Real numbers by income slab — from ₹21,000 to ₹1 lakh+ — plus what it takes to qualify for ₹50 lakh or ₹1 crore.

“How much home loan can I get?” is the question every property search actually starts with — before the shortlisting, before the site visits, before falling for a flat that’s out of budget. Banks don’t lend against your dream home; they lend against your home loan eligibility, a number built entirely from your salary, existing debt, age, and credit score. This guide breaks that number down by income slab, so you know your real range before you start scrolling listings. If you already have an EMI running, check it against the EMI Calculator first — it directly affects the number below.

Key Takeaways

- Home loan eligibility is driven by FOIR, not just your salary number in isolation.

- A ₹50,000 salary typically supports ₹28–32 lakh; ₹1 lakh supports ₹57–65 lakh, at 20-year tenure.

- A ₹50 lakh home loan generally needs a net monthly salary of roughly ₹85,000–₹90,000, assuming no existing EMIs.

- Clearing a ₹5,000 existing EMI before applying can add ₹5–6 lakh back to your home loan eligibility.

- CIBIL score below 700 can shrink both your loan amount and your rate — sometimes enough to disqualify you entirely.

How Banks Actually Calculate Home Loan Eligibility

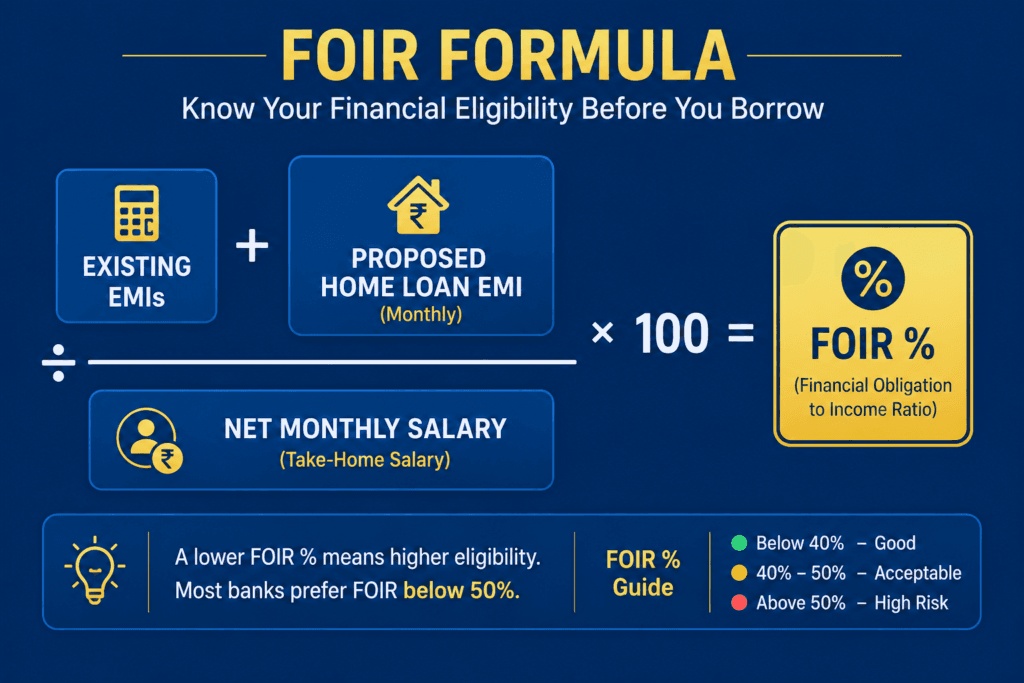

FOIR stands for Fixed Obligation to Income Ratio, and it’s the single number that decides everything else. The formula is simple:

FOIR = (Existing EMIs + Proposed Home Loan EMI) ÷ Net Monthly Salary × 100 — this single formula is what determines your home loan eligibility.

Say your take-home salary is ₹60,000 a month, and the bank applies a 50% FOIR cap. Your total EMI room is ₹30,000. If you’re already paying ₹8,000 toward a car loan, your available room for a home loan EMI drops to ₹22,000 — and your eligible loan amount shrinks accordingly. This is the part most salary-based rules of thumb skip entirely, and it’s usually the difference between the number you expected and the number the bank actually offers.

Lenders also apply a rough shortcut early in the process — a salary multiplier of roughly 55 to 65 times your net monthly income — as a quick sanity check before the detailed FOIR calculation takes over. Property value matters too: under RBI’s Loan-to-Value norms, banks typically finance 75–90% of the property’s value, with the rest expected as your down payment.

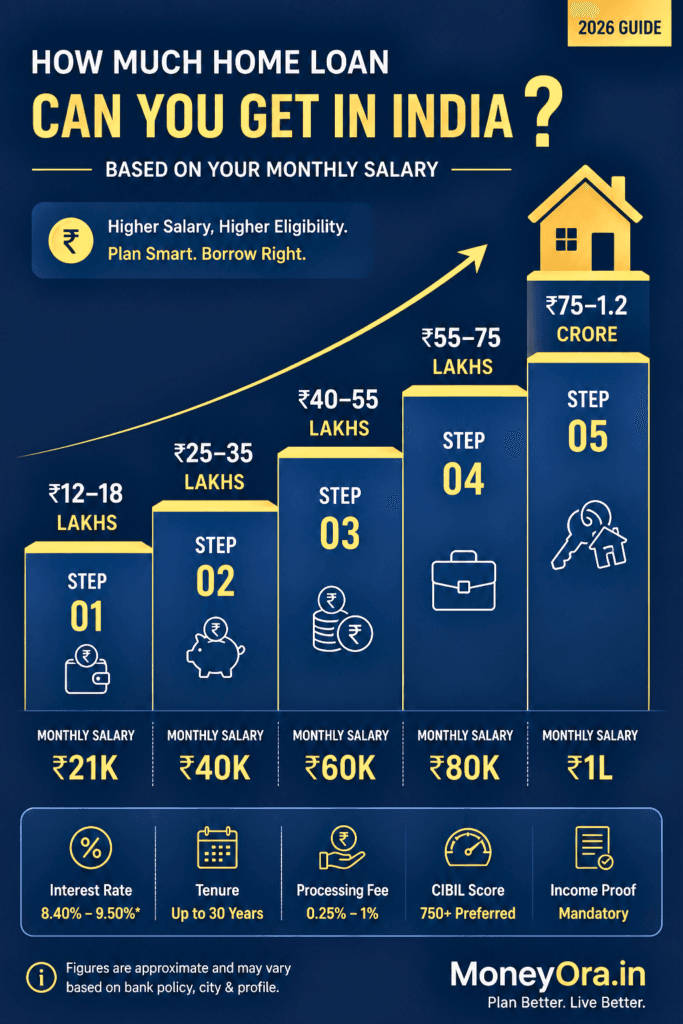

Home Loan Eligibility by Salary — ₹21,000 to ₹1 Lakh+

Here’s the full home loan eligibility breakdown, slab by slab. These are indicative ranges based on standard FOIR methodology — your actual sanction will vary with CIBIL score, employer category, and city.

| Net Monthly Salary | Max EMI (50% FOIR) | Approx. Eligibility (20-yr, 8.5%) | Approx. Eligibility (25-yr, 8.5%) |

|---|---|---|---|

| ₹21,000 | ₹10,500 | ₹12–13 lakh | ₹13–14 lakh |

| ₹30,000 | ₹15,000 | ₹17–19 lakh | ₹18–20 lakh |

| ₹40,000 | ₹20,000 | ₹23–25 lakh | ₹24–27 lakh |

| ₹50,000 | ₹25,000 | ₹28–32 lakh | ₹31–35 lakh |

| ₹60,000 | ₹30,000 | ₹34–38 lakh | ₹37–41 lakh |

| ₹80,000 | ₹40,000 | ₹46–51 lakh | ₹50–55 lakh |

| ₹1,00,000 | ₹50,000 | ₹57–65 lakh | ₹62–70 lakh |

Can I get a home loan with a ₹30,000 salary?

Yes. Most major lenders will approve a home loan on a ₹30,000 net monthly salary, typically in the ₹17–19 lakh range over 20 years, provided you have no major existing EMIs and a CIBIL score above 700. This comfortably covers a compact flat in a Tier 2 or Tier 3 city, or a smaller unit on the outskirts of a metro.

How much home loan can I get on a ₹60,000 salary?

At a ₹60,000 net monthly salary with no existing EMIs, most lenders will sanction between ₹34 lakh and ₹38 lakh over a 20-year tenure at around 8.5% interest. Extending the tenure to 25 years can push this closer to ₹40–41 lakh, since the EMI drops enough to fit comfortably within the FOIR cap.

How much home loan for a ₹21,000 salary?

A ₹21,000 net monthly salary typically supports a home loan of roughly ₹12–13 lakh over 20 years. This is close to the minimum income threshold several major lenders apply, so a clean repayment history and zero existing EMIs matter more at this level than at higher income bands.

How Much Salary Do You Need for a ₹50 Lakh Home Loan?

Work the FOIR formula backward and your ₹50 lakh home loan eligibility figure becomes concrete rather than aspirational. An EMI of ₹43,400 needs ₹86,800 in net monthly income to stay under a 50% cap — round up slightly for safety, and ₹90,000 is a comfortable target. If you already carry a ₹10,000 car loan EMI, your required salary climbs to roughly ₹1.06 lakh, since the bank still needs your total obligations to fit within the same 50% ceiling.

Stretching tenure to 25 or 30 years lowers the required EMI and, with it, the minimum salary — but it also means paying meaningfully more in total interest over the life of the loan. Run both scenarios on the Home Loan EMI Calculator before deciding which trade-off works for your budget.

How Much Salary for a ₹1 Crore Home Loan?

At this loan size, lenders lean harder on employer category, income stability, and CIBIL score — a ₹1 crore sanction on a single salaried income is achievable, but it’s far more common with a working spouse as co-applicant. Two incomes of roughly ₹90,000 each comfortably clear this bar, since combined income is what FOIR is actually calculated against once a co-applicant is added.

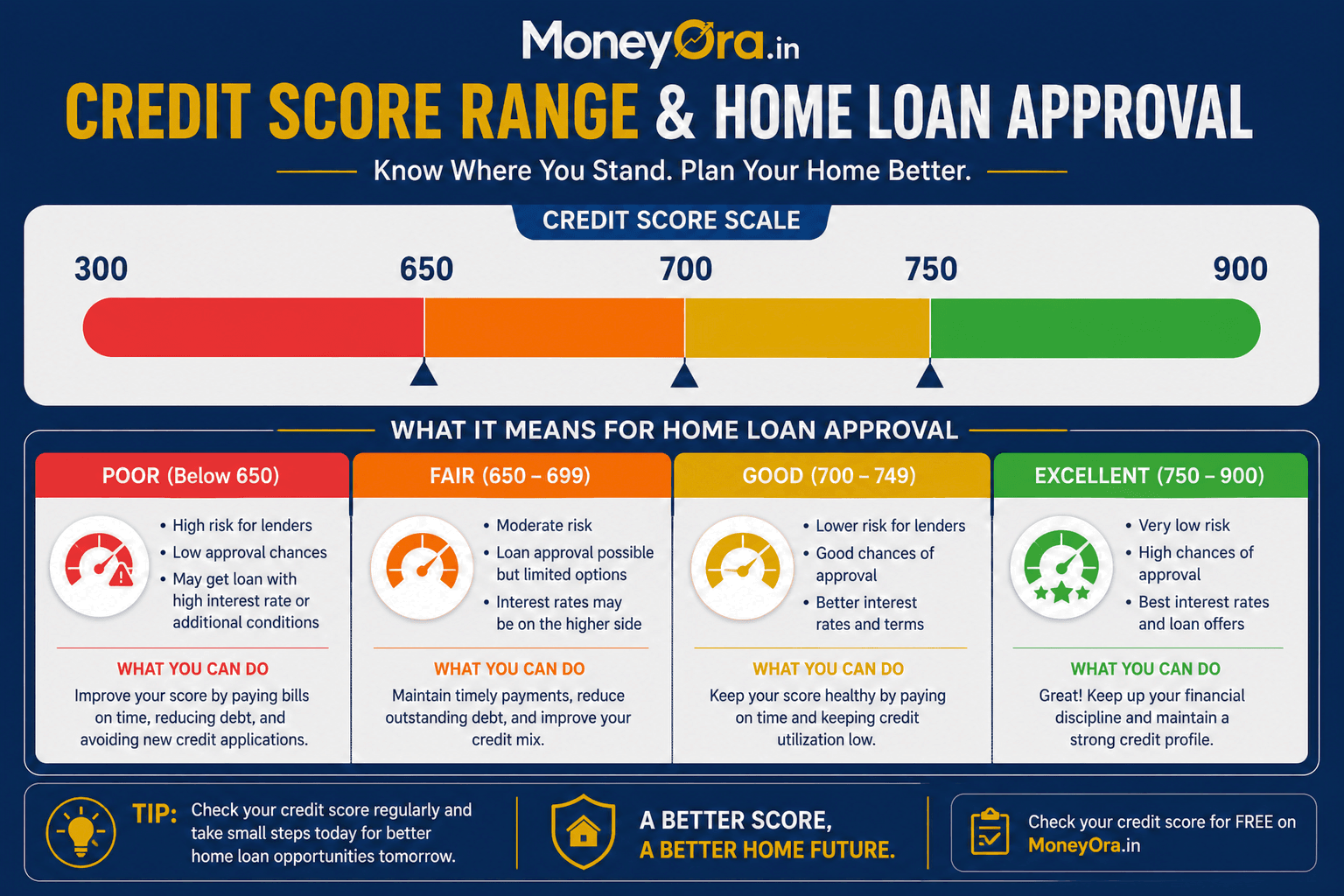

CIBIL Score: The Multiplier Most People Ignore

Salary decides your home loan eligibility ceiling. CIBIL score decides whether you actually get there — and at what price. Most major banks require a minimum score of 650–700 to even consider an application; 750 and above unlocks the best rates and the full eligible amount.

| CIBIL Score Range | Typical Outcome |

|---|---|

| 750+ | Best rates (from ~8.35% p.a.), maximum eligible loan amount |

| 700–749 | Approved, but at 0.25–0.5% higher interest |

| 650–699 | Approved by some lenders, reduced loan amount likely |

| Below 650 | Rejected by most major banks |

A 0.5% rate difference doesn’t sound like much until you run it over 20 years — on a ₹50 lakh loan, that gap alone costs close to ₹3.8 lakh in extra interest. Checking and improving your score before applying is one of the highest-leverage moves in this entire process, and it costs nothing but time.

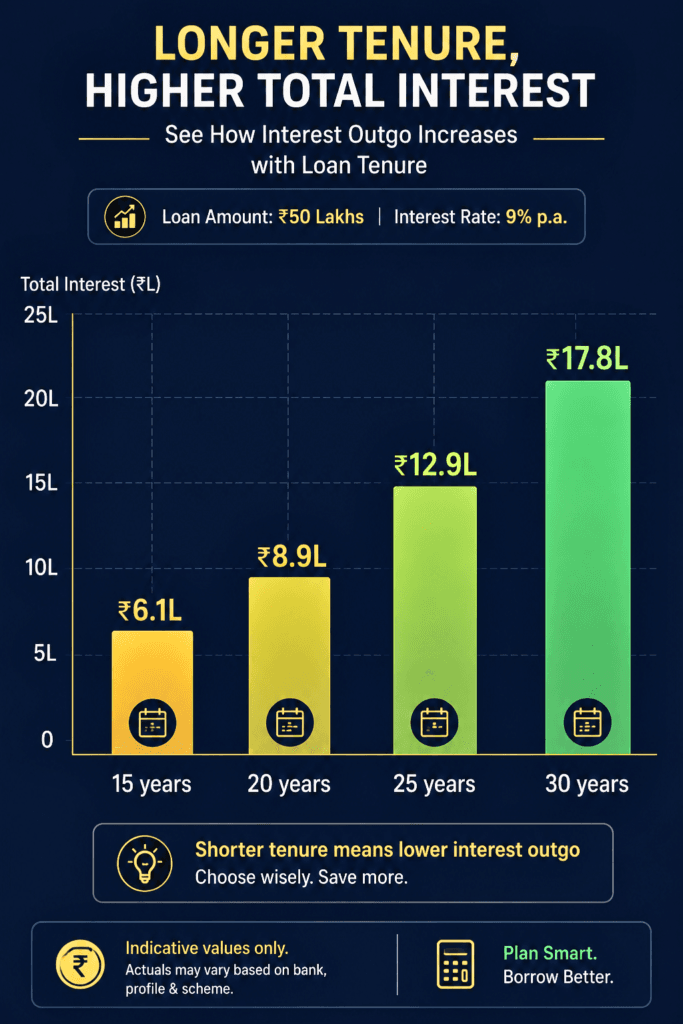

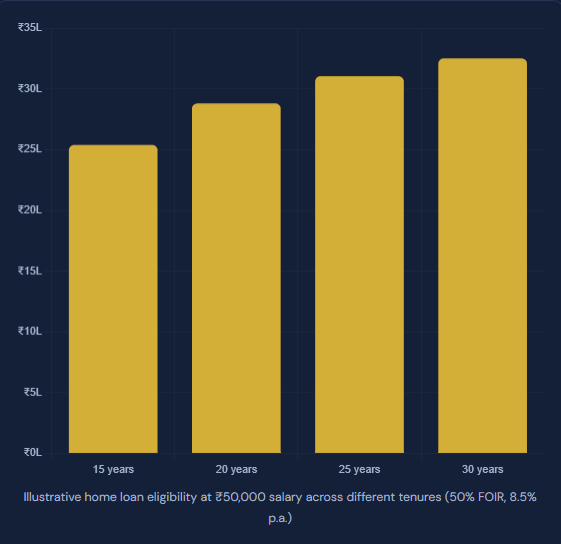

How Loan Tenure Changes Your Eligibility

Longer tenure lowers your EMI, which raises your home loan eligibility under the same FOIR cap. It also means paying interest for longer, which meaningfully increases your total repayment. Most banks cap tenure so the loan closes by age 65–70, so a 45-year-old applicant simply won’t get access to a 30-year term regardless of income.

Bank-Wise Eligibility Snapshot (SBI, HDFC, ICICI, Axis)

| Lender | Indicative Rate (2026) | Min. Net Salary | Notes |

|---|---|---|---|

| SBI | ~8.35–8.75% p.a. | ₹15,000–₹25,000 | Lower rates, government-employee concessions |

| HDFC | ~8.35–9.0% p.a. | ₹25,000+ | Faster digital processing, salaried-focus products |

| ICICI | ~8.4–9.1% p.a. | ₹25,000+ | Strong for salaried MNC/PSU employees |

| Axis Bank | ~8.4–9.2% p.a. | ₹25,000+ | Flexible tenure options, women-borrower concessions |

Bank-wise rate differences also shift your home loan eligibility slightly, since a lower rate means a lower EMI for the same loan amount. Rates move with the RBI’s policy repo rate and change frequently — always confirm the current published rate directly with the lender before applying. A 0.25% difference across lenders on a ₹50 lakh loan can still save close to ₹2 lakh in interest over 20 years, so comparing at least three offers is worth the extra hour.

6 Ways to Increase Your Home Loan Eligibility

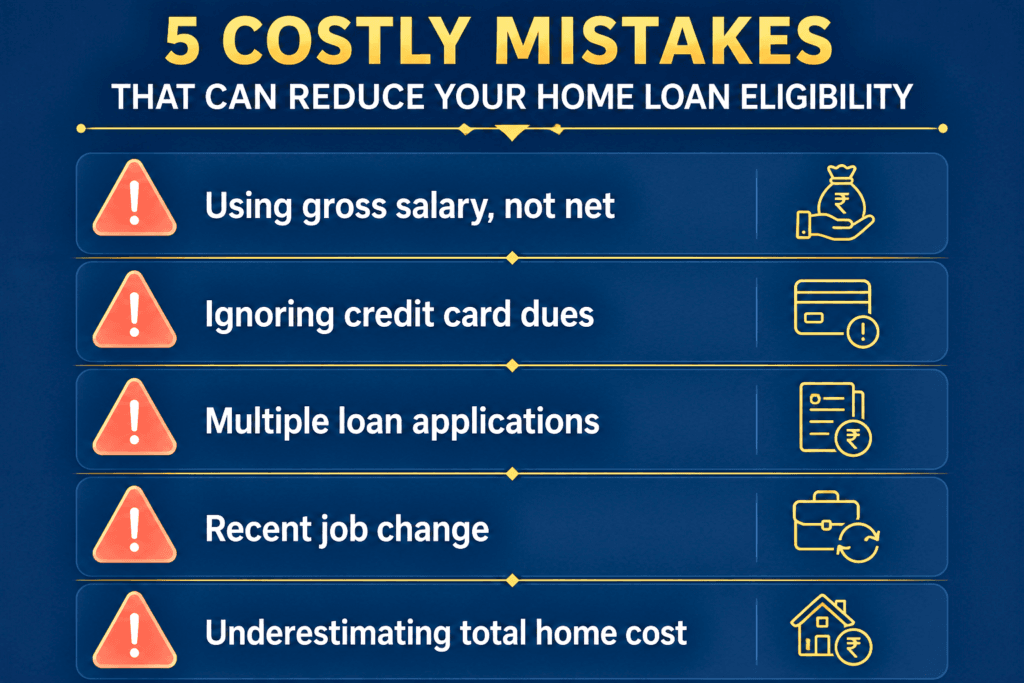

- Add a co-applicant. An earning spouse or parent merges incomes for the FOIR calculation — two ₹50,000 salaries can push combined home loan eligibility toward ₹50–55 lakh instead of ₹28–32 lakh alone.

- Clear existing EMIs first. Closing a ₹5,000 personal loan or car loan EMI typically adds ₹5–6 lakh back to your home loan eligibility.

- Extend your tenure. Moving from 20 to 25 or 30 years lowers your EMI and raises your eligible amount, at the cost of more total interest.

- Improve your CIBIL score. Six to twelve months of clean repayment history before applying can shift you into a better rate bracket and lift your home loan eligibility at the same time.

- Reduce credit card utilisation. Keeping utilisation under 30% supports a healthier FOIR and credit profile simultaneously.

- Build a larger down payment. This doesn’t raise your loan eligibility directly, but it reduces the loan amount you actually need — sometimes the more practical lever. Park this savings in an FD or grow it through a SIP while you house-hunt.

Common Mistakes That Shrink Your Home Loan Eligibility

Try This Calculation Yourself

Numbers land differently when they’re yours. Run your own salary and existing EMIs through these before you start property hunting:

- Use the Home Loan EMI Calculator to see your exact EMI across different loan amounts and tenures.

- Use the EMI Calculator to check how an existing car or personal loan EMI is eating into your FOIR room.

- Use the Mortgage Calculator to compare total interest across 15, 20, and 25-year tenures.

- Use the SIP Calculator to plan a down-payment corpus if you’re not buying immediately.

Related MoneyOra Tools: Also check the FD Calculator and PPF Calculator for parking your down-payment savings while you search for the right property.

Most home loan eligibility content stops at “55–65 times your salary” and calls it done. That shortcut is fine for a first pass, but it quietly overstates what many applicants will actually get once FOIR, existing EMIs, and CIBIL score enter the picture. In our view, the more useful mental model is to work backward from the property you actually want: calculate the EMI for that price point first, then check whether your current salary and obligations clear the FOIR bar — rather than starting from “how much can I borrow” and stretching your search to match it.

The other pattern worth flagging: co-applicant income is the single biggest eligibility lever in this entire guide, larger than tenure extension or CIBIL improvement combined, yet it’s usually mentioned as an afterthought. If a working spouse or parent is willing to be a co-applicant, run that scenario before you consider a longer tenure or a smaller property.

Expert Perspective

Here’s the trade-off nobody frames clearly enough: a longer tenure buys you a bigger loan today, but it’s really borrowing against your future self’s flexibility. A 30-year home loan taken at 30 runs until 60 — right through the years you’d otherwise want to ramp up retirement savings. Before stretching tenure purely to hit a bigger eligibility number, check what that extra interest actually costs using the Home Loan EMI Calculator, and weigh it against a smaller loan on a slightly more modest property.

Watch two things over the next few quarters: the RBI’s stance on the repo rate, since every home loan in India is now largely externally benchmarked and moves quickly with policy changes, and your own CIBIL trend — a score climbing past 750 in the months before you apply is worth more than almost any other single action you can take.

Risks to Consider

- Interest rate risk: Most home loans are floating-rate and linked to the RBI’s repo rate — your EMI can rise if rates move up after disbursement.

- Over-leverage risk: Borrowing up to the maximum FOIR limit leaves little room for other financial goals or a sudden income disruption.

- Job-stability risk: A long tenure assumes stable income for decades — a career change, business slowdown, or health event can strain repayment capacity.

- Property risk: Under-construction or unclear-title properties can delay disbursement or reduce the LTV a bank is willing to offer.

- Co-applicant risk: Adding a co-applicant increases home loan eligibility, but both parties become equally liable for the full loan, including in case of separation or dispute.

Your home loan eligibility is never just your salary multiplied by a fixed number — it’s your salary, filtered through FOIR, your existing EMIs, your CIBIL score, and your chosen tenure. Use the slab table in this guide as your starting reference, then run your exact numbers through the calculators below before you start shortlisting properties. Whether your target is ₹20 lakh or ₹1 crore, the math is the same formula scaled up — know it before the bank tells it to you.

Ready to see your exact eligibility? Run your salary, existing EMIs, and preferred tenure through the calculator now.

Use the free calculator now on MoneyOra.in

Related reading: EMI Calculator · Mortgage Calculator · Bank Calculators hub · Financial Calculators India · Hidden bank charges

This article is for educational purposes only and does not constitute financial advice. Home loan eligibility figures are indicative estimates based on standard FOIR methodology and publicly available rate information as of 2026. Actual eligibility, interest rates, and sanction amounts vary by lender, applicant profile, property, and internal credit policy — confirm current terms directly with your bank or with the National Housing Bank. Consult a qualified financial advisor before making a borrowing decision. Source references: RBI monetary policy and LTV guidelines, NHB, and the Income Tax Department (Sections 80C and 24(b) home loan deductions).

Frequently Asked Questions

How much salary is needed for a ₹50 lakh home loan?

A ₹50 lakh home loan over 20 years at around 8.5% interest needs a net monthly salary of approximately ₹85,000–₹90,000, assuming no other EMIs are running. Existing obligations reduce this available room and raise the required salary further.

Can I get a home loan with a ₹30,000 salary?

Yes. A ₹30,000 net monthly salary typically supports a home loan eligibility of roughly ₹17–19 lakh over 20 years, provided you have no major existing EMIs and a CIBIL score above 700.

How much home loan can I get on a ₹60,000 salary?

At a ₹60,000 net monthly salary with no existing EMIs, most lenders sanction between ₹34 lakh and ₹38 lakh over 20 years, rising to around ₹40–41 lakh with a 25-year tenure.

How much home loan for a ₹21,000 salary?

A ₹21,000 net monthly salary typically supports a home loan of roughly ₹12–13 lakh over 20 years, near the minimum income threshold several major lenders apply for salaried applicants.

How much home loan can I get on a ₹40,000 salary?

A ₹40,000 net monthly salary generally supports a home loan eligibility of around ₹23–25 lakh over 20 years at a 50% FOIR cap, rising to roughly ₹24–27 lakh with a 25-year tenure.

How much home loan can I get on a ₹1 lakh salary?

A ₹1 lakh net monthly salary typically supports a home loan eligibility of ₹57–65 lakh over 20 years, and closer to ₹62–70 lakh over 25 years, assuming no significant existing EMIs.

How much salary is required for a home loan of ₹1 crore?

A ₹1 crore home loan over 20 years at 8.5% interest needs an EMI of roughly ₹86,800, which requires a net monthly salary of approximately ₹1.7–1.75 lakh at a 50% FOIR cap, or a lower individual salary with a co-applicant.

What is the minimum salary required for a home loan in India?

Most lenders look for a minimum net monthly take-home of ₹15,000–₹25,000, though this varies by city and lender. Government and PSU-regulated housing finance companies sometimes accept slightly lower incomes for affordable housing loans.

Does the salary required for a home loan differ between banks like HDFC and SBI?

The underlying FOIR logic is similar across lenders, but minimum income thresholds and rate slabs vary. Public sector banks like SBI often apply slightly more flexible criteria, while private lenders like HDFC tend to have faster processing with broadly similar income requirements.

How can I increase my home loan eligibility without a co-applicant?

Clear existing EMIs and credit card dues, improve your CIBIL score, extend your loan tenure, and build a larger down payment to reduce the loan amount you actually need. These levers can meaningfully raise your eligibility even on a single income.

Pingback: Hidden Bank Charges: 9 Fees Costing You ₹2,000+ - MoneyOra