| Year | Opening Balance | Yearly Deposit | Interest Earned | Closing Balance | Cumul. Interest |

|---|

PPF Calculator – Free Public Provident Fund Calculator Online (2026)

Table of Contents

MoneyOra’s free PPF Calculator shows you exactly how much your Public Provident Fund investment will be worth at maturity — the total amount deposited, the interest earned on it, and a full year-by-year breakdown. Enter your yearly deposit and tenure. The current rate of 7.1% p.a. is fixed by the government and already loaded in. “how PPF compares to equity SIP in a ₹100 per day investment plan”

A PPF account is one of the few investments in India that qualifies for the EEE tax treatment the deposit is deductible under Section 80C, the interest earned is tax-free, and the maturity amount is tax-free. “include PPF in your salary investment plan for safe returns” That combination is genuinely hard to find elsewhere. The only catch is the 15-year lock-in. This PPF Calculator helps you figure out if the wait is worth it for your numbers.

What Is a PPF Calculator?

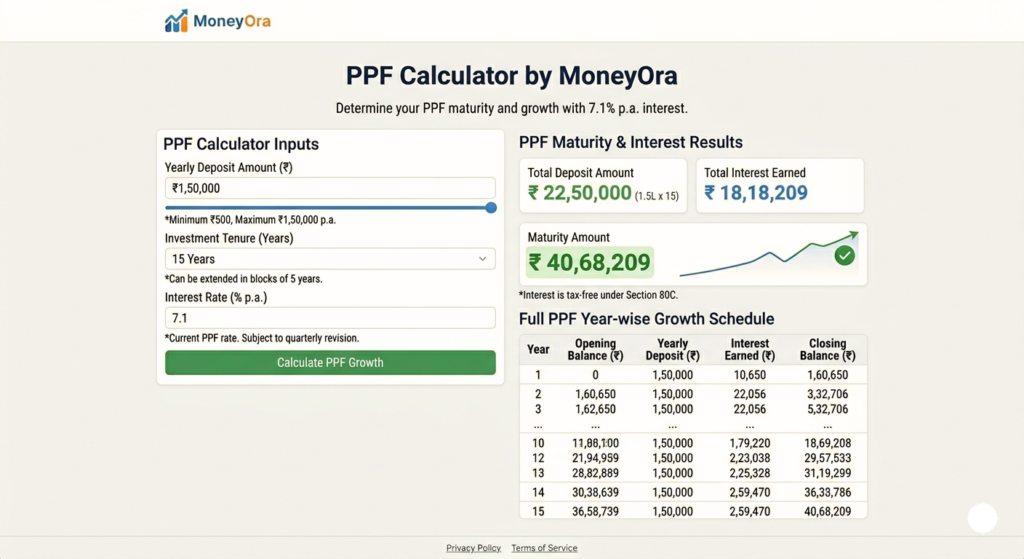

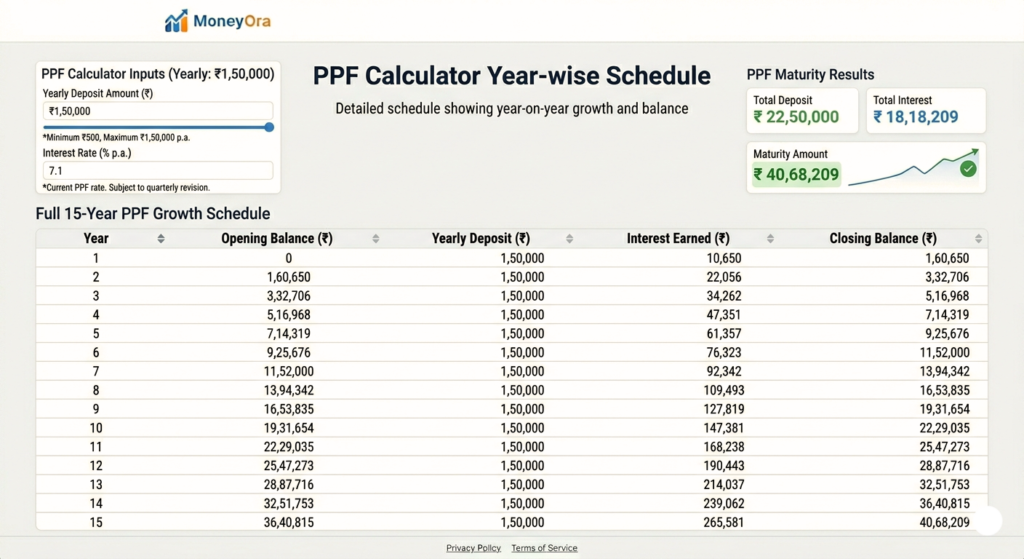

A PPF Calculator takes two inputs — your yearly deposit and the tenure — and calculates the maturity value of your Public Provident Fund account at the current government-set interest rate of 7.1% p.a.

A Public Provident Fund is a government-backed savings scheme. You deposit anywhere from ₹500 to ₹1.5 lakh per year, the money compounds annually at 7.1%, and after 15 years you get the full maturity amount — principal plus interest — completely tax-free.

The interest rate is reviewed by the government every quarter, but has been steady at 7.1% since April 2020. MoneyOra’s PPF Calculator uses this current rate and shows you the full year-by-year schedule so you can see exactly how compounding works over 15 to 50 years.

How Does a PPF Calculator Help?

PPF compounds annually, which means the calculation across 15 or 25 years is straightforward compared to monthly-compounding instruments. But the numbers still get large enough that most people underestimate how much they’ll actually end up with.

Here’s where a Public Provident Fund Calculator is useful:

- You see the real maturity number. ₹1.5 lakh per year for 15 years feels like ₹22.5 lakh. The actual maturity amount at 7.1% is around ₹40.7 lakh. The gap between what you put in and what you get out is the whole point of the PPF — and the calculator makes that visible immediately.

- You can plan around extensions. PPF allows 5-year extensions after the initial 15-year term. Use the PPF Calculator to see how much extra you’d accumulate at year 20, 25, or 30. For most people, extending once or twice significantly changes the retirement corpus.

- You estimate your Section 80C savings. The calculator shows an estimated tax saved based on your yearly deposit — useful for annual tax planning, especially if you’re maximising the ₹1.5 lakh 80C limit.

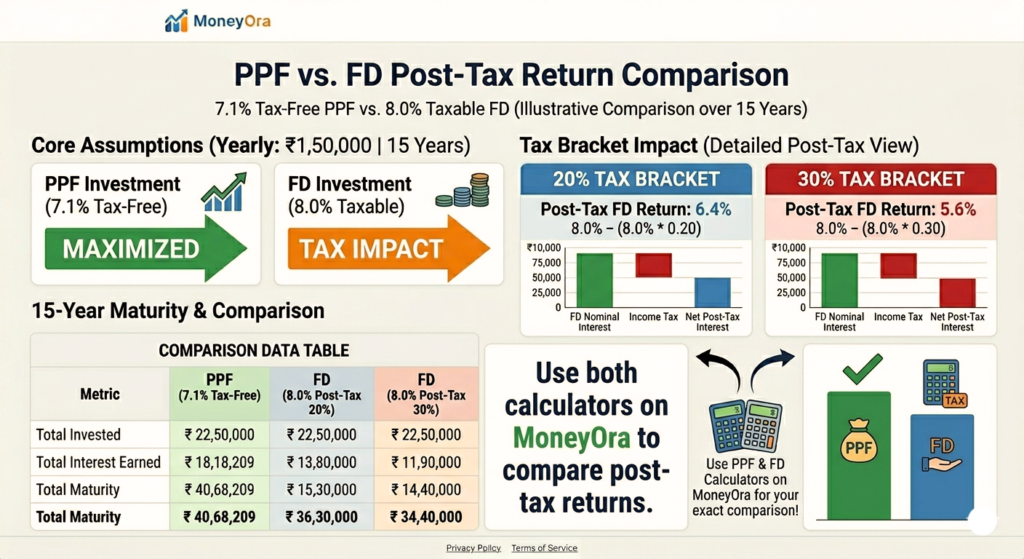

- You compare against other instruments. PPF at 7.1% tax-free is often more valuable than an FD at 7.5% that’s fully taxable. The calculator gives you the gross PPF number to compare against our FD Calculator on a like-for-like basis.

How PPF Interest Is Calculated

PPF interest is compounded annually. The formula is straightforward:

A = P × (1 + r)n

- A = Maturity amount

- P = Yearly deposit

- r = Annual interest rate (7.1% = 0.071)

- n = Number of years

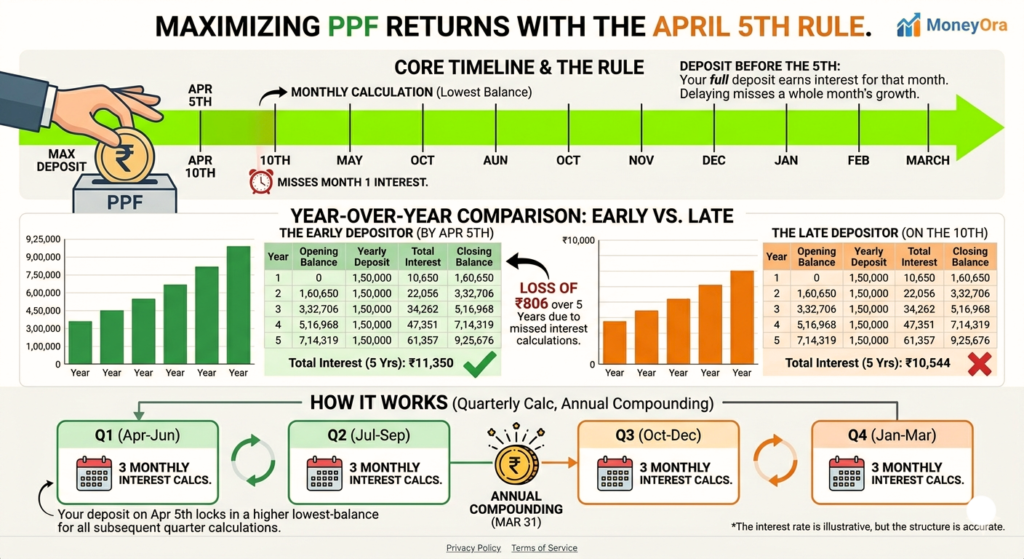

There’s one detail worth knowing: PPF interest is calculated on the minimum balance between the 5th and the last day of each month. This is why financial advisors consistently recommend depositing before the 5th of April each year — the full year’s deposit earns interest for the entire year rather than from the deposit date.

Worked Example

Yearly deposit: ₹1,00,000 | Rate: 7.1% | Tenure: 15 years

Year 1: ₹1,00,000 × 1.071 = ₹1,07,100

Year 2: (₹1,07,100 + ₹1,00,000) × 1.071 = ₹2,21,804

… and so on for 15 years.

Final maturity value at year 15: approximately ₹27.1 lakh

Total deposited: ₹15 lakh | Interest earned: ₹12.1 lakh

That’s ₹12.1 lakh earned on top of ₹15 lakh invested — all of it tax-free. Use the PPF Calculator above to try different yearly amounts and tenures.

PPF Tax Benefits – The EEE Advantage

PPF is one of the very few investments in India that qualifies for EEE tax treatment. Here’s what that means in practice:

- Exempt on investment (E1): Deposits up to ₹1.5 lakh per year are deductible under Section 80C of the Income Tax Act. At a 30% tax slab, that’s up to ₹45,000 saved in tax per year.

- Exempt on interest (E2): The interest earned on your PPF balance every year is completely tax-free. No TDS, no ITR declaration needed for this interest.

- Exempt on maturity (E3): The full maturity amount — principal plus all accumulated interest — is tax-free when you withdraw at maturity.

To understand what your Section 80C deduction limit covers, check the Income Tax India portal’s Section 80C guide. PPF is one of 20+ instruments that qualify — but unlike ELSS or insurance products, there’s no market risk.

How to Use MoneyOra’s Free PPF Calculator

Two inputs. That’s it.

- Yearly investment: Enter how much you plan to deposit each financial year — from ₹500 to ₹1,50,000. The maximum limit is set by the government; you can’t deposit more than ₹1.5 lakh in a single PPF account per year.

- Tenure: Enter the number of years — minimum 15, maximum 50 (accounting for extensions). After the initial 15-year lock-in, you can extend in 5-year blocks. The calculator accepts any value from 15 to 50.

The interest rate (7.1% p.a.) is pre-filled and locked — it’s set by the Government of India and reviewed quarterly. You don’t enter it manually.

The PPF Calculator instantly shows:

- Total maturity value

- Total amount invested

- Total interest earned

- Effective yield percentage

- Estimated tax saved at 30% slab

- Year-by-year growth bar chart

- Full year-wise schedule with opening balance, deposit, interest, and closing balance

Year 15 is marked with a lock icon in the schedule — it’s the first maturity point. Any year beyond that represents an extension block.

PPF vs Other Tax-Saving Investments

Section 80C gives you a ₹1.5 lakh deduction limit — PPF competes with ELSS, NSC, tax-saving FDs, and insurance premiums for that same limit. Here’s how they compare:

| Instrument | Returns | Lock-in | Risk | Tax on Returns |

|---|---|---|---|---|

| PPF | 7.1% p.a. | 15 years | None | Fully tax-free (EEE) |

| ELSS Mutual Fund | 10%–14% (market-linked) | 3 years | High | LTCG above ₹1L taxable |

| NSC | 7.7% p.a. | 5 years | None | Interest taxable |

| Tax-saving FD | 6.5%–7.5% p.a. | 5 years | None | Interest fully taxable |

| NPS (Tier I) | 8%–10% (market-linked) | Until age 60 | Low–Medium | 60% tax-free on exit |

| Sukanya Samriddhi | 8.2% p.a. | 21 years | None | Fully tax-free (EEE) |

PPF isn’t the highest-return option and the 15-year lock-in is genuinely long. But for investors who want zero risk, guaranteed government-backed returns, and complete tax exemption on both interest and maturity, nothing else in this list matches all three at once.

If you’re evaluating NPS alongside PPF, our NPS Calculator shows projected returns and the tax benefit breakdown for both Tier I and Tier II accounts.

Getting the Most Out of Your PPF Account

- Deposit before 5th April every year. PPF interest is calculated on the minimum balance between the 5th and the last day of each month. If you deposit on April 6th instead of April 4th, you lose one full month of interest on that year’s deposit. On ₹1.5 lakh, that’s roughly ₹900 lost for missing a date by two days. Set a reminder.

- Max out the ₹1.5 lakh limit if you can. The tax-free compounding over 15+ years is most powerful at the maximum deposit. Use the PPF Calculator to see the difference between ₹50,000/year and ₹1,50,000/year over 25 years — it’s not proportional, it’s significantly more due to compounding.

- Consider extending rather than withdrawing at 15 years. At maturity (year 15), you have three options: full withdrawal, extension with deposits, or extension without deposits. If you don’t need the money, extending with continued deposits for 5 more years adds disproportionately more interest than the first 15 years — because the base is now larger.

- Partial withdrawal is allowed from year 7. You can withdraw up to 50% of the balance at the end of the 4th year preceding the withdrawal year. This makes PPF more liquid than most people think — it’s not completely locked away for 15 years.

- Loans against PPF are available. Between years 3 and 6, you can take a loan against your PPF balance at a relatively low interest rate (currently 1% above the PPF rate). It’s a useful emergency option that doesn’t require breaking the account.

- Open a PPF account for your children too. You can open a PPF account in a minor child’s name (parent as guardian). Deposits in a child’s PPF account count towards the parent’s 80C limit, and the child has a 15-year account starting early — giving compounding more time to work.

Other calculators on MoneyOra useful for long-term investment planning:

- NPS Calculator — National Pension Scheme projections with tax breakdown

- FD Calculator — compare fixed deposit returns with PPF

- RD Calculator — recurring deposit maturity calculator

- EMI Calculator — loan EMI planning alongside your investments

Before You Open That PPF Account

PPF works best when you treat it as a fixed, non-negotiable annual commitment — not something you top up when you happen to have spare cash. The compounding advantage over 15–25 years is real, but only if you’re consistent. Missing a year or depositing late in the year quietly erodes the returns.

Use the PPF Calculator above to model your specific numbers — try ₹50,000/year vs ₹1,50,000/year over 15 and 25 years. The difference is larger than most people expect.

And if you’re comparing PPF against a tax-saving FD or NPS, use the FD Calculator and NPS Calculator on MoneyOra to see the post-tax difference before you decide.

FAQs

The current PPF interest rate is 7.1% per annum, compounded annually.

This rate has been in effect since April 2020.

The government reviews it every quarter, but it has remained unchanged for several years.

MoneyOra's PPF Calculator uses this rate and updates it whenever a revision is announced.

The minimum yearly deposit to keep a PPF account active is ₹500.

The maximum limit is ₹1,50,000 per financial year per account.

You can make up to 12 deposits in a year.

The total amount across all deposits cannot exceed ₹1.5 lakh.

Deposits above this limit do not earn interest and are returned without benefits.

Full premature closure is allowed only in specific situations.

These include serious illness, higher education expenses, or change in residency status.

Partial withdrawals are allowed from the 7th financial year onwards.

You can withdraw up to 50% of the balance.

The balance is calculated based on the 4th year preceding withdrawal.

You can also take a loan against PPF between years 3 and 6.

At maturity, you have three options.

You can withdraw the full amount.

You can extend the account for 5 years without deposits.

Or you can extend with deposits up to ₹1.5 lakh per year.

Extensions can be repeated in 5-year blocks.

Use the PPF Calculator to compare long-term scenarios.

No. PPF follows EEE (Exempt-Exempt-Exempt) tax treatment.

Your deposits qualify for deduction under Section 80C.

The interest earned is completely tax-free.

The maturity amount is also tax-free.

No TDS is deducted, and it does not need separate declaration in ITR.

Interest is calculated on the lowest balance between the 5th and last day of each month.

It is credited annually on March 31.

Depositing before the 5th of each month helps maximize returns.

A deposit after the 5th misses interest for that month.

MoneyOra's PPF Calculator uses annual compounding for estimation.

PPF accounts can be opened in nationalised banks like SBI, PNB, and Bank of Baroda.

They are also available in private banks like ICICI, Axis, and HDFC.

All post offices in India offer PPF accounts.

Many banks allow online account opening.

You can hold only one PPF account in your name.

No. NRIs cannot open a new PPF account.

Existing accounts can continue until maturity.

However, they cannot be extended beyond 15 years.

The account continues earning 7.1% interest.

The maturity amount remains tax-free.