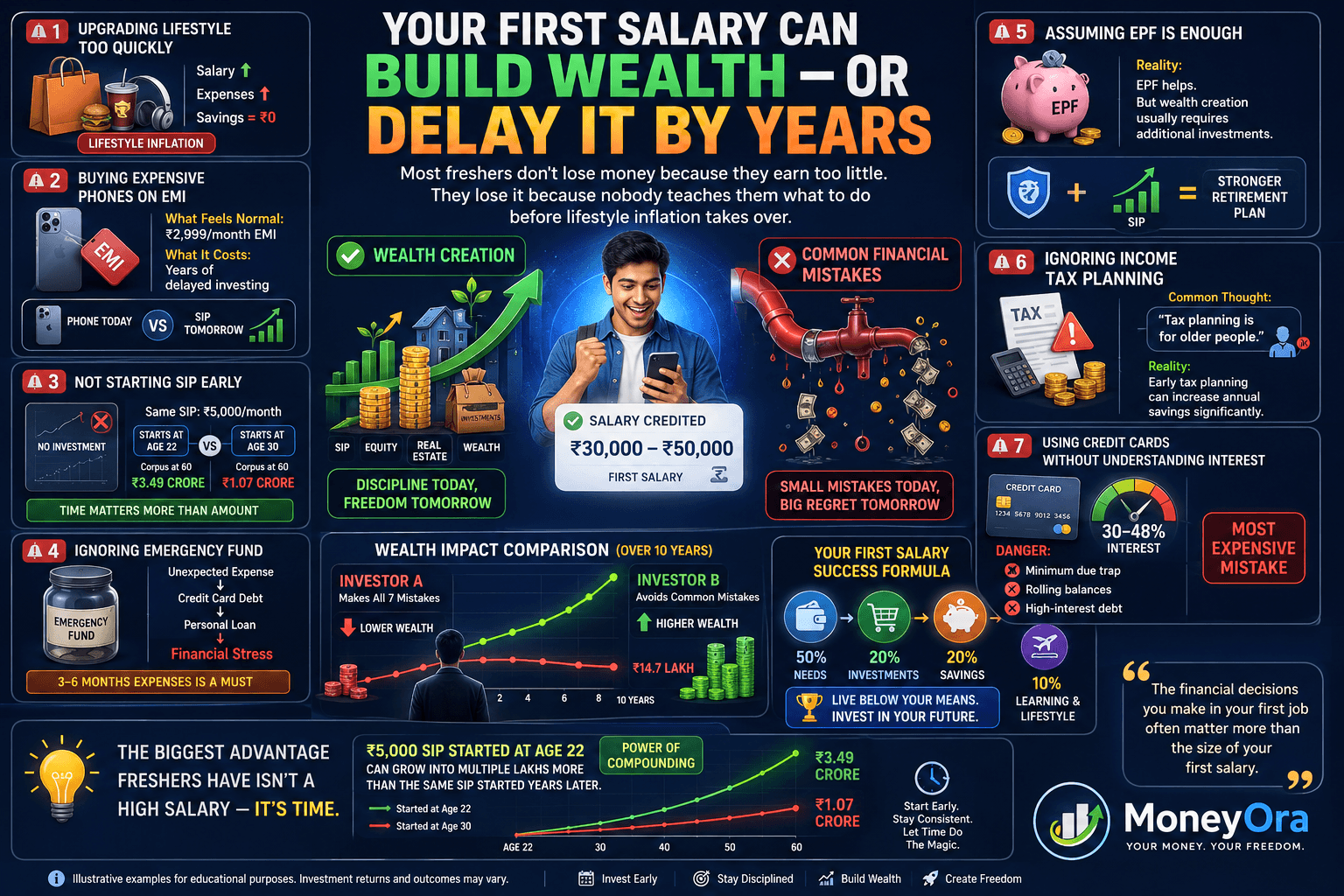

The first salary hits and you feel invincible. ₹30,000 or ₹50,000 in your account — real money, finally. And then, somehow, three weeks later it’s gone.

This isn’t rare. It’s almost a rite of passage for freshers in India. The problem isn’t that you earn too little. The problem is that nobody teaches you what to actually do with a salary before the lifestyle inflation kicks in and the financial mistakes start stacking up. According to SEBI’s investor education data, a significant share of first-time investors in India are under 30 — and most enter markets without any structured financial plan.

These financial mistakes freshers make in their first job don’t feel like mistakes in the moment. They feel like normal decisions — buying a phone on EMI, assuming EPF “sorts itself out,” skipping income tax planning because “that’s for older people.” Each one looks small. Together, they can cost you lakhs in lost compounding over the next decade.

Here are the 15 most common financial mistakes freshers make — and exactly how to avoid each one.

Key Takeaways — Financial Mistakes Freshers Must Know

- Starting a ₹3,000/month SIP at age 22 instead of 30 can generate roughly ₹30–35 lakh more at retirement — just from 8 extra years of compounding. (AMFI India)

- Withdrawing EPF before 5 years of service makes the entire amount taxable — one of the most common financial mistakes freshers make when switching jobs.

- The new income tax regime is the default from FY 2024–25 onwards. Not comparing regimes once a year can mean paying thousands more in tax than necessary.

- An emergency fund of 3–6 months of expenses is the single most protective step any fresher can take before starting to invest.

1. Spending the Entire First Salary Before Saving Anything

The classic financial mistake freshers make — and almost universally. First salary lands, celebrations happen, new phone gets bought, dinner gets treated, weekend trip gets planned. By the time the second month starts, zero savings exist from month one.

The issue isn’t the spending. It’s the order. Most freshers spend first and plan to save “whatever’s left.” That leftover is almost always zero. India’s household savings rate has been declining steadily — RBI data shows net household financial savings dropped to around 5.1% of GDP in FY2023, a multi-decade low.

The fix: Reverse it. The day salary hits, transfer a fixed amount to a separate savings or investment account — before anything else gets touched. Even ₹2,000 on day one is better than ₹0 on day thirty.

The concept has a name: pay yourself first. It works because it removes willpower from the equation.

Pro Tip: Set up an auto-debit SIP on the same date your salary credits. You never see that money in your “spending account,” so you never feel like you’re giving something up. Use MoneyOra’s SIP Calculator to decide how much to set aside.

2. Not Understanding CTC vs. Take-Home Salary

Your offer letter says ₹6 LPA (lakhs per annum). You do the math: ₹6,00,000 ÷ 12 = ₹50,000 a month. Then your first salary arrives and it’s ₹38,000.

This shocks almost every fresher — and it’s one of the first financial mistakes freshers make before they even get started. CTC — Cost to Company — includes your EPF contribution, professional tax, gratuity components, insurance premiums, and sometimes variable pay that only comes quarterly or annually. Take-home is always lower. The Income Tax Department’s portal has a clear breakdown of all salary deductions applicable to salaried employees.

| Component | Monthly (₹) |

|---|---|

| Basic Salary (40% of CTC) | 20,000 |

| HRA (50% of Basic, metro) | 10,000 |

| Special Allowance | 10,000 |

| Employer EPF (12% of Basic) | 2,400 |

| Gratuity provision | 962 |

| Gross CTC (monthly) | 50,000 |

| Less: Employee EPF (12% of Basic) | –2,400 |

| Less: Professional Tax (varies by state) | –200 |

| Less: TDS (income tax) | ~–1,500 |

| Approximate Take-Home | ~38,000–40,000 |

Know your actual take-home before you make spending plans. Ask HR for a salary breakup sheet if your offer letter doesn’t include one.

3. Ignoring EPF — or Withdrawing It When Changing Jobs

Among the costliest financial mistakes freshers make is mishandling EPF. The EPF interest rate for FY 2025-26 is 8.25% per annum, tax-free (up to ₹2.5 lakh annual contribution) — confirmed by the EPFO official site. That’s better than most bank FDs after tax. Yet freshers either ignore their EPF passbook entirely or, worse, withdraw the balance when they switch jobs.

Here’s why early withdrawal is a mistake that compounds over time:

- If you withdraw before 5 years of continuous service, the entire amount becomes taxable — principal and interest both.

- TDS at 10% is deducted on withdrawals above ₹50,000 if your PAN is linked; 20% if it isn’t.

- You lose years of 8.25% compounding that can’t be replaced easily.

What to do instead: When you change jobs, transfer your EPF through the EPFO Unified Portal using your UAN number. Takes 10 minutes online. Your balance continues compounding without a break.

To understand how much your EPF will grow over 30–35 years, run the numbers on MoneyOra’s EPF Calculator. The result tends to surprise people who thought EPF was “just a deduction.”

4. Not Comparing Old vs. New Income Tax Regime

Not comparing tax regimes is a financial mistake freshers make every April without realising it. From FY 2024-25, the new income tax regime is the default for all salaried employees — as notified by the Income Tax Department. If you do nothing, you’re in the new regime. The problem: for many freshers with HRA, education loan interest, or 80C investments, the old regime might save more tax.

| Feature | Old Regime | New Regime |

|---|---|---|

| Standard deduction | ₹50,000 | ₹75,000 |

| HRA exemption | Yes | No |

| 80C deduction (up to ₹1.5L) | Yes | No |

| NPS deduction (80CCD) | Up to ₹2L | Employer NPS only |

| Tax-free income (rebate u/s 87A) | Up to ₹5L taxable income | Up to ₹12L taxable income |

| Who benefits more? | Higher earners with many deductions | Freshers & lower earners with few deductions |

The only way to know which regime saves you more is to calculate both. Run your actual numbers — don’t guess. You can switch regimes every year if you’re salaried with no business income.

5. Taking EMIs for Everything Without a Repayment Plan

The “no-cost EMI” trap — a financial mistake freshers fall into fast

Phones, laptops, appliances, even vacations — all available on easy EMIs. No-cost EMI sounds free. It usually isn’t. The processing fee, GST on interest charges, or higher product price often covers the “zero interest” promise quietly. Credit card debt in India carries interest of 36–42% per annum, as tracked by the Reserve Bank of India.

More importantly: every EMI you take is a fixed monthly commitment that competes with saving and investing. A fresher with ₹3,000 in EMIs every month for 18 months has locked ₹54,000 of future income before even deciding how to use it.

The rule of thumb: Keep total EMI obligations below 30% of take-home salary. Above that, your financial flexibility disappears fast.

Before taking any loan, calculate the actual total cost using MoneyOra’s Personal Loan EMI Calculator or EMI Calculator. The total interest amount is usually uncomfortable to see. That discomfort is useful.

6. Having No Emergency Fund

Medical emergency. Sudden job loss. Family crisis. These don’t ask for permission. Having no emergency fund is a financial mistake freshers almost universally make — and one that forces borrowing at high interest when life doesn’t go to plan.

The standard guidance is 3–6 months of expenses in a liquid account. For a fresher in their first year, even 1–2 months saved is a real protective buffer.

Where to keep it: a liquid mutual fund or a high-interest savings account — not a regular savings account that earns 2.5–3%, but not locked away in FDs either. The fund has to be accessible within 24–48 hours.

Beginner Trap: A lot of freshers think their credit card is their emergency fund. Credit cards solve short-term cash problems, but they create medium-term debt problems — at 36–42% annual interest. They are not an emergency fund.

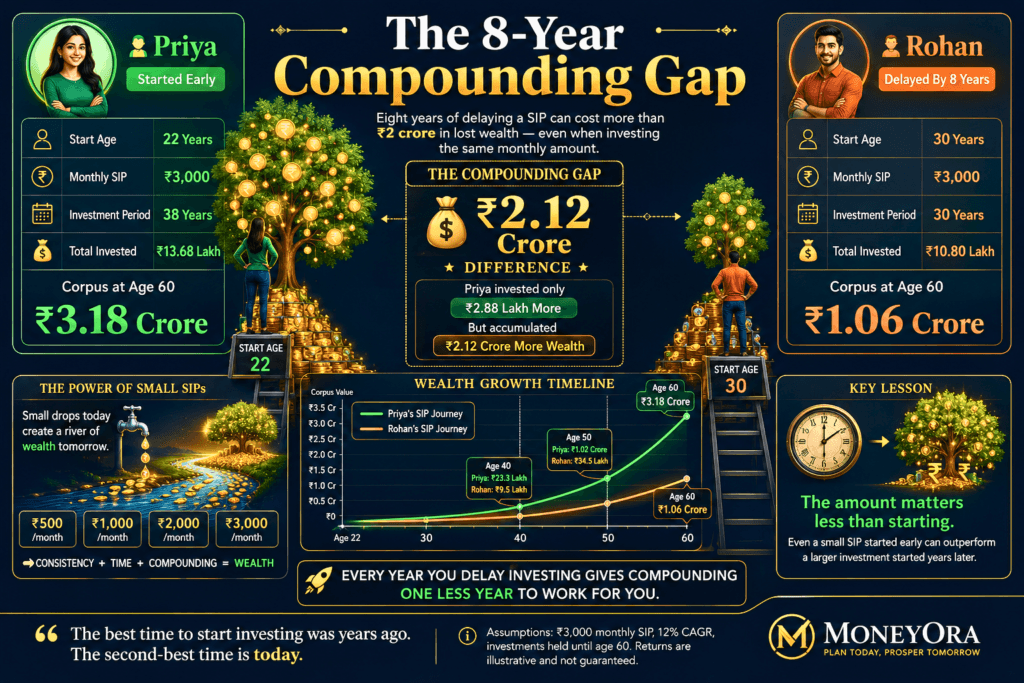

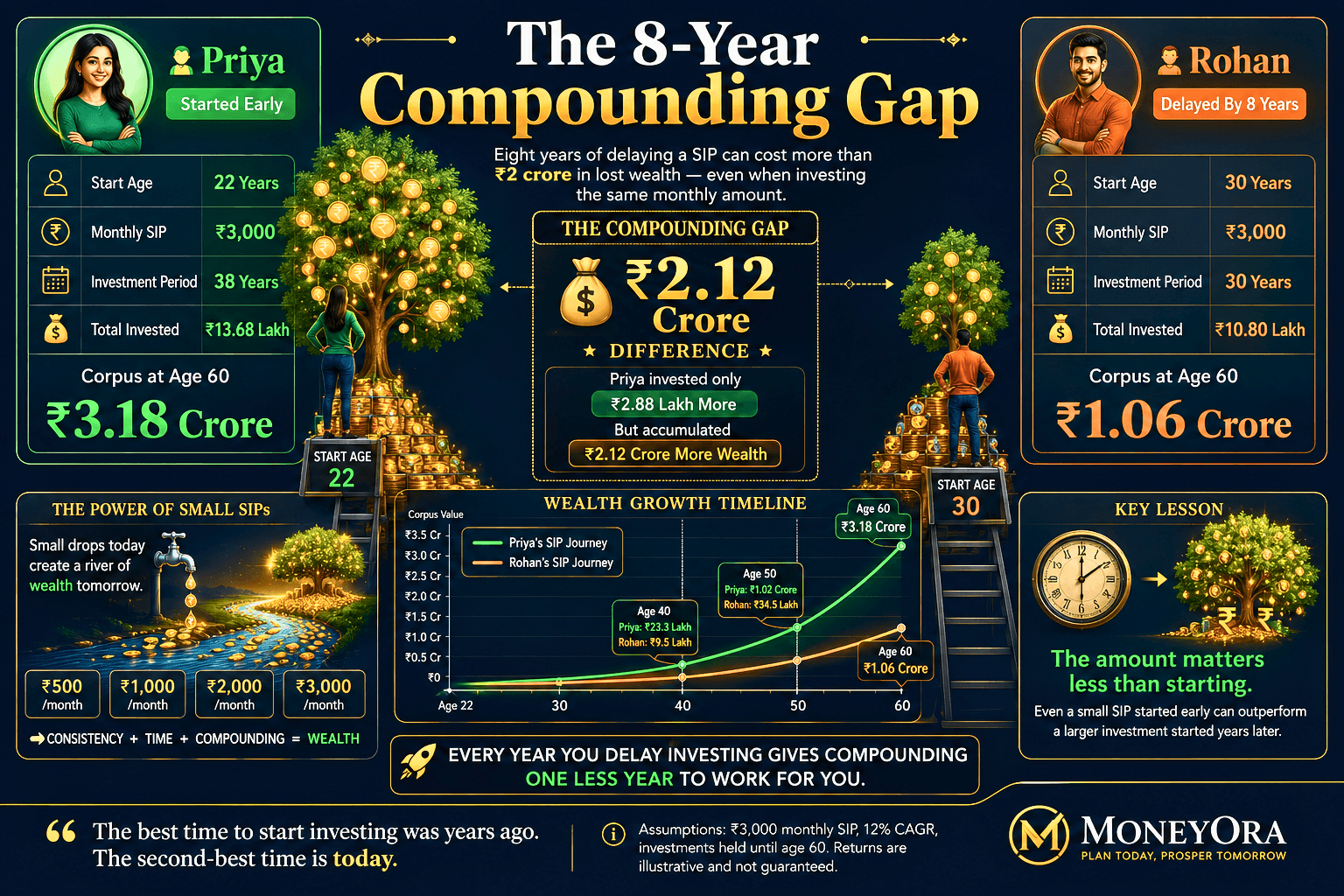

7. Waiting to Start SIP — “I’ll Start Next Year”

Delaying SIP is the single most expensive financial mistake freshers make. Not in a dramatic, obvious way — in a quiet, compounding way that only shows up 20 years later. AMFI’s data shows SIP inflows hit ₹26,632 crore in a single month in 2025 — proof that early SIP habits built by young earners now create massive long-term wealth pools.

The 8-year compounding gap — real numbers

Let’s say two people, Priya and Rohan, both aim for a retirement corpus. Priya starts a ₹3,000/month SIP at age 22. Rohan starts the same SIP at age 30. Both stop at 60. Assumed return: 12% CAGR.

| Investor | Start Age | Total Invested | Corpus at 60 |

|---|---|---|---|

| Priya | 22 | ₹13.68 lakh | ₹3.18 crore |

| Rohan | 30 | ₹10.80 lakh | ₹1.06 crore |

| Difference (the cost of 8 years of delay) | ₹2.12 crore | ||

Priya invested ₹2.88 lakh more than Rohan in total. But she ended up with ₹2.12 crore more. That’s the compounding gap. Eight years of “I’ll start next year” cost Rohan over two crore rupees.

Run your own scenario on MoneyOra’s SIP Calculator. Start with whatever you can manage — ₹500, ₹1,000, ₹2,000. The amount matters less than starting.

8. Treating Fixed Deposits as a Wealth-Building Tool

Over-relying on FDs is a quiet financial mistake freshers make because FDs feel safe — but they’re consistently beaten by inflation over long periods. A 7% FD sounds solid until you factor in the 30% tax on interest (if you’re in the 30% bracket), bringing the actual post-tax return to roughly 4.9%. With India’s average CPI inflation at 5–6%, an FD may not grow your real wealth at all.

FDs have a place — they’re excellent for the emergency fund component or for money you need within 1–2 years. For anything longer, equity mutual funds via SIP have historically produced meaningfully better returns for patient investors.

Check current FD rates and calculate maturity values using MoneyOra’s FD Calculator before locking in any amount.

Disclaimer: Equity mutual fund returns are market-linked and not guaranteed. Historical performance does not guarantee future returns. Invest based on your risk profile and investment horizon.

9. Relying Only on Employer Health Insurance

Skipping personal health insurance is a financial mistake freshers make that only shows up as a crisis — never as a slow burn. Your employer provides group health insurance — ₹3 lakh or ₹5 lakh cover. Sounds adequate. But the IRDAI (Insurance Regulatory and Development Authority of India) consistently notes that employer group health cover lapses immediately upon job change, leaving a dangerous gap. There are three reasons why depending on it entirely is a mistake:

- It disappears the moment you leave the job. No notice period, no buffer — the coverage ends with employment.

- ₹3–5 lakh is not adequate for serious hospitalisation in a private hospital in a metro city. A single cardiac event or surgery can cross ₹8–12 lakh easily.

- Waiting periods apply on individual policies. If you buy health insurance at 30, pre-existing conditions (diabetes, hypertension) may have a 2–4 year waiting period before coverage kicks in. Buying at 22–24 often means zero or minimal waiting periods and significantly lower premiums.

A basic ₹5–10 lakh individual health policy in your mid-twenties costs ₹4,000–8,000 per year. That’s less than a single restaurant bill for many freshers. It’s worth prioritising.

10. Investing in Individual Stocks Without Any Foundation

Jumping into stocks without a foundation is a financial mistake freshers make with real money consequences. The stock market surge of 2020–2021 created a wave of new retail investors — many of them freshers who saw friends double money in months.

SEBI’s investor education portal notes that a large portion of new demat accounts opened during 2020–2022 belonged to first-time investors under 30, many with no prior market knowledge. Some made money. Many lost it quietly, and didn’t talk about those trades.

Stocks aren’t inherently dangerous for freshers. The danger is investing without understanding what you’re buying, why you’re buying it, and what price makes sense.

A practical starting framework before buying any stock:

- Understand the company’s business model and revenue sources

- Check valuation — is the P/E ratio reasonable for the sector? (MoneyOra’s P/E Ratio Calculator can help)

- Know your stop-loss before you buy — not after (Stop-Loss Calculator)

- Keep direct stock allocation to a manageable portion of your portfolio, not everything

For freshers who want stock market exposure without picking individual companies, index funds (Nifty 50 or Nifty Next 50) via SIP are a reasonable starting point. They’re diversified, low-cost, and don’t require daily monitoring.

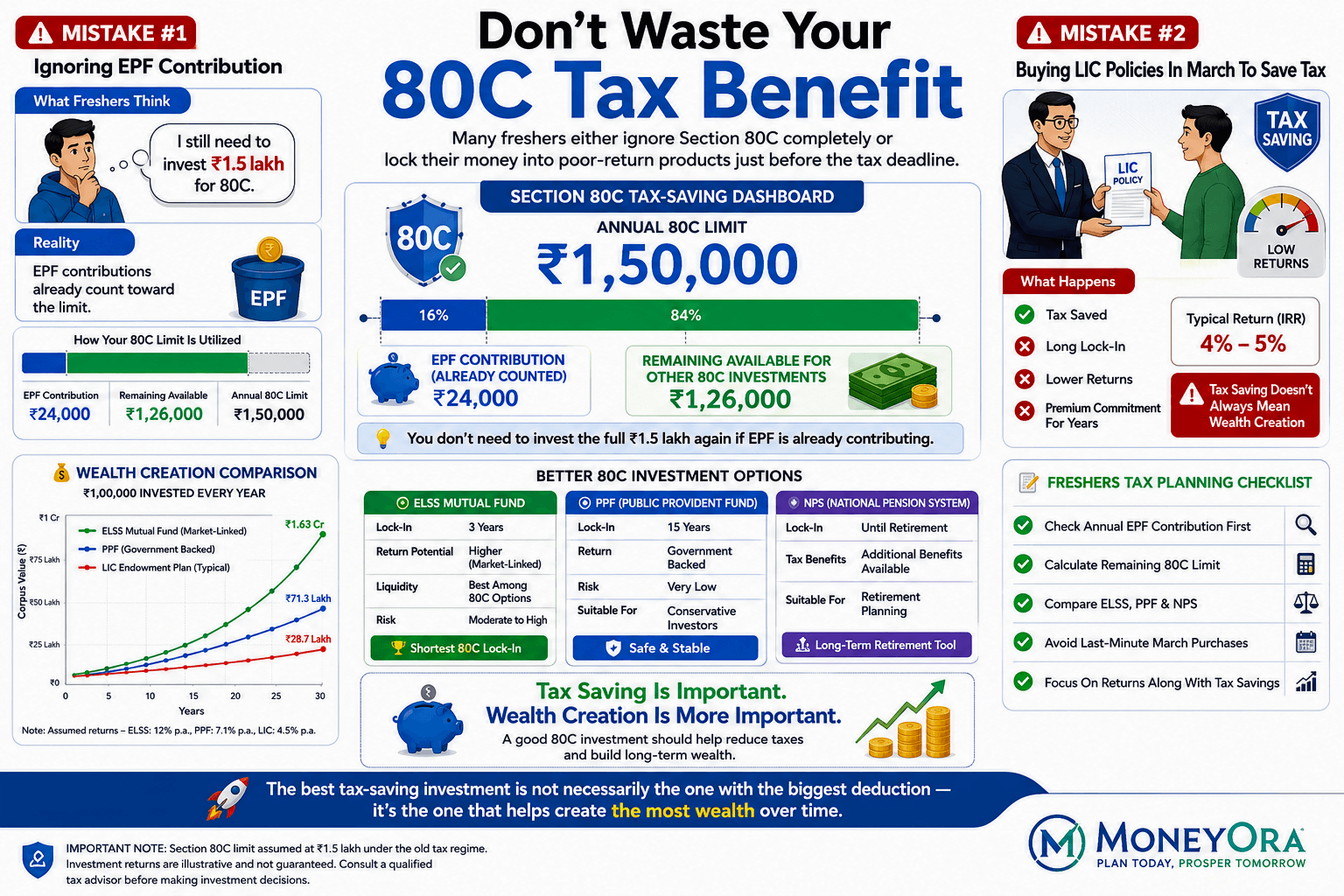

11. Missing the ₹1.5 Lakh 80C Limit — or Not Using It Well

Misusing or ignoring Section 80C is a financial mistake freshers make that directly increases their tax liability. Section 80C of the Income Tax Act allows a deduction of up to ₹1.5 lakh per year under the old tax regime. EPF contributions count toward this. So do ELSS mutual funds, PPF, LIC premiums, NPS (partial), home loan principal, and others.

Two common mistakes freshers make with 80C:

- Forgetting that EPF already partially fills it. If your EPF contribution is ₹24,000/year, you only need ₹1,26,000 more to max 80C — not the full ₹1.5 lakh.

- Rushing into LIC endowment policies in March to “save tax.” LIC endowment returns are low (typically 4–5% IRR), the lock-in is long (10–25 years), and the premiums don’t stop. You save tax, but you may tie up money in a poor-returning product for two decades.

ELSS (Equity Linked Savings Schemes) are worth comparing — they have the shortest lock-in of all 80C instruments (3 years) and have historically offered better returns than traditional instruments. They’re equity-linked, so returns are not guaranteed.

Use MoneyOra’s PPF Calculator or NPS Calculator to model long-term returns for different 80C instruments.

12. Having No Budget Whatsoever

Not budgeting is the invisible financial mistake freshers make. You don’t feel it happening. You just notice, every month, that the account is lower than you expected and you can’t quite explain where it went.

Freshers often resist budgets because they think budgeting = restriction. It doesn’t. A budget is just a plan. It tells your money where to go instead of you wondering where it went.

A simple starting framework for freshers (50-30-20 rule, adapted)

| Category | % of Take-Home | What Goes Here |

|---|---|---|

| Needs | 50% | Rent, food, transport, utilities, insurance |

| Wants | 30% | Entertainment, eating out, shopping, travel |

| Savings & Investments | 20% | SIP, PPF, emergency fund, EPF top-up |

This isn’t a rigid rule — it’s a starting point. In an expensive metro on a fresh salary, 50% for needs might be unavoidable. Even 10–15% saved consistently beats 0% perfectly planned.

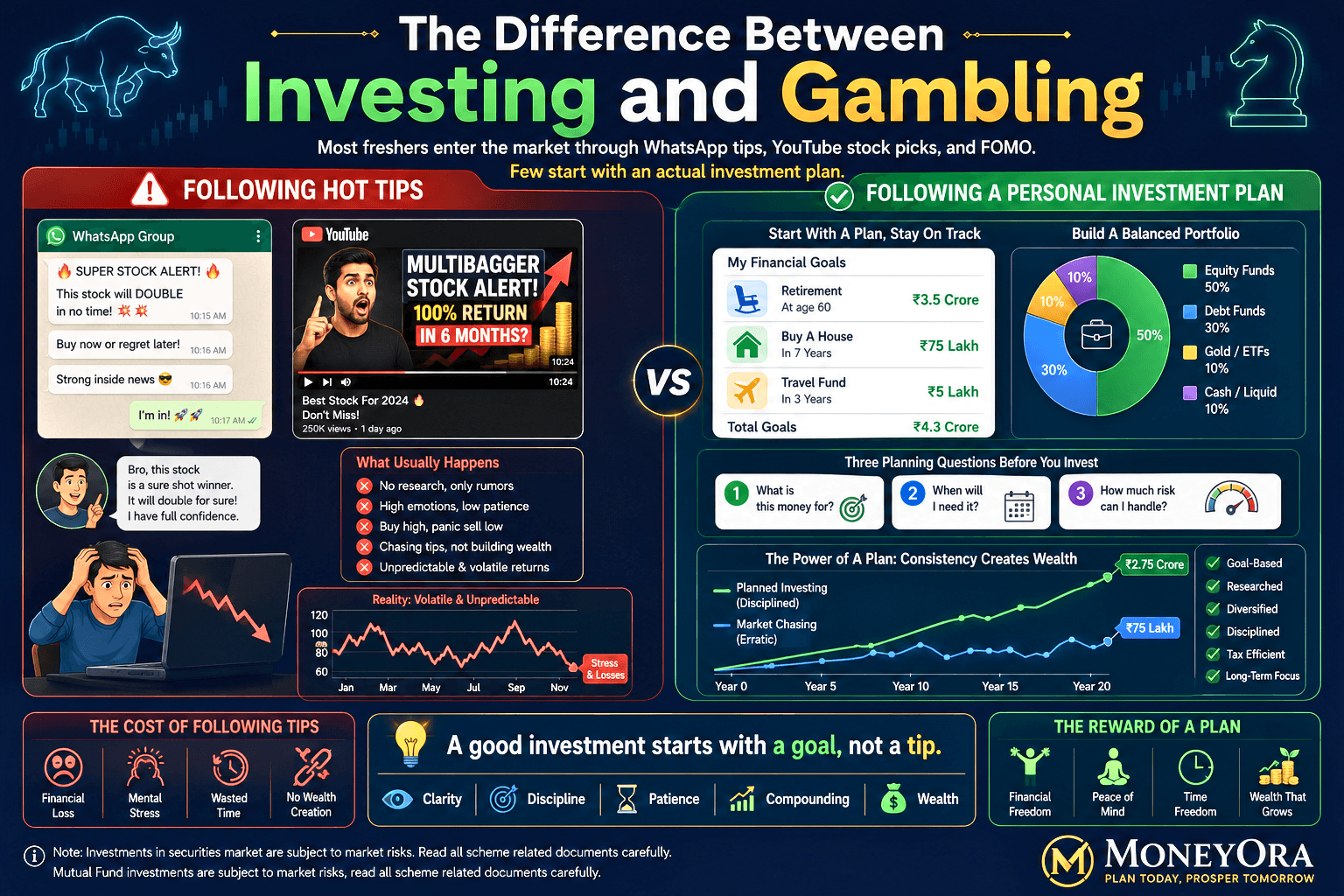

13. Chasing “Hot Tips” Instead of a Personal Investment Plan

Chasing unverified stock tips is a financial mistake freshers make that feels like investing but is really gambling. Office WhatsApp groups, YouTube channels with “100% guaranteed returns,” a cousin who “made 3x in 6 months” — this is the environment many freshers enter the market through. SEBI has repeatedly issued warnings about unregistered “finfluencers” giving investment advice without qualifications.

Hot tips aren’t inherently wrong. The problem is investing real money in something you don’t understand, with no exit plan, based on someone else’s conviction. When the trade goes wrong (and it often does), you don’t know why, and you don’t know what to do.

A personal investment plan doesn’t need to be complicated. It just needs to answer three questions:

- What is this money for? (retirement, house, travel fund — specific goal)

- When do I need it? (5 years? 20 years?)

- How much risk can I realistically handle without panic-selling?

Once you have answers, the right instruments become much clearer. Lumpsum Calculator and CAGR Calculator on MoneyOra can help you work out whether a given investment is on track for your goal.

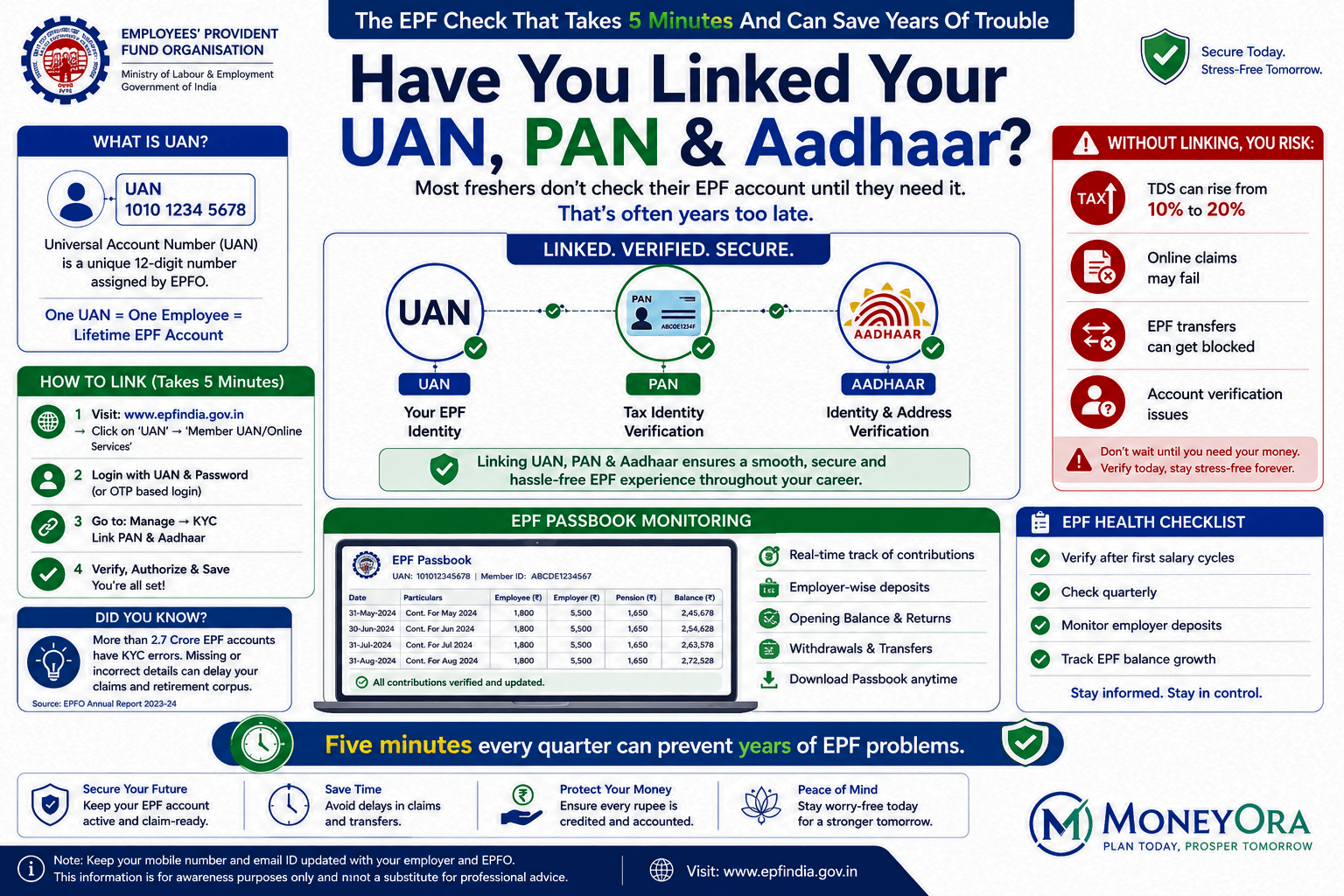

14. Not Linking UAN, PAN, and Aadhaar — and Ignoring the EPF Passbook

Your UAN (Universal Account Number) is the single most important number for your EPF account. Without linking it to your PAN and Aadhaar:

- TDS on EPF withdrawals jumps from 10% to 20% (for withdrawals above ₹50,000)

- Online claims and transfers get blocked

- You can’t verify whether your employer is depositing EPF on time

Employers sometimes delay EPF deposits — especially smaller companies. The only way you know is by checking your EPF passbook on the EPFO Unified Member Portal or the UMANG app. Not checking is a financial mistake freshers make that only surfaces as a nasty surprise years later when they try to transfer or withdraw.

Log in once when you join, verify the balance after your first two salary cycles, and check again every quarter. Takes five minutes.

15. Not Increasing Investments When Salary Increases

This is the one that separates people who build wealth slowly from people who stay stuck. Salary hike of 15% comes in April. Lifestyle immediately adjusts upward — better apartment, more eating out, new gadget. Investment amount: unchanged from two years ago.

A simple rule that works: whenever your salary increases, put at least 50% of the increment into investments before lifestyle adjusts. If your take-home goes from ₹38,000 to ₹44,000 (₹6,000 increase), add ₹3,000 to your SIP. Spend the other ₹3,000 however you want.

Over 5–7 years, this habit builds a meaningfully larger portfolio than any single “right investment” decision ever could. Use MoneyOra’s SIP Calculator to see how adding ₹1,000–2,000 per year to your SIP changes your end corpus.

Also, check your Stock Return Calculator periodically to track whether your individual investments are performing in line with your expectations.

MoneyOra Analysis: What the Numbers Tell You

The 15 mistakes above aren’t random. They share a pattern: they all look harmless individually and compound quietly into large financial gaps.

Consider this comparison between two freshers, both starting at ₹5 LPA in Mumbai:

Fresher A (avoids the mistakes above): Starts ₹3,000/month SIP at 22, builds ₹1 lakh emergency fund in 18 months, maintains EPF continuity across two job changes, and increases SIP by ₹1,000 per year. By 35, this person has roughly ₹20–25 lakh in investments and a clear financial runway.

Fresher B (typical path): Spends the first two salaries freely, no SIP until 27, withdraws EPF at first job change, takes 3 EMIs simultaneously at 25. By 35, this person may have ₹3–5 lakh in scattered FDs and a sense that “investing is for later.”

The salary difference between A and B at 35 is probably minimal. The wealth gap could be ₹15–20 lakh. Built not through superior intelligence or luck — just through a handful of habits started 5 years earlier.

The compounding window is widest in your 20s. Every year you delay costs you more than you think — not in a scary way, but in a very real, calculable way. Run the numbers. The math is honest in a way that motivation rarely is.

Risks to Keep in Mind

- Market risk: Equity mutual funds and stocks carry market risk. Returns are not guaranteed. Invest only what you won’t need in the short term.

- Over-investment risk: Investing so aggressively that you have no liquid cash for genuine needs is also a mistake. Balance matters.

- Job security in early career: The first 1–2 years carry higher uncertainty. Keep your emergency fund accessible before moving money into locked instruments.

- Tax law changes: Tax deduction limits, EPF rules, and regime defaults can change with each Budget. Verify current rules on the Income Tax Department’s official portal (incometax.gov.in) or EPFO (epfindia.gov.in) before making decisions.

Where to Start — Right Now

You don’t need to fix all 15 financial mistakes at once. Pick three. The ones with the biggest impact for most freshers:

- Set up a ₹500–2,000 SIP today. Even a small amount started now is worth more than a large amount started later.

- Build one month of emergency fund before anything else gets invested.

- Check your EPF passbook within the next 48 hours. Verify contributions are being deposited.

The rest can follow over the next 6–12 months as habits build and income grows. Financial mistakes freshers make are almost always fixable — the earlier you start, the less expensive they are to correct.

Run your own numbers, model your own scenarios, and see what your money can actually become.

Start with a free calculator

SIP • EMI • EPF • PPF • FD • NPS • Lumpsum — all free, no login required.

Use the free calculator now on MoneyOra.inMoneyOra Tools

- SIP Calculator — Plan your monthly investment and see 10–30 year projections

- EPF Calculator — Model how your PF grows over your working life

- EMI Calculator — Calculate the true cost of any loan before taking it

- FD Calculator — Compare FD maturity amounts at different tenures and rates

- PPF Calculator — Long-term tax-free wealth building projection

- NPS Calculator — Model your pension corpus under the National Pension System

- Lumpsum Calculator — See what a one-time investment grows to over time

- CAGR Calculator — Measure actual annual growth rate of any investment

What are the most common financial mistakes freshers make in their first job?

The most common financial mistakes freshers make include spending the first salary before saving anything, not understanding their actual take-home vs. CTC, withdrawing EPF early, skipping SIP investments, taking multiple EMIs without a plan, and having no emergency fund. These mistakes individually seem small but compound into large wealth gaps over 5–10 years.

How much should a fresher save from their first salary in India?

A practical starting target is 20% of take-home salary. On a take-home of ₹35,000, that’s ₹7,000 — split between an emergency fund and a SIP. If 20% is too tight, even 10% (₹3,500) invested consistently from the first month has a meaningful compounding impact over 30+ years. The amount matters less than the habit of starting.

Is it okay for a fresher to withdraw EPF when switching jobs?

No — EPF withdrawal before 5 years of continuous service makes the entire amount taxable, including TDS deductions. The better option is to transfer the EPF balance to your new employer’s account using your UAN on the EPFO Unified Portal. The process is free, takes about 10 minutes online, and your corpus continues compounding without interruption.

Should freshers choose the old or new income tax regime?

It depends on income and deductions. The new regime is now the default and benefits freshers with taxable income below ₹12 lakh (after the ₹75,000 standard deduction) through the expanded rebate. Those with significant HRA, 80C investments, or home loan interest may save more under the old regime. Compare both each April before declaring to your employer.

What is the right order of financial priorities for someone in their first job?

A sensible order: (1) Build 1 month emergency fund. (2) Ensure EPF is active and UAN is KYC-linked. (3) Start even a small SIP — ₹500–1,000/month. (4) Max out 80C deductions once income justifies it. (5) Add health insurance outside employer cover. Everything else builds on this foundation over time.

How much should a fresher invest in stocks?

There’s no universal number, but a common starting point is keeping direct stock allocation to 20–30% of your investment portfolio — not 20–30% of salary. For freshers with limited financial knowledge, index funds (Nifty 50) via SIP offer broad market exposure with less risk than individual stock picking. Never invest money you may need within 1–2 years in equities.

Can a fresher earn ₹1 crore through SIP investments?

Yes — with time and consistency. A ₹5,000/month SIP at 12% assumed CAGR reaches approximately ₹1 crore in about 26 years. Starting at 23, that means reaching ₹1 crore by age 49. The number is sensitive to returns (which are not guaranteed), so it’s worth running different scenarios using MoneyOra’s SIP Calculator to set realistic expectations.

What is lifestyle inflation and how do freshers avoid it?

Lifestyle inflation is when spending increases in proportion to income, leaving savings unchanged despite higher earnings. Freshers avoid it by automating investments first (the “pay yourself first” method) and by committing to invest at least 50% of each salary increment before upgrading lifestyle. Even partial discipline here has a substantial long-term impact on net worth.

Pingback: Salary Investment Plan: The Proven Way to Build ₹1 Crore

Pingback: 100 Per Day Investment: How Wealth Can You Build - MoneyOra