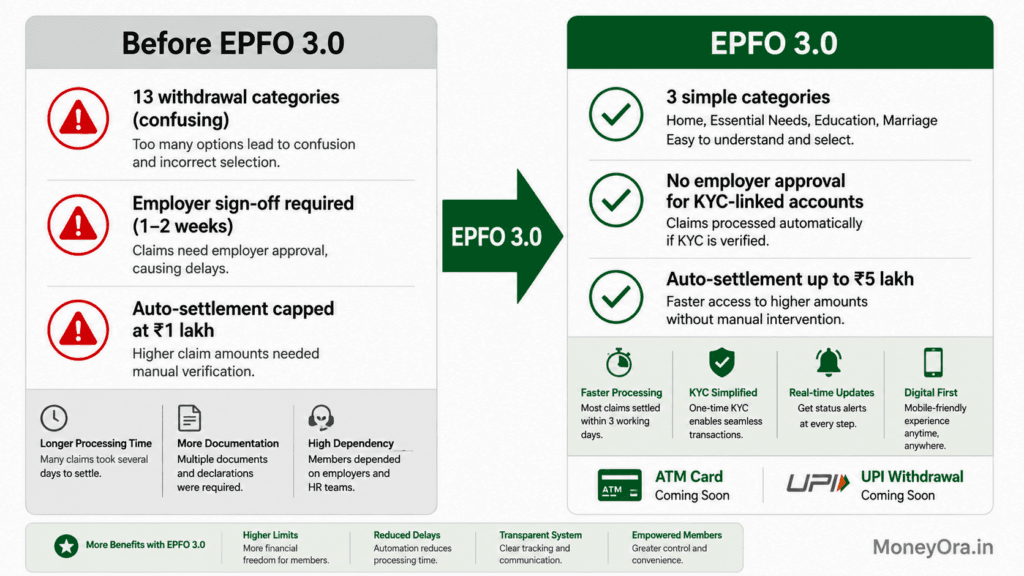

For most of the past seven decades, withdrawing money from your EPF account felt like applying for a government job. Multiple forms, employer sign-offs, 13 separate categories with different eligibility rules, and a waiting period that stretched from days to weeks. EPFO 3.0 is the most significant overhaul of India’s provident fund system since its founding in 1952 — and it changes almost everything about how 30 crore members access their savings.

The Central Board of Trustees formally approved EPFO 3.0 at its 238th meeting on October 13, 2026, chaired by Union Minister Dr. Mansukh Mandaviya. The rollout is happening in phases. Some features are already live. The ATM card and UPI withdrawal features are in final testing as of June 2026, with clearance expected shortly. This guide covers every change — what’s live, what’s coming, and one thing most other guides won’t tell you about why easy access to PF could actually hurt some members’ retirement outcomes.

Run your numbers using MoneyOra’s free EPF Calculator to understand what your current balance becomes by retirement — and what repeated partial withdrawals cost you over time.

Key Takeaways

- EPFO 3.0 was approved on October 13, 2026. ATM card and UPI PF withdrawals are in testing as of June 2026 — not yet live for all members.

- Auto-settlement limit raised from ₹1 lakh to ₹5 lakh — 95% of all advance claims now settle automatically without any human intervention.

- The old 13 withdrawal categories have been merged into 3: Essential Needs, Housing, and Special Circumstances.

- Employer attestation is eliminated for most KYC-complete, Aadhaar-linked accounts — a change that removes the single biggest friction point in PF withdrawals.

- Form 121 (effective April 1, 2026) has replaced Forms 15G and 15H for TDS declarations on PF withdrawals — submit it before claiming if your income is below the taxable threshold.

- A mandatory 25% balance floor applies to all partial withdrawals during active service — this protects your retirement corpus but limits emergency access.

What Is EPFO 3.0 and Why Does It Matter?

Quick answer: EPFO 3.0 is a cloud-based digital upgrade to India’s provident fund system that enables ATM card and UPI-based PF withdrawals, auto-settles claims up to ₹5 lakh without employer involvement, merges 13 withdrawal categories into 3, and eliminates employer attestation for most members. It serves 30 crore EPF members.

The existing system wasn’t broken — it just hadn’t kept pace with how people expect to handle money in 2026. You can transfer ₹10,000 via UPI in three seconds, but accessing your own provident fund savings could take two to three weeks. That gap between what digital India expects and what EPFO could deliver is precisely what EPFO 3.0 addresses.

According to the EPFO, the organisation settled 8.31 crore claims in FY 2025-26 — a 38% increase from 6.01 crore the previous year. That volume, on ageing backend infrastructure, was creating delays. The cloud-based platform under EPFO 3.0 is built to handle that scale and beyond.

Think of EPFO 3.0 less as a single product launch and more as an ongoing modernisation — some features are already active (auto-settlement at ₹5 lakh, CPPS for pensioners, no employer attestation for eligible accounts), others are in final rollout (ATM card, UPI withdrawal), and some are still being defined.

6 Key EPFO 3.0 Changes Every Member Must Know

| Feature | Before EPFO 3.0 | After EPFO 3.0 |

|---|---|---|

| Withdrawal method | Online portal + bank transfer (7–15 days) | Portal + UPI + ATM card (hours to 3 days) |

| Auto-settlement limit | ₹1 lakh | ₹5 lakh |

| Employer attestation | Required for most claims | Eliminated for Aadhaar-linked KYC-complete accounts |

| Withdrawal categories | 13 (complex, confusing) | 3 (Essential, Housing, Special) |

| Pension credit | Required Pension Payment Order (PPO), specific bank | CPPS via NPCI — any bank account, no PPO needed |

| TDS declaration form | Forms 15G / 15H | Form 121 (from April 1, 2026) |

| Detail correction | Office visit for most changes | Online via OTP for name, DOB, mobile updates |

The single most important change

Of all the EPFO 3.0 changes, the most practically impactful isn’t the ATM card (which gets the most coverage) — it’s the auto-settlement limit increase from ₹1 lakh to ₹5 lakh. This means 95% of all advance PF claims now settle automatically without a single human reviewing them. Processing time drops from a week or more to hours or a few business days. That one change alone resolves the biggest real-world frustration for most members.

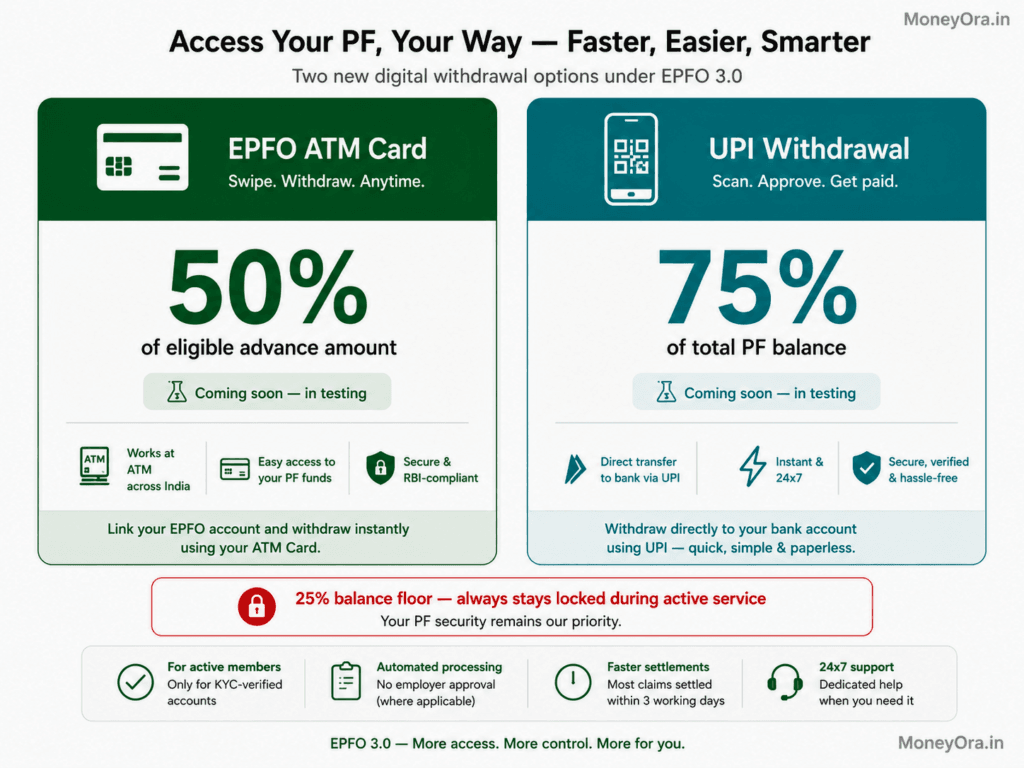

Via ATM: up to 50% of eligible advance. Via UPI: up to 75% of total PF balance. A mandatory 25% floor stays locked during active service

ATM Card and UPI Withdrawal — How It Works Under EPFO 3.0

This is the feature most people are waiting for. Here’s the honest status as of late June 2026: testing is complete, regulatory clearances are pending, and the launch is expected shortly. Don’t plan a withdrawal around these features until an official date is announced on the EPFO portal.

When they do go live, here’s how each works:

ATM card withdrawal

- EPFO issues a dedicated PF withdrawal card — similar to a bank debit card, linked to your UAN rather than a bank account

- Withdraw up to 50% of the eligible advance amount from any ATM

- The universal 25% floor rule still applies — at least 25% of your total PF balance must stay in the account at all times during service

- Cards are being rolled out in phases — check your EPFO portal or UMANG app for availability on your account

UPI withdrawal

- Log in to the EPFO member portal or a UPI-enabled app when the feature goes live

- Aadhaar OTP authentication required — your Aadhaar-registered mobile number must be active

- The system shows your “Withdrawable Balance” versus your “Locked Retirement Balance” before you proceed

- Enter the amount, provide your UPI ID — money is pushed directly to your linked bank account

- Withdraw up to 75% of your total PF balance via UPI (higher than the 50% ATM limit)

- Works with PhonePe, Google Pay, Paytm, and other UPI-enabled apps

What changes most for these withdrawal methods

The old system required you to visit the EPFO portal, submit a claim, wait for employer verification, then wait again for EPFO processing. The new ATM and UPI flows eliminate every step after authentication. For genuine emergencies — medical, sudden financial need — that difference in speed is real and significant.

₹5 Lakh Auto-Settlement — What Changes Under EPFO 3.0

This feature is already live. And it’s the most impactful change under EPFO 3.0 for day-to-day members.

Under the old system, auto-settlement was capped at ₹1 lakh. Any claim above that went through manual processing — meaning a human reviewer at EPFO had to verify and approve it. Under EPFO 3.0, claims up to ₹5 lakh are settled automatically by the system, with no human intervention, provided your UAN is fully KYC-compliant.

The numbers are striking. In FY 2024-25, EPFO processed 2.34 crore advance claims through auto-settlement alone — a 161% jump over the previous year. In just the first 2.5 months of FY 2025-26, 76.52 lakh claims were auto-settled, making up 70% of all advance claims. With the limit now at ₹5 lakh, that percentage will be higher still.

What auto-settlement means in practice

| Claim Amount | Processing Path | Typical Timeline |

|---|---|---|

| Up to ₹5 lakh (KYC complete) | Auto-settled — no human review | Hours to 3 business days |

| Above ₹5 lakh | Manual review by EPFO | 7–10 working days |

| KYC incomplete (any amount) | Cannot access auto-settlement | Blocked until KYC fixed |

The key condition: your UAN must have Aadhaar, PAN, and bank account all linked and showing “Digitally Approved” in the EPFO portal. Anything pending blocks auto-settlement immediately — and blocks ATM/UPI access once those features go live.

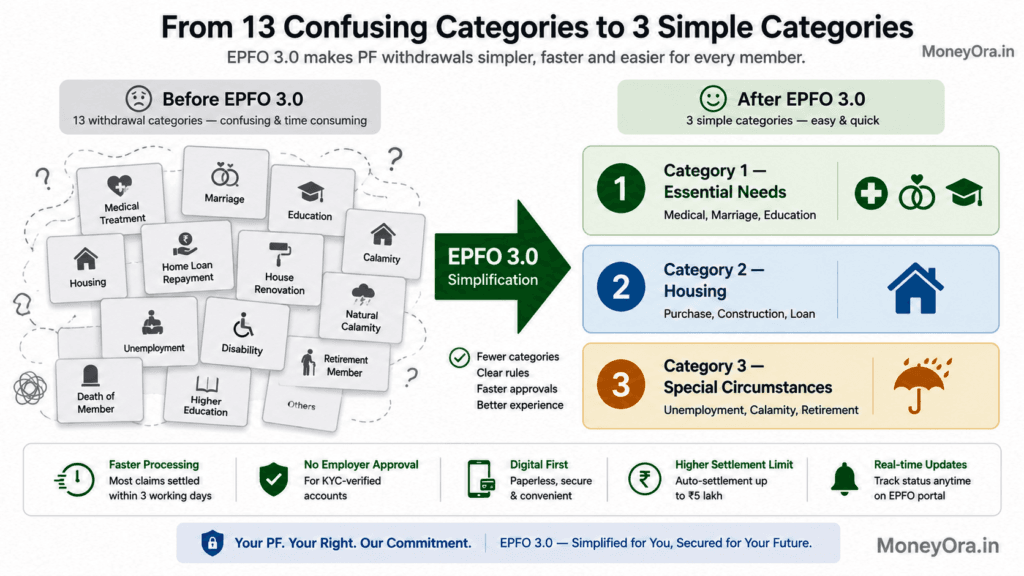

Thirteen confusing PF withdrawal sub-categories simplified into three clear groups under EPFO 3.0 — reducing the most common cause of valid claim rejections

13 Categories Merged Into 3 — The New Withdrawal Framework

This change is more significant than it sounds. The old 13-category system was one of the main reasons valid PF claims got rejected — members selected the wrong category, didn’t meet that specific category’s service requirement, or didn’t know which form applied. Under EPFO 3.0, that entire confusion disappears.

| Category | Covers | Minimum Service | Max Withdrawal |

|---|---|---|---|

| Category 1 Essential Needs | Medical emergencies Marriage (up to 5 times) Education (up to 10 times) | Medical: Nil Marriage/Education: 7 years | 50% of employee share (Medical: 6 months basic wages or full employee share) |

| Category 2 Housing | Property purchase Home construction Home loan repayment Renovation | 5 years | Up to 90% of balance for purchase/construction |

| Category 3 Special Circumstances | Unemployment Natural calamity Retirement at 58 Permanent disability | Nil (for unemployment and calamity) | 75% after 1 month jobless 100% after 2 months or retirement |

The big change: employer’s contribution is now included

Under the old rules, partial withdrawals were typically limited to the employee’s own contribution plus interest. Under EPFO 3.0, the withdrawable corpus now includes the employer’s contribution as well. This substantially increases how much members can actually access — 75% of total balance (employee + employer + interest) is meaningfully larger than 75% of only the employee’s share.

What the 12-month uniform service rule means

Previously, different withdrawal reasons had different service requirements — 5 years for housing, 7 years for marriage and education, varying rules across the 13 categories. A uniform 12-month minimum service period now applies to most partial withdrawal categories (medical remains an exception). This is a significant simplification for early-career employees who previously couldn’t access PF for many life events.

No Employer Approval — Who Qualifies and How Under EPFO 3.0

This was the single biggest pain point in PF withdrawal before EPFO 3.0. Your money, locked behind your employer’s willingness to click “approve” in a portal. If you’d left on bad terms, if the company had restructured, if HR was simply slow — your claim sat in limbo. Sometimes for months.

Under EPFO 3.0, employer attestation is removed for members who meet these conditions:

- UAN is Aadhaar-linked and Aadhaar-seeded

- KYC shows “Digitally Approved” for Aadhaar, PAN, and bank account

- Either: both old and new PF accounts link to the same UAN, or different UANs both link to the same Aadhaar

For claims up to ₹5 lakh that meet these conditions, the process is entirely self-service. You authenticate with Aadhaar OTP, submit the claim, and auto-settlement takes over. No employer involved, no waiting for HR.

For claims above ₹5 lakh, or where KYC is incomplete, the old employer-attestation path still applies for some cases. This is the category of member who most urgently needs to fix KYC now, before they need the money.

What EPFO 3.0 Means for Your Pension — CPPS and EPS Changes

Centralised Pension Payment System (CPPS) — live since January 2025

This one’s already active and solves a problem pensioners have faced for decades. Under the old system, EPS pension could only be credited to a specific bank tied to the Pension Payment Order (PPO). Pensioners had to maintain an account at that bank even if they didn’t want to — and relocating to another city could turn pension access into a logistical problem.

CPPS changed this. Pensions are now credited directly via NPCI to any bank account — any bank, any branch, anywhere in India. The PPO dependency is gone. For the roughly 73 lakh EPS pensioners, this alone is a meaningful quality-of-life improvement.

Digital life certificates from home

Pensioners previously had to submit a Jeevan Pramaan (life certificate) in person at a bank or EPFO office every year — a process that was genuinely difficult for older or unwell pensioners. Under EPFO 3.0, pensioners can submit Jeevan Pramaan via India Post Payments Bank (IPPB) from their doorstep. EPFO bears the ₹50 service fee, making it free for the pensioner.

EPS waiting period extended — the change most guides miss

One reform that gets far less coverage than the ATM card: under EPFO 3.0, the waiting period for EPS pension eligibility at unemployment has been extended from 2 months to 36 months. This means you need to be unemployed for 3 years before accessing pension benefits — a significant tightening designed to discourage premature pension draws and preserve EPS corpus.

This affects anyone who switches jobs and remains between employment for extended periods. If you’re planning a career break or expect a gap between jobs, factor this new 36-month EPS waiting period into your financial plan.

Tax Rules and Form 121 — What’s the Same, What Changed Under EPFO 3.0

Good news first: the core PF tax rules are unchanged under EPFO 3.0. What changed is the declaration process for avoiding TDS.

| Scenario | Tax Treatment | TDS |

|---|---|---|

| Withdrawal after 5 years of continuous service | Fully tax-free | Nil |

| Withdrawal before 5 years — amount below ₹50,000 | Taxable (add to income) | No TDS |

| Withdrawal before 5 years — ≥ ₹50,000 (PAN linked) | Taxable — entire amount | 10% TDS |

| Withdrawal before 5 years — PAN not linked | Taxable at max rate | 30% TDS |

| Transfer (not withdrawal) | Not a taxable event | Zero |

Form 121 — what it replaces and why it matters

Effective April 1, 2026, Form 121 under the new Income Tax Act, 2025, has replaced Forms 15G and 15H for TDS declarations on PF withdrawals. If you’re withdrawing before 5 years of service and your total income is below the taxable threshold, Form 121 lets you declare zero tax liability and avoid TDS deduction upfront.

The submission process is now integrated into the online claims flow — you upload Form 121 at Step 7 of the portal process, alongside your claim. You don’t need to submit it separately to your employer or EPFO office. Members who submitted old Forms 15G or 15H after April 1, 2026, won’t be immediately rejected, but EPFO may follow up requesting Form 121.

Check your tax liability first using the Income Tax Department portal. If you’re in any doubt about whether to submit Form 121, consult a CA before claiming.

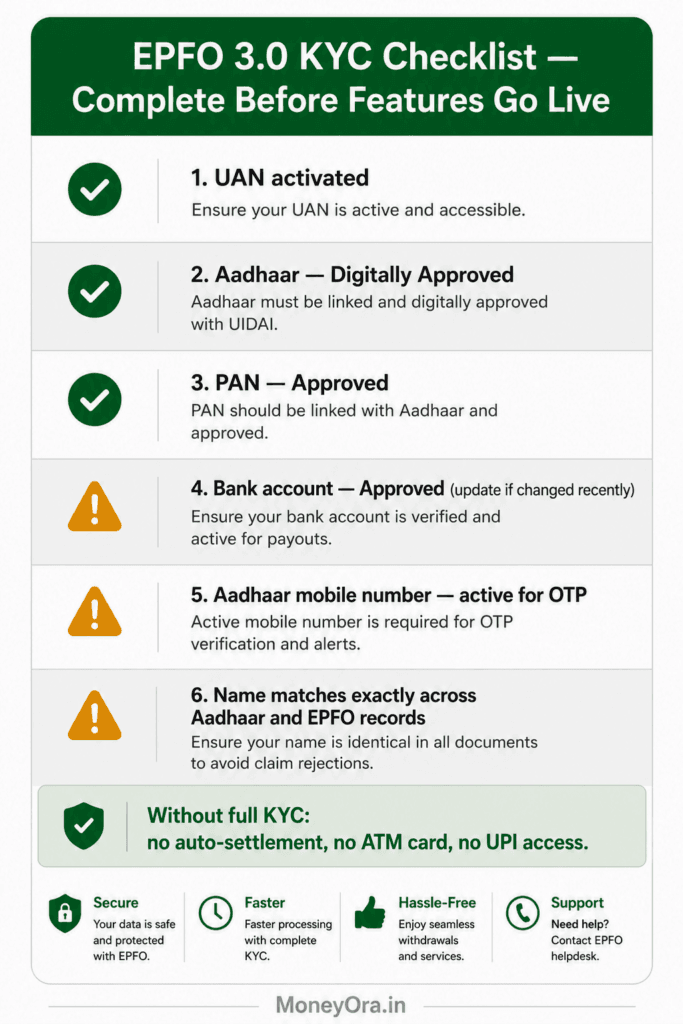

KYC Checklist — Get Ready Before EPFO 3.0 Features Go Live

Every benefit under EPFO 3.0 — auto-settlement, no-employer-approval withdrawal, UPI access, ATM card — requires KYC to be complete and showing “Digitally Approved.” This isn’t a suggestion. Without full KYC, none of these features work.

Check each item in the EPFO portal under Manage → KYC:

| KYC Item | Required Status | If “Pending” — What to Do |

|---|---|---|

| Aadhaar | Digitally Approved | Contact HR to approve via employer portal, or use UMANG face auth |

| PAN | Approved | Add via Member Portal and ask HR to approve |

| Bank account (with IFSC) | Approved | Update via portal if bank has changed; wait 48 hrs after update before claiming |

| UAN activated | Active | Activate at epfindia.gov.in with UAN + mobile |

| Aadhaar-registered mobile | Active and receiving OTP | Update mobile in UIDAI records; or use UMANG face authentication |

| Name match: Aadhaar = EPFO records | Exact match | Raise correction via Profile → Change Member Details with documents |

One thing most guides skip: wait 48 hours after any KYC update before filing a claim. EPFO’s backend sync doesn’t always reflect changes immediately, and filing too soon after an update can cause an unnecessary rejection.

Also — submit Form 121 annually in April if your income is below the taxable threshold. Having it ready before you need to make a claim avoids a last-minute scramble during an emergency.

Risks Most EPFO 3.0 Guides Don’t Cover

1. The retirement depletion risk

This is the big one. Easier access to PF is genuinely useful in a medical emergency or sudden job loss. But the same frictionless access that helps in a crisis can erode retirement savings if used casually — a wedding fund, a travel plan, a gadget upgrade. The 25% floor is a partial safeguard, not a complete one.

Consider: if you withdraw 75% of your PF balance three times over a 30-year career, your retirement corpus looks very different than if you never touched it. A ₹5 lakh withdrawal at age 35 doesn’t just cost ₹5 lakh — it costs every rupee that ₹5 lakh would have compounded to at retirement. At 8.25% over 23 years, that’s roughly ₹36 lakh.

Use MoneyOra’s EPF Calculator to see what your current balance compounds to by retirement before deciding whether to withdraw.

2. ATM card fraud risk

A dedicated PF ATM card introduces the same risks as any debit card — skimming, PIN theft, phishing. Most people are reasonably careful with bank cards because of years of habit. The EPFO card will be new, and members in rural areas or lower digital literacy contexts may be more vulnerable in the early rollout period. Treat it exactly like a bank card: PIN confidential, enable SMS alerts, report loss immediately.

3. UPI and ATM features aren’t live yet (June 2026)

As of late June 2026, the UPI and ATM withdrawal features have completed testing but are awaiting final regulatory clearances. Don’t plan an urgent withdrawal around these features until an official launch date is confirmed at epfindia.gov.in. The auto-settlement increase to ₹5 lakh and the no-employer-attestation pathway are fully live — use those in the interim.

4. EPS pension waiting period extension

The extension of the EPS unemployment waiting period from 2 months to 36 months is largely unreported in competitor articles. If you’re between jobs and were counting on EPS pension access during that gap, the rules have changed significantly. Plan your financial bridge accordingly.

5. Old claims in process aren’t affected

If you’ve already submitted a PF withdrawal claim under the old system and it’s in process, EPFO 3.0 doesn’t retroactively accelerate it. Check your claim status via Track Claim Status on the portal. If it’s stuck, raise a grievance at epfigms.gov.in rather than submitting a new claim.

MoneyOra Analysis — The Real Question EPFO 3.0 Raises

Most coverage of EPFO 3.0 frames this as a purely positive development. Faster access, less paperwork, ATM card, UPI. All true. All useful. But there’s a tension worth naming.

EPF is designed as a retirement instrument. Its power comes from the fact that money stays invested over a 30–35 year working career, compounding at 8.25% per annum without tax on interest or withdrawal after 5 years. That’s an extraordinarily good deal — better than most fixed income instruments available in India after accounting for taxation.

Making that money easier to access is a genuine benefit in crises. But it also turns EPF into something that competes with your spending impulses in normal times. The old friction — the 15-day wait, the employer approval, the form confusion — wasn’t just bureaucracy. Part of it was a behavioural lock that prevented casual, non-emergency withdrawals.

Here’s the compounding math on what easy access costs over a career:

| Scenario | Withdrawals Made | Est. Retirement Corpus at 58 |

|---|---|---|

| Never withdrew — always transferred at job change | ₹0 | ~₹1.8–2.2 cr (₹5,000/month at ₹40,000 basic) |

| Withdrew once at age 32 (₹3 lakh) | ₹3 lakh | ~₹1.5–1.9 cr (₹27–30 lakh less) |

| Withdrew 75% three times across career | ~₹15–20 lakh | ~₹45–65 lakh (significantly below potential) |

These are illustrative projections assuming consistent contributions. The actual impact depends on salary, basic pay percentage, and withdrawal timing.

The MoneyOra take: Use EPFO 3.0‘s new access features for what they’re designed for — genuine emergencies, housing needs where EPF advances make financial sense, and the auto-settlement speed that makes normal claims less of a headache. Don’t treat the ATM card like a bank account. The retirement corpus you’re building is largely invisible until you need it — and by then, what you withdrew in your 30s will feel very expensive.

EPFO 3.0 — What to Do Right Now

EPFO 3.0 is a genuine improvement. The auto-settlement increase to ₹5 lakh, no-employer-attestation for eligible members, the 3-category simplification, and the incoming ATM and UPI features all reduce real friction for 30 crore members. The CPPS for pensioners and digital life certificates remove decades-old pain points.

What to do before the ATM and UPI features go live:

- Check KYC now — log in to the EPFO portal, go to Manage → KYC, and confirm Aadhaar, PAN, and bank all show “Digitally Approved”

- Verify your passbook — confirm your employer is crediting contributions correctly; check monthly

- Submit Form 121 in advance if your income is below the taxable threshold — have it ready before you need to claim

- Never withdraw at job change — transfer your EPF balance. The compounding you preserve is worth far more than the immediate cash

- Calculate before you touch it — see what your current EPF balance becomes at retirement before making any withdrawal decision

See What Your EPF Balance Becomes at Retirement

EPF • PPF • NPS • SIP • EMI — all calculators free, no login required.

Use the free calculator now on MoneyOra.in →Related MoneyOra Tools and Articles

- EPF Calculator — Project what your PF balance becomes at 8.25% compounding by retirement

- PPF Calculator — Compare EPF growth against PPF at 7.1%

- NPS Calculator — Model your total retirement corpus including NPS Tier 1

- SIP Calculator — Build equity returns alongside your guaranteed EPF base

- FD Calculator — Compare EPF’s 8.25% against FD returns after tax

- Lumpsum Calculator — See how a one-time PF balance grows over remaining years

- Financial Calculator India — Full MoneyOra calculator directory

- EPF Transfer Guide — Step-by-step process to transfer PF at job change

- EPF vs PPF vs NPS — Which retirement instrument should freshers prioritise?

- Financial Mistakes Freshers Make — 15 money mistakes that cost lakhs in compounding

Frequently Asked Questions — EPFO 3.0

What is EPFO 3.0?

EPFO 3.0 is the Employees’ Provident Fund Organisation’s major digital overhaul approved by the Central Board of Trustees on October 13, 2026. It raises auto-settlement limits to ₹5 lakh, enables ATM card and UPI-based PF withdrawals, merges 13 withdrawal categories into 3, and removes employer attestation requirements for most KYC-complete members. It covers 30 crore EPF members across India.

Is EPFO 3.0 live yet — can I withdraw PF via UPI or ATM today?

Partially. The auto-settlement increase to ₹5 lakh and the no-employer-attestation pathway are already live. The ATM card and UPI withdrawal features completed testing as of June 2026 but are awaiting final regulatory clearances. Check epfindia.gov.in or the UMANG app for the official launch date before planning a digital withdrawal via these channels.

How much PF can I withdraw via ATM under EPFO 3.0?

Via the EPFO ATM card: up to 50% of the eligible advance amount per transaction. Via UPI: up to 75% of your total PF balance. A mandatory 25% floor applies to all partial withdrawals during active service — at least 25% of your total balance (employee + employer + interest) must remain in the account at all times.

What is the auto-settlement limit under EPFO 3.0?

₹5 lakh — raised from the previous ₹1 lakh limit. Claims up to ₹5 lakh from fully KYC-compliant accounts are now settled automatically without any human intervention or employer approval. Auto-settled claims typically credit within hours to 3 business days. Claims above ₹5 lakh still follow the manual processing path and take 7–10 working days.

Do I need employer approval to withdraw PF under EPFO 3.0?

No, for eligible members. If your UAN is Aadhaar-linked and your KYC shows “Digitally Approved” for Aadhaar, PAN, and bank account, employer attestation is no longer required for claims up to ₹5 lakh. This change, effective since the January 2025 EPFO circular, removes the most common cause of PF withdrawal delays — unresponsive employers.

What is Form 121 and how is it different from Form 15G or 15H?

Form 121 is the unified TDS declaration form introduced under the Income Tax Act, 2025, effective April 1, 2026. It replaces Forms 15G (for below-60 members) and 15H (for senior citizens) with a single form. If you’re withdrawing before 5 years of service and your total income is below the taxable threshold, submit Form 121 online during the claim process to declare zero tax liability and avoid TDS deduction.

What are the 3 new withdrawal categories under EPFO 3.0?

The old 13 categories have been merged into three: Category 1 — Essential Needs (medical, marriage up to 5 times, education up to 10 times); Category 2 — Housing (purchase, construction, home loan repayment, renovation); Category 3 — Special Circumstances (unemployment, natural calamity, retirement at 58, permanent disability). A uniform 12-month minimum service applies to most categories, with medical being an exception.

What is the CPPS under EPFO 3.0?

The Centralised Pension Payment System (CPPS) allows EPS pensions to be credited via NPCI to any bank account in India — eliminating the old requirement for a specific bank account tied to the Pension Payment Order (PPO). Active since January 2025, CPPS benefits the roughly 73 lakh EPS pensioners who previously had to maintain accounts at specific banks regardless of their banking preferences.

How does EPFO 3.0 affect my retirement savings if I make partial withdrawals?

Tax rules are unchanged — partial withdrawals for approved purposes remain permissible. But the compounding impact is real. A ₹3 lakh withdrawal at age 32 costs approximately ₹27–30 lakh in retirement corpus (at 8.25% over 26 years). Easier access under EPFO 3.0 makes it more important, not less, to calculate the retirement cost before withdrawing. Use MoneyOra’s free EPF Calculator before deciding.

What is the EPS waiting period under EPFO 3.0 and how does it change?

The EPS (Employee Pension Scheme) waiting period for pension access at unemployment has been extended from 2 months to 36 months under EPFO 3.0 reforms. This means you need to be unemployed for 3 years before accessing pension benefits — a significant change from the old 2-month wait. Plan your financial bridge accordingly if you’re expecting any gap between jobs.

What should I do right now to prepare for EPFO 3.0?

Complete your KYC immediately — check that Aadhaar, PAN, and bank account all show “Digitally Approved” in the EPFO member portal. Verify your EPF passbook to confirm contributions are being deposited correctly. Submit Form 121 in April each year if your income is below the taxable threshold. And never withdraw EPF at job change — always transfer to preserve compounding and 5-year service continuity.

Pingback: EPF Transfer Online 2026: The Best Way to Switch Jobs

Pingback: EPF vs PPF vs NPS: Which Is Best for Freshers? (2026)