The EPF transfer process in 2026 is largely automated — but KYC must be clean before you begin

The EPF transfer process in 2026 is largely automated — but KYC must be clean before you begin

Most people treat EPF transfer as something to figure out “later.” Then six months pass, the old employer stops responding, the EPFO portal throws an error, and a casual delay turns into a genuine headache. Between April 2024 and January 2025 alone, the EPFO received over 1.30 crore EPF transfer claims — proof that millions of Indians are switching jobs constantly but handling the EPF piece poorly. EPFO 3.0 auto-transfer and new employer rules

The good news: EPF transfer online in 2026 is faster and simpler than it has ever been. The bad news: a few small errors — a name mismatch, an unlinked Aadhaar, an exit date not updated by your old employer — can freeze the process for weeks. This guide walks you through every step, covers the 2025–2026 rule changes that most guides haven’t caught up to, and shows you exactly why transferring beats withdrawing by a margin most people don’t calculate until it’s too late. Use MoneyOra’s free EPF Calculator to model what your transferred balance will compound to by retirement.

Key Takeaways

- Since April 1, 2024, EPF transfer triggers automatically when your new employer credits the first monthly contribution — no manual Form 13 needed if your UAN is Aadhaar-linked and KYC-complete.

- Since January 15, 2025, employer approval is no longer required for most EPF transfer requests — the biggest process change in years.

- Withdrawing EPF before 5 years of service makes the entire amount fully taxable — and TDS at 10% (or 30% without PAN) is deducted upfront.

- EPF earns 8.25% interest for FY 2024-25 — a rate that continues during transfer. You don’t lose a single day’s interest while the process is underway.

- The most common reason EPF transfers fail isn’t process complexity — it’s a KYC mismatch that takes 30 seconds to fix beforehand.

Why You Must Do EPF Transfer — Not Withdrawal — When Changing Jobs

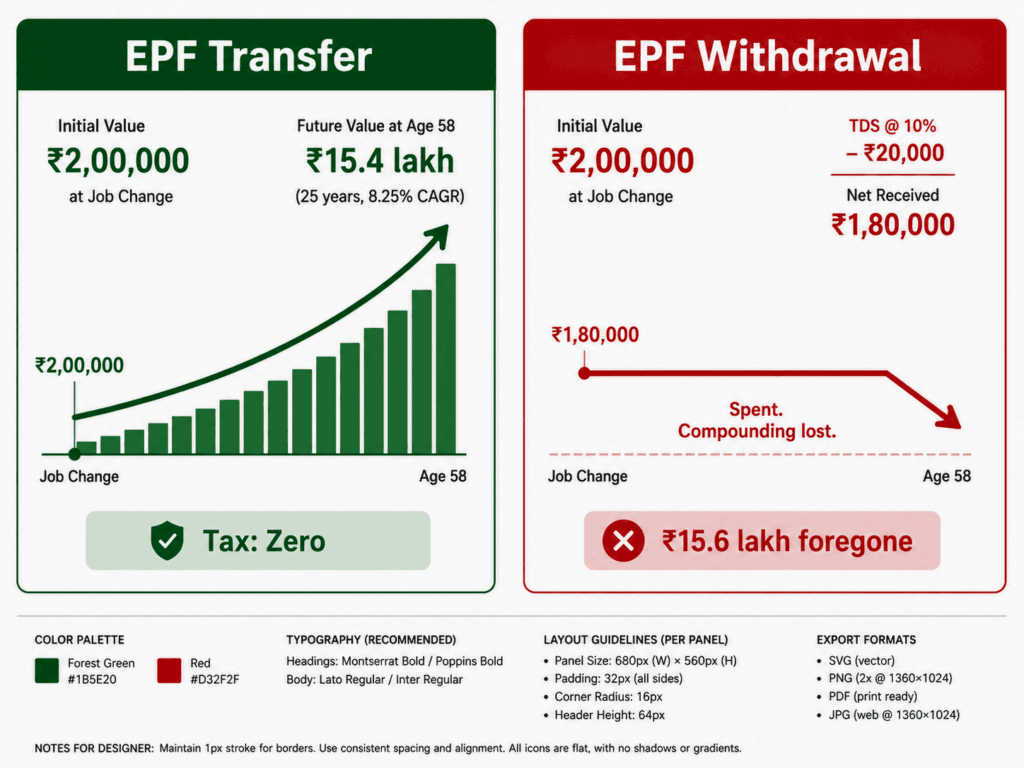

Every year, a large number of employees withdraw their EPF when leaving a job. It feels like the simpler choice. The money lands in your account within a few weeks and you move on. What you don’t see is what that decision costs.

Here’s the honest maths. Say you’ve built ₹2 lakh in your EPF account over three years. You withdraw it at job change. Here’s what actually happens:

| Scenario | At Job Change | At Age 58 (25 years later) |

|---|---|---|

| EPF transfer (compounding at 8.25%) | ₹2,00,000 stays intact | ~₹15.4 lakh |

| Withdrawal (before 5 years — taxable) | ₹2,00,000 − TDS ₹20,000 = ₹1,80,000 | ₹0 — spent |

| What early withdrawal actually costs (compounding foregone + tax) | ~₹15.6 lakh | |

That ₹20,000 TDS hurts in the moment. But the real cost is the ₹15+ lakh of compounding you quietly gave up. This is why every financial adviser says the same thing: do the EPF transfer, not the withdrawal.

Beyond the maths, EPF withdrawal before 5 years of continuous service also resets your service history for EPS pension eligibility. You need 10 years of continuous service to qualify for monthly pension at 58. Every withdrawal interrupts that count. The EPF transfer keeps it intact.

New EPFO Rules in 2025–2026 That Change the EPF Transfer Process

Most online guides are still explaining the old EPF transfer process. These are the rule changes that actually matter right now:

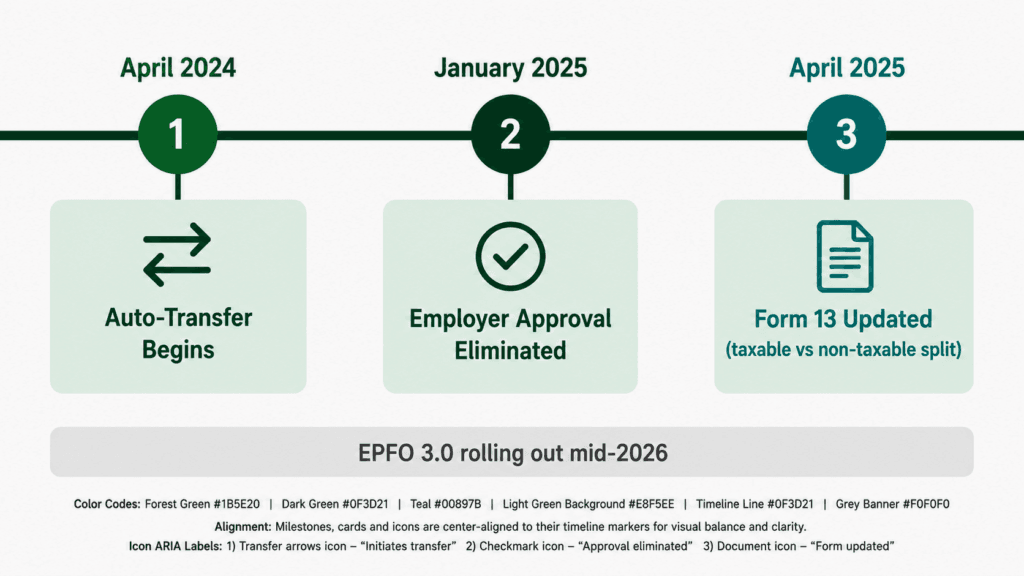

1. Auto-Transfer from April 1, 2024

Since April 1, 2024, EPF transfer happens automatically when your new employer credits your first monthly contribution to the new account — provided your UAN is Aadhaar-linked and fully KYC-compliant. You don’t need to submit Form 13 manually. The auto-trigger fires when the new joining date is updated.

This applies if the automatic transfer isn’t stopped by the member. You do have the option to opt out — but for most people, just letting the auto-transfer run is the cleanest path.

2. Employer Approval Eliminated (January 15, 2025)

EPFO’s January 15, 2025 circular is the biggest change in years. For eligible accounts, employer approval is no longer needed to process an EPF transfer request. The old pain point — waiting for an unresponsive HR team to click “approve” — is largely gone.

This applies when:

- Both PF accounts are linked to the same UAN (allotted on or after October 1, 2017) and the UAN is Aadhaar-linked

- PF accounts belong to different UANs (both allotted after October 2017), but both link to the same Aadhaar

- PF accounts are under the same UAN (allotted before October 2017) and the UAN is Aadhaar-linked with matching name, DOB, and gender

3. Updated Form 13 (April 25, 2025)

EPFO released a revised Form 13 through a circular dated April 25, 2025. The updated form now separates taxable from non-taxable PF components — allowing precise TDS calculation. If you’re submitting Form 13 manually, make sure you’re using the version from the current EPFO portal, not a downloaded copy from 2023.

4. EPFO 3.0 — Faster Everything (Rolling Out Mid-2026)

Under EPFO 3.0, claims up to ₹5 lakh are auto-settled without human intervention — 95% of all PF claims now process this way. UPI withdrawal and EPFO ATM card access are being phased in. For transfers specifically, this means status updates are faster and backend processing delays are reducing significantly.

5. Interest Continues During Transfer

Old rule: EPF interest stopped accruing while a transfer was in progress. New rule: interest continues uninterrupted from old account to new account throughout the transfer period. You don’t lose a rupee of interest while the paperwork moves.

EPF Transfer Prerequisites — Check All These Before You Start

Most EPF transfer rejections aren’t caused by process errors. They’re caused by skipping this checklist. Verify all five items before logging into the EPFO portal:

| Item | Where to Check | Status Needed |

|---|---|---|

| UAN activated | epfindia.gov.in | Active |

| Aadhaar seeded & verified | Manage → KYC on portal | “Digitally Approved” |

| PAN linked | Manage → KYC on portal | “Approved” |

| Bank account linked & verified | Manage → KYC on portal | “Approved” |

| Mobile linked to UAN (for OTP) | Profile → Basic Details | Active & receiving SMS |

| Previous employer’s exit date updated | Check Member ID on portal | Date of Exit entered |

| New employer’s PF account active | Confirm with HR/payslip | Enrolled and active |

The name on your Aadhaar must exactly match the name in the EPFO system. A single character difference — “Suresh Kumar” vs “Suresh K.” — will block the transfer. If your name doesn’t match, fix it first via the EPFO portal under Profile → Change Member Details.

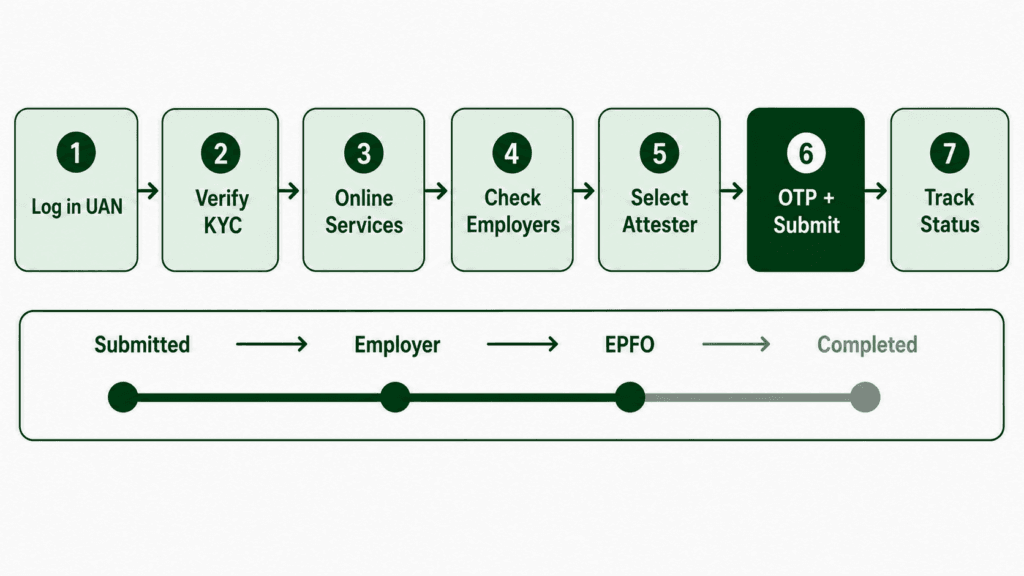

How to Do EPF Transfer Online — Step-by-Step Guide (2026)

Quick answer (40 words): Log in to the EPFO Member Portal with your UAN → go to Online Services → One Member One EPF Account (Transfer Request) → verify details → get OTP → submit. The EPF transfer request goes in without employer approval if KYC is clean.

Here’s the full process:

Step 1 — Log In to the EPFO Unified Portal

Go to unifiedportal-mem.epfindia.gov.in and log in using your UAN and password. If you’ve forgotten your password, click “Forgot Password” — you’ll get a reset link via OTP on your registered mobile.

Once logged in, check the top-right corner — your UAN should show as active. If it shows “inactive,” contact your HR immediately before proceeding.

Step 2 — Verify Your KYC Status

Go to Manage → KYC. You need to see “Digitally Approved” against Aadhaar and your bank account. “Pending” means your employer hasn’t approved the KYC update yet — that will block the EPF transfer request. Follow up with HR to approve the pending KYC before proceeding.

Step 3 — Go to Online Services → EPF Transfer Request

In the top navigation, click Online Services. From the dropdown, select “One Member – One EPF Account (Transfer Request)”. This is the section for initiating your EPF transfer to a new employer.

Step 4 — Check Previous and Current Employer Details

The system will display both your previous employer (Member ID with old PF account) and your current employer (Member ID with new PF account). Verify that both show correctly. If the previous employer’s account doesn’t appear, it may mean your old Member ID isn’t linked to your UAN — contact your old HR to fix this.

Step 5 — Select the Attesting Authority

Under the old process, you had to choose which employer (previous or current) would verify your EPF transfer request. As of January 2025, for eligible accounts, this step is skipped — the system processes without employer attestation. If you still see the employer selection dropdown, choose whichever employer is more likely to respond promptly. Current employer is usually faster.

Step 6 — Get OTP and Submit

Click “Get OTP.” An OTP is sent to your registered mobile number. Enter it and click Submit. You’ll see a Tracking ID on screen — save this immediately. This is how you monitor your EPF transfer status going forward.

Step 7 — Print and Submit Form 13 (If Required)

After submitting online, the portal generates Form 13. Download it, print it, sign it, and submit it to the attesting employer within 10 days of submission. In cases where employer approval has been eliminated (January 2025 rule), this physical submission may not be needed — check the portal confirmation screen for instructions specific to your account.

Step 8 — Monitor and Follow Up

Track your EPF transfer status on the EPFO portal under Online Services → Track Claim Status. The timeline is typically 20 days, though EPFO 3.0 processing is reducing this for many accounts. You’ll also get an SMS when your employer approves the request and when EPFO processes the transfer.

Time this right

Initiate the EPF transfer within 30 days of joining your new employer. The longer you wait, the more likely your old employer’s HR team has changed and verification gets delayed. The auto-transfer system handles this from April 2024 onwards — but if your UAN isn’t KYC-complete, auto-transfer won’t fire and you’ll need the manual process.

Does Auto-Transfer Apply to You? How to Check

Since April 1, 2024, EPFO automatically initiates EPF transfer when the new employer credits the first monthly contribution. The transfer happens in the background — you don’t log in, you don’t fill Form 13, you don’t chase your old employer.

But auto-transfer only works if all of these are true:

- Your UAN is activated and Aadhaar-seeded

- KYC (Aadhaar + PAN + bank) is fully verified and shows “Digitally Approved”

- Your previous employer has updated your Date of Exit on the EPFO portal

- Your new employer has enrolled you in EPFO and credited the first contribution

If any of those four conditions isn’t met, auto-transfer doesn’t fire. You’ll need to initiate the manual EPF transfer process described above.

How to check if auto-transfer happened: Log in to your EPFO account and check your passbook under the current Member ID. If the old balance appears, auto-transfer worked. If only new contributions show, it hasn’t triggered yet — verify each condition above and either fix the blocker or initiate manually.

How to Track Your EPF Transfer Status

There are two ways to track your EPF transfer request:

Method 1 — EPFO Member Portal

- Log in to epfindia.gov.in with your UAN

- Click Online Services → Track Claim Status

- Your EPF transfer claim status will appear with the current stage

The status moves through: Submitted → Approved by Employer → Processed by EPFO → Completed. If it’s stuck at “Approved by Employer” for more than a week, call your employer’s HR or raise a grievance on the portal.

Method 2 — UMANG App

Download the UMANG app (Android/iOS) → search EPFO → log in with UAN → track claim status. The UMANG app also lets you view your EPF passbook in real time and see whether the transferred balance has credited to your new account.

What the Status Messages Mean

| Status | What It Means | Action Needed |

|---|---|---|

| Submitted | Request received by EPFO | Wait |

| Under Process at Employer | Employer is reviewing | Follow up with HR if stuck >7 days |

| Approved by Employer | HR approved; now at EPFO | Wait 5–10 working days |

| Under Process at EPFO | EPFO backend is processing | Wait |

| Transfer Completed | Balance credited to new PF account | Verify passbook to confirm amount |

| Rejected | Request denied — reason given | Fix the stated issue, re-submit |

7 Mistakes That Get EPF Transfers Stuck — and How to Avoid Them

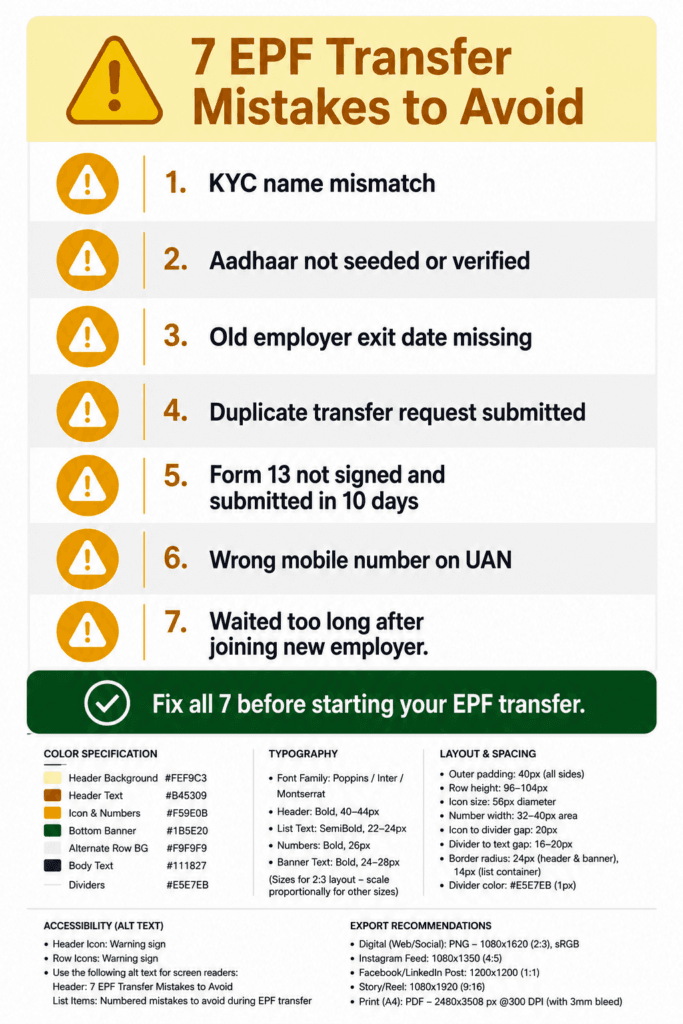

Mistake 1 — KYC Mismatch

The single most common reason EPF transfers fail. Your name on Aadhaar must exactly match your EPFO records. Even a middle name included on one and dropped on the other causes a mismatch. Fix this first — it takes 5 minutes and prevents weeks of delays.

Mistake 2 — Aadhaar Not Seeded

Aadhaar seeding has been mandatory for PF transactions since 2021. Without it, your EPF transfer request won’t proceed at all. Go to Manage → KYC, add your Aadhaar, and wait for employer digital verification. If your employer is slow, follow up with HR — this is on their side, not yours.

Mistake 3 — Old Employer Hasn’t Updated Exit Date

One of the biggest delays in the EPF transfer process is an old employer who hasn’t entered your Date of Exit on the EPFO portal. Without it, the system doesn’t recognise you as having left that job. Contact your old HR and ask them to update the date immediately. EPFO’s 2025 rules now push employers to update this on time — but not all comply promptly.

Mistake 4 — Submitting More Than One Transfer Request for the Same Member ID

EPFO allows only one EPF transfer request per previous Member ID. If your first request is pending or stuck, don’t submit a second one — it gets rejected. Instead, track the first request and raise a grievance via the EPFO portal if it’s not moving after 30 days.

Mistake 5 — Not Printing and Submitting Form 13 Within 10 Days

If the portal still requires physical Form 13 submission (for accounts where employer attestation is needed), you have to print, sign, and submit it to the attesting employer within 10 days of submitting online. Missing this deadline stalls the entire EPF transfer process.

Mistake 6 — Wrong Mobile Number

The OTP for EPF transfer goes to the mobile number registered with your UAN — not your current phone number. If you’ve changed numbers since joining your first job, update the mobile number on the EPFO portal before initiating the transfer request. You’ll need your old number to receive the update OTP, so do this while you still have access to it.

Mistake 7 — Waiting Too Long After Joining New Employer

The longer you wait after joining a new job to initiate EPF transfer, the harder it becomes. Old employer HR teams change, companies restructure, and EPFO records get harder to reconcile. Start the process within 30 days of joining. If you’re on the auto-transfer system and all KYC is clean, it fires automatically — but even then, verify in your passbook that it happened.

The Real Cost of Skipping EPF Transfer and Withdrawing Instead

People understand withdrawal is taxed. What they don’t calculate is the compounding cost. Here’s a realistic scenario:

Arjun, a 27-year-old software developer in Bengaluru, changed jobs after 3.5 years. His EPF balance was ₹1.8 lakh. He withdrew it, paid 10% TDS (₹18,000), and received ₹1,62,000 — which he spent on a laptop and travel.

What happened in the alternate universe where he did the EPF transfer:

- ₹1,80,000 transferred to new PF account

- Continued earning 8.25% compounded annually

- At age 58 (31 years later): approximately ₹19.6 lakh from that single transferred balance

The laptop cost him ₹19.6 lakh in retirement wealth. Not dramatically — quietly, 31 years later, when it was too late to recalculate.

Run your own numbers using MoneyOra’s EPF Calculator. Enter your current balance, your age, and your expected retirement age. The compounding output is usually enough to make the EPF transfer decision obvious within 20 seconds.

| Scenario | Tax Treatment | TDS Rate |

|---|---|---|

| Withdrawal after 5+ years continuous service | Fully tax-free | Nil |

| Withdrawal before 5 years — amount < ₹50,000 | Taxable (add to income) | No TDS |

| Withdrawal before 5 years — amount ≥ ₹50,000 (PAN linked) | Taxable — entire amount | 10% TDS |

| Withdrawal before 5 years — PAN not linked | Taxable at maximum rate | 30% TDS |

| EPF transfer (any duration) | Not a taxable event | Zero |

New from April 1, 2026: Form 121 has replaced Forms 15G/15H for tax declaration on PF withdrawals. If you’re withdrawing before 5 years and believe your income is below the taxable threshold, submit Form 121 online while filing the withdrawal claim to avoid TDS deduction.

MoneyOra Analysis — What the 2025 Rule Changes Actually Mean for Salaried Indians

The January 2025 EPFO circular eliminating employer approval for eligible EPF transfers is more significant than most coverage suggests. Think about what the old process actually looked like: you’d switch jobs, initiate a transfer request online, then wait for a HR team at your old company — where you no longer work and have no leverage — to click approve. If they were slow, disorganised, or simply hostile, your money sat in limbo for months. This was one of the most consistently frustrating parts of changing jobs in India.

Removing that dependency for Aadhaar-linked accounts changes the dynamic entirely. EPF transfer is now effectively a self-service process for most salaried employees. Combined with auto-transfer from April 2024, the system has moved from “something employees had to actively chase” to “something that largely handles itself if KYC is clean.”

The practical implication for freshers and mid-career employees: your EPF health is now almost entirely in your own hands. Keep your KYC updated. Keep your Aadhaar and PAN linked. Make sure your old employer updates your exit date. Do those three things every time you change jobs, and EPF transfer becomes a 10-minute activity rather than a months-long saga.

What competitors miss in their EPF transfer guides: Almost none of the top-ranking articles mention the January 2025 employer-approval elimination clearly. Most still walk through “choose previous or current employer to attest” as a live step — that step is now skipped for a large proportion of accounts. If you’re on a guide that shows that as mandatory, you’re reading 2023 instructions for a 2026 process.

The numbers context: 1.30 crore EPF transfer claims were filed between April 2024 and January 2025 alone. With 7+ crore active EPF subscribers in India and millions switching jobs every year, the EPF transfer process touches an enormous number of lives. Getting it right — or wrong — has real compounding consequences, as the table in Section 8 shows.

One thing to watch in 2026: EPFO 3.0’s ATM card and UPI withdrawal rollout. These are designed for withdrawals, not transfers. But as the digital layer of EPF improves, the temptation to withdraw “instantly” via ATM card rather than transfer may increase. Don’t confuse speed of access with financial wisdom. The EPF transfer remains the correct choice in almost every job-change scenario.

Risks to Watch During EPF Transfer

- Employer non-compliance: Despite EPFO rules, some employers still don’t update exit dates promptly. If your old employer is unresponsive, raise a grievance on the EPFO portal under Help → Grievance and copy the EPFO regional office.

- Duplicate UAN risk: If you were accidentally given two UANs (rare but happens), the transfer process can get complicated. Check your UAN status on the portal and get duplicates merged before initiating the EPF transfer.

- Passbook delay ≠ transfer failure: EPFO’s passbook updates for wage months sometimes run behind due to backend processing. Don’t panic if your balance doesn’t appear immediately — check status via Track Claim before assuming failure.

- Rule changes: EPFO rules have been evolving rapidly in 2024–2026. Always verify current process on the official EPFO website before initiating a transfer.

- Tax law changes: TDS thresholds and tax treatment of EPF withdrawals can change with each Budget. The Form 121 replacement of 15G/15H effective April 2026 is an example of this. Stay updated via the Income Tax Department website before filing any withdrawal claims.

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. EPFO rules and tax provisions are subject to change. Always verify current rules on the official EPFO portal and consult a CA for complex tax scenarios. MoneyOra does not guarantee returns or recommend specific financial actions.

EPF Transfer — The Bottom Line

The EPF transfer process in 2026 is about as simple as it’s going to get. Auto-transfer handles most cases automatically. Employer approval has been eliminated for Aadhaar-linked accounts. Interest runs uninterrupted. Processing is faster under EPFO 3.0.

The only thing that still trips people up is not having KYC clean before they need it. Fix that now, today — not when you’re already in the middle of a job change and need the transfer to happen fast.

And if you’re tempted to withdraw instead of doing the EPF transfer: calculate what your balance becomes at retirement first. The number tends to be more persuasive than any guide.

See What Your EPF Balance Becomes at Retirement

EPF • PPF • NPS • SIP • FD — all calculators free, no login required.

Use the free calculator now on MoneyOra.in →MoneyOra Tools and Articles

- EPF Calculator — Project your PF corpus at 8.25% from current balance to retirement age

- PPF Calculator — Compare EPF growth against voluntary PPF contributions

- NPS Calculator — Model your total retirement corpus combining EPF, PPF, and NPS

- SIP Calculator — Build equity returns alongside your guaranteed EPF/PPF base

- FD Calculator — Compare EPF vs FD returns after tax

- Bank Calculators Hub — All savings, deposit, and income calculators in one place

- Financial Calculator India — Complete MoneyOra calculator directory

- ₹25,000 Salary Investment Plan — How to build wealth from a starter salary (EPF, SIP, PPF)

- ₹100/Day Investment Plan — Small daily investments and the compounding reality

- Hidden Bank Charges — Other money leaks salaried employees don’t notice

Frequently Asked Questions — EPF Transfer Online

How long does an EPF transfer take in 2026?

The official EPFO timeline is approximately 20 days. Under EPFO 3.0, auto-settled claims are processing faster — many within 10–15 working days. The biggest delay factor is employer verification (if still required). Accounts eligible for the January 2025 no-employer-approval rule process faster. Track your EPF transfer status under Online Services → Track Claim Status on the EPFO portal.

Is EPF transfer taxable?

No. EPF transfer is not a taxable event regardless of how long you’ve been employed. You’re moving money from one EPF account to another — there’s no withdrawal, no TDS, and no income tax liability. Tax only applies on actual EPF withdrawal, and only if it happens before 5 years of continuous service. The transfer itself is completely tax-free.

Can I do EPF transfer without employer approval in 2026?

Yes, for most accounts. Following EPFO’s January 15, 2025 circular, employer approval has been eliminated for accounts where the UAN is Aadhaar-linked and personal details match across accounts. If your account meets the eligibility criteria — which most UAN accounts allotted after October 2017 do — the EPF transfer processes without any employer attestation needed.

What happens if I don’t do EPF transfer and just leave the old account?

Your EPF account continues earning 8.25% interest for 3 years after your last contribution. After 3 years of inactivity, the account becomes dormant and stops earning interest. After 7 years, unclaimed balances go to the Senior Citizens’ Welfare Fund but remain claimable. The right move is always to initiate EPF transfer to your active account — either manually or via auto-transfer — soon after joining the new employer.

My old employer is not responding for EPF transfer. What do I do?

First check if your account is eligible for the no-employer-approval pathway (January 2025 rule). If it is, your EPF transfer should have processed without needing their response. If not, raise a grievance on the EPFO portal under Help → Grievance. You can also email the EPFO regional office covering your old employer’s location. EPFO typically responds to grievances within 15–30 days. Don’t sit on this — unresponsive employers cause the most transfer delays.

What is Form 13 in EPF transfer?

Form 13 is the official EPF transfer request form used to transfer your PF balance from a previous employer’s account to the current employer’s account. It captures your personal details, previous and current Member IDs, and the transfer request. Since April 2025, an updated version of Form 13 separates taxable and non-taxable PF components for accurate TDS calculation. Always download Form 13 from the current EPFO portal — not from old cached PDFs online.

Will my EPS (pension) amount also transfer?

Yes. When you initiate an EPF transfer, both the EPF balance and the EPS (Employee Pension Scheme) service record transfer together. Your years of service in EPS are accumulated across employers through the same UAN. Importantly, you need 10 continuous years of EPS service to be eligible for monthly pension at age 58. Withdrawing EPF (and EPS) at job change resets this count — another strong reason to always transfer, never withdraw.

Can I transfer EPF to a PPF account?

No. EPF and PPF are separate schemes — EPF is an employer-linked retirement fund managed by EPFO, while PPF is a voluntary savings scheme through banks or post offices. You can’t directly transfer EPF funds to a PPF account. EPF transfer only moves your PF balance from one EPFO-linked employer account to another. If you want to invest additionally beyond EPF, you can open a separate PPF account and contribute to it independently — plan contributions using MoneyOra’s PPF Calculator.

What is auto-transfer and do I need to do anything for it?

Auto-transfer, effective April 1, 2024, automatically moves your EPF balance to the new employer’s PF account when the first monthly contribution is credited — without you submitting Form 13 or selecting any options. For it to work, your UAN must be Aadhaar-linked, KYC must be fully verified, and your old employer must have updated your Date of Exit. If all these are in place, the transfer happens in the background. Verify it worked by checking your EPF passbook after 30–45 days of joining.

How do I check my EPF transfer status?

Log in to your EPFO Member Portal (unifiedportal-mem.epfindia.gov.in) → Online Services → Track Claim Status. Select “Transfer Claim Status” to see the current stage. You can also check via the UMANG app. Save your Tracking ID from when you submitted the request — it makes status checks faster. If the status hasn’t moved in 10+ working days, raise a grievance on the portal or contact your HR.

Pingback: 100 Per Day Investment: How Wealth Can You Build - MoneyOra

Pingback: Hidden Bank Charges: 9 Fees Costing You ₹2,000+ - MoneyOra

Pingback: EPFO 3.0: The Best Way to Access Your PF in 2026 - MoneyOra