Open your bank statement right now and scroll past the salary credit, the UPI payments, the EMI debit you already know about. Keep scrolling. Somewhere in there is a line that says something like “AMB Non-Maint Chrg” or “SMS Alert Chrg Q3” or “Avg Bal Chrg.” Most people scroll right past these. They assume it is some bank processing thing. It is not. It is bank charges — and they are designed to be unnoticed. other financial mistakes salaried employees make

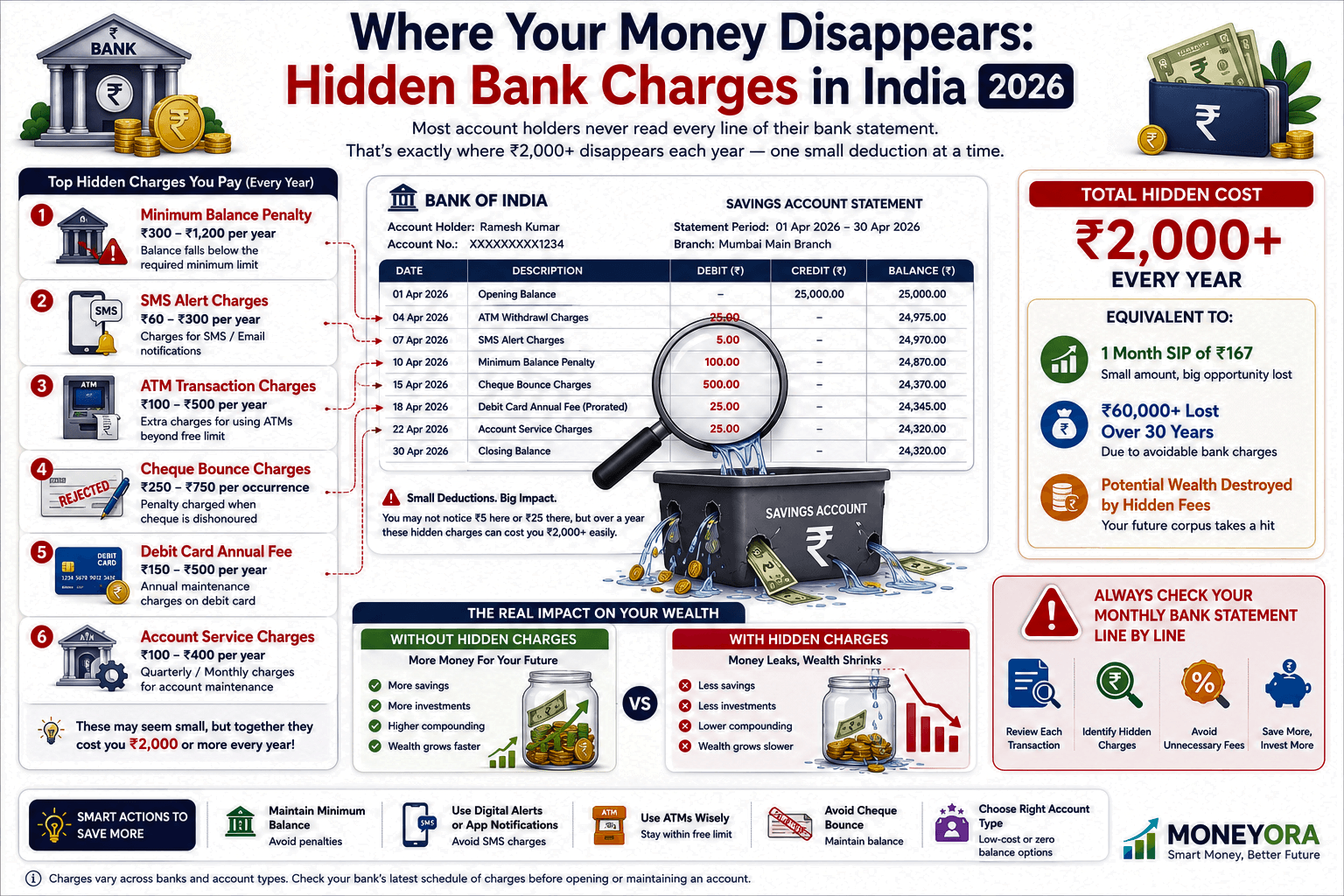

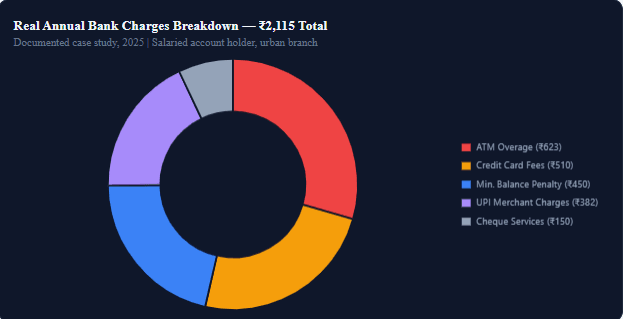

A 2025 case study tracked one millennial account holder’s annual deductions: ₹623 for exceeding ATM limits, ₹450 in minimum balance penalties, ₹382 from UPI merchant payment charges, ₹510 in credit card fees, and ₹150 for cheque-related services. Total: ₹2,115 in a single year — gone, without a single fraud alert, without a single moment of conscious spending.

That is not an edge case. SBI alone collected over ₹415 crore in minimum balance penalties in 2025 from its savings account holders. That number is not from fraud. It is from ordinary bank charges that customers either did not know existed or could not avoid.

This guide breaks down every common bank charge in India — what triggers it, how much it costs across SBI, HDFC, ICICI, Axis, and PNB, why RBI’s own rules still allow most of it, and exactly how to stop paying for things you never agreed to pay for. At the end, calculate what these charges are actually costing your long-term wealth using MoneyOra’s free SIP calculator.

Quick Answer: What are hidden bank charges in India?

Hidden bank charges in India are fees deducted from your account that are rarely communicated clearly — minimum balance penalties, ATM withdrawal charges beyond free limits, SMS alert fees, cheque bounce charges, debit card renewal fees, and cash transaction charges. Together, these can cost the average account holder ₹2,000–₹2,500 per year, often without any advance warning or easy opt-out.

Why Bank Charges Stay Hidden — And Why It’s Technically Legal

Here is the part that frustrates people once they understand it: none of this is illegal. Every bank charge covered in this article is disclosed somewhere — in a 40-page terms and conditions PDF you clicked “I agree” on, or in a fee schedule buried three menus deep on the bank’s website. The bank is not hiding anything in a legal sense. It is just not telling you in a way you would actually notice.

Compare this to how banks handle an EMI or SIP deduction. You get an SMS days in advance. You get a reminder. You get visibility. For minimum balance penalties, ATM overage charges, or SMS fees, there is no such alert system. The deduction just happens, quietly, and shows up as one line in a statement most people check only when something looks obviously wrong.

The Reserve Bank of India does regulate some of this — minimum free transactions, for instance, are mandated. But the actual fee amounts beyond the free limit are set by individual banks, and they vary widely. This is exactly why a side-by-side comparison matters so much, and why most people have no idea their bank is charging more than a competitor for the same exact thing.

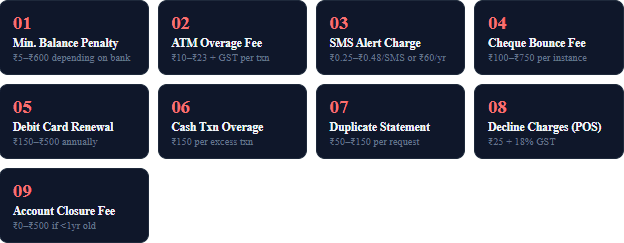

All 9 Hidden Bank Charges in India — Explained

1 – Minimum Average Balance Non-Maintenance Penalty

This is the reason for bank charges in India. Banks want you to keep an amount of money in your account every month or every few months. This amount can be anywhere from ₹500 to ₹10,000. It depends on where your bank’s what kind of account you have. If you do not have money in your account you have to pay a penalty. The penalty is based on how money you are short.

The way banks calculate the penalty can be confusing. Let us say your bank wants you to keep ₹10,000 in your account. If you only have ₹6,000 in your account on average that means you are ₹4,000. This is a 40% shortfall. Different banks use formulas to calculate the penalty. That is why you might pay an amount of money to different banks even if you are short the same percentage of money. You can see this in the comparison table.

2 – ATM Withdrawal Charges Beyond Free Limit

The Reserve Bank of India says you can use your banks ATM for five times a month. You can also use banks ATMs for free three or five times a month depending on where you live. If you use the ATM more than that you have to pay a fee. You pay this fee for taking out cash and for checking your balance. The fee is usually ₹10 to ₹21 plus tax for taking out cash. It is usually around ₹8.50 for checking your balance at another banks ATM.

3 – SMS Alert Charges

Most banks charge you money for sending you messages about your account. They charge ₹0.25 to ₹0.48 per message.. They charge a flat fee of ₹15 every few months. This is ₹60 per year. This is even though banks say that using their websites and apps is free. Banks have actually asked the Reserve Bank of India if they can stop sending messages for transactions. This is because it costs them a lot of money to send all those messages.

4 – Cheque Bounce Charges

If you write a cheque and you do not have money in your account the bank will charge you a penalty. This penalty can be ₹100 to ₹750. The State Bank of India charges around ₹150 plus tax if the cheque is for than ₹1 lakh. This is not the problem you will have if you bounce a cheque. It is also against the law. You can go to jail for up to two years. Pay a fine. The fine can be twice the amount of the cheque. Most people do not know about this. They only know about the banks penalty.

5 – Debit Card Annual/Renewal Fees

Many bank accounts come with a debit card. You have to pay a fee every year to keep this card. The fee can be ₹150 to ₹500. The bank will take this money from your account automatically. They do this even if you do not use the card. If you have a card you do not use you are still paying for it. You have to tell the bank to cancel it if you do not want to pay the fee.

6 – Cash Deposit and Withdrawal Charges

If you put cash into your account or take cash out of your account at the bank you might have to pay a fee. This is if you do more than a number of transactions per month. The fee can be around ₹150 per transaction. This affects people who own businesses more than people who work for someone else. This is because they handle cash often.

7 – Duplicate Statement and Passbook Charges

If you need a paper copy of your account statement you might have to pay a fee. This can be ₹50 to ₹150. You might need this for a loan or a visa. Some banks also charge a fee if you want them to update your passbook often.

8 – Transaction Decline Charges

If you try to take out cash from an ATM or pay for something with your card but you do not have money the bank might charge you a fee. This fee can be around ₹25 plus tax. This is frustrating because you are paying a fee even though the transaction did not go through.

9 – Account Closure Fee

If you close your bank account within a year of opening it you might have to pay a fee. This fee can be ₹0, to ₹500. The bank does this to stop people from opening and closing accounts often.. It can also affect people who open an account for a short time. For example you might open an account to get your salary. If you close it after you might have to pay a fee.

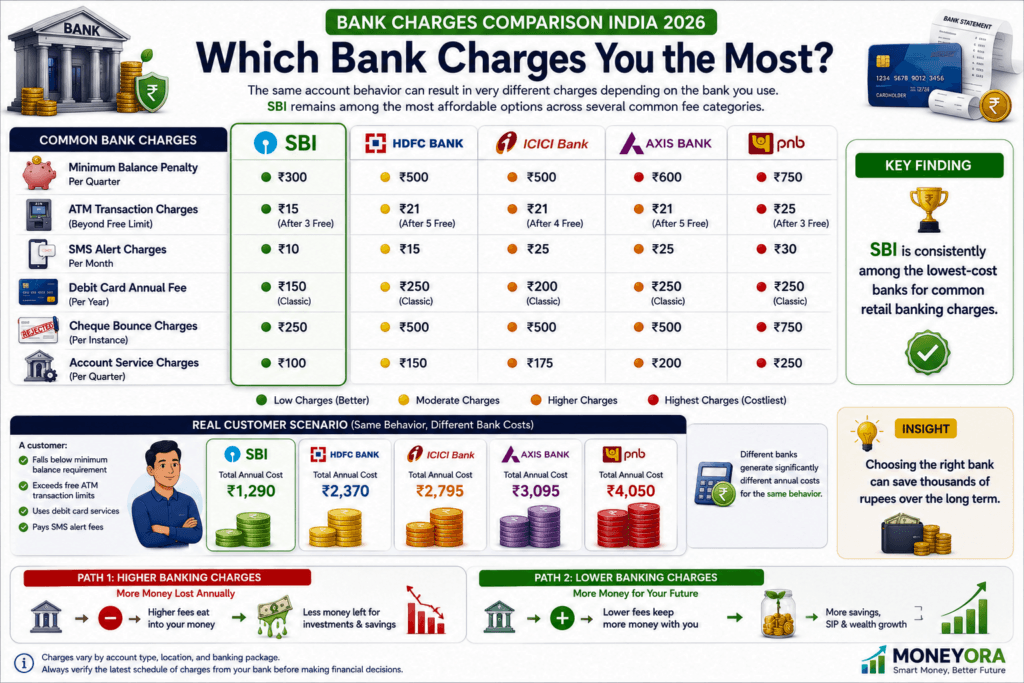

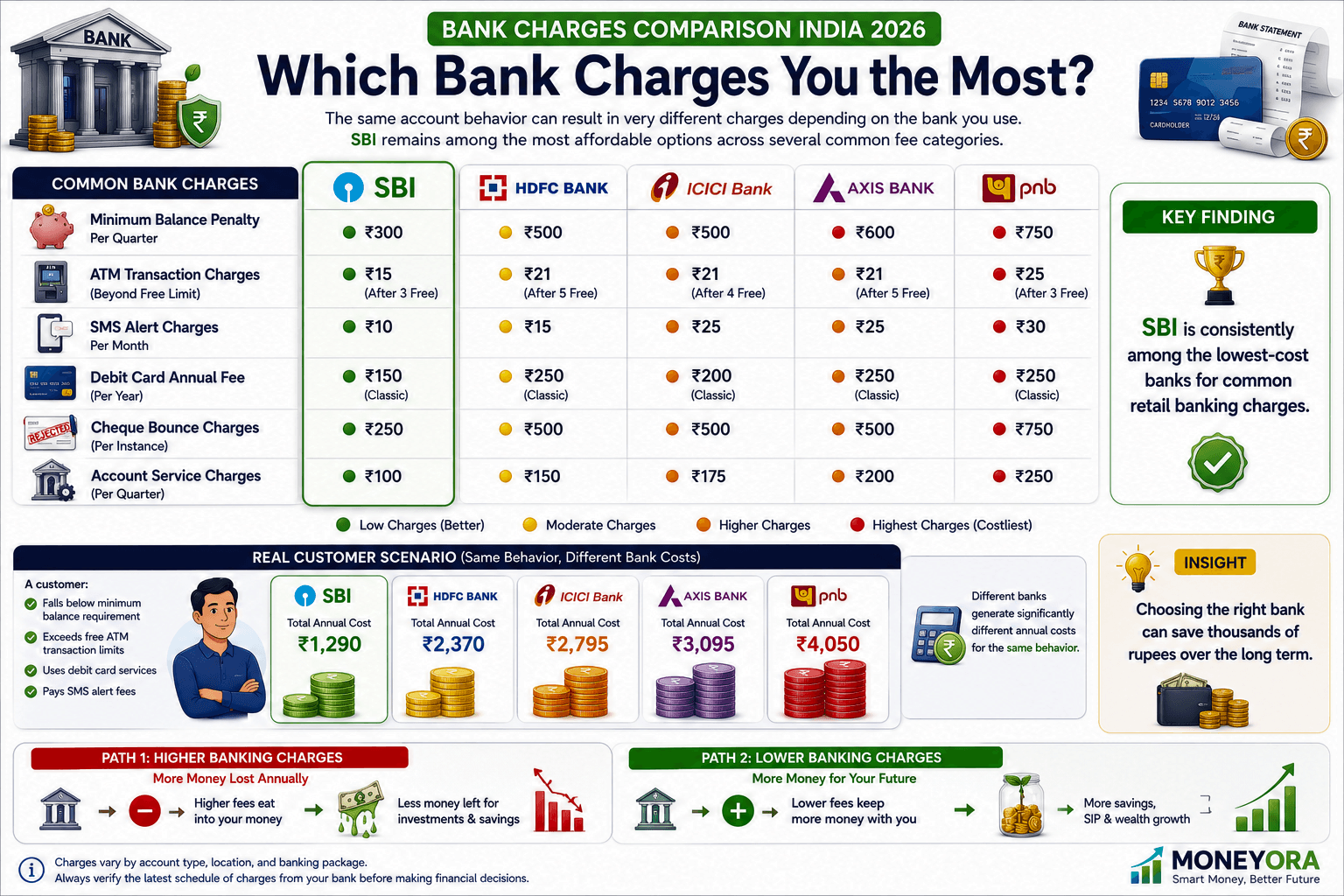

SBI vs HDFC vs ICICI vs Axis vs PNB — Full Bank Charges Comparison

| Charge Type | SBI | HDFC Bank | ICICI Bank | Axis Bank |

|---|---|---|---|---|

| Min. Balance Penalty | ₹10–₹15 + GST | ₹150–₹600 | ₹100 + 5% shortfall | ₹150–₹500 |

| ATM Own-Bank Overage | ₹10 + GST | ₹21 + taxes | ₹20 + GST | ₹20–₹21 |

| ATM Other-Bank Overage | ₹23 + GST | ₹23 + taxes | ₹21 + GST | ₹21 |

| SMS Alert (annual) | ~₹60 | ~₹60 | ~₹60 | ~₹60 |

| Cheque Bounce | ~₹150 + GST | ₹200–₹500 | ₹200–₹350 | ₹250–₹500 |

| Debit Card Annual Fee | ₹150–₹300 | ₹150–₹750 | ₹150–₹500 | ₹150–₹500 |

| Foreign ATM Fee | ₹100 + 3.5% | ₹125 + taxes | ₹125 + 3.5% | ~₹150 + taxes |

| Free ATM Txns/Month (Own) | 5 | 5 | 5 | 5 |

The clearest pattern: SBI is consistently the cheapest across almost every bank charge category, especially minimum balance penalties — its ₹10–₹15 + GST is a fraction of HDFC’s ₹150–₹600. This is one reason SBI remains India’s largest bank for mass-market savings accounts despite the recent controversy over its penalty hikes (covered in detail below). Private banks generally charge more across the board but often provide more digital convenience and faster service — whether that trade-off is worth it depends on how often you actually trigger these charges.

The RBI Rule That Most People Are Not Aware Of

Here is something the Reserve Bank of India has a rule about free transactions. The RBI says that banks must give their savings account holders a number of free transactions every month.

* At their banks ATMs they should get at least 5 free transactions per month.

For ATMs of banks the rules are a bit different.

* In cities like Mumbai, New Delhi, Chennai, Kolkata, Bengaluru and Hyderabad you get 3 free transactions per month.

* In areas you get 5 free transactions per month.

You can find details on the Reserve Bank of Indias website. They publish rules about customer service in banks.

The thing is, this rule only sets a minimum. Banks can charge more if they want to. They can also decide on their minimum balance requirements and penalties. The RBI only says how free transactions you should get, not how much banks can charge for extra transactions. This is why different banks have charges. The RBI rule explains the minimum, but not the wide range of charges.

The Reserve Bank of India’s official website, does not regulate the amount of most bank charges.The RBI mandate is 3 transactions per month in 6 metro cities and 5 free transactions in non-metro areas.

The RBI stated that banks should offer their savings bank account holders a minimum of five financial transactions per month at their own banks ATMs.

The Reserve Bank of India publishes its master circulars on customer service, in banks.

Real Example: Where ₹2,115 Disappeared in One Year

| Charge Category | Annual Amount | % of Total |

|---|---|---|

| ATM withdrawal limit overage | ₹623 | 29.5% |

| Minimum balance penalties | ₹450 | 21.3% |

| Credit card-related fees | ₹510 | 24.1% |

| UPI merchant payment charges | ₹382 | 18.1% |

| Cheque-related services | ₹150 | 7.1% |

| TOTAL | ₹2,115 | 100% |

None of these were one large, obvious deduction. Each individual entry looked small enough to ignore — ₹20 here, ₹150 there. That is precisely the design problem. A single ₹2,000 deduction triggers scrutiny. Ten ₹200 deductions across a year usually do not.

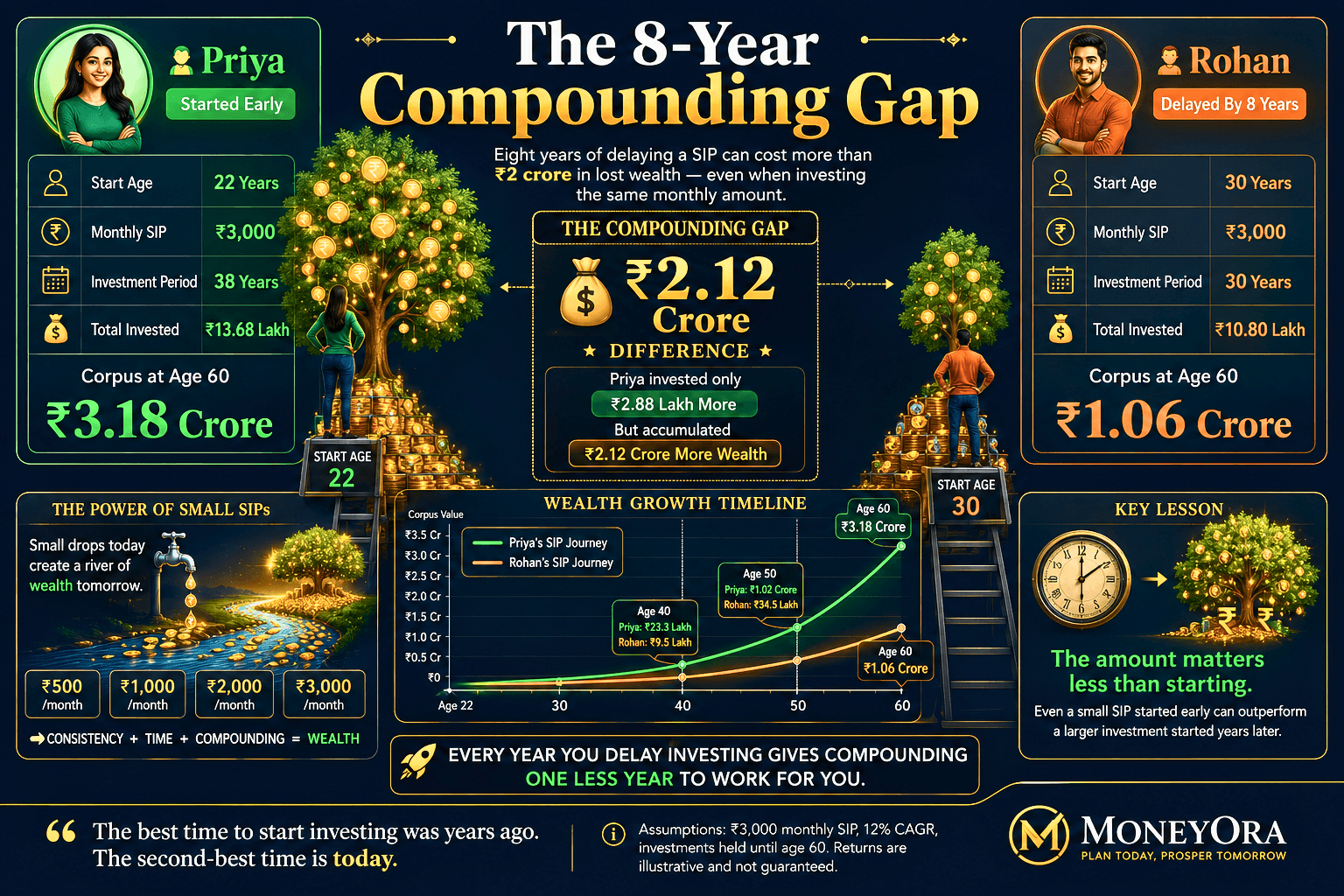

The Real Cost: What ₹2,000/Year in Bank Charges Is Worth Over 20 Years

This is the calculation no other article on this topic makes — and it is the one that should actually motivate you to act.

₹2,000 a year does not sound dramatic in isolation. But money that goes to bank charges is money that never gets invested. If you redirected that same ₹2,000 per year (roughly ₹167/month) into an equity mutual fund SIP at 12% CAGR instead of losing it to fees, here is what it would be worth:

| Duration | Total “Saved” from Charges | If Invested at 12% CAGR Instead |

|---|---|---|

| 5 years | ₹10,000 | ₹13,230 |

| 10 years | ₹20,000 | ₹38,650 |

| 15 years | ₹30,000 | ₹84,280 |

| 20 years | ₹40,000 | ₹1,66,400 |

| 30 years | ₹60,000 | ₹5,84,500 |

Over 30 years, bank charges that you can avoid by redirecting into a SIP could be worth nearly ₹5.85 lakh. It’s not that ₹2,000 a year is a lot. Compounding turns small, regular leaks into big costs over time, just like it makes small, steady investments valuable. Use MoneyOra’s SIP calculator to model your own number. Just enter your actual annual bank charges after you do the audit in the section below.

Pro Tip: This is not theoretical. The ₹100 or ₹200 you save each month by avoiding an ATM fee or a minimum balance penalty is the same ₹100 or ₹200 that, if invested regularly, can build real wealth. Our lumpsum calculator and CAGR calculator can help you view this from different angles.

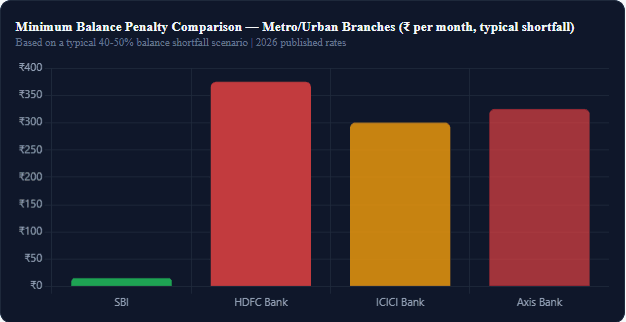

The SBI Minimum Balance Controversy, When the Government Stepped In

This part of the bank charges story deserves more attention. When SBI announced plans to raise its minimum balance penalty, it affected over 310 million savings account holders. The penalty could reach ₹100 for savings accounts and ₹500 for current accounts, while the minimum balance increased to ₹5,000 for branches in six metro cities.

The response was strong enough that the Indian government formally asked SBI to rethink its decision. The government also urged SBI and other lenders, including private banks, to reconsider charges on cash transactions and ATM withdrawals above certain limits. This was a concern for financial inclusion since many of SBI’s customers are low-income, rural, and first-time bank account holders under schemes like Jan Dhan Yojana.

This episode is important for two reasons. First, it shows that bank charges are not fixed rules. They are business choices that change in response to public and political pressure when enough attention is given. Second, it explains why SBI’s current charges, while still present, are lower than many private banks today; public scrutiny created a lasting deterrent against steep fee increases.

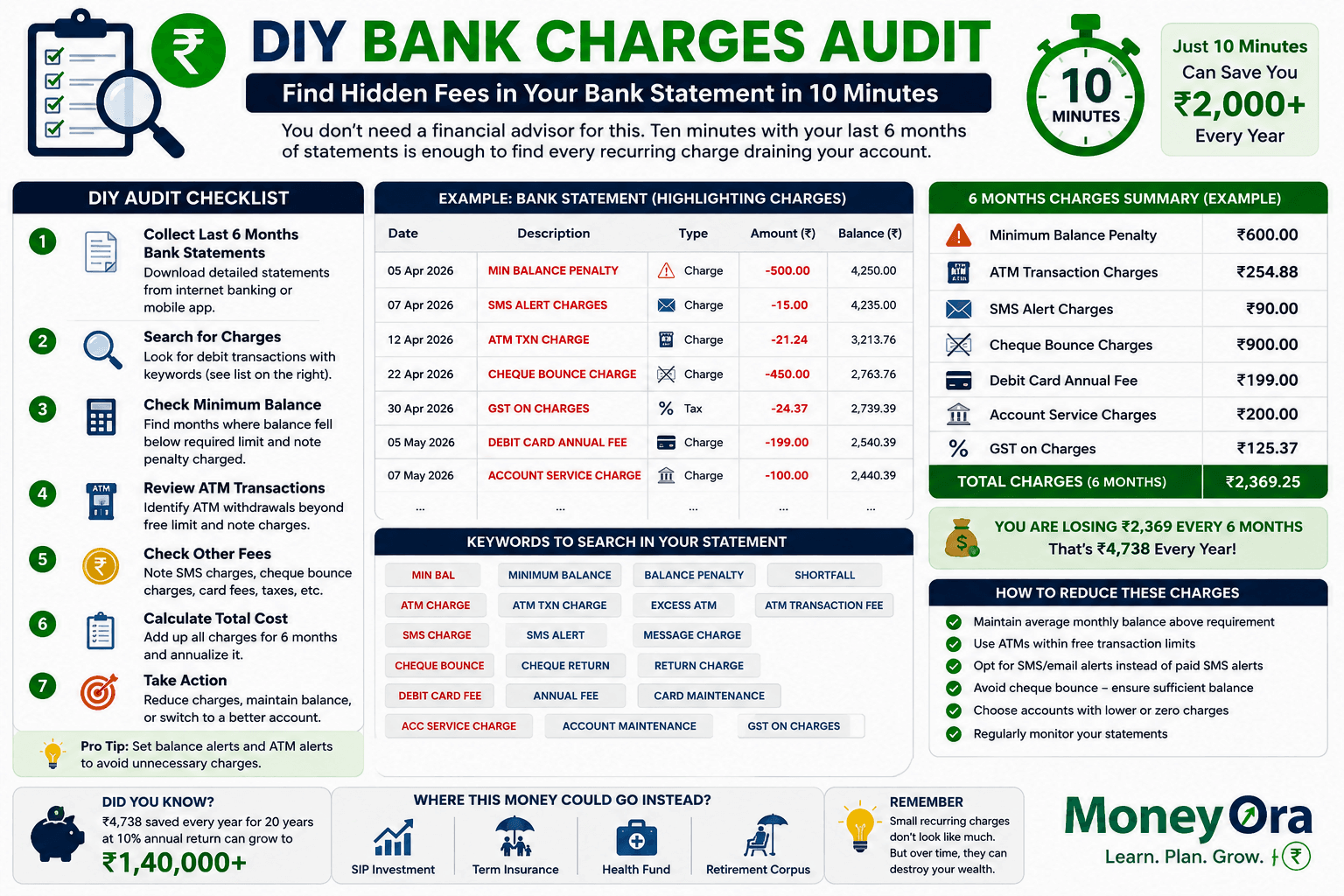

DIY Bank Statement Audit: Find Your Own Hidden Bank Charges in 10 Minutes

Do this right now. Log into your net banking or mobile banking app and pull up the last six months of statements. Look specifically for these line items; they often use shorthand that is easy to miss:

Search for “AMB” or “Avg Bal.” This is your minimum balance penalty. If you see it more than once in six months, your balance management needs attention.

Search for “SMS” or “Alert Chrg.” This is usually a small quarterly fee. Check if you can switch to email alerts to eliminate it.

Search for “ATM” combined with any rupee amount. Count how many ATM transactions you made in a month. If you exceeded five at your own bank or three at other banks (in metros), you are paying extra fees.

Search for “Cheque Return” or “CHQ RET.” This means a bounced cheque charge. If this appears even once, check if it was due to a balance issue you can prevent in the future.

Search for “Debit Card AMC” or “Card Fee.” This is the annual card maintenance fee. If you rarely use this card, consider downgrading or canceling it.

Search for “POS Decline” or “Insufficient Funds.” These are charges for failed transactions. They add up quickly if your balance is low often near month-end.

Add up everything you found over the last six months and multiply by two. That is your estimate for annual bank charges. Compare it to the ₹2,115 example above.

After you have your number, plug it into the SIP calculator as a monthly figure to see how much avoiding these charges and investing the saved amount could be worth over time.

How to Avoid Every One of These Bank Charges:

1. Switch to a Zero-Balance Account If You Can’t Maintain AMB Consistently.

Most major banks now offer Basic Savings Bank Deposit Accounts (BSBDA) or zero-balance digital accounts with no minimum balance requirement. If you struggle to keep ₹5,000 to ₹10,000, this switch eliminates your biggest bank charges.

2. Use Your Own Bank’s ATM and Bundle Withdrawals.

Instead of withdrawing ₹2,000 five times a week, take out a larger amount less often to stay within the free transaction limit. Stick to your own bank’s ATM network when possible since the extra charge is usually lower than at other banks.

3. Switch SMS Alerts to Email Where Possible.

Most banks let you choose email-only transaction alerts instead of SMS, at no cost. Check your net banking settings under “Alerts & Notifications.” This change can eliminate the ₹60 yearly SMS fee entirely.

4. Never Issue a Cheque Without Checking Your Balance First.

Before writing any cheque, especially for a large amount, check your balance through net banking. A ₹150 to ₹500 bounce fee plus possible legal issues is avoidable with a quick balance check.

5. Audit and Cancel Unused Debit Cards.

If you have a second account you rarely use — perhaps from a previous employer’s salary account — check if the debit card has an annual fee. If you have switched entirely to UPI, ask the bank to deactivate or downgrade the card to a no-fee version.

6. Keep a Buffer Above Your Required Minimum Balance.

Don’t run your balance to the exact minimum required amount. Banks calculate AMB as an average over the month. A few days below the line can still trigger penalties. Keep a small buffer (10 to 15% above the requirement) to avoid edge-case penalties.

7. Compare Banks Before Opening a New Account.

If you are opening a new account for a new job, city, or to consolidate, use the comparison table above as your reference. SBI’s lower fee structure in most categories makes it a reasonable choice for a primary account, while private banks may be worth it if you value their digital services or specific features.

For broader financial planning regarding your banking and loans, tools like MoneyOra’s EMI calculator, IFSC code finder, and bank details finder can help you manage banking tasks more efficiently.

Tools That Help You Stop Losing Money to Fees

- SIP Calculator — See what your “saved” bank charges could be worth if invested instead

- FD Calculator — Compare what your minimum balance could earn as a fixed deposit instead

- RD Calculator — Plan a recurring deposit with the money you save from avoided charges

- PPF Calculator — Redirect saved bank charges into a tax-free long-term instrument

- Lumpsum Calculator — Model a one-time investment of your accumulated savings from fee avoidance

- CAGR Calculator — Calculate the real annualised cost of recurring bank charges

- EMI Calculator — Plan loan repayments without missing payments that could trigger penalties

- IFSC Code Finder — Find correct bank branch codes to avoid failed-transfer charges

- Bank Details Finder — Verify account details before transfers to avoid reversal charges

None of the nine bank charges covered in this guide require a lawsuit or a complaint to the banking ombudsman to fix. Almost every one of them is avoidable through small, deliberate habits — checking your balance before writing a cheque, switching to email alerts, bundling your ATM withdrawals, keeping a small buffer above the minimum requirement.

The hard part is not the fix. The hard part is noticing the problem in the first place, because banks have very little incentive to make these charges obvious. A statement full of small ₹20 and ₹150 deductions rarely triggers the same scrutiny as one large unexplained debit — even though, over a year, the small deductions can easily add up to more.

You now have the checklist. You have the bank-by-bank comparison. You have the actual rupee number — ₹2,115 in a real documented case — that shows exactly how this happens to ordinary, careful people. The only step left is the ten minutes it takes to open your own statement and check.

What you find might be small. It might also be the first ₹2,000 of a much larger habit you can build — one where money that used to leak out quietly instead compounds quietly, in your favour.

Use the Free Calculator Now on MoneyOra.in

Found ₹2,000 a year in avoidable bank charges? See what that same amount could become if invested consistently instead.

Open SIP Calculator →

Use the free calculator now on MoneyOra.in — also explore our FD calculator, PPF calculator, lumpsum calculator, and CAGR calculator for your complete financial planning toolkit.

Disclaimer: Bank charge rates mentioned in this article are based on published rate cards as of 2026 and are subject to change. Always verify current charges on your bank’s official website or with your branch before making decisions. This article is for informational purposes only and is not financial advice.

What are the most common hidden bank charges in India?

The most common bank charges in India are: minimum balance (AMB) non-maintenance penalty, ATM withdrawal charges beyond the free limit, SMS alert charges, cheque bounce fees, debit card annual/renewal fees, cash deposit/withdrawal charges beyond free limits, duplicate statement charges, account closure fees, and POS/ATM decline charges. Together these can cost an average account holder ₹2,000–₹2,500 per year without them realising it.

How much is the minimum balance penalty in SBI, HDFC, ICICI?

SBI charges ₹5–₹15 plus GST based on the shortfall percentage. HDFC Bank charges ₹150–₹600 depending on balance shortfall in metro/urban branches. ICICI Bank charges ₹100 plus 5% of the shortfall amount. SBI alone collected over ₹415 crore in minimum balance penalties in 2025 from its savings account holders — making it the largest single source of bank charges revenue among India’s retail banks.

How many free ATM transactions does RBI allow per month?

The RBI mandates a minimum of 5 free financial transactions per month at your own bank’s ATMs. For other banks’ ATMs, the mandate is 3 free transactions per month in 6 metro cities and 5 free transactions in non-metro areas. Beyond these limits, banks can charge up to ₹21 plus GST per financial transaction and around ₹8.50 per non-financial (balance check) transaction.

What is the SMS alert charge from banks?

Most Indian banks charge ₹0.25 to ₹0.48 per SMS, or a flat quarterly fee of approximately ₹15 (₹60 annually) for transaction alerts — despite digital banking being marketed as free. You can typically switch to free email alerts through your net banking settings to avoid this bank charge entirely.

What happens if a cheque bounces in India?

A bounced cheque attracts a bank penalty of ₹100–₹750 depending on the bank — SBI charges approximately ₹150 plus GST for amounts up to ₹1 lakh. Beyond the bank charge, cheque bounce is also a criminal offence under Section 138 of the Negotiable Instruments Act, punishable with up to 2 years imprisonment or a fine of up to twice the cheque amount, or both.

How can I avoid hidden bank charges in India?

To avoid hidden bank charges: maintain the required minimum balance or switch to a zero-balance account, limit ATM withdrawals to the free quota, switch to email alerts instead of SMS, never issue a cheque without confirming sufficient balance, cancel unused debit cards with annual fees, keep a buffer above your minimum balance requirement, and audit your statement every quarter for unexplained deductions using the checklist in this guide.

Did the government intervene on SBI’s minimum balance charges?

Yes. The Indian government previously asked SBI to reconsider penalty charges on non-maintenance of minimum balance after the bank announced hikes affecting over 310 million savings account holders, with penalties as high as ₹100 for savings accounts and ₹500 for current accounts. The government also urged SBI and other lenders to reconsider ATM and cash transaction charges, citing concerns about financial inclusion for lower-income account holders.