FD vs Liquid Fund: Which Actually Wins in 2026?

Ask ten people where to park idle money and most will say “FD” without thinking twice. It’s the familiar answer, not necessarily the better one in the FD vs liquid fund decision. A liquid fund solves a similar problem — parking money safely for the short term — but does it with faster access and, for many taxpayers, a real edge on how the tax bill lands.

This guide skips the vague “both are good options” conclusion and puts real FD vs liquid fund numbers side by side: what ₹1 lakh actually earns in each, how the tax treatment genuinely differs, and which one fits specific situations like an emergency fund or a lump sum waiting to be deployed. By the end, the FD or liquid fund question should have a concrete answer for your specific situation rather than a generic “it depends.”

Once you’ve decided, you can run your own numbers using MoneyOra’s FD calculator to see the exact maturity value for your amount and tenure.

1. FD vs Liquid Fund: The Real Difference in One Line

Quick answer: An FD is a bank’s promise of a fixed return in exchange for you not touching the money for a set period. A liquid fund is a mutual fund that lends your money to banks, the government, and large companies for very short periods (up to 91 days), giving market-linked but historically stable returns with much faster access.

Both exist to solve the same basic problem — keeping money safe while it isn’t actively working toward a bigger goal — but they trade off differently on certainty versus flexibility. An FD locks in a rate today, for better or worse, regardless of what happens to interest rates later. A liquid fund’s return moves gently with short-term market rates, which usually works in the investor’s favour but isn’t contractually guaranteed the way an FD’s rate is.

Why this comparison keeps coming up: The FD vs liquid fund question resurfaces every time someone receives a bonus, sells an asset, or simply wants somewhere better than a savings account to park money for a few months to a few years. Neither instrument is “wrong” — the right answer in the FD vs liquid fund debate depends entirely on your time horizon, tax bracket, and how quickly you might need the money back.

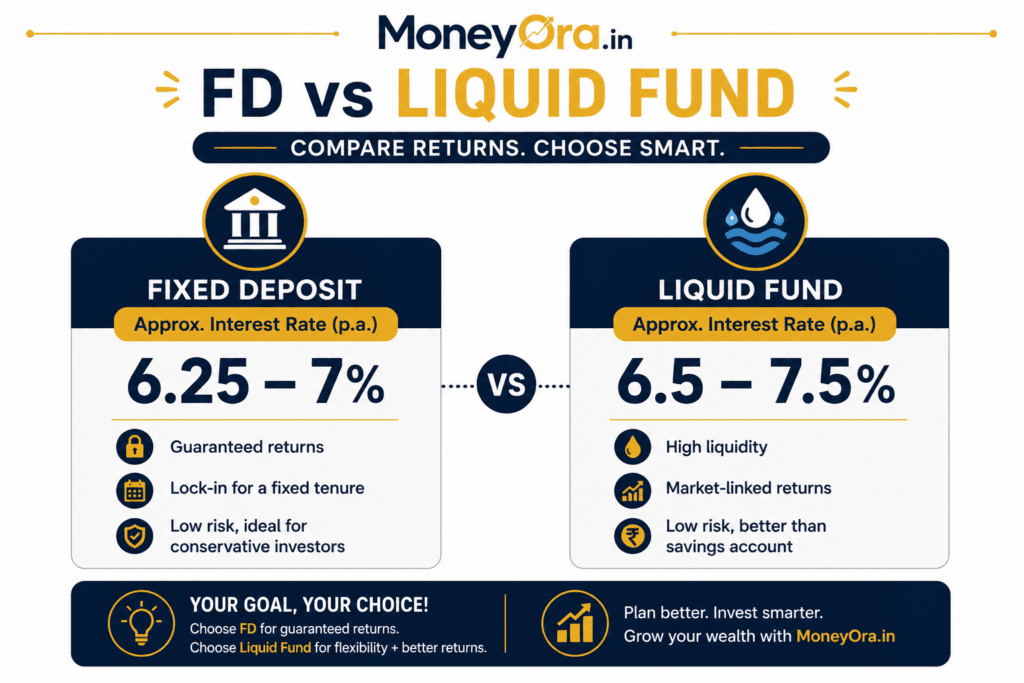

2. Returns Compared: What ₹1 Lakh Actually Earns in FD vs Liquid Fund (2026)

In the FD vs liquid fund returns comparison, most Indian banks currently offer 1-year FD rates in the roughly 6.25–7% range, locked at the time of deposit and unaffected by any market movement afterward. Liquid funds have typically delivered returns in a similar or slightly higher 6.5–7.5% band over the past year, though — unlike an FD — that number isn’t contractually fixed and moves with short-term money-market conditions.

Simple example: ₹1 lakh parked for one year at a 6.5% FD rate grows to roughly ₹6,500 in interest. The same ₹1 lakh in a liquid fund averaging 7% over the year would earn closer to ₹7,000, with the added detail that liquid fund returns compound daily rather than at fixed quarterly intervals like most bank FDs.

Original calculation — 3-year horizon: A reader with ₹5 lakh to park for exactly 3 years, choosing between a 7% FD and a liquid fund averaging 7% pre-tax, would see near-identical headline returns before tax. The real separation between the two doesn’t show up in the returns table at all — it shows up in Section 3, once taxation enters the picture.

Beginner trap: Comparing only the advertised rate and assuming the FD vs liquid fund winner is obvious. The pre-tax numbers are often close enough that returns alone rarely settle the FD vs liquid fund decision — tax treatment usually does.

3. Taxation Compared: Where the Real FD vs Liquid Fund Gap Is

This is the section that actually decides most FD vs liquid fund decisions, and it’s the part most casual FD vs liquid fund comparisons gloss over.

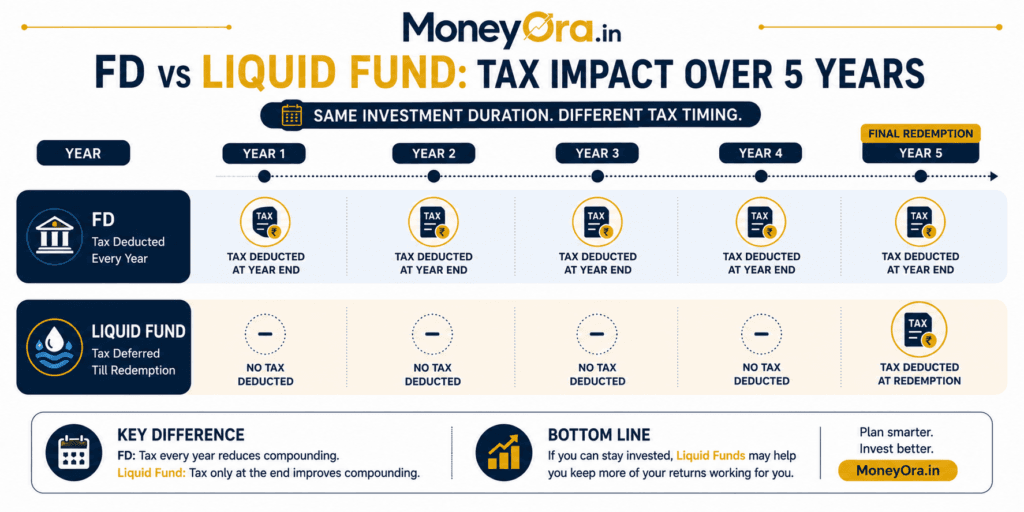

FD taxation: Interest earned on a bank FD is fully taxable every year as “Income from Other Sources,” added to your total income and taxed at your slab rate — 5%, 20%, or 30%, whichever applies. This happens annually even on a cumulative FD where you haven’t actually received any cash yet. Banks deduct TDS at 10% once annual interest crosses ₹40,000 (₹50,000 for senior citizens), but TDS isn’t your final tax — if your slab rate is higher, you owe the difference at return-filing time.

Liquid fund taxation: Gains are taxed only when you actually redeem, not annually on paper gains. There’s no TDS at all for resident Indian investors. For most debt-oriented mutual funds bought after 1 April 2023 (which includes liquid funds), gains are taxed at your income slab rate without indexation benefit — so the tax rate ends up similar to an FD for most investors, but the timing is very different.

Why timing matters more than people expect: With an FD, tax is deducted every single year, which means the portion that goes to the government stops compounding for you immediately. With a liquid fund, your entire corpus — including the portion that will eventually be taxed — keeps compounding until the day you redeem. On a larger sum held over several years, that deferral advantage adds up to a meaningfully larger final amount, even when both instruments earn the same headline rate.

Custom calculation: On roughly ₹50 lakh held over 10 years, the tax-deferral advantage of a liquid fund over an equivalent-return FD can amount to a difference of several lakh rupees, purely from letting the taxable portion continue compounding each year instead of being deducted annually.

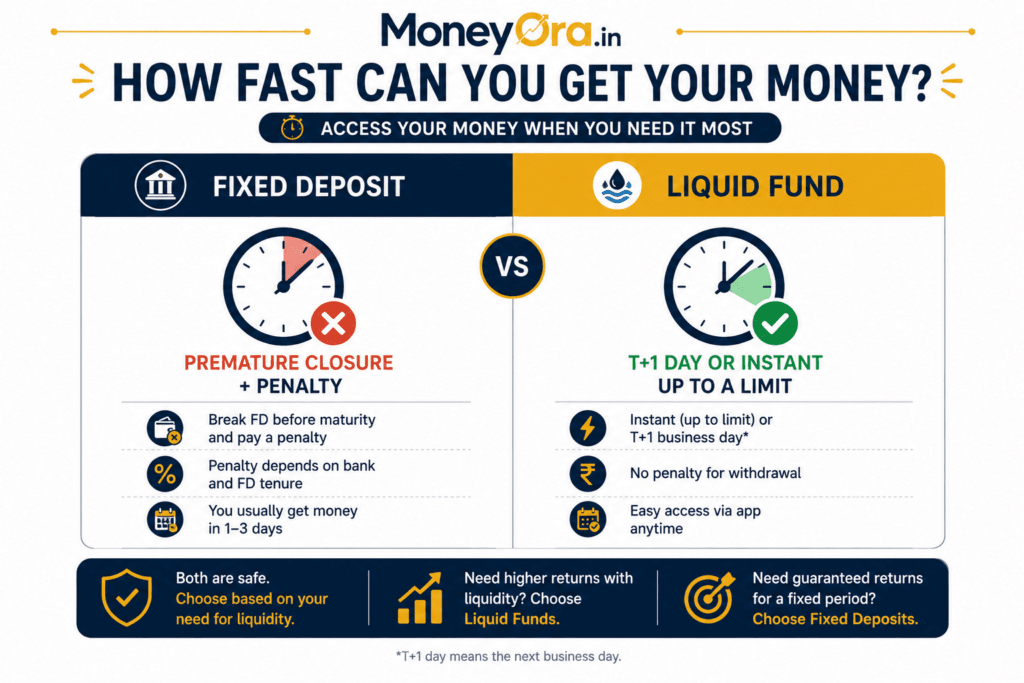

4. Liquidity Compared: How Fast Can You Actually Get Your Money?

In the FD vs liquid fund liquidity comparison, an FD, once locked, generally requires premature closure to access funds early, which usually triggers an interest-rate penalty of 0.5–1%, applied to the whole tenure held so far — not just the days you’re short of maturity.

A liquid fund typically credits redemption within 1 business day (T+1), and many fund houses offer instant or same-day redemption up to a limit (commonly around ₹50,000, AMC-dependent). A small exit load may apply only if you redeem within the first 6–7 days of investing; after that window, there’s usually no exit load at all.

Practical difference: If an unexpected expense comes up on a Tuesday, a liquid fund investor can typically have the money by Wednesday with little to no penalty. An FD holder facing the same situation either breaks the FD early (losing accrued interest) or scrambles for funds elsewhere. https://www.rbi.org.in

5. Risk Compared: Is a Liquid Fund as Safe as an FD?

Not identical, but close for most practical purposes when weighing FD vs liquid fund risk. A bank FD carries virtually no market risk and is protected by DICGC deposit insurance up to ₹5 lakh per depositor per bank — an important detail if you’re parking a large sum in a smaller or cooperative bank chasing a higher advertised rate.

A liquid fund carries low but non-zero risk. Because it invests in very short-term instruments (treasury bills, high-quality commercial paper, certificates of deposit with maturities up to 91 days), it’s minimally affected by interest rate swings, and losses are rare — but not impossible in stress scenarios involving a credit default in the underlying portfolio.

Beginner trap: Assuming “safe” and “FD” are synonyms and stopping the risk analysis there. A 9% FD from a small finance bank sounds appealing, but DICGC insurance still caps at ₹5 lakh — parking ₹20 lakh in one such account for the extra yield means ₹15 lakh is genuinely uninsured if that bank fails. A well-chosen liquid fund investing in high-quality instruments can, in that specific comparison, carry a more diversified and arguably lower practical risk than concentrating a large sum in a single small bank’s FD.

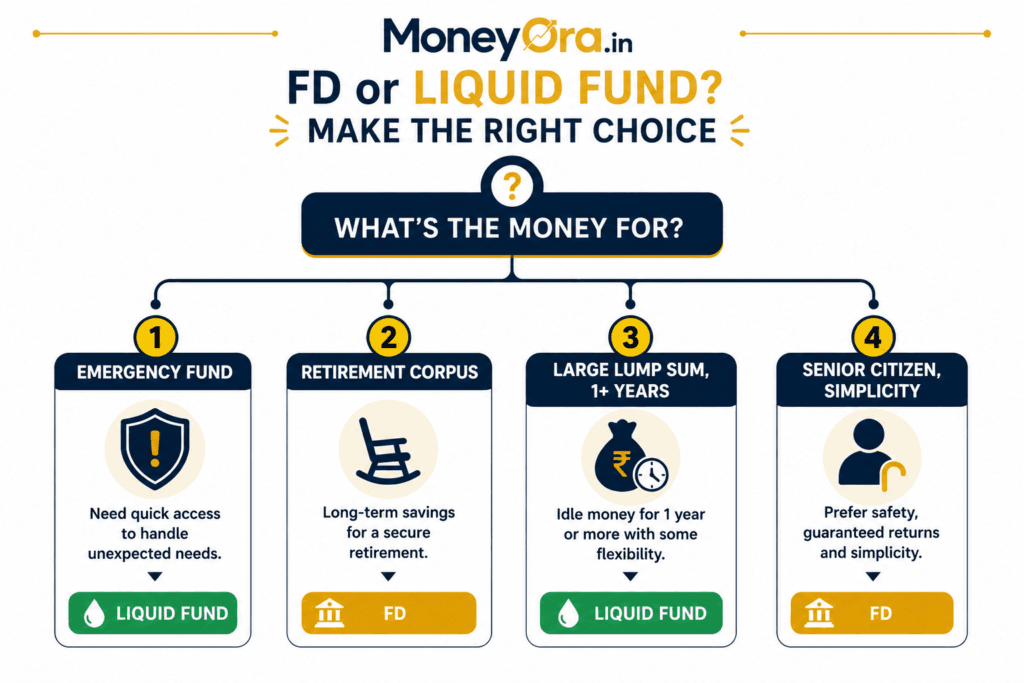

6. Which One Fits Your Situation? (FD vs Liquid Fund by Use Case)

| Your Situation | Better Fit | Why |

|---|---|---|

| Emergency fund | Liquid fund (with a small savings-account buffer) | Fast access, no penalty for withdrawal timing |

| Money for a fixed date 1–3 years out | Either — compare current rates | Similar pre-tax returns; liquid fund edges ahead post-tax for most slabs |

| Retirement corpus, capital protection priority | FD | Contractual certainty matters more than a small return edge as you approach retirement |

| Large lump sum (bonus, sale proceeds) parked temporarily | Liquid fund | Tax deferral advantage compounds meaningfully on larger amounts |

| Senior citizen prioritising simplicity | FD | Section 80TTB exemption on interest up to ₹50,000, plus simpler annual tax filing |

| High tax bracket (30% slab), multi-year horizon | Liquid fund | Tax-deferral advantage is largest for investors in the highest slab |

The short version of the FD vs liquid fund decision: if certainty and simplicity matter more to you than squeezing out the last bit of return, choose FD. If flexibility, faster access, and better post-tax efficiency over a multi-year horizon matter more, the liquid fund side of the FD vs liquid fund comparison usually wins. Very few situations are genuinely “wrong” either way — it’s a matter of which trade-off suits your specific goal.

7. FD vs Liquid Fund for Emergency Funds

This specific FD vs liquid fund comparison for emergency funds deserves its own section since it’s one of the most common real-world use cases. A savings account typically offers 2.7–4%, an FD offers roughly 6.25–7% but with a penalty for early withdrawal, and a liquid fund offers a similar or slightly better return with same-day or T+1 access and no early-withdrawal penalty after the first week.

For an emergency fund specifically, the combination of decent returns and genuinely fast, penalty-free access makes liquid funds the structurally better fit compared to locking the same money in an FD — the whole point of an emergency fund is that you might need it on short notice, and an FD’s penalty structure works against exactly that need.

Practical split many advisors recommend: Keep 1–2 months of expenses in an instant-access savings account, and the remainder of the emergency fund in a liquid fund — this mirrors the broader emergency fund strategy covered in MoneyOra’s emergency fund planning guide.

8. Common Mistakes People Make Choosing Between the Two

- Comparing only the headline rate in the FD vs liquid fund decision, ignoring tax timing. Two instruments with the same advertised return can produce meaningfully different after-tax outcomes over several years.

- Forgetting that TDS isn’t your final tax liability. If a bank deducts 10% TDS but your slab rate is 30%, you still owe the remaining 20% — missing this is a common way people underpay and later get a notice.

- Assuming a liquid fund carries the same risk as an equity fund. It doesn’t — liquid funds invest in short-term debt instruments, not stocks, and behave very differently in a market downturn.

- Chasing a high FD rate from a small or cooperative bank without checking DICGC coverage. The extra 1–2% yield isn’t worth it if a meaningful portion of the deposit sits outside the ₹5 lakh insurance limit.

- Treating “liquid fund” and “debt fund” as identical. Liquid funds are a specific, low-duration category of debt fund; other debt fund categories carry meaningfully higher interest-rate risk and shouldn’t be substituted for a liquid fund in a short-term or emergency-fund context.

9. MoneyOra Analysis: Why the Post-2023 Tax Change Matters Here

Since 1 April 2023, debt mutual funds — including liquid funds — lost the indexation benefit, a change that reshaped the FD vs liquid fund tax comparison that previously let long-term holders reduce their taxable gain for inflation. Gains are now taxed at the investor’s income slab rate, similar in rate to FD interest. This genuinely narrowed the tax-rate gap between the two instruments compared to the pre-2023 rules.

What didn’t change, and what still matters most for this comparison, is the timing of taxation. An FD is taxed every year regardless of whether you’ve touched the money; a liquid fund is taxed only on redemption. For someone holding either instrument for multiple years, that single difference in timing — not the tax rate itself — is now the main reason a liquid fund can end up ahead of an FD on a genuinely comparable pre-tax return.

Assumptions stated: this reflects the general tax framework in effect as of early 2026 and is not a substitute for personalised tax advice; always confirm current rules with a tax professional before making a large allocation decision. https://www.amfiindia.com

10. Risks to Consider

- Market risk: Liquid funds are low-volatility, not risk-free; rare credit-quality issues in the underlying portfolio can cause temporary NAV pressure.

- Concentration risk: A high-rate FD at a small or cooperative bank exceeding the ₹5 lakh DICGC insurance limit exposes the excess amount if the bank fails.

- Tax-rule risk: Mutual fund taxation rules have changed materially in recent years (the 2023 indexation removal is one example); today’s tax-timing advantage could shift again with future policy changes.

- Rate risk: Both FD and liquid fund yields move with broader interest rate cycles over time; the specific percentages cited here will shift as RBI policy rates change.

- Behavioural risk: The easier access a liquid fund offers can tempt some investors to dip into money meant for a longer-term goal — a firm FD lock-in can, for some people, be a helpful behavioural guardrail rather than a drawback.

This is general educational information, not personalised financial or tax advice — your specific slab rate, horizon, and risk comfort should guide the final decision. https://www.incometax.gov.in

For money you genuinely won’t touch and want locked away from your own future temptation — FDs still do that job well, especially for senior citizens using the Section 80TTB exemption. For an emergency fund, a large lump sum parked temporarily, or anyone in a higher tax bracket investing for more than a year, a liquid fund’s tax-deferral advantage and faster access usually make it the stronger choice on the actual numbers. https://www.dicgc.org.in

The FD vs liquid fund decision ultimately isn’t about which instrument is universally “better” — it’s about matching the trade-off to your goal. Run the FD vs liquid fund comparison for your own amount, tenure, and tax bracket before deciding, rather than defaulting to whichever option feels more familiar. Use the free FD calculator now on MoneyOra.in to see your own comparison.

FREQUENTLY ASKED QUESTIONS

1. Which gives better returns, FD or liquid fund?

Pre-tax returns are usually close — FDs currently offer roughly 6.25–7%, liquid funds roughly 6.5–7.5%. The bigger difference shows up after tax: because liquid funds are taxed only on redemption rather than annually, they often deliver better post-tax returns over multi-year horizons, especially for investors in higher tax brackets.

2. Is a liquid fund as safe as an FD?

Not identical, but close for practical purposes. FDs carry virtually no market risk and are DICGC-insured up to ₹5 lakh per bank. Liquid funds carry low but non-zero market risk since they invest in short-term debt instruments, though losses are rare when the fund holds high-quality instruments.

3. How is FD interest taxed compared to liquid fund gains?

FD interest is taxed every year at your income slab rate, whether or not you’ve received the cash, and TDS applies once annual interest crosses ₹40,000 (₹50,000 for senior citizens). Liquid fund gains are taxed only when you redeem, at your slab rate, with no TDS for resident Indian investors.

4. Which is better for an emergency fund, FD or liquid fund?

Liquid funds are generally better suited for emergency funds because they offer T+1 or same-day redemption with little to no penalty, while FDs typically impose a 0.5–1% interest penalty for premature withdrawal.

5. Can I lose money in a liquid fund?

It’s rare but not impossible. Liquid funds invest in very short-term, high-quality debt instruments, so losses are uncommon, but they can occur in stress scenarios involving credit defaults in the underlying portfolio — unlike an FD, which offers a contractually guaranteed return.

6. How quickly can I withdraw money from a liquid fund versus an FD?

Liquid funds typically credit redemptions within 1 business day, and many offer instant redemption up to a limit (often around ₹50,000). FDs generally require premature closure to access funds early, which usually comes with an interest-rate penalty.

7. Do liquid funds have a lock-in period like FDs?

No. Liquid funds have no lock-in period and can be redeemed anytime, though a small exit load may apply if redeemed within the first 6–7 days of investment. FDs are locked for the chosen tenure unless you accept a penalty for early withdrawal.

8. Is TDS on FD interest my final tax liability?

No. TDS at 10% is just an advance deduction. If your income slab rate is higher — say 30% — you still owe the remaining tax when filing your return. Many people mistakenly assume TDS equals their full tax obligation.

9. Are liquid funds good for senior citizens?

FDs are often simpler for senior citizens due to the Section 80TTB exemption on interest up to ₹50,000 and more predictable, contractual returns. Liquid funds can still suit senior citizens who prioritise flexibility and don’t need the FD’s fixed-return certainty.

10. What’s the difference between a liquid fund and other debt funds?

Liquid funds specifically invest in very short-term instruments with maturities up to 91 days, making them one of the lowest-risk categories of debt fund. Other debt fund categories (like corporate bond funds or longer-duration funds) carry meaningfully higher interest-rate risk and aren’t a direct substitute for a liquid fund in a short-term or emergency-fund context.

Pingback: How to Build a ₹10 Lakh Emergency Fund in India - MoneyOra

Pingback: Hidden Bank Charges: 9 Fees Costing You ₹2,000+ - MoneyOra