the 4th or 5th preceding year (whichever is lower)

- Loans: Available from years 3 to 6, up to 25% of balance — useful in genuine emergencies

- Extension: After 15 years, the account can be extended indefinitely in 5-year blocks, with or without contributions. Without contributions, you can withdraw any amount once a year

Run a projection for your PPF account using MoneyOra’s free PPF Calculator to see what your corpus looks like at 7.1% over 15, 20, or 25 years.

What Is NPS and When Does It Make Sense for Freshers?

NPS (National Pension System) is a market-linked, government-backed retirement scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Unlike EPF vs PPF, it invests across equity, government bonds, and corporate bonds — so returns vary and aren’t guaranteed.

NPS tax benefits — and why the new regime changes the calculus

NPS had three tax levers under the old regime:

- 80C (Employee Tier 1 contribution): Up to ₹1.5 lakh combined with EPF, PPF, ELSS, etc.

- 80CCD(1B): An additional ₹50,000 deduction exclusively for NPS Tier 1 contributions — completely separate from and above the 80C ceiling. At the 30% bracket + 4% cess, that’s ₹15,600 saved annually. No other instrument qualifies for this.

- 80CCD(2): Employer NPS contribution (up to 10% of salary for private employees, 14% for government) — deductible even under the new tax regime.

That third point is crucial for 2026. If you’re on the new tax regime (which is now the default), points 1 and 2 give you nothing. But 80CCD(2) still works. So ask your HR: can some of my CTC be structured as employer NPS contribution? For a fresher at ₹8 LPA, routing even ₹40,000 annually as employer NPS saves roughly ₹8,000–12,000 in tax — legally, cleanly, and without touching your investment choices.

NPS exit rules — where freshers tend to miscalculate

- Funds are locked until age 60 (with exceptions for premature exit after 3 years or specific reasons)

- At maturity: up to 60% can be withdrawn tax-free as lump sum. The remaining 40% must be converted to an annuity — and annuity income is taxable at your slab rate

- Partial withdrawal (up to 25% of own contributions) is allowed after 3 years for specific purposes: children’s education, medical treatment, home purchase, disability

The annuity requirement is where NPS loses some of its shine for long-term tax efficiency. Compare your NPS projected corpus with alternative scenarios using MoneyOra’s NPS Calculator.

EPF vs PPF vs NPS — Full Comparison Table 2026

| Feature | EPF | PPF | NPS |

|---|---|---|---|

| Who can use it? | Salaried (20+ employee firms) | Any Indian citizen | Any citizen aged 18–70 |

| Mandatory? | Yes | Voluntary | Voluntary |

| Interest / Returns | 8.25% (FY24-25, fixed) | 7.1% (Q1 FY26-27, fixed) | Market-linked (varied) |

| Return type | Declared, govt-backed | Declared, sovereign guaranteed | Market returns, not guaranteed |

| Employer contribution | Yes — 3.67% to EPF | None | Optional (80CCD(2)) |

| Min annual contribution | 12% of basic salary | ₹500 | ₹1,000 (Tier 1) |

| Max annual contribution | 100% of basic salary (VPF) | ₹1.5 lakh | No upper limit |

| Lock-in | Until retirement (58) | 15 years | Until age 60 |

| Tax on contributions (old regime) | 80C (up to ₹1.5L) | 80C (up to ₹1.5L) | 80C + additional ₹50K (80CCD1B) |

| Tax on contributions (new regime) | No 80C benefit | No 80C benefit | Employer NPS — 80CCD(2) |

| Tax on returns | Tax-free (up to ₹2.5L/yr contribution) | 100% tax-free — no ceiling | Tax-deferred (taxed at exit) |

| Tax at withdrawal | Tax-free after 5 years service | 100% tax-free at maturity | 60% tax-free; 40% annuity (taxable) |

| Liquidity | Partial withdrawal (conditions) | Partial from year 7 | 25% after 3 yrs (specific reasons) |

| Best for | All salaried freshers — mandatory base | Extra stable, tax-free bucket | Old regime users; employer NPS structuring |

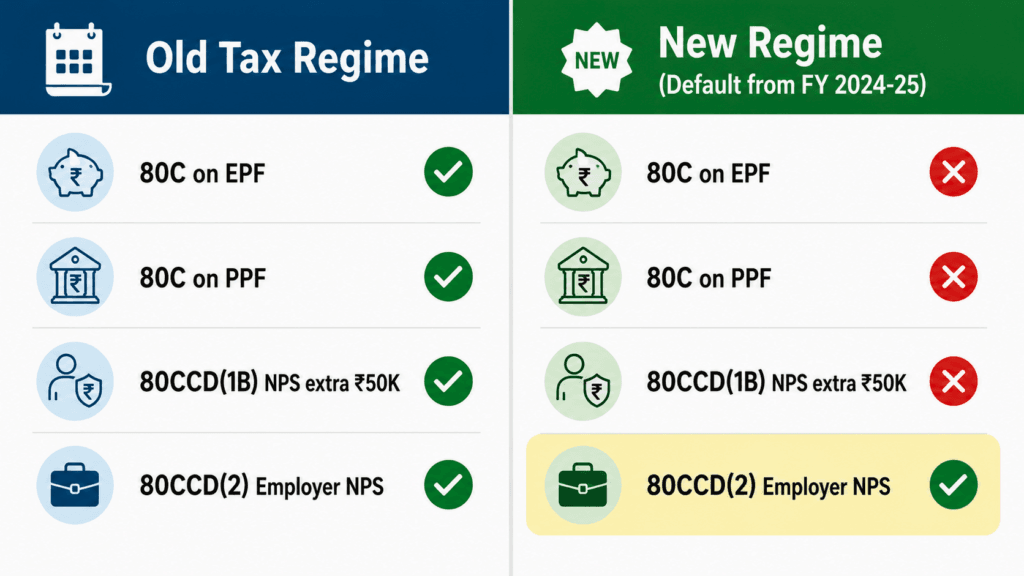

The new tax regime (default since FY 2024-25) removes 80C and 80CCD(1B) benefits — but employer NPS under 80CCD(2) still works

The new tax regime (default since FY 2024-25) removes 80C and 80CCD(1B) benefits — but employer NPS under 80CCD(2) still works

The new tax regime (default since FY 2024-25) removes 80C and 80CCD(1B) benefits — but employer NPS under 80CCD(2) still works

The Tax Angle — What Changes Under the New Regime in 2026

This is the part most EPF vs PPF articles get wrong, and it’s where freshers make the most costly decisions.

Since FY 2024-25, the new tax regime is the default for all salaried employees (as per the Income Tax Department). If you haven’t explicitly opted out, you’re on the new regime. And under the new regime:

- The 80C deduction doesn’t apply — meaning your EPF vs PPF contributions don’t reduce your taxable income

- The ₹50,000 extra deduction under 80CCD(1B) for NPS Tier 1 also doesn’t apply

- The only retirement contribution that still gets deducted is employer NPS under 80CCD(2)

- However — and this is critical — EPF vs PPF returns and maturity amounts remain tax-free regardless of which regime you’re on

| Tax Benefit | Old Regime | New Regime (default) |

|---|---|---|

| 80C on EPF contribution | Up to ₹1.5L | Not available |

| 80C on PPF contribution | Up to ₹1.5L (shared with EPF) | Not available |

| 80CCD(1B) — extra NPS deduction | Additional ₹50,000 | Not available |

| 80CCD(2) — employer NPS contribution | Up to 10% of salary | Up to 10% of salary (still works!) |

| EPF interest (if ≤ ₹2.5L/yr contributed) | Tax-free | Tax-free |

| PPF interest and maturity | 100% tax-free | 100% tax-free |

| Note for FY 2026-27: Under the new Income Tax Act 2025, Section 80C becomes Section 123 read with Schedule XV from tax year 2026-27. The ₹1.5L limit and EEE status for PPF remain unchanged. Only the section reference changes. |

The practical implication for a fresher on the new regime: you should still contribute to EPF (mandatory), still consider PPF (tax-free growth even without the deduction), and specifically ask HR about employer NPS under 80CCD(2) — that’s the one tax lever that’s still live under the default regime.

Real Corpus Calculations — What ₹5,000/Month Builds in Each

Assume a fresher invests ₹5,000/month (₹60,000/year) in each instrument for 30 years. These are projections, not guarantees — particularly for NPS, which is market-linked.

| Instrument | Rate Used | Total Invested | Projected Corpus | Tax at Exit |

|---|---|---|---|---|

| EPF (employee share only) | 8.25% | ₹18 lakh | ~₹73 lakh | Zero (after 5 yrs service) |

| PPF (₹5,000/month = ₹60K/year) | 7.1% | ₹18 lakh | ~₹55 lakh | Zero (EEE) |

| NPS Tier 1 (conservative, 60% debt / 40% equity) | 9–10% assumed CAGR* | ₹18 lakh | ~₹90–1.02 lakh | 40% must buy annuity (taxable) |

| EPF with employer match (3.67% extra) | 8.25% | ₹18 lakh (you) + employer | ~₹87–95 lakh | Zero |

For most Indian freshers, the right sequence is EPF first (mandatory), PPF second (open on day one), and NPS third (only if the tax situation justifies it)

*NPS Tier 1 historical returns have varied. SBI NPS equity fund has delivered approximately 13–14% CAGR since inception; balanced/moderate allocation estimates 9–10% for long-term projections. Past performance does not guarantee future results. These are illustrative, not investment promises.

The employer match on EPF is what makes it the strongest single instrument for most salaried freshers. You put in 12% — and 3.67% more comes in from your employer at zero additional cost to you. No other retirement instrument in India has this feature.

Use MoneyOra’s EPF Calculator to model your own corpus with your actual basic salary and years to retirement. For SIP-style projections, the SIP Calculator can help you model EPF equivalent contributions.

The Employer Match No Fresher Should Ignore

Here’s something most EPF vs PPF comparison articles skip entirely: the employer EPF contribution is, functionally, a 30% boost on every rupee you put in.

If your basic salary is ₹25,000/month:

- Your EPF contribution: ₹3,000/month (12%)

- Employer contribution to EPF: ₹917.5/month (3.67%)

- Your effective starting EPF balance per month: ₹3,917.5 — from a ₹3,000 investment

- That’s a ~30.6% immediate return before interest is even calculated

No PPF, no NPS, no FD, no equity fund gives you this. The employer match is EPF’s single most valuable feature — and the reason why, for salaried freshers, EPF isn’t just “a forced deduction.” It’s the most efficient savings instrument you’ll ever have access to.

Mistakes Freshers Make with EPF vs PPF vs NPS

Mistake 1: Withdrawing EPF at every job change

This is the single most expensive retirement mistake a salaried Indian can make. Every withdrawal before 5 years resets your service continuity, makes the full amount taxable, and destroys compounding that’s nearly impossible to replace. Always transfer, never withdraw.

Mistake 2: Treating the 80C pool as three separate limits

EPF contribution + PPF contribution + ELSS + LIC premiums — they all share the same ₹1.5 lakh Section 80C ceiling. A fresher with ₹24,000/year in EPF doesn’t need to invest the full ₹1.5L more in PPF to max 80C. They only need ₹1,26,000 more. Many freshers don’t realise this and either double-count or under-invest.

Mistake 3: Opening NPS before understanding the exit rules

NPS locks your money until 60. The 40% mandatory annuity means you can’t access your full corpus even at retirement. Freshers who open NPS for the 80CCD(1B) benefit without reading the exit rules often feel blindsided. Know what you’re signing up for before you contribute.

Mistake 4: Assuming PPF is useless under the new tax regime

PPF’s tax-free returns and maturity aren’t linked to which tax regime you choose. Even on the new regime with zero 80C benefit, a PPF account growing at 7.1% compounded annually — with the entire maturity tax-free — is still one of the cleanest long-term debt instruments in India.

Mistake 5: Not checking if employer NPS is available

80CCD(2) lets your employer contribute to NPS Tier 1 on your behalf — and this deduction works even under the new tax regime. Many HR teams don’t proactively offer this structuring. Ask. For a fresher at ₹8 LPA, this single adjustment can save ₹6,000–12,000 in tax annually.

Mistake 6: Never logging into the EPF passbook

Some employers — particularly smaller companies — delay or default on EPF deposits. You won’t know unless you check. Log in to epfindia.gov.in after your first two salary cycles and verify the balance. Check quarterly after that. It takes five minutes and has saved people from discovering months of missed contributions only when trying to withdraw or transfer.

MoneyOra Analysis — The Smartest Combination Strategy for Freshers in 2026

The EPF vs PPF vs NPS debate creates a false choice. The right question isn’t “which one” — it’s “which one first, and how much to each?”

Here’s what the numbers actually suggest for freshers at different salary levels:

Stage 1 — Fresher (Age 22–28, salary ₹4–10 LPA)

- Let EPF run. Don’t touch it. Don’t withdraw it. Transfer it at every job change. That’s 80% of retirement planning done automatically.

- Open a PPF account in month one. Even ₹500/month to start. The account’s 15-year clock starts ticking immediately — and the earlier it starts, the longer the extension runway after maturity.

- Ask HR about employer NPS structuring (80CCD(2)). If they offer it and you’re on the new regime, this is your most useful active tax move right now.

- NPS Tier 1 through 80CCD(1B)? Only if you’re on the old regime and in the 20–30% bracket. Otherwise, it adds complexity without enough benefit at this salary level.

Stage 2 — Growing Career (Age 28–35, salary ₹10–25 LPA)

- Max PPF at ₹1.5 lakh/year (₹12,500/month). This becomes increasingly valuable as income grows and tax-free maturity amounts get larger.

- Consider VPF if you want more guaranteed-return exposure beyond PPF’s ₹1.5L cap — same 8.25% rate, no new account needed.

- At 30% bracket (old regime): NPS via 80CCD(1B) saves ₹15,600/year in tax — compelling enough to justify the lock-in and annuity constraints.

- Add equity SIPs separately for inflation-beating growth that neither EPF, PPF, nor NPS (in conservative mode) will reliably provide over 20–30 years.

The compounding math over 30 years: A fresher who starts EPF + ₹500/month PPF at 22 and never withdraws EPF will have more retirement wealth by 52 than someone who started the same instruments at 27 but contributed twice as much. Time does more work than amount — especially in guaranteed-return instruments.

What competitors don’t mention: EPF’s employer match effectively gives salaried freshers a 30% immediate return on their mandatory contribution. No PPF or NPS equivalent exists. That alone makes EPF the non-negotiable priority — and the reason why “which one” is the wrong question to start with.

Risks to Keep in Mind

- Interest rate risk (EPF vs PPF): Both rates are declared periodically by the government and can change. EPF has averaged 8–9% over the past decade but is not contractually fixed. PPF has been at 7.1% for several quarters. Neither is guaranteed in perpetuity.

- Market risk (NPS): NPS returns depend on market performance. NPS equity funds have delivered strong historical returns, but past performance doesn’t guarantee the same over your specific investment period.

- Annuity risk (NPS): 40% of your NPS corpus must buy an annuity at exit. Annuity rates at the time of your retirement (30–35 years from now) are unknown. You may get less regular income than current annuity rates suggest.

- Employer insolvency risk (EPF): In theory, EPFO guarantees the principal, but delayed or missed employer contributions can happen. Monitor your passbook regularly.

- Liquidity risk (all three): None of these are liquid. EPF has conditions, PPF locks for 15 years, NPS locks until 60. Never put money you might need in the next 1–3 years into any of these instruments.

- Tax law changes: The new tax regime became default in FY 2024-25. The rules may change again. What’s optimal today may not be optimal in 10 years. Review your regime choice every April with a CA if your income has grown significantly.

Disclaimer: This article is for educational purposes only. Interest rates, tax provisions, and withdrawal rules are subject to change. Equity and market-linked investments carry risk. Verify current provisions at incometax.gov.in and epfindia.gov.in before making decisions. This is not financial advice — consult a SEBI-registered financial advisor for personalised planning.

EPF vs PPF vs NPS — Where to Start Right Now

The EPF vs PPF comparison matters, but the decision paralysis around it costs freshers more than the decision itself. Here’s the action list:

- Activate your UAN — link PAN, Aadhaar, and bank account on the EPFO portal within your first month of employment

- Open a PPF account at your bank or post office — even ₹500 to start; the 15-year clock matters more than the initial amount

- Ask HR about employer NPS under 80CCD(2) — one conversation that could save ₹6,000–15,000 in tax annually

- Check your EPF passbook after the first two salary cycles — verify contributions are being deposited

- Run your numbers — model your EPF corpus, PPF maturity, and NPS projection using MoneyOra’s free calculators before deciding how much to allocate to each

The EPF vs PPF vs NPS comparison isn’t really a competition. Each fills a gap the others can’t. Get EPF right first (it’s mandatory anyway), add PPF as a parallel stable bucket, and evaluate NPS based on your tax regime and salary level. That order is right for most freshers in India in 2026.

Calculate Your EPF, PPF & NPS Corpus Free

SIP • EPF • PPF • NPS • FD • CAGR — all calculators free, no login required.

Use the free calculator now on MoneyOra.in →MoneyOra Calculators

- EPF Calculator — Model your PF corpus with your actual basic salary and retirement age

- PPF Calculator — Project PPF maturity at 7.1% across 15, 20, or 25 years

- NPS Calculator — Estimate retirement corpus and monthly pension from NPS Tier 1

- SIP Calculator — Plan your SIP alongside EPF/PPF for inflation-beating equity exposure

- FD Calculator — Compare FD returns vs EPF/PPF after-tax

- Lumpsum Calculator — See what a one-time investment grows to over 15–30 years

- CAGR Calculator — Measure real annual growth rate of any investment

- SWP Calculator — Plan retirement income from your accumulated corpus

Frequently Asked Questions — EPF vs PPF vs NPS

Which is better for freshers — EPF vs PPF?

For a salaried fresher, EPF is the higher priority because it’s mandatory, carries employer contributions (an immediate ~30% boost on your money), and pays 8.25% tax-free. PPF is the better choice for voluntary, additional long-term savings because it’s self-controlled, has no employer-link risk, and provides truly unconditional EEE status with a 15-year compounding runway. Most freshers should prioritise both — EPF as mandatory base, PPF as a voluntary addition starting with even ₹500/month.

Does PPF make sense under the new tax regime in 2026?

Yes. Under the new tax regime, you can’t claim 80C on PPF contributions — but PPF’s interest and maturity remain 100% tax-free regardless. For someone in a 20–30% tax bracket, a 7.1% return that’s entirely tax-free translates to an effective pre-tax equivalent of 9–10%. That’s competitive with most debt instruments, especially over a 15+ year horizon. The investment case for PPF doesn’t disappear without 80C — it just changes from “tax saving” to “tax-free compounding.”

Should freshers open NPS immediately after joining a job?

Not necessarily. NPS makes the most sense in two scenarios: (1) you’re on the old tax regime at the 20–30% bracket, and the additional ₹50,000 80CCD(1B) deduction saves you ₹10,000–15,000 per year; or (2) your employer routes contributions through 80CCD(2), which works under the new regime too. If neither applies — you’re on the new regime and your employer doesn’t offer structured NPS — the lock-in until 60 and mandatory annuity at exit make EPF vs PPF a cleaner starting point for most freshers.

What happens to EPF when I change jobs?

Your EPF doesn’t disappear when you leave a job — it stays in your account earning 8.25% interest. You must transfer it to your new employer’s account using your UAN on the EPFO Unified Portal. The process takes under 10 minutes online. Withdrawing instead of transferring is a serious mistake: withdrawal before 5 years of continuous service makes the full amount taxable, and TDS at 10% is deducted on withdrawals above ₹50,000. Transferring preserves compounding that can be worth ₹10–40 lakh over a career.

Can I have both EPF vs PPF at the same time?

Yes, and most financial advisors recommend it. EPF is mandatory if you’re salaried in a covered organisation; you can open a PPF account independently at any bank or post office regardless of your employment status. Both operate simultaneously, and both offer EEE tax treatment. There’s no rule preventing contributions to both — they serve different roles and have separate limits.

What is the 80C overlap between EPF vs PPF?

Both EPF employee contributions and PPF contributions count toward the same ₹1.5 lakh Section 80C ceiling (under the old tax regime). They’re not additive. If your annual EPF contribution is ₹36,000, you only need ₹1,14,000 more in PPF to max the 80C limit — not ₹1.5 lakh more. Many freshers over-invest in PPF thinking they get ₹1.5L from each, missing the shared pool. Calculate your EPF contribution first, then fill the remaining 80C space with PPF or ELSS.

Is VPF better than PPF for salaried employees?

For salaried employees specifically, VPF (Voluntary Provident Fund) is worth comparing seriously to PPF. VPF earns the same 8.25% as EPF (vs PPF’s 7.1%), requires no new account, and is automated through payroll. The only caveat: VPF contributions above ₹2.5 lakh per year attract tax on interest earned above that threshold. For amounts within the ₹2.5L ceiling, VPF is arguably the highest risk-free, tax-efficient instrument available to salaried employees — higher rate than PPF, no separate account management, and same EEE treatment up to the threshold.

What is the NPS annuity rule and why does it matter?

At NPS maturity (age 60), up to 60% of your corpus can be withdrawn as a tax-free lump sum. The remaining 40% must be used to purchase an annuity — a regular monthly income for life from an approved insurance company. The annuity income is taxable at your slab rate. This is the key reason NPS is sometimes less tax-efficient than EPF or PPF at exit, even though it may accumulate a larger corpus due to equity exposure. If you’re in a lower tax bracket at retirement, the annuity tax impact is smaller. Plan accordingly using MoneyOra’s NPS Calculator.

How does inflation affect EPF vs PPF returns?

Both EPF (8.25%) and PPF (7.1%) provide positive real returns after India’s average CPI inflation of 4–6%. But neither keeps pace with inflation in a high-inflation environment above 7–8%. Over a 30-year retirement savings horizon, fixed-rate instruments alone — without any equity exposure — may leave your corpus below what you need to sustain current lifestyle. The solution is using EPF/PPF as the guaranteed base (preserving capital) while adding equity SIPs for inflation-beating growth. Check how SIP contributions complement EPF/PPF in your overall plan.

Pingback: Salary Investment Plan: The Proven Way to Build ₹1 Crore

Pingback: 100 Per Day Investment: How Wealth Can You Build - MoneyOra

Pingback: Hidden Bank Charges: 9 Fees Costing You ₹2,000+ - MoneyOra

Pingback: EPFO 3.0: The Best Way to Access Your PF in 2026 - MoneyOra