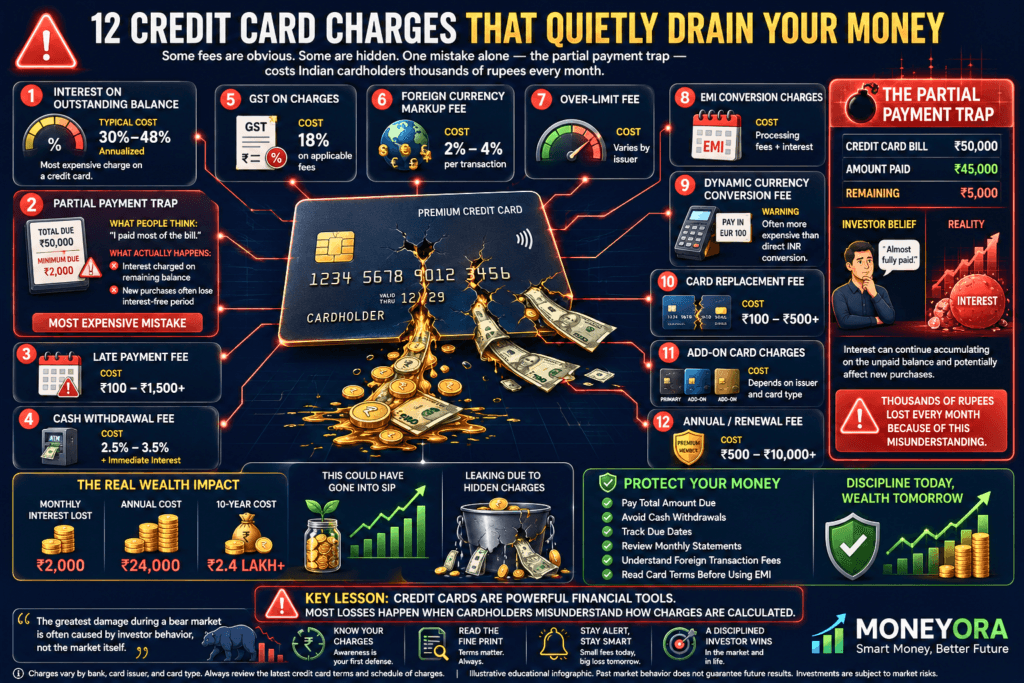

Most people who use a credit card in India have no idea what it actually costs them every year. Not in a vague sense — in rupees. The bank sends a statement, you pay the minimum, and somewhere in between, fees accumulate that most cardholders never trace back to their source.

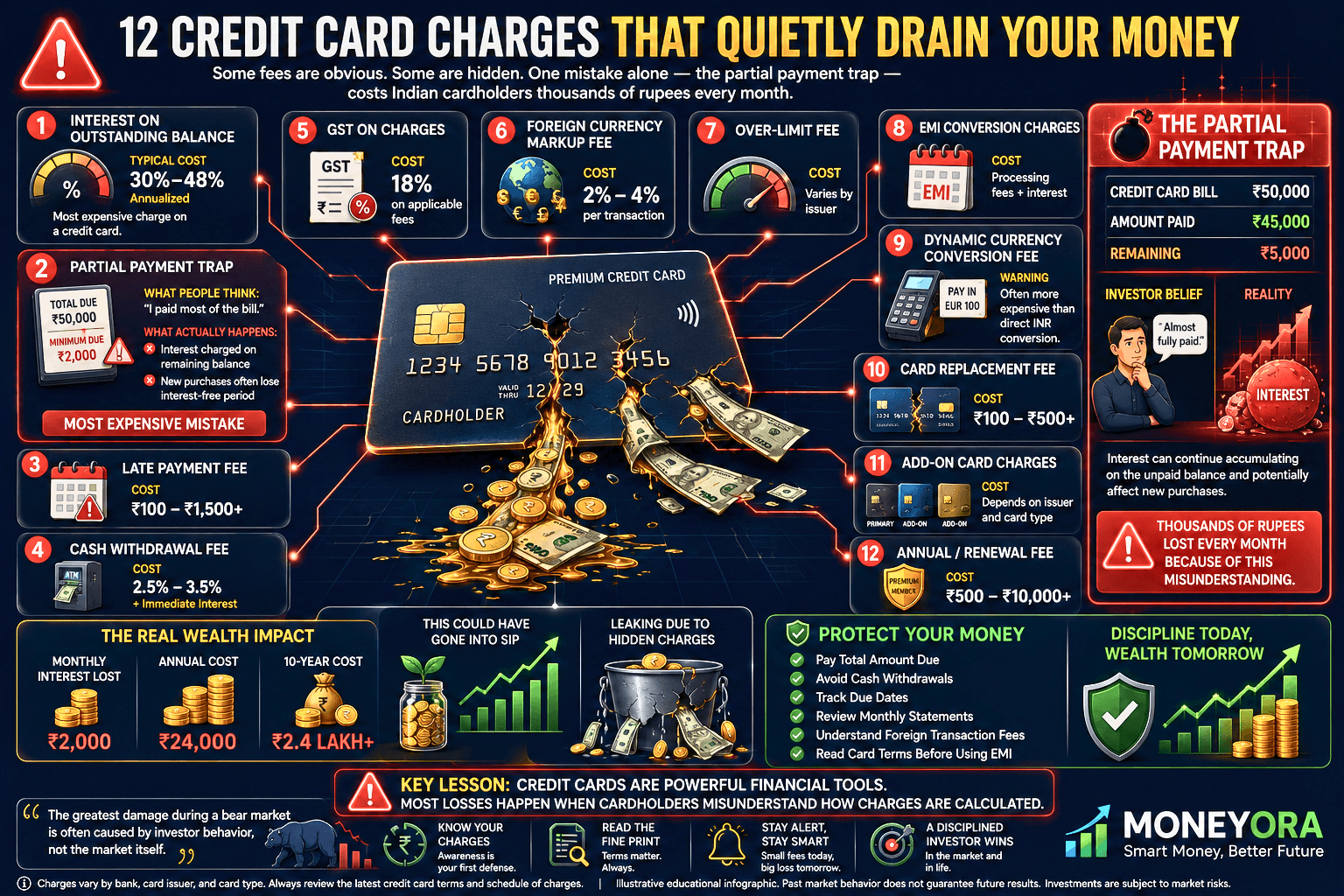

Credit card charges in India now span at least 12 distinct fee categories. Some are obvious. A few are genuinely tricky. And one — the partial payment trap — costs Indian cardholders thousands of rupees every month for a mistake they believe they’ve avoided.

This guide breaks down every charge, shows you the real rupee cost of each one, explains what the RBI now mandates, and tells you exactly how to reduce what you’re paying. If you’ve ever wondered why your credit card bill feels slightly wrong, this is where the answer is. You can also use the free FD Calculator on MoneyOra or our EMI Calculator to model what that wasted interest could have earned for you instead.

How Much Can Credit Card Charges Actually Cost You?

Before going through each charge separately, here’s a quick scenario that shows the combined damage.

Scenario: A typical Indian credit card user, ₹50,000 credit limit, ₹30,000 average monthly spend

| Charge Type | Trigger | Annual Cost (Estimate) |

|---|---|---|

| Annual fee | Card held | ₹500 – ₹5,000 |

| Finance charge (interest) | Partial payment once a month | ₹4,000 – ₹12,000 |

| Late payment fee | 1 missed payment | ₹500 – ₹1,300 |

| GST on all fees | Every fee charged | ₹90 – ₹2,000+ |

| Foreign markup (2 trips or 3 subscriptions abroad) | Foreign currency usage | ₹1,500 – ₹4,000 |

| Cash advance (1 withdrawal) | ATM cash from credit card | ₹750 – ₹2,500 |

| Total potential annual loss | ₹7,340 – ₹26,800+ |

That range is wide because behavior determines exposure. But the point stands: a cardholder who makes a few common mistakes every year is quietly losing somewhere between ₹7,000 and ₹27,000 in charges that never show up as a single obvious line item.

The Partial Payment Trap — The Most Expensive Mistake Most People Don’t Know They’re Making

This one deserves its own section before anything else, because it catches people who think they’re being responsible.

Here’s how it works. Your credit card bill is ₹1,00,000. You pay ₹95,000. Reasonable, right? You paid 95% of your bill. The bank should charge interest only on the ₹5,000 you didn’t pay.

That is not how it works.

Most Indian banks — including HDFC, ICICI, SBI, Axis, and Kotak — charge interest on the full ₹1,00,000 for the entire billing cycle the moment you fail to pay the complete statement balance. This is called the full-statement interest rule, and it’s in every MITC (Most Important Terms & Conditions) document that most people never read.

| Amount Paid | Outstanding | Interest Charged On | Monthly Interest (@ 3.5%) |

|---|---|---|---|

| ₹0 | ₹1,00,000 | ₹1,00,000 | ₹3,500 |

| ₹50,000 | ₹50,000 | ₹1,00,000 | ₹3,500 |

| ₹95,000 | ₹5,000 | ₹1,00,000 | ₹3,500 |

| ₹1,00,000 (full) | ₹0 | ₹0 | ₹0 |

The rule: pay the full statement balance, or accept that interest applies to everything you spent that month. There is no middle ground that saves you money.

MoneyOra Tip: Set auto-pay for the full statement balance. If that’s not possible due to cash flow, don’t pay 50% or 90% — it doesn’t reduce the interest charge. Instead, use the Personal Loan EMI Calculator to check if a personal loan at 12–16% p.a. would cost you less than a credit card rollover at 42% p.a. It almost always does.

Annual Fee and Joining Fee

This is the most visible credit card charge, and also the most negotiable.

- Joining fee: ₹0 to ₹10,000 (one-time, on card issuance)

- Annual renewal fee: ₹0 to ₹15,000 per year

- GST: 18% added on the fee amount

Most cards with annual fees in the ₹500–₹3,000 range have a spend-based waiver: spend ₹1.5 lakh to ₹3 lakh in the year and the fee is reversed. Premium cards (₹5,000–₹15,000 range) rarely waive fees but come with lounge access, travel credits, and higher reward rates that can justify the cost — if you actually use those benefits.

A lot of people hold 3–4 cards they barely use and pay ₹1,500–₹3,000 in annual fees per card. That’s ₹4,500–₹12,000 gone every year for cards sitting in a drawer.

What to do: Cancel any card you haven’t used in 6 months. Before canceling, confirm there’s no outstanding balance — RBI rules require the bank to process closure within 7 business days, and if they delay past that, they owe you ₹500 per day in penalty (per the RBI Master Direction, 2022).

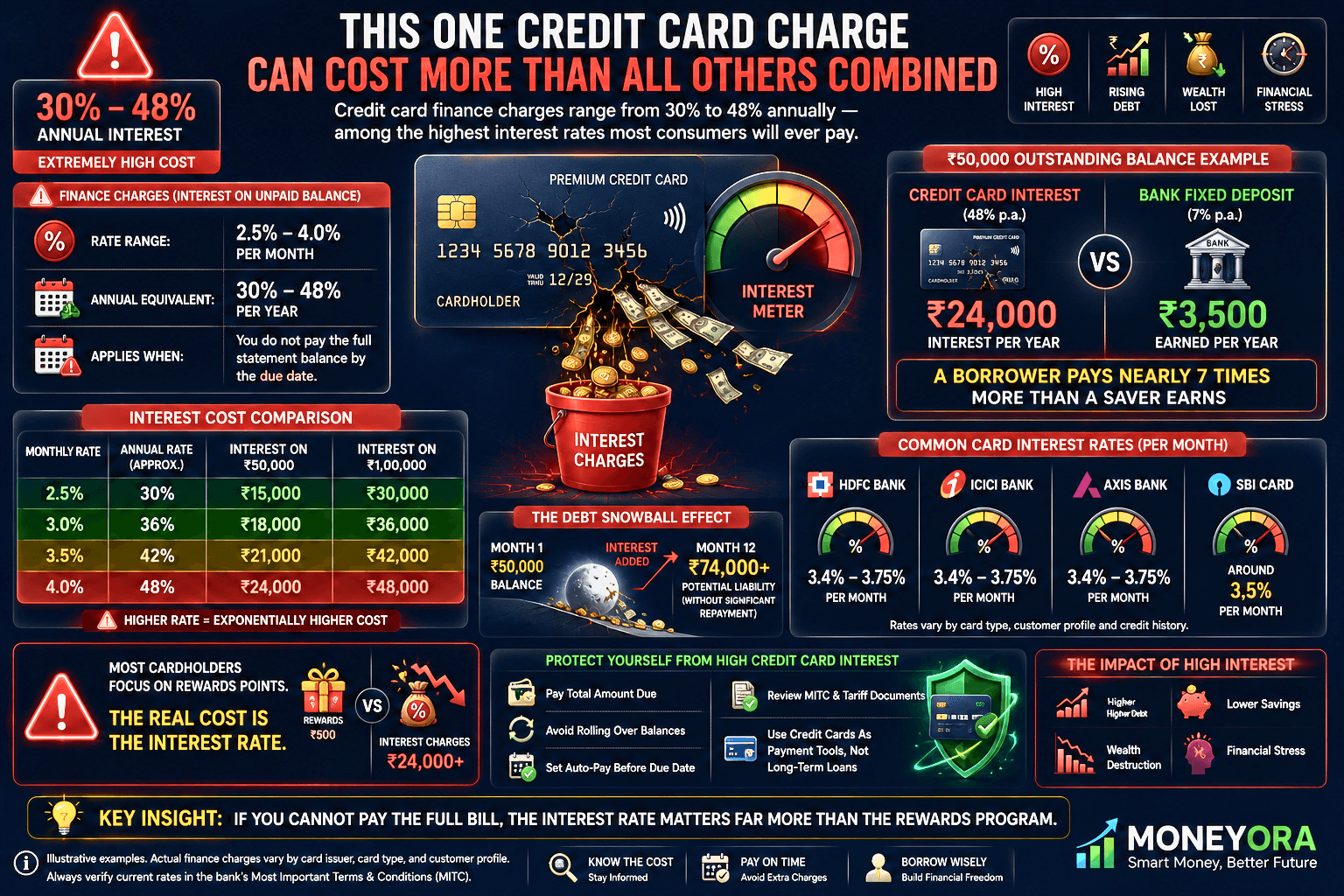

Finance Charges (Interest Rate on Unpaid Balance)

This is where the real money goes.

- Rate range: 2.5% to 4% per month

- Annual equivalent: 30% to 48% per year

- Applies from: Transaction date (not billing date) once you miss full payment

To put that in context: a 48% annual interest rate on ₹50,000 is ₹24,000 in interest per year. A fixed deposit at 7% earns only ₹3,500 on the same amount. One cardholder rolling over credit card debt is paying six times what a saver earns on the equivalent sum. Use our FD Calculator to see the gap clearly.

| Monthly Rate | Annual Rate | Annual Interest on ₹50,000 | Annual Interest on ₹1,00,000 |

|---|---|---|---|

| 2.5% | 30% | ₹15,000 | ₹30,000 |

| 3.0% | 36% | ₹18,000 | ₹36,000 |

| 3.5% | 42% | ₹21,000 | ₹42,000 |

| 4.0% | 48% | ₹24,000 | ₹48,000 |

Check your specific card’s rate in the MITC document or on your bank’s tariff page. HDFC, ICICI, and Axis currently charge 3.4%–3.75% per month on most cards. SBI Card charges 3.5% across most variants.

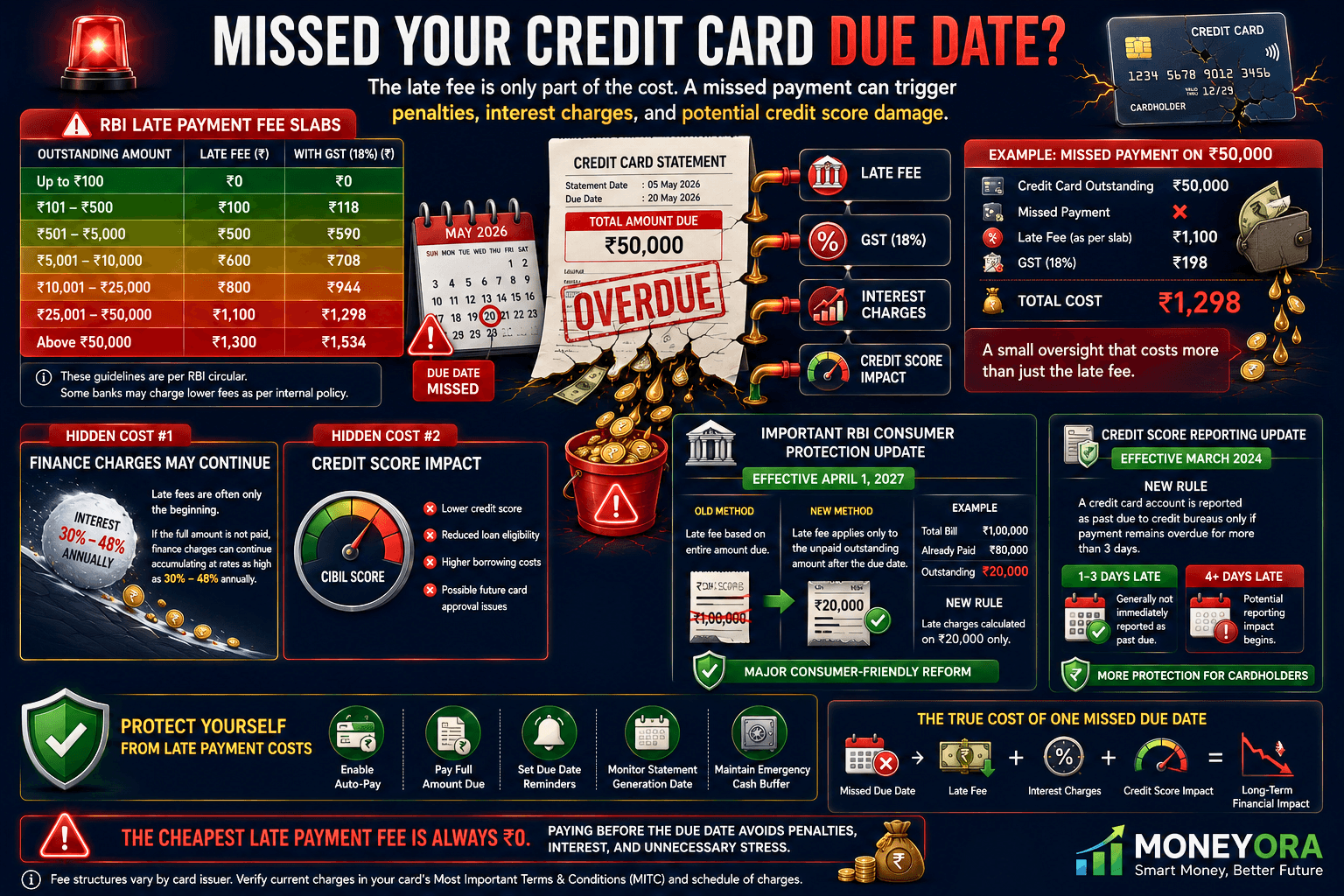

Late Payment Fee

Missing the due date costs you in two ways: the late fee itself, and a credit score hit that can affect loan eligibility for years.

RBI-mandated slab structure (effective October 2024):

| Outstanding Amount | Late Payment Fee (typical slab) | With GST @ 18% |

|---|---|---|

| Up to ₹100 | ₹0 | ₹0 |

| ₹101 – ₹500 | ₹100 | ₹118 |

| ₹501 – ₹5,000 | ₹500 | ₹590 |

| ₹5,001 – ₹10,000 | ₹600 | ₹708 |

| ₹10,001 – ₹25,000 | ₹800 | ₹944 |

| ₹25,001 – ₹50,000 | ₹1,100 | ₹1,298 |

| Above ₹50,000 | ₹1,300 | ₹1,534 |

New RBI rule (effective April 1, 2027): Late payment charges will be calculated only on the outstanding amount after the due date — not on the total amount due. This prevents penalizing partial payments unfairly. If you’ve paid ₹80,000 of a ₹1,00,000 bill and the ₹20,000 remainder is late, the late fee applies to ₹20,000 only, not ₹1,00,000. This is a meaningful consumer win from the RBI.

Also from March 2024: a credit card account is only reported as “past due” to credit bureaus if payment is overdue by more than three days. A couple of days late doesn’t immediately hurt your CIBIL score anymore.

Cash Advance Fee

Withdrawing cash from an ATM using a credit card is the most expensive single transaction most people make without realizing it.

- Cash advance fee: 2.5%–3% of withdrawal amount, minimum ₹250–₹500

- Plus: Finance charge starts from the transaction date — no grace period

- Effective annual cost: Can exceed 50% p.a.

Real example: Withdraw ₹10,000 cash from credit card ATM.

- Cash advance fee: ₹300 (3%) + GST ₹54 = ₹354

- Finance charge at 3.5%/month for 30 days: ₹350

- Total cost of accessing ₹10,000 for 30 days: ₹704

- That’s a 7% cost for one month — 84% annualized

Compare: a personal loan at 15% p.a. would cost ₹125 for the same ₹10,000 for one month. The credit card cash advance costs 5.6x more. Use the Personal Loan Calculator to run this comparison yourself.

Never use your credit card for ATM cash withdrawals. If you need emergency cash, UPI transfers, personal loan top-ups, or even a loan against FD all cost significantly less.

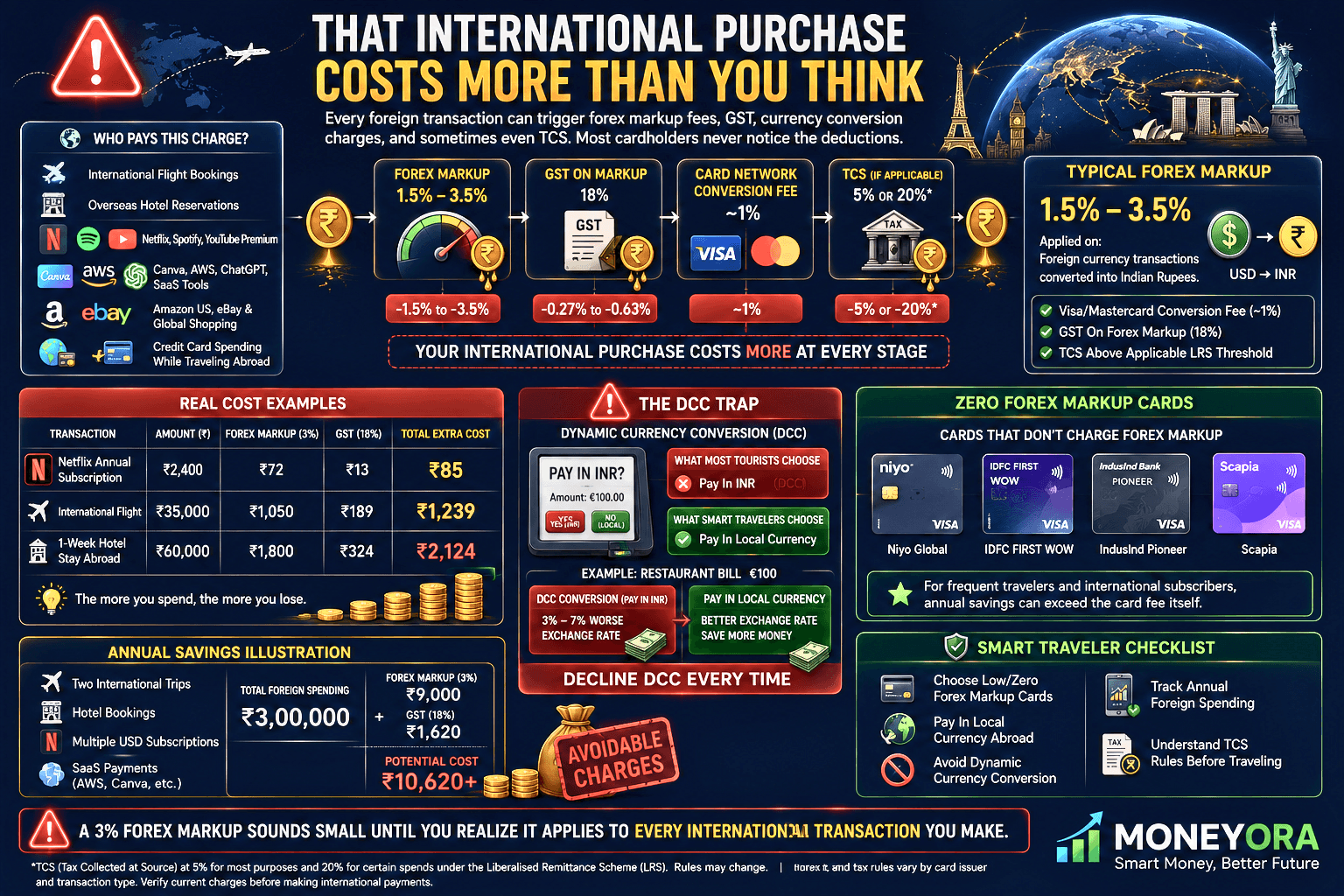

Foreign Transaction Markup Fee (Forex Markup)

This charge affects anyone who:

- Books international flights or hotels online

- Pays for Netflix, Spotify, Canva, AWS, or other apps billed in USD

- Shops on Amazon US, eBay, or other international platforms

- Travels abroad and swipes their Indian credit card

Typical forex markup range: 1.5%–3.5% of the transaction amount in rupee equivalent

On top of this, Visa and Mastercard add a currency conversion fee (~1%), and if you’re spending over ₹7 lakh abroad in a financial year, TCS (Tax Collected at Source) at 20% applies on the excess under the LRS (Liberalised Remittance Scheme).

| Transaction | Amount (INR) | Forex Markup (3%) | GST on Markup | Total Extra Cost |

|---|---|---|---|---|

| Netflix annual plan (USD) | ₹2,400 | ₹72 | ₹13 | ₹85 |

| International flight booking | ₹35,000 | ₹1,050 | ₹189 | ₹1,239 |

| 1 week hotel abroad | ₹60,000 | ₹1,800 | ₹324 | ₹2,124 |

Cards with zero forex markup do exist — Niyo Global, IDFC First WOW, and IndusInd Pioneer are frequently cited options. If you travel or use international subscriptions regularly, the markup savings can easily exceed the annual fee of such cards within a year.

One more trap here: if you’re at an ATM or merchant abroad and they offer to charge you in Indian Rupees (Dynamic Currency Conversion / DCC), always decline. Pay in local currency. DCC rates are typically 3–7% worse than your bank’s conversion, meaning you get marked up twice.

Over-Limit Fee

Many banks silently allow you to exceed your credit limit on small transactions — especially recurring auto-debits — and then charge you for it.

- Fee: 2.5%–3% of the over-limit amount, minimum ₹500–₹600

- Plus GST: 18% on the fee

- RBI rule: Banks cannot increase your limit without your explicit consent — but they can allow temporary over-limit usage if you’ve pre-opted in

What to do: Call your bank and confirm you’ve opted out of the over-limit facility. Most banks’ net banking portals also have this setting under “Card Controls.” This prevents the fee entirely.

GST on All Credit Card Charges

This is the charge most people overlook because it hides inside other charges rather than appearing as its own line.

GST at 18% applies to every fee on your credit card — annual fee, late payment fee, cash advance fee, forex markup, over-limit fee, statement fee, card replacement fee. Everything except the principal amount you borrowed.

The GST is non-waivable. It’s mandated under the Central GST Act and State GST Act. Even if a bank waives another fee as a goodwill gesture, they cannot waive the GST component — so you’ll still see a residual GST charge even when the underlying fee is reversed.

If you’re a business owner or registered GST entity using your credit card for business expenses, you may be able to claim input tax credit on some of this GST. Worth checking with your CA

EMI Conversion Fee

Converting a large purchase to EMI sounds smart, but it carries its own costs.

- Processing fee: ₹99–₹250 per conversion

- Interest rate: 12%–24% p.a. (lower than revolving credit interest, but real)

- GST: 18% on processing fee

The key distinction: “no-cost EMI” is not actually interest-free. Banks recover the cost either by removing the discount you’d have gotten on the product, or through a subvention fee charged to the merchant. You’re not saving the interest — it’s been priced into the product.

If you genuinely need EMI, the interest rate on credit card EMI (12–18% p.a.) is usually still better than revolving credit card interest (36–48% p.a.). Use our EMI Calculator to compare total interest paid under different EMI tenures before choosing.

Balance Transfer Fee

Transferring outstanding balance from one card to another for a lower interest rate comes with:

- Balance transfer fee: 1%–2% of transferred amount, minimum ₹250–₹500

- Interest on transferred amount: Typically 0%–2% p.a. for a promotional period of 3–6 months

Balance transfer can make sense if you’re carrying a large outstanding at 42% p.a. and can move it to 0–2% for 6 months while you pay it down. But read the fine print: if you miss even one payment during the promotional period on the new card, the promotional rate often reverts to the regular rate (36–48% p.a.) on the entire outstanding balance.

Fuel Surcharge

Fuel stations charge a 1% surcharge on credit card transactions. Most banks waive this on transactions between ₹400 and ₹4,000 per transaction — but there’s usually a monthly cap on the total waiver (₹250–₹500 per billing cycle).

If you fill up a car regularly, this adds up. A car owner who spends ₹6,000 on petrol monthly across two fill-ups:

- Surcharge per fill-up at ₹3,000: ₹30 × 2 = ₹60/month waived

- Annual waiver: ₹720

- If spend exceeds cap: residual surcharge applies

Most fuel-benefit credit cards advertise this waiver prominently. Just check the monthly cap and whether your typical per-transaction fill amount falls in the waiver range.

Reward Point Redemption Fee

Reward points feel free until you try to use them.

- Redemption fee: ₹99–₹250 per redemption request (not per point)

- Point expiry: Most banks expire points in 2–3 years

- Minimum redemption threshold: Usually 500–2,500 points minimum

If you’ve accumulated 800 reward points worth ₹160 and pay a ₹99 redemption fee plus 18% GST (₹117 total), you’ve kept ₹43 in net value. That’s a 73% fee on the value you’re redeeming. Not worth it unless you have a large points balance.

Other Small Charges Worth Knowing

| Charge | Typical Amount | How to Avoid |

|---|---|---|

| Paper statement fee | ₹50–₹100/month | Switch to e-statement (free on all banks) |

| Card replacement fee | ₹100–₹250 | Cards lost/stolen and reported before misuse: free under RBI Customer Liability Framework 2017 |

| ECS/auto-debit bounce | ₹500–₹600 + bank charge ₹200–₹500 | Ensure auto-pay source account always has sufficient balance 2 days before due date |

| Duplicate statement | ₹100–₹200 per statement | All previous statements are downloadable from net banking for free |

| Foreclosure/EMI cancellation | 3% of outstanding (RBI capped) | Complete the EMI tenure or calculate whether savings justify the penalty |

MoneyOra Analysis: What RBI Changed for Credit Card Users in 2024–2026

The regulatory landscape for credit card charges shifted meaningfully in 2024, and one more big change is coming in 2027. Here’s a clear summary of what’s changed:

What Changed in March–October 2024

- Late payment: 3-day rule. An account is only marked “past due” with credit bureaus if payment is overdue by more than three days. A short delay no longer immediately damages your CIBIL score.

- Late fee slab cap. RBI capped late payment fees within a slab structure. Banks can no longer charge arbitrary amounts.

- Billing transparency mandate. Banks must now show transaction date, posting date, merchant name, amount, and applicable charges for every line on your statement. Delayed or unclear entries are a compliance violation.

- No unsolicited limit increases. Banks cannot increase your credit limit without explicit consent. No more auto-upgrades.

What’s Coming in April 2027

- Late fee on outstanding only. Charges will apply only to the amount unpaid after the due date — not the total statement balance. This is a direct fix for a longstanding consumer complaint.

- Dispute resolution capped. Banks must resolve chargebacks and unauthorized transaction disputes within a defined number of days, with mandatory customer updates at each stage.

What Did Not Change

- The full-statement interest rule is still in effect. Pay everything or accept interest on everything.

- Forex markup, cash advance fees, and EMI processing fees remain bank-determined.

- GST at 18% on all credit card fees is non-negotiable.

Source: RBI Master Direction — Credit Card and Debit Card Issuance and Conduct, 2022 (last amended 2024)

Risks to Consider

- Debt spiral risk. Credit card revolving debt at 42–48% p.a. compounds faster than almost any investment returns. Anyone carrying forward a balance month-on-month is almost certainly losing money net of any rewards earned.

- CIBIL damage risk. Even one missed payment reported creates a mark on your credit report that lenders see for up to 7 years. This affects home loan and car loan eligibility and interest rates.

- Hidden subscription trap. International subscriptions (Netflix, Adobe, Microsoft) billed in foreign currency attract forex markup automatically every month. Most users set these up once and forget the markup adds to the monthly charge.

- Reward over-optimization trap. Spending more than you normally would to earn reward points or hit annual fee waiver thresholds often costs more than the reward is worth. Run the math before making the spend.

- Minimum due illusion. The minimum amount due on your statement is designed to keep you in debt. Paying only the minimum on a ₹50,000 balance at 3.5%/month, paying ₹2,000 per month, takes over 4 years to clear and costs ₹46,000+ in interest alone.

Action Checklist: How to Cut Your Credit Card Charges

- Set auto-pay for the full statement balance, not minimum due

- Cancel every card you haven’t used in 6+ months

- Switch all card accounts to e-statements (saves ₹600–₹1,200/year per card)

- Opt out of the over-limit facility from your bank’s net banking portal

- Never withdraw cash from a credit card ATM — use UPI or debit card

- For international travel or foreign-currency subscriptions, switch to a zero-forex-markup card

- Always pay in the local currency when abroad — never choose “Pay in INR” at a foreign ATM or merchant

- If carrying EMI, use MoneyOra’s EMI Calculator to compare total interest across different tenure options

- Set a calendar reminder 5 days before your due date — or enable auto-pay

- Read your MITC document once. It has every fee your bank can ever charge you. If a charge appears that isn’t in it, you can dispute it under RBI’s Charter of Customer Rights

According to the Reserve Bank of India (RBI), credit card issuers must clearly disclose fees and charges to customers before card activation.

Pay Once, Not Forever

Credit card charges in India are not a mystery — they’re a disclosed system that most people simply don’t read. The fees are all in the MITC. The interest rate is on the website. The rules around late fees and bureau reporting changed in 2024 and are changing again in 2027.

The cardholders who get hurt are not the ones who lack information. They’re the ones who pay 95% of their bill thinking that’s close enough, or who withdraw ATM cash in an emergency without knowing the effective rate, or who hold four cards and pay ₹12,000 in annual fees for benefits they never use.

The fix is straightforward: pay 100% of your statement balance every month, eliminate cards you don’t use, set up e-statements, and check your forex markup rate if you spend in foreign currency. That alone can save most Indian cardholders ₹5,000–₹15,000 every year.

If you’re currently carrying credit card debt and want to model the cost of converting it to a personal loan instead, or want to calculate what that saved interest could do in a fixed deposit or SIP, try the free tools on MoneyOra:

- EMI Calculator — compare loan EMIs and total interest

- Personal Loan EMI Calculator — check if a personal loan is cheaper than credit card rollover

- FD Calculator — see what saved interest money earns in a fixed deposit

- SIP Calculator — model long-term wealth if you invest what you currently spend on card interest

Use the free calculator now on MoneyOra.in

What is the highest credit card interest rate banks in India can charge?

There is no regulatory cap on credit card interest rates in India. Banks currently charge between 2.5% and 4% per month (30%–48% per year). The RBI requires the rate to be disclosed in the MITC and on the bank’s website, but does not mandate a maximum. Always check your specific card’s rate before carrying a balance.

Can a bank charge GST on the credit card annual fee?

Yes. GST at 18% is mandatory on all credit card service fees, including annual fees, late payment charges, cash advance fees, and forex markup. This is governed by the CGST Act and cannot be waived by the bank, even when they waive the underlying fee.

If I pay ₹1 extra above the minimum due, does that reduce my interest?

No. Most Indian banks charge finance interest on the full statement balance the moment you don’t pay 100% of it. Paying ₹1 above minimum due changes nothing about the interest calculation. The fix is to pay the complete statement balance every cycle.

What is the RBI rule on credit card late payment fees from 2024?

From March 2024, RBI mandated that credit card accounts are only reported as “past due” to credit bureaus if payment is more than three days late. Late payment fees must follow a slab structure and apply only on the outstanding unpaid amount. A further update (effective April 2027) will require late fees to apply only to the amount not paid after the due date, not the total bill.

Can I dispute a credit card charge I didn’t authorize?

Yes. Under the RBI’s Charter of Customer Rights and the Master Direction on Credit Cards, unauthorized transactions must be investigated. If reported promptly and the bank’s liability framework is triggered, you may receive provisional credit during the investigation period. Report the charge to your bank in writing and escalate to the RBI Banking Ombudsman if unresolved within 30 days.

Is “no-cost EMI” actually free?

Not always. “No-cost EMI” typically involves the merchant paying an interest subvention to the bank, or the discount on the product is removed. The effective cost is built into the price you pay. The processing fee and GST on EMI conversion are always charged regardless. Use MoneyOra’s EMI Calculator to compare actual costs before choosing EMI.

How do I waive my credit card annual fee?

Call customer care before the annual fee billing date and ask for a waiver. If your card has a spend-based waiver threshold (usually ₹1.5–3 lakh/year), confirm whether you’ve met it. Many banks will also offer a waiver as a retention gesture if you’ve been a loyal customer. If they refuse, evaluate whether the card’s benefits justify the fee.

What is Dynamic Currency Conversion and why should I avoid it?

Dynamic Currency Conversion (DCC) is when a foreign merchant or ATM offers to charge your Indian credit card in Indian Rupees instead of the local currency. The rate used by the merchant is almost always 3–7% worse than your bank’s forex conversion rate, meaning you pay double markup. Always select “Pay in local currency” when abroad.

How many credit cards should I hold?

Most financial advisors suggest 2–3 cards maximum: one primary card with the best rewards for daily spending, one travel card with zero forex markup, and optionally one for fuel benefits. Holding more than 3 cards typically means paying annual fees on cards that don’t deliver sufficient benefit to justify the cost.

Where can I read the full fee schedule for my credit card?

Every bank is required by RBI to publish the MITC (Most Important Terms & Conditions) and a Schedule of Charges on their website and send it to you before card activation. Search “[Bank name] credit card schedule of charges MITC” on Google. All current fees must be listed there by law.