Personal Loan EMI

Calculator

Monthly instalments for any currency — Home, Car, Personal & Education loans.

| Year | Principal | Interest | Total | Balance |

|---|

Free Personal Loan EMI Calculator – Accurately Calculate 2026 Monthly EMI Online

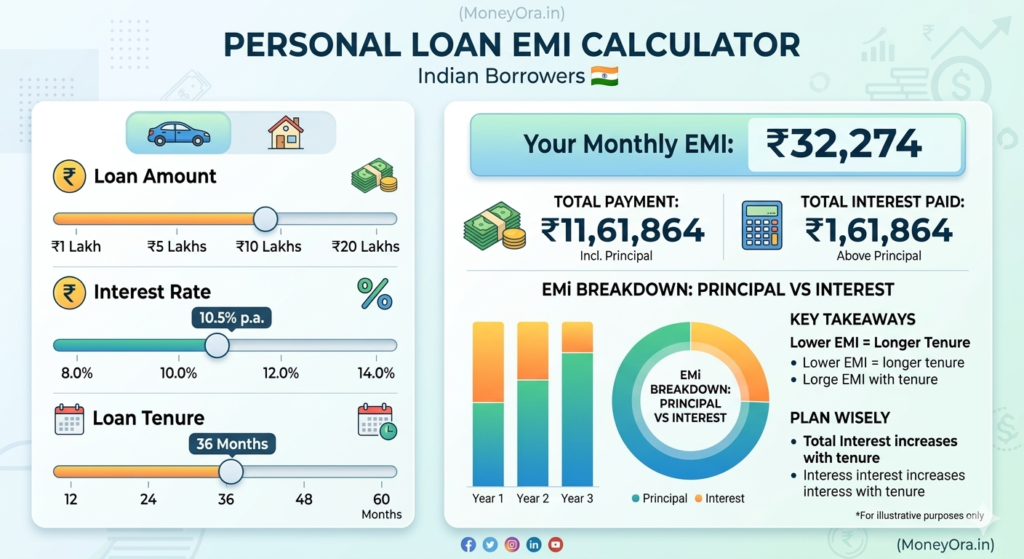

A personal loan EMI calculator is the fastest way to know exactly what you are committing to before you borrow.

Enter three numbers — loan amount, interest rate, and tenure — and the personal loan EMI calculator tells you your monthly instalment, total interest payable, and complete repayment breakdown in under 5 seconds.

No guesswork. No dealer estimates. Just the accurate number.

Personal loans are the most commonly availed loan product in India. Over 78% of all retail credit falls under this category. They are unsecured — no property to pledge, no collateral required — which makes them fast and flexible.

But “easy to get” is not the same as “easy to repay” if you have not calculated the numbers first.

Use Moneyora’s personal loan EMI calculator above before you apply. This page explains everything behind the numbers.

Table of Contents

What Is a Personal Loan EMI Calculator?

A personal loan EMI calculator is a free online tool that computes your Equated Monthly Instalment — the fixed amount you pay every month until the loan is fully repaid.

EMI stands for Equated Monthly Instalment.

Every personal loan EMI has two components: principal repayment and interest. In the early months, a larger share of your EMI goes toward interest. As the loan progresses, the principal component grows and the interest component shrinks.

A personal loan EMI calculator makes this visible. It shows not just the monthly number but also the complete split — what goes to principal and what goes to interest — month by month.

This matters because:

- You can plan your monthly budget accurately before borrowing

- You can decide the right tenure for your cash flow situation

- You can identify the best time to make a prepayment to save maximum interest

- You can compare different loan offers side by side in real time

Using a personal loan EMI calculator before applying is one of the most useful things a borrower can do. It takes 30 seconds and saves you from unpleasant surprises for the next 2–5 years.

Personal Loan EMI Formula

Every bank, NBFC, and digital lender in India calculates EMI using the same standard reducing balance formula. Moneyora’s personal loan EMI calculator uses the same formula:

EMI = [P × R × (1+R)^N] ÷ [(1+R)^N – 1]

Where:

- P = Principal — the loan amount you are borrowing

- R = Monthly interest rate = Annual rate ÷ 12 ÷ 100

- N = Loan tenure in months

Worked example:

Mr. Rahul wants to borrow Rs 15 lakh at 12% per annum for 5 years (60 months).

- Monthly rate R = 12 ÷ 12 ÷ 100 = 0.01

- (1+R)^N = (1.01)^60 = 1.8167

- EMI = 15,00,000 × 0.01 × 1.8167 ÷ (1.8167 – 1) = Rs 33,367

Total paid = Rs 33,367 × 60 = Rs 20,02,020

Total interest = Rs 20,02,020 – Rs 15,00,000 = Rs 5,02,020

That is Rs 5 lakh paid in interest on a Rs 15 lakh personal loan.

The personal loan EMI calculator runs this computation instantly so you never need to touch the formula manually.

How to Use the Personal Loan EMI Calculator

Moneyora’s personal loan EMI calculator has three inputs. No login required.

Step 1 — Enter the loan amount

Type the amount you plan to borrow. Personal loans in India start from as low as Rs 10,000 and go up to Rs 50 lakh depending on your income and lender.

Step 2 — Enter the interest rate

Use the exact rate your lender has quoted. If you have not applied yet, personal loan rates in India typically range from 10.5% to 24% depending on your CIBIL score, employer, and lender type.

Run the personal loan EMI calculator at the low end and high end of your expected rate. The difference in monthly EMI and total interest is often significant enough to influence your decision.

Step 3 — Select the tenure

Personal loan tenures in India run from 12 to 60 months, with some lenders offering up to 84 months.

Shorter tenure = higher EMI, less total interest.

Longer tenure = lower EMI, more total interest.

The personal loan EMI calculator shows both the monthly number and the total cost so you can make the right tradeoff for your situation.

Personal Loan EMI Table – Quick Reference

Approximate monthly EMI at 12% annual interest:

| Loan Amount | 1 Year | 2 Years | 3 Years | 5 Years |

|---|---|---|---|---|

| Rs 1 Lakh | Rs 8,885 | Rs 4,707 | Rs 3,321 | Rs 2,224 |

| Rs 2 Lakh | Rs 17,769 | Rs 9,415 | Rs 6,642 | Rs 4,449 |

| Rs 3 Lakh | Rs 26,654 | Rs 14,122 | Rs 9,963 | Rs 6,672 |

| Rs 5 Lakh | Rs 44,424 | Rs 23,537 | Rs 16,607 | Rs 11,122 |

| Rs 10 Lakh | Rs 88,849 | Rs 47,073 | Rs 33,214 | Rs 22,244 |

| Rs 15 Lakh | Rs 1,33,273 | Rs 70,610 | Rs 49,821 | Rs 33,367 |

These figures are indicative at 12% reducing balance rate. Use the personal loan EMI calculator above for your exact quoted rate.

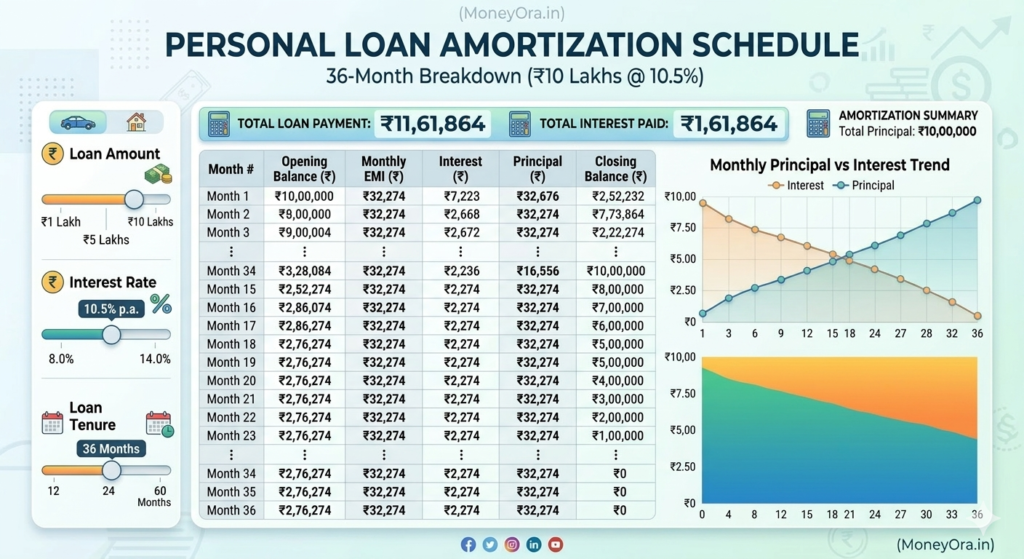

Amortization Schedule Explained

An amortization schedule is the month-by-month breakdown of every EMI payment.

It shows exactly how much of each payment reduces the principal and how much pays interest.

Here is the amortization for a Rs 5 lakh personal loan at 12% for 3 years (36 months):

| Month | Principal (Rs) | Interest (Rs) | EMI (Rs) | Balance (Rs) |

|---|---|---|---|---|

| 1 | 11,607 | 5,000 | 16,607 | 4,88,393 |

| 2 | 11,723 | 4,884 | 16,607 | 4,76,670 |

| 3 | 11,840 | 4,767 | 16,607 | 4,64,830 |

| 6 | 12,199 | 4,408 | 16,607 | 4,28,595 |

| 12 | 12,971 | 3,636 | 16,607 | 3,63,592 |

| 18 | 13,799 | 2,808 | 16,607 | 2,93,098 |

| 24 | 14,681 | 1,926 | 16,607 | 2,16,661 |

| 30 | 15,621 | 986 | 16,607 | 1,33,661 |

| 36 | 16,443 | 164 | 16,607 | 0 |

Notice how the interest drops from Rs 5,000 in month one to just Rs 164 in the final month.

Why does this matter practically?

If you receive a bonus and want to make a part-prepayment, doing it in month 6 saves far more interest than doing it in month 30.

In month 6, you still owe Rs 4,28,595. A Rs 50,000 prepayment there eliminates months of future interest.

By month 30, the balance is Rs 1,33,661 — there is very little interest left to save.

The full 36-month schedule is available in the personal loan EMI calculator output above.

Factors That Affect Personal Loan EMI

1. Loan Amount

The higher the principal, the higher the personal loan EMI — directly proportional.

Before deciding on an amount, check that your total monthly EMI commitment across all active loans stays below 40–50% of your net monthly income. Use the personal loan EMI calculator to find the loan amount where your EMI falls within that boundary.

2. Interest Rate

This is the single biggest lever on your personal loan EMI.

On a Rs 5 lakh loan over 3 years:

| Interest Rate | Monthly EMI | Total Interest |

|---|---|---|

| 10.5% | Rs 16,247 | Rs 84,892 |

| 14% | Rs 17,090 | Rs 1,15,240 |

| 18% | Rs 18,080 | Rs 1,50,880 |

| 22% | Rs 19,121 | Rs 1,88,356 |

The difference between 10.5% and 22% on the same Rs 5 lakh loan is Rs 1,03,464 in total interest — more than 20% of the principal itself.

Your CIBIL score is the primary factor determining which rate you are offered. A score of 750+ consistently fetches the lowest available rate. According to TransUnion CIBIL, scores below 700 result in higher rates or rejection at most banks.

3. Loan Tenure

Longer tenure reduces the monthly personal loan EMI but significantly increases total interest paid.

On a Rs 10 lakh loan at 14%:

| Tenure | Monthly EMI | Total Interest |

|---|---|---|

| 1 year | Rs 89,979 | Rs 79,748 |

| 2 years | Rs 48,013 | Rs 1,52,312 |

| 3 years | Rs 34,178 | Rs 2,30,408 |

| 5 years | Rs 23,268 | Rs 3,96,080 |

Going from 1 year to 5 years reduces the monthly EMI by Rs 66,711.

But it adds Rs 3,16,332 in total interest paid.

Run both scenarios in the personal loan EMI calculator and decide based on your monthly cash flow.

4. CIBIL Score

Your credit score determines your interest rate, which directly sets your personal loan EMI.

- Score 750+ — best available rate, fastest approval

- Score 700–749 — slightly higher rate, most banks approve

- Score 650–699 — significantly higher rate, limited lender options

- Score below 650 — most banks decline, NBFCs may lend at 20%+

Even a 1% lower rate saves Rs 8,000–20,000 in total interest on a typical personal loan. It is worth spending 3–6 months improving your score before applying for a large loan.

5. Employment Type

Salaried employees at large companies and government workers typically get the lowest personal loan rates.

Self-employed borrowers face higher rates due to income variability.

The same borrower profile at a public sector bank versus a small NBFC can face a rate difference of 5–8%.

6. Lender Type

| Lender Type | Typical Rate | Processing Time |

|---|---|---|

| Public sector banks | 10.5% – 13% | 3–7 days |

| Private banks | 11% – 16% | 1–3 days |

| NBFCs | 13% – 22% | Same day to 2 days |

| Fintech lenders | 14% – 30% | Hours |

Always input the rate from your specific lender into the personal loan EMI calculator — do not rely on advertised “starting from” rates, which apply only to the most creditworthy applicants.

Personal Loan vs Other Loan Types – Comparison

| Feature | Personal Loan | Home Loan | Car Loan | Gold Loan |

|---|---|---|---|---|

| Collateral | Not required | Property | Vehicle | Gold |

| Typical rate | 10.5% – 24% | 8% – 9.5% | 8.5% – 12% | 9% – 18% |

| Max tenure | 5–7 years | 30 years | 7 years | 3 years |

| Approval time | 1–3 days | 2–4 weeks | 1–3 days | Same day |

| Max loan | Rs 50 lakh | Rs 10 crore+ | 90% of value | 75% of value |

| Use restriction | None | Property only | Vehicle only | None |

A personal loan costs more than a secured loan. That is the price of flexibility and speed.

If you have assets to pledge and time to wait, a secured loan is cheaper. If you need funds quickly for any purpose, a personal loan is the practical choice.

Use the personal loan EMI calculator alongside our home loan EMI calculator and car loan EMI calculator to compare monthly commitments across loan types before deciding.

5 Proven Ways to Reduce Your Personal Loan EMI

1. Improve your CIBIL score before applying

A 50-point improvement in your CIBIL score can reduce your rate by 1–2%.

On a Rs 5 lakh, 3-year personal loan, that saves Rs 15,000–30,000 in total interest.

Check your score free at TransUnion CIBIL before approaching any lender.

2. Negotiate the interest rate

Most borrowers accept the first rate offered. Banks have flexibility — especially if you hold a salary account, fixed deposit, or existing relationship with them.

Asking directly for their best rate costs nothing and often works.

3. Choose a shorter tenure where possible

Monthly EMI goes up, but total interest drops significantly.

Run both tenure options in the personal loan EMI calculator and compare the total cost — not just the monthly number. The difference often surprises borrowers.

4. Compare at least 3 lenders

Your own bank, one NBFC, and one fintech lender.

Rate differences of 3–5% for the same borrower profile are common. On a Rs 10 lakh loan, 3% rate difference = Rs 50,000+ in total interest savings.

5. Make part-prepayments early in the tenure

A bonus or windfall deployed as a prepayment in month 6 saves far more than the same amount in month 30.

The amortization table in the personal loan EMI calculator shows exactly how much you save at each point in the tenure.

Check your loan agreement for foreclosure charges — typically 2–5% of outstanding principal on fixed-rate personal loans. As per RBI’s fair lending guidelines, lenders cannot charge foreclosure penalties on floating-rate loans.

Tax Benefits on Personal Loans in India

Standard personal loans for personal consumption have no tax deduction.

However, two exceptions apply:

Home renovation or purchase: If you use personal loan funds specifically for home renovation or property purchase, the interest may qualify for deduction under Section 24(b) of the Income Tax Act — up to Rs 2 lakh per year. Documentation proving end-use is required.

Business use: If you are self-employed and deploy the funds for business purposes, the interest can be claimed as a business expense under Section 37(1).

Salaried borrowers using a personal loan for travel, medical expenses, or consumer purchases cannot claim any deduction.

Refer to the Income Tax Department’s official portal or consult a chartered accountant to confirm your eligibility.

Why Use Moneyora’s Personal Loan EMI Calculator?

Most personal loan EMI calculators give you three numbers — monthly EMI, total interest, total payable. Moneyora goes further.

Moneyora’s personal loan EMI calculator gives you:

- Full month-by-month amortization breakdown

- Real-time adjustment across all three variables

- Instant total cost comparison across different tenures

- No registration or login required

- No personal data stored

The personal loan EMI calculator is free and available 24/7.

For multi-loan comparisons, visit our loan comparison tool.

For home loan calculations, the home loan EMI calculator handles larger amounts

Disclaimer: All EMI figures on this page are calculated using the standard reducing balance formula and are indicative only. Actual EMI from your lender may vary based on processing fees, rounding, and lender-specific terms. Moneyora does not offer loans directly. Verify all figures with your lender before committing to any loan agreement. and longer tenures.

Frequently Asked Questions

No. Personal loans are fully unsecured.

You do not need to pledge any property, gold, or asset to get a personal loan in India.

This makes them the fastest loan type to process and the most flexible in terms of end-use.

Yes, for fixed-rate personal loans — which is the standard across all major Indian banks and NBFCs.

Your personal loan EMI does not change from month one to the final payment unless you make a part-prepayment that results in a revised schedule.

Maintain a CIBIL score of 750 or above.

Keep your existing debt-to-income ratio below 40%.

Compare offers from at least three lenders.

Customers with salary accounts at the lending bank often get preferential rates.

As per RBI's fair lending guidelines, lenders must disclose the annualised interest rate on a reducing balance basis.

Always ask for this in writing before signing.

Most banks and NBFCs offer up to Rs 40–50 lakh for salaried individuals with strong income and credit profiles.

The actual amount depends on your net monthly income, existing loan obligations, and employer category.

Missing one EMI triggers a late payment fee of Rs 500–2,000.

It also results in a negative entry on your CIBIL report.

Missing three or more consecutive EMIs leads to NPA classification.

This makes future credit very difficult to access.

If you foresee difficulty, contact your lender before the due date.

Most lenders will offer restructuring or a short moratorium.

Yes. Most lenders allow part-prepayment and full foreclosure after a lock-in period of 6–12 months.

Foreclosure charges on fixed-rate loans are typically 2–5% of outstanding principal.

On floating-rate loans, RBI rules prohibit prepayment penalties entirely.

The personal loan EMI calculator shows your exact monthly commitment before you borrow.

Financial advisors recommend keeping total EMI across all loans below 40–50% of monthly net income.

Running the calculator before applying helps you stay within that range and avoid overextension.

Debt-to-income ratio is your total monthly EMI divided by your net monthly income.

For example, if your salary is Rs 60,000 and your total EMIs are Rs 24,000, your ratio is 40%.

Most lenders consider 40–50% the maximum safe level.

The EMI calculator helps you check this before you apply.

The personal loan EMI calculator uses the standard reducing balance formula.

This is the same method all RBI-regulated banks use.

Minor differences can arise from rounding, processing fee inclusion, or GST on charges.

The calculator gives you a highly accurate estimate.

Always confirm the final figure with your lender's official sanction letter.

Absolutely. The personal loan EMI calculator works identically for salaried, self-employed, and business borrowers.

The formula does not change based on employment type.

The only practical difference is that self-employed borrowers typically face higher interest rates.

They can input this directly into the calculator to get accurate results.