₹100 per day does not seem like a lot. It is the cost of a coffee. A samosa. Something you buy online on impulse and forget about two days later. “see how even ₹100/day works in a salary investment plan” Many of us spend ₹100 times a day without a second thought. And by the end of the month we have no idea where the money went.

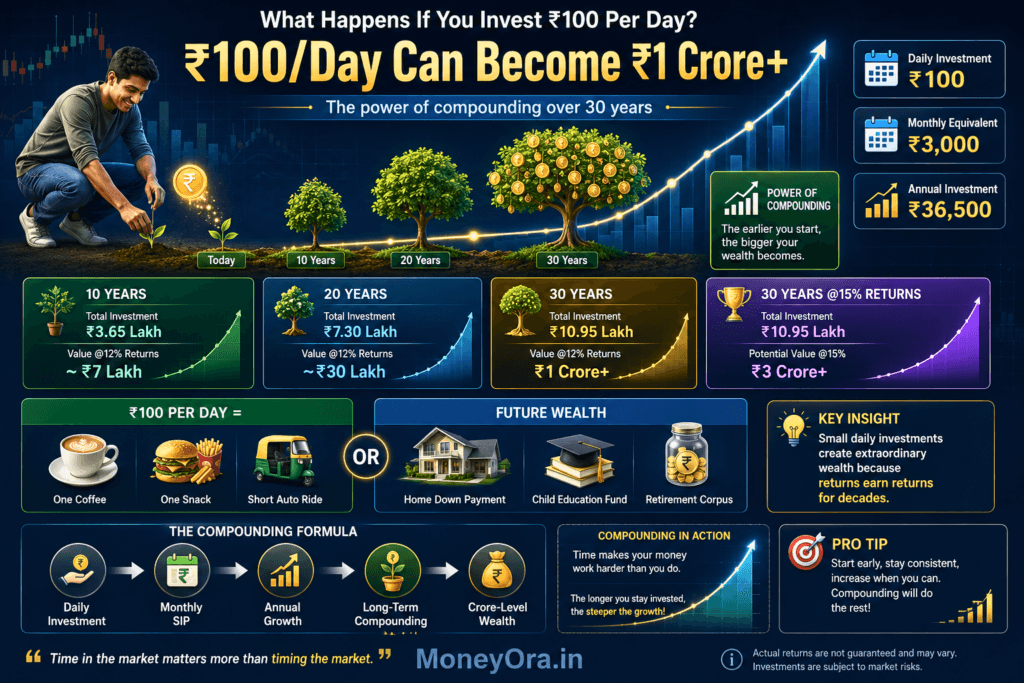

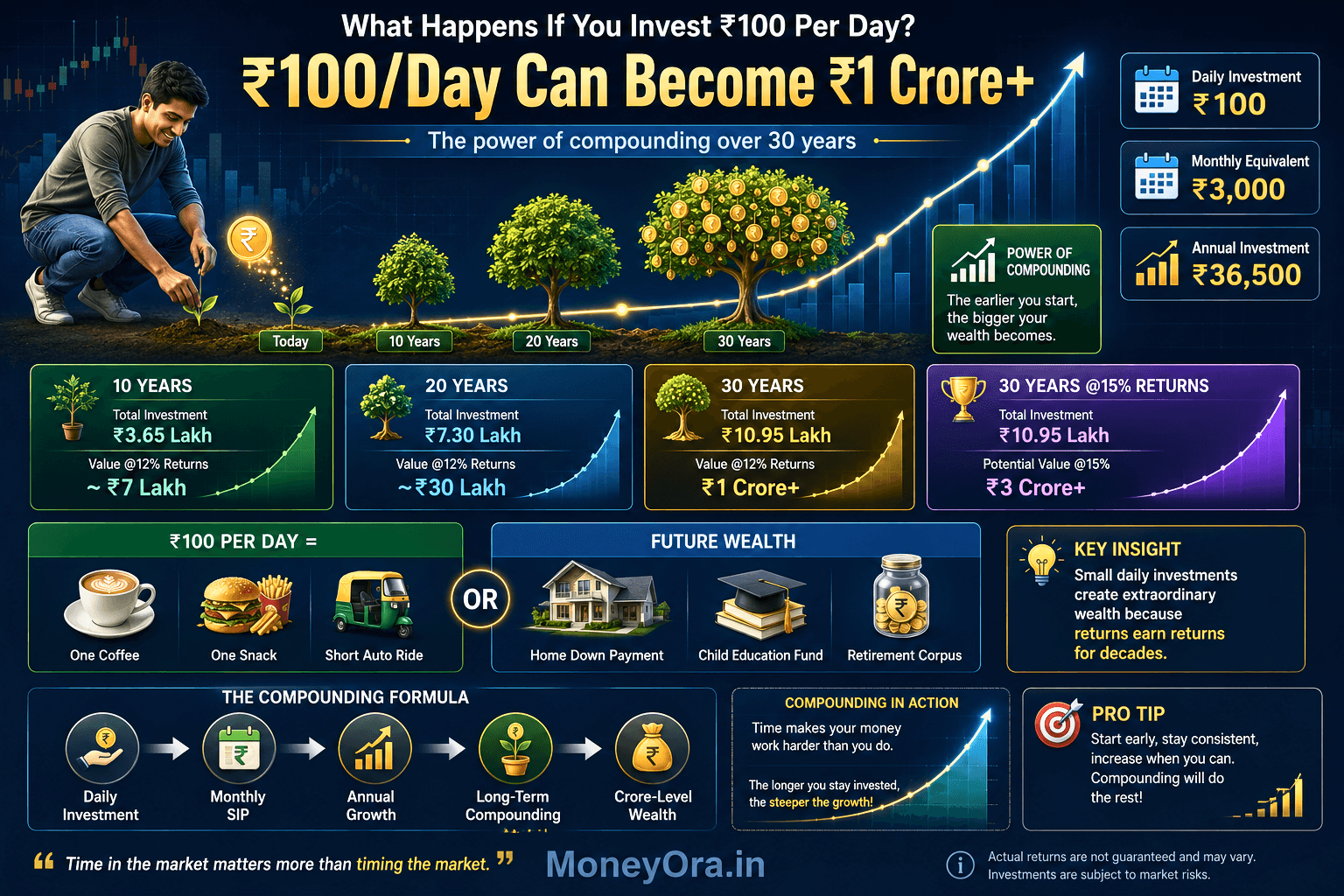

Here is what people do not tell you clearly: investing ₹100 per day. Which is ₹3,000 per month. At 12% returns per year grows to over ₹1 crore in 30 years. At 15% it grows to over ₹3 crore. Mistakes to avoid when starting to invest The ₹100 you do not invest today is not just ₹100. It is ₹80,000 that you could have had for your retirement. Because that is what ₹3,000 invested once grows to over 25 years at 12%.

This article explains the 100 per day investment challenge. It has rupee projections for 10, 20 and 30 years across five different instruments. It also has an inflation-adjusted reality check. We will look at the three mistakes that quietly ruin the compounding curve. “what happens to a ₹100/day SIP when the market crashes — the real data” We will give you a Day 1 action plan that takes 15 minutes to do. You can use MoneyOras SIP calculator with this guide to model your personal numbers.

Quick Answer: What does ₹100 per day investment return?

A ₹100 per day investment or ₹3,000 per month in equity funds at 12% returns per year grows to approximately ₹6.17 lakh in 10 years. It grows to ₹29.96 lakh in 20 years.. It grows to ₹1.05 crore in 30 years. Your total invested amount over 30 years is ₹10.8 lakh. The remaining ₹94+ lakh is entirely, from compounding. Your money making money.

The Exact Math: ₹100 Per Day Investment at 5%, 10%, 12% and 15% CAGR

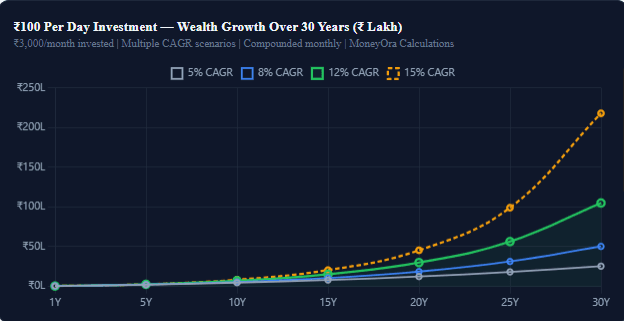

The most important number in the 100 per day investment equation is not the amount — it is the return. Let us look at what ₹3,000 per month (₹100 × 30 days) actually produces across different return scenarios.

₹100 Per Day Investment Returns — Full Projection Table

| Duration | Principal Invested | 5% CAGR (₹) | 8% CAGR (₹) | 12% CAGR (₹) | 15% CAGR (₹) |

|---|---|---|---|---|---|

| 5 Years | ₹1.80 lakh | ₹2.04 lakh | ₹2.20 lakh | ₹2.47 lakh | ₹2.63 lakh |

| 10 Years | ₹3.60 lakh | ₹4.65 lakh | ₹5.50 lakh | ₹6.99 lakh | ₹8.32 lakh |

| 15 Years | ₹5.40 lakh | ₹7.93 lakh | ₹10.52 lakh | ₹15.17 lakh | ₹20.46 lakh |

| 20 Years | ₹7.20 lakh | ₹12.33 lakh | ₹18.57 lakh | ₹29.96 lakh | ₹45.42 lakh |

| 25 Years | ₹9.00 lakh | ₹18.15 lakh | ₹31.30 lakh | ₹56.34 lakh | ₹99.09 lakh |

| 30 Years | ₹10.80 lakh | ₹25.35 lakh | ₹50.31 lakh | ₹1.05 crore | ₹2.18 crore |

Look at the 30-year row carefully. You invested ₹10.80 lakh total across 30 years. At 12% CAGR, you have ₹1.05 crore. That is ₹94 lakh that came from compounding alone — without a single extra rupee of investment from you. At 15%, the corpus is ₹2.18 crore against ₹10.80 lakh invested. The compounding contribution is 91% of the final number.

What ₹100 Per Day Investment Looks Like at 12% CAGR

Model these numbers for your situation using MoneyOras SIP calculator. Change the return rate change the duration and see how much your specific ₹100 per day investment can grow.

One thing to note: a 12% growth rate assumption is realistic for equity mutual funds over 15+ years in India. Historical data from Nifty 50 shows returns of 12–15% over 15-year periods. This is not guaranteed,. It is based on actual market history.

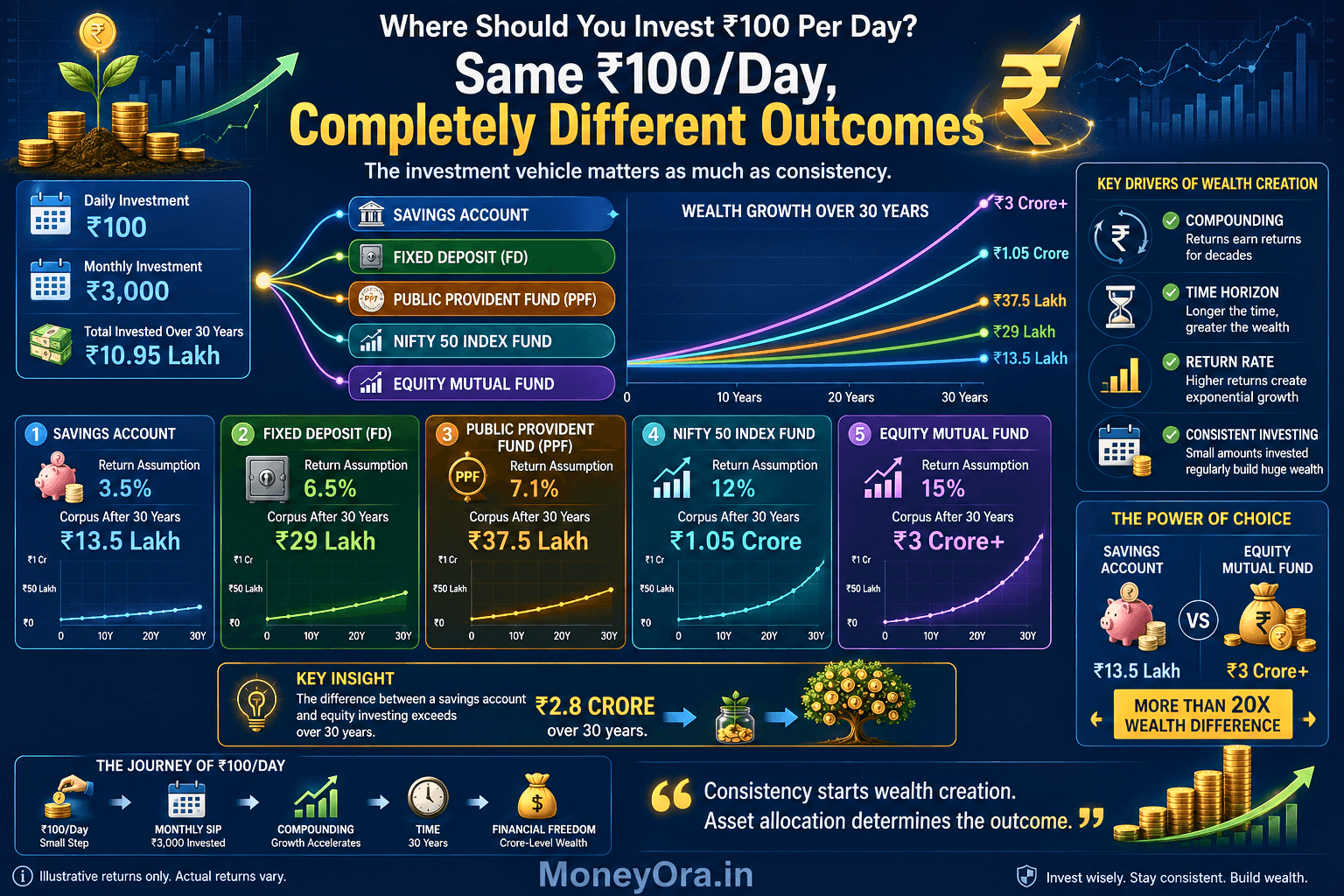

Which Instrument? SIP, PPF, FD, Index Fund. The ₹100/Day Comparison

The ₹100 per day investment question has another question inside it: where should you put it? The same ₹3,000 per month produces different results depending on the instrument. Here is a fair comparison, over 30 years.

Which Instrument Is Right for Your ₹100 Per Day Investment?

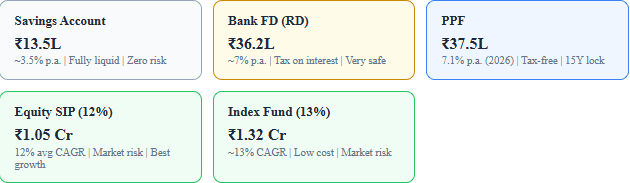

| Instrument | 30-Year Corpus | Tax Treatment | Risk | Best For |

|---|---|---|---|---|

| Savings Account | ~₹13.5 lakh | Interest taxed at slab | Nil | Emergency fund only |

| Bank RD | ~₹36.2 lakh | Interest taxed at slab | Very Low | Conservative investors |

| PPF | ~₹37.5 lakh | Fully tax-free (EEE) | Nil | Risk-averse, tax saving |

| ELSS (Mutual Fund) | ~₹90 lakh–₹1.1 crore | LTCG after 1 year; ₹1.25L exempt | High | Tax savers who can hold 3+ years |

| Equity SIP (diversified) | ~₹1.05 crore | LTCG after 1 year | High | Long-term wealth creation |

| Nifty 50 Index Fund | ~₹1.1–₹1.3 crore | LTCG after 1 year; low expense | Medium-High | Best risk-adjusted long-term pick |

For Indians who get a salary starting to invest one hundred rupees per day is a good idea.

The advice is to do the following:

If you do not like taking risks or this is your first time investing you should start by putting one thousand five hundred rupees per month in a PPF account and also put one thousand five hundred rupees per month in an index fund SIP.

If you are okay with the risk of the market and you will not need this money for fifteen years or more you can put the three thousand rupees per month into a Nifty 50 index fund.

If you want to save on taxes you can choose ELSS which is also called Equity Linked Savings Scheme. You cannot take out your money for three years. You can get a tax deduction, under Section 80C.

You can use MoneyOras calculator to see how much money you will get from a Recurring Deposit.

You can also use their calculator to see how money you will get from a PPF account and compare this to how much money you will get from a Fixed Deposit.

Then you can compare all of these to see how money you will get from an equity SIP to make a decision that you think is a good one.

Daily SIP versus Monthly SIP: Does It Make A Difference For A ₹100 Per Day Investment?

People often ask: should I invest ₹100 every day with a SIP or ₹3,000 on one fixed date every month with a monthly SIP?

The simple answer is: the difference in the amount of money you have after 20 to 30 years is very small. It is usually 0.5 to 1 percent. Daily SIPs are a bit better because you are investing at different times during the month.. If you do the math the difference after 30 years is only around ₹5,000 to ₹25,000 on a total of ₹1 crore or more. This is really not a deal.

What is more important than whether you do a SIP or a monthly SIP is being consistent. If you start a SIP of ₹100 and stop it for 4 months when the market is bad it will not do as well as a monthly SIP of ₹3,000 that keeps going for 30 years without stopping.

A Good Thing About Daily SIP: Daily SIPs have one big advantage. They work well with the way people get paid every day. If you get paid a bit every day like some workers do it is easier to invest ₹100 every day. This is better than trying to invest ₹3,000 all at every month which might not work if you do not have enough money in your account on that day.

Some platforms that allow daily SIPs include Paytm Money, Groww, HDFC Securities and SBI Securities. You can start with little as ₹100, per day. Most big mutual fund companies also allow SIPs if you invest directly with them.

The Inflation Reality Check. What Is That ₹1 Crore Worth in 30 Years?

This is the part that most articles leave out.. It is the part that really matters when you want to know what to expect.

In India inflation usually goes up by 5 to 6 percent every year. When inflation is 6 percent the money you have will be worth half much every 12 years. So if you have ₹1 crore in 30 years it will be like having ₹17 to ₹22 lakh today. This might sound bad.. Think about the other option. ₹1 Crore will not be worth much as you think it will be, in 30 years because of inflation. The value of ₹1 crore will go down a lot.

| Instrument | Nominal Corpus (30Y) | Real Corpus (6% inflation adj.) | Real CAGR |

|---|---|---|---|

| Savings Account (3.5%) | ₹13.5 lakh | ₹2.3 lakh | −2.5% real |

| Bank FD/RD (7%) | ₹36.2 lakh | ₹6.2 lakh | +0.94% real |

| PPF (7.1%) | ₹37.5 lakh (tax-free) | ₹6.4 lakh real value | +1.04% real |

| Equity SIP (12%) | ₹1.05 crore | ₹17–22 lakh real | +5.66% real |

| Index Fund (13%) | ₹1.32 crore | ₹22–27 lakh real | +6.6% real |

The savings account is not doing what you think it is. When you consider inflation the money in your savings account is actually losing value every year. This means that even if the amount of money in your savings account goes up the things you can buy with that money do not. Fixed Deposits and Public Provident Funds are not much better. They barely keep up with inflation. The value of your money only grows by less than one percent per year.

On the hand Equity Systematic Investment Plans are a different story. When you account for inflation Equity Systematic Investment Plans can grow the value of your money by five to six percent per year. This is what sets apart people who’re able to stay ahead of inflation from those who spend their whole lives saving but still struggle with money when they retire.

Important: You should remember that these numbers are based on what happened in the past not on what will happen in the future. There are years when the stock market does poorly like 2008 and 2020 and you can actually lose money. The twelve percent average return is what happens over a time. Some years are great and some years are terrible. This is why you should only invest in the stock market if you can leave your money there for ten years or more.

You can use our calculator to see how inflation affects an investment and another calculator to figure out what your real return on investment is after inflation by subtracting the inflation rate from the rate of return, on your investment.

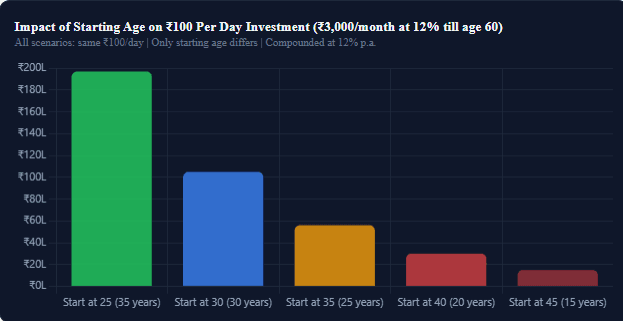

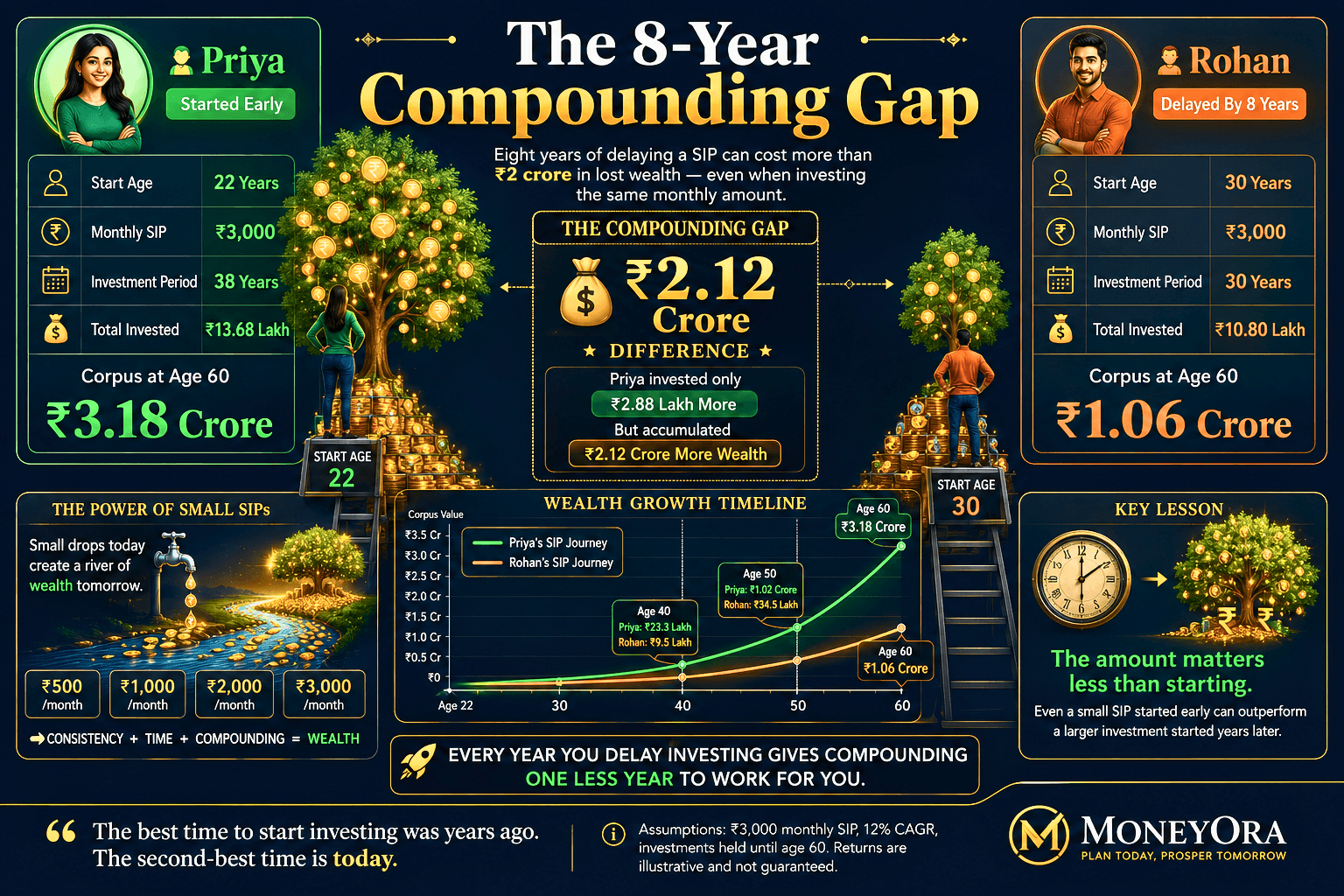

Starting Age Matters: The 5-Year Delay Costs ₹50+ Lakh on a ₹100/Day Investment

| Start Age | Years Invested | Total Invested | Corpus at 60 | Cost of Waiting |

|---|---|---|---|---|

| 25 | 35 years | ₹12.60 lakh | ₹1.97 crore | — |

| 30 | 30 years | ₹10.80 lakh | ₹1.05 crore | ₹92 lakh lost |

| 35 | 25 years | ₹9.00 lakh | ₹56 lakh | ₹1.41 crore lost |

| 40 | 20 years | ₹7.20 lakh | ₹30 lakh | ₹1.67 crore lost |

| 45 | 15 years | ₹5.40 lakh | ₹15 lakh | ₹1.82 crore lost |

If you start investing ₹100 per day at the age of 25 of 30 you will have ₹92 lakh more by the time you are 60. This is because you invested for 5 years. You paid ₹1.80 lakh more. You got ₹92 lakh more in return. That is a good payoff for the extra money you invested.

The main thing to learn here is that it is very important to start investing. If you are young and reading this the important thing you can do is start investing today instead of waiting until next month. It is not about choosing the investment plan. It is about starting

Let us look at an example. Riya starts investing ₹3,000 per month at the age of 25. Does this for 10 years. She invests a total of ₹3.6 lakh. Then she stops investing at the age of 35. Arun starts investing ₹3,000 per month at the age of 35. Continues to invest until he is 60. He invests a total of ₹9 lakh. If both of them get a 12% return on their investment Riya will have ₹1.85 crore at the age of 60. Arun will have ₹56 lakh at the age of 60. Riya invested money than Arun but she has more wealth because she started investing early. The key thing here is that it is the time you invest your money that matters, not how money you invest

Can investing ₹100 per day really make you a crorepati?

Yes it can. If you invest ₹100 per day which’s ₹3,000 per month in equity mutual funds and get a 12% return you will have approximately ₹1 crore in 29-30 years. If you get a 15% return you will have ₹1 crore in 24-25 years. Investing ₹100 per day can make you a crorepati. The Exact Timeline for this is 29-30 years at 12% return and 24-25 years, at 15% return.

| Return Rate | Time to ₹1 Crore | Total Invested | From Compounding |

|---|---|---|---|

| 8% CAGR (Conservative) | ~37 years | ₹13.32 lakh | ₹86.68 lakh |

| 10% CAGR | ~32 years | ₹11.52 lakh | ₹88.48 lakh |

| 12% CAGR (Realistic equity) | ~29 years | ₹10.44 lakh | ₹89.56 lakh |

| 15% CAGR (Aggressive equity) | ~24 years | ₹8.64 lakh | ₹91.36 lakh |

In every situation, than 85 percent of the ₹1 crore amount comes from something called compounding, not from the money you put in every month. This is the fact of investing for a long time. You do not save ₹1 crore by putting in money. The ₹1 crore comes from compounding. The ₹100 you put in every day is what gets everything started.

To figure out how long it will take you to have ₹1 crore, based on what you think you will get back you can use our SIP calculator. You just need to set the amount you want to ₹1,00,00,000, which’s ₹1 crore.

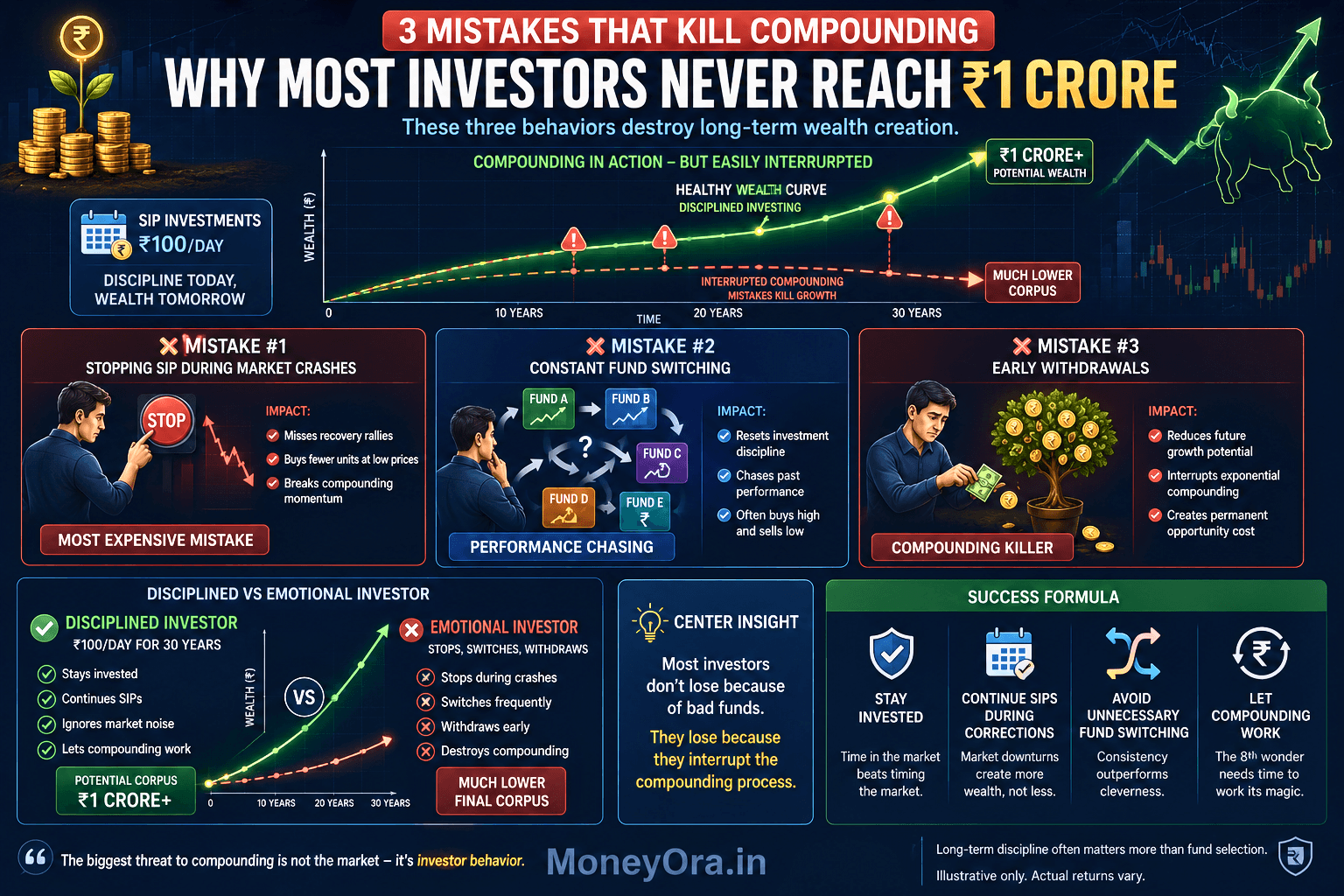

3 Investor Mistakes That Silently Destroy the ₹100 Per Day Investment Plan

Mistake 1: Stopping the Systematic Investment Plan During a Market Crash

This is the mistake people make when it comes to investing. When the market falls by 20 to 30 percent like it did in March 2020 people get scared. Stop their Systematic Investment Plan. This is the time to stop investing

When the market is down your money can buy units at a lower price. For example if you invest ₹3,000 every month you will get units when the price is low. Let us say the price is ₹30 per unit you will get 100 units for ₹3,000.. If the price falls to ₹20 you will get 150 units for the same ₹3,000. That is 50 units for the same amount of money.. When the market goes back up those extra units will give you more returns.

There was an investor who stopped investing 100 per day investment for 6 months during the 2020 market crash. This person missed a chance to invest and grow their money. After 20 years this person had around ₹4 to ₹5 lakh less than someone who kept investing every month.

Mistake 2: Switching Mutual Funds Often

Every time you switch from one mutual fund to another you have to sell your units and buy new ones. You might also have to pay tax on your gains.. You have to start the clock again for your investment. If you switch funds 4 or 5 times in 30 years you will not get the benefit of compounding. Studies have shown that when people switch funds often they get lower returns than the fund itself. This can cost you around 1 to 2 percent per year.

If you invest 100 per day investment for 30 years and get 1 percent returns per year you will have around ₹25 to ₹35 lakh less at the end. So it is better to choose a mutual fund and stick with it. Check on it once a year. Do not switch to a different fund just because it has done well recently.

Mistake 3: Withdrawing Money Before 10 Years

The way your money grows over time is like a curve. For the 10 years it might not seem like much. Let us say you invest ₹3,000 every month for 10 years and get a 12 percent return. After 10 years you will have around ₹6.99 lakh, which’s not much more than the ₹3.60 lakh you invested. People might think it is not worth continuing to invest.

The magic happens after 15 years. From year 10 to year 20 your money will more than quadruple.. From year 20, to year 30 it will triple again. If you take out your money after 10 years to buy something you want you will miss out on the growth that is about to happen.

Pro Tip: Treat your Systematic Investment Plan like your Employee Provident Fund. Do not think about touching it. Do not check on it every day. Use MoneyOras SWP calculator to plan when you can take out money from your investment. Only after you have reached your goal.

Day 1 Action Checklist: Start Your ₹100 Per Day Investment in 15 Minutes

The best part of this article is this section. It’s not because its complicated. It’s because its simple and straightforward. Many people read about investing. Never actually start. They get excited feel motivated. Then they move on to something else.

Here’s how to avoid that. Do it today, not tomorrow.

- Check your KYC status— Visit the AMFI website or any mutual fund app. If your PAN and Aadhaar are linked and your KYC is active, you can invest today. If not, complete e-KYC through Digilocker in 10 minutes.

- Open a direct mutual fund account— Use MF Central (mfcentral.com), Groww, Zerodha Coin, or Paytm Money. Direct plans have lower expense ratios than regular plans — that 0.5–1% difference compounds into lakhs over 30 years.

- Choose ONE fund to start— For most beginners: Nifty 50 Index Fund (any AMC — UTI, SBI, HDFC, Nippon). Low cost, broad diversification, no fund manager risk. Do not overthink this step.

- Set up a Monthly SIP of ₹3,000 or a Daily SIP of ₹100— Choose a date just after your salary credit (3rd or 5th of the month) to ensure your account has sufficient balance for the auto-debit.

- Set up auto-debit (e-mandate)— This removes the need to remember. Missing SIPs because you forgot is a common problem. Auto-debit eliminates it.

- Set a 10-year “Do Not Touch” reminder— Literally put a reminder in your calendar for the date 10 years from now. Your only job before that date is to make sure the SIP does not stop.

- Run your projection on MoneyOra’s SIP calculator— Verify your expected corpus at 12% and 15% return to build conviction. Seeing the number makes it real. It makes missing the SIP feel expensive.

That’s it. Seven steps, 15 minutes and your ₹100 per day investment is up and running. The hardest part is not choosing the fund. The hardest part is actually starting. Investors who build wealth are not smarter, than you. They just. Kept going.

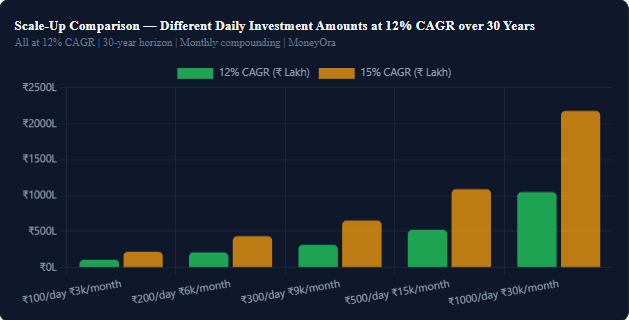

What If You Scale Up? ₹200, ₹300, ₹500 Per Day — The Numbers

| Daily Investment | Monthly Amount | Total Invested (30Y) | Corpus at 12% | Corpus at 15% |

|---|---|---|---|---|

| ₹100/day | ₹3,000 | ₹10.80 lakh | ₹1.05 crore | ₹2.18 crore |

| ₹200/day | ₹6,000 | ₹21.60 lakh | ₹2.10 crore | ₹4.36 crore |

| ₹300/day | ₹9,000 | ₹32.40 lakh | ₹3.15 crore | ₹6.54 crore |

| ₹500/day | ₹15,000 | ₹54.00 lakh | ₹5.25 crore | ₹10.9 crore |

| ₹1,000/day | ₹30,000 | ₹1.08 crore | ₹10.5 crore | ₹21.8 crore |

The relationship is linear with the investment amount but exponential with time. If you can increase your 100 per day investment by ₹50 every year as your income grows — a step-up SIP — the final corpus grows even faster. Use the SIP calculator with a step-up percentage to model this.

If your employer offers EPF, check your EPF calculator to see how your provident fund contributions are compounding alongside your voluntary SIP — your total retirement wealth is both together, not one or the other.

For those with NPS (National Pension System), use the NPS calculator to project your Tier-1 corpus alongside a mutual fund SIP for a complete retirement picture.

Related Stock Market Tools for Advanced Investors

Once your 100 per day investment in mutual funds is running on autopilot, you may want to explore direct equity investing alongside it. For that, MoneyOra’s stock tools will help:

- Stock Return Calculator — Track your actual returns from any direct stock investment

- Dividend Calculator — Estimate dividend income from equity holdings

- PE Ratio Calculator — Evaluate stock valuations before investing

- Stock Average Calculator — Track average cost across multiple stock purchases

Conclusion: Your ₹100 Per Day Investment Is Worth More Than You Think

100 per day investment is not a serious investment plan, most people think.

It is “not enough to make a difference.” But the math says otherwise consistently and decisively.

At 12% CAGR over 30 years, that ₹100 per day investment becomes ₹1.05 crore.

You invested ₹10.80 lakh. The remaining ₹94 lakh came from time and compounding two things that are entirely free and available to everyone equally.

The wealthy do not have a monopoly on compounding. They just start earlier and do not stop.

The difference between the person who builds

₹1 crore from 100 per day investment and the person who does not is not income.

It is not intelligence. It is not timing the market right. It is simply this:

one of them started, set up an auto-debit, and left it alone for 30 years.

The 100 per day investment challenge does not require a financial advisor,

a sophisticated portfolio, or market timing skills.

It requires one afternoon to set it up and one commitment to not touch it.

If you are still reading this without having started, 100 per day investment

now is the moment. Not next month after your next salary. 100 per day investment

Not after you have done more research. Now.

Calculate Your ₹100 Per Day Investment Returns Now

See exactly how much ₹100/day grows over 10, 20, and 30 years with different return assumptions. Model the crorepati timeline with your own numbers.

Use the free calculator now on MoneyOra.in — also explore our lumpsum calculator, PPF calculator, FD calculator, and CAGR calculator to build your complete investment plan.

Disclaimer: All return projections are illustrative based on historical market CAGR. Mutual fund investments are subject to market risk. Past performance does not guarantee future results. Please read all scheme-related documents carefully before investing.

Frequently Asked Questions About ₹100 Per Day Investment

What is the return on a ₹100 per day investment in India?

A ₹100 per day investment which’s ₹3,000 a month grows to around ₹6.99 lakh in 10 years ₹29.96 lakh in 20 years and ₹1.05 crore in 30 years at 12 percent returns. Your total investment over 30 years is ₹10.80 lakh. The remaining ₹94+ lakh comes from the power of compounding. At 15 percent returns your 30-year investment corpus crosses ₹2.18 crore. You can use a SIP calculator to see how your investment will grow.

Can ₹100 per day investment make me a crorepati?

Yes it can. At 12 percent returns a ₹100 per day investment takes around 29-30 years to cross ₹1 crore. At 15 percent it takes 24-25 years. If you start investing at 25 you can have a ₹1 crore+ corpus by retirement. The key is to keep investing during market crashes.

Which is better for ₹100 per day investment. SIP, PPF or FD?

For long-term wealth, which’s 15+ years equity SIP in an index fund gives you the highest corpus, which is ₹1+ crore in 30 years. PPF is best for those who do not like taking risks and want tax- returns, which is ₹37.5 lakh in 30 years. FD gives returns to PPF but the interest is taxed. A savings account is not an option as it loses to inflation.

How does daily ₹100 SIP work in India?

A daily ₹100 SIP deducts ₹100 from your bank account every trading day. Invests it into a mutual fund. You benefit from rupee cost averaging. Many platforms offer SIP from ₹100. You can set it up with auto-debit. It runs without any manual action.

What happens if I miss 30 days of my ₹100 per day investment?

Missing one month of investment costs around ₹25,000-₹30,000 in corpus due to lost compounding. Consistently missing one month per year could reduce your corpus by ₹5-7 lakh. This is why auto-debit is critical.

Is ₹100 per day investment enough for retirement?

It depends on when you start and what lifestyle you expect. Starting at 25 with ₹100/day at 12 percent returns gives around ₹1.05 crore by age 55. For a retirement you would need ₹3-5 crore. The ₹100 per day investment is a start but you should scale it up as your income grows. Use our SWP calculator to plan retirement withdrawals from your corpus.

How tax do I pay on SIP returns?

Equity mutual fund SIP returns are taxed. Gains from units held than 12 months are taxed at 20 percent. Gains from units held 12+ months are taxed at 12.5 percent on gains exceeding ₹1.25 lakh, per year. Always check the Income Tax India website for the latest rates.

Pingback: SIP vs FD During Market Crashes: Which Performs Better? (2026) - MoneyOra